|

市场调查报告书

商品编码

1639474

云端安全软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Cloud Security Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

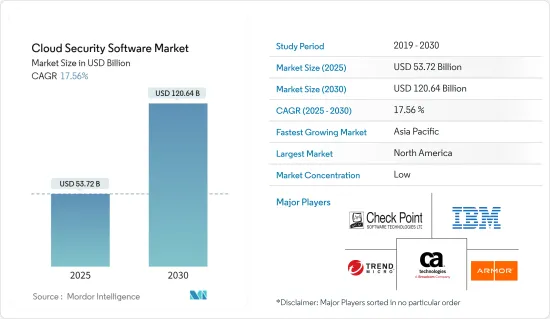

预计2025年云端安全软体市场规模为537.2亿美元,预计到2030年将达到1,206.4亿美元,预测期内(2025-2030年)的复合年增长率为17.56%。

主要亮点

- 不断增长的资料量和技术复杂性使得企业越来越依赖云端服务进行营运和资料管理。云端服务的日益普及直接影响了对云端安全解决方案的需求。

- 云端技术和云端基础的资源可以帮助减轻致命网路安全威胁的出现。云端安全需要一系列对于应用程式、基础架构和资料的安全至关重要的策略和控制。资料遗失、外洩和不安全的应用程式介面(API)等威胁在云端处理平台上频繁发生。网路环境和相关技术的演变为新的威胁铺平了道路。网路攻击已变得具有高度的标靶化、持续性和技术先进性。

- BFSI 产业是关键基础设施领域之一,由于其庞大的基本客群和财务资讯受到威胁,该产业面临多次资料外洩和网路攻击。网路犯罪分子利用大量有害的网路攻击来破坏金融业,因为它提供了相对低风险、易于检测的优势和高利润的商业模式。这些攻击的威胁包括木马、恶意软体、ATM 恶意软体、勒索软体、行动银行恶意软体、资料外洩、组织入侵、资料窃取和财务外洩。

- 安全解决方案供应商正在积极寻求与其他託管安全服务提供者合作。例如,2022年10月,Google Cloud宣布对其可信任云端生态系统进行重大扩展。与 20 多个合作伙伴的新整合重点是实现更好的资料主权、支援零信任模型、统一身分管理以及提高全球和企业的端点安全性。

- 然而,与传统基础设施的各种复杂整合等因素可能会在整个预测期内限制整体市场的成长。

- 新冠疫情爆发,引发云端安全市场激增。随着各国在封锁期间越来越多企业透过实施远端工作存取来适应新冠疫情,云端基础的服务和工具将成为后疫情时代的主角。疫情期间,云端基础服务的使用增加,导致数百万人在陌生且不太安全的环境中工作,成为网路攻击的热点。因此,云端安全解决方案在这次疫情期间发挥着至关重要的作用,预计未来将继续普及。

云端安全软体市场趋势

医疗保健产业将经历显着成长

- 医疗保健组织正变得越来越分散,拥有远距临床办公室、临床实验站点、復健设施、外包、异地工作人员等,每个办公室和个人都透过各种设备存取应用程式和资源。无缝访问。医疗保健组织正在认识到云端技术提供的好处,包括提高系统和应用程式的灵活性、扩充性和可用性。

- 随着医疗保健的发展,医院存储了电子健康记录和其他患者详细资讯,资料的潜在漏洞也随之增加,因此网路安全实施成为重中之重。

- 利用人工智慧、资料主导的安全监控和行为分析可以使云端基础的安全性更加有效。例如,微软的统一智慧安全图每天收集数十亿个资料点,并使用机器学习和人工智慧来分析和识别不断演变的网路安全攻击。

- 2022年4月,美国食品药物管理局发布了医疗设备网路安全指导草案《医疗设备网路安全、上市前提交内容和品质系统注意事项》。建议的指南强调在整个产品生命週期中保护医疗设备。这些建议将使上市前审查流程更加高效,并有助于确保所销售的医疗设备能够充分抵御网路安全威胁。

- 根据2023年5月医疗保健资料外泄报告,当月大多数资料外泄都是骇客攻击导致的IT事件,其中许多是勒索软体攻击、资料窃取或勒索企图。骇客攻击和 IT 事件占当月资料外洩事件的约 81.33%,这些事件占所有外洩记录的约 99.54%。这些事件导致约18,956,101人的受保护健康资讯外洩或窃取。资料外洩的平均规模为 310,756,中位数为 3,833。

亚太地区将经历最高成长

- 随着亚太地区数位转型的范围和速度随着各种物联网设备的使用增加而增加,目前的网路基础设施越来越容易受到网路攻击。近年来,社群媒体、网路和行动装置的使用呈指数级增长,促进了该地区网路安全的强劲发展。预计这将在整个预测期内推动该地区的市场成长机会。

- 此外,该地区各国政府正在製定新的网路安全法,以减轻网路钓鱼、恶意软体和其他网路安全威胁的影响。例如,韩国资讯通信技术部宣布,计划在2023年投资6,700亿韩元(6.07亿美元),以加强该国的网路安全能力,以应对日益增加的新数位威胁。该国计划与主要的云端运算和资料中心公司合作,开发能够透过即时收集威胁资讯快速应对网路安全威胁的基础设施。

- 近期,中国多次对印度电网进行攻击。 2022年4月,印度电力部门遭到骇客的长期攻击。该组织主要使用 Shadowpad垫片,据信该病毒是由中国国家安全部承包商开发的。

- 此外,技术进步也正在增加中国连网设备的数量。它是全球重要的物联网(IoT)市场。此外,5G和支援5G的设备将大大提高设备互联互通性。由于连网设备整体适应性的增强,这将直接增加市场对安全产品的需求。此外,网站可能更容易被第三方操纵或欺骗,与网站通讯的使用者的敏感资料可能更容易被外国情报机构截获。

- 2023 年 7 月,专注于云端运算和网路安全的IT基础设施解决方案供应商深信服科技与泰国云端安全和保全服务供应商 Cloudsec Asia 宣布建立业务合作伙伴关係,以开发新的云端服务供应商,主要用于网路威胁侦测。深信服科技与Cloudsec Asia的合作旨在满足企业对有效网路威胁管理日益增长的需求。两家公司的综合专业知识将使组织能够主动缓解和侦测网路威胁,同时克服与管理网路安全相关的挑战,包括时间限制、资源有限和技术复杂性。

云端安全软体产业概况

由于多年来网路攻击不断增加,云端安全软体市场变得分散。企业对储存在云端的资料的认识越来越深刻,也越来越谨慎。因此,NortonLifeLock(Broadcom Inc.)、CA Technologies(Broadcom Inc.)、Microsoft Corporation 和 Armor Defense Inc. 等公司都推出了产品。

Uptycs 将于 2023 年 4 月推出,提供第一个整合的 CNAPP 和 XDR 平台,从 Okta 和 Azure Active Directory 收集和分析 GitHub审核日誌和用户身份信息,以帮助开发人员将程式码移入和移出存储库并投入生产。结果是一个“警报系统”,使安全团队能够在威胁行为者访问云端的宝库——资料和服务之前识别并阻止他们。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提和结果

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 产业影响及復苏评估

第五章 市场动态

- 市场驱动因素

- 数位转型正在实施

- 透过行动装置和其他装置使用数位服务的情况增加

- 市场挑战

- 与传统基础设施的复杂集成

- 网路安全相关实践的关键创新与进步分析

- 领先的行业标准和框架

- 关键使用案例

第六章 市场细分

- 按软体

- 云端 IAM

- Web 和电子邮件安全

- SIEM

- CASB

- 脆弱性和风险管理

- 其他软体

- 按组织规模

- 中小企业

- 大型企业

- 按最终用户

- 资讯科技和电信

- BFSI

- 零售和消费品

- 卫生保健

- 製造业

- 政府

- 其他最终用户

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 双子座

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争格局

- 公司简介

- IBM Corporation

- Symantec(Broadcom)

- Palo Alto Networks

- Cisco

- McAfee

- HPE

- Checkpoint

- Zscaler

- Fortinet

- Sophos

第八章投资分析

第九章 市场机会与未来趋势

The Cloud Security Software Market size is estimated at USD 53.72 billion in 2025, and is expected to reach USD 120.64 billion by 2030, at a CAGR of 17.56% during the forecast period (2025-2030).

Key Highlights

- The growing data generation and increasing complexity of technologies have resulted in a heavy dependence of organizations on cloud services for operations and data management. This growth in the adoption of cloud services directly impacts the demand for cloud security solutions.

- Cloud technology and cloud-based resources help mitigate the rise in lethal cyber-security threats. Cloud security requires a set of policies and controls vital for the security of applications, infrastructure, and data. Threats, such as data loss, breaches, and insecure application programming interfaces (API), are frequent on the cloud computing platform. The evolution of the cyber environment and related technologies paved the way for new threats. Cyber-attacks are highly targeted, persistent, and technologically advanced.

- The BFSI industry is one of the critical infrastructure segments that face multiple data breaches and cyber-attacks, owing to the massive customer base that the sector serves and the financial information that is at stake. Cybercriminals are leveraging an abundance of harmful cyberattacks to immobilize the financial industry since it is a highly lucrative operating model with the added benefit of relatively low risk and detectability. These attacks' threat landscape ranges from Trojans, malware, ATM malware, ransomware, mobile banking malware, data breaches, institutional invasion, data thefts, fiscal breaches, etc.

- Vendors offering security solutions are actively involved in collaborating with other managed security service providers. For instance, in October 2022, Google Cloud declared a significant extension of its trusted cloud ecosystem. It highlighted new integrations and offerings with more than twenty partners focused on enabling more excellent data sovereignty controls, assisting Zero Trust models, unifying identity management, and improvising endpoint security for global businesses.

- However, factors like integrating various complexities with legacy infrastructure could limit the market's overall growth throughout the forecast period.

- Due to the outbreak of COVID-19, the cloud security market grew significantly. It was expected to witness massive growth during the post-COVID-19 period as cloud-based services and tools were increasingly adapted due to organizations deploying remote work access amid lockdowns in different countries. The rise in the usage of cloud-based services during this pandemic became a hotspot for cyberattacks as millions worked in unfamiliar, less secure circumstances. Thus, a cloud security solution played a vital role during this pandemic and is expected to witness a surge.

Cloud Security Software Market Trends

Healthcare Sector to Witness the Significant Growth

- Healthcare organizations have become more distributed, owing to remote clinical offices, trial sites, rehab facilities, outsourcing, and off-site workers, leading each office and individual to require unique yet seamless access to applications and resources via various devices. Healthcare organizations recognize the benefits provided by cloud technology, such as greater flexibility, scalability, and availability of systems and applications.

- With advancements in healthcare, such as electronic medical records and other patient details being registered with the respective hospitals, the potential vulnerability for the data has been increasing, owing to which the implementation of network security has been of primary importance.

- Using AI, data-driven security monitoring, and behavioral analytics makes cloud-based security more effective. For instance, Microsoft's integrated intelligent security graph collects billions of data points daily and uses machine learning and AI to analyze and identify evolving cybersecurity attacks.

- In April 2022, the U.S. Food and Drug Administration published a draft guidance, Cybersecurity in Medical Devices, Content of Premarket Submissions and Quality System Considerations, regarding medical device cybersecurity. The draft guidance emphasizes safeguarding medical devices throughout a product's life cycle. These recommendations can enable an efficient premarket review process and help assure that marketed medical devices are sufficiently resilient to cybersecurity threats.

- According to May 2023 Healthcare Data Breach Report, most of the month's data breaches were hacking IT incidents, many of which were ransomware attacks and data theft or extortion attempts. Around 81.33% of the month's data breaches were hacking, and IT incidents, and those incidents accounted for approximately 99.54% of all breached records. The protected health information of about 18,956,101 individuals was exposed or stolen in those incidents. The average data breach size was 310,756 records, and the median breach size was 3,833.

The Asia-Pacific to Witness the Highest Growth

- Due to the rise in the usage of various IoT devices and the increasing scope and speed of digital transformation in the Asia-Pacific region, the current network infrastructure is becoming widely exposed to cyberattacks. Social media, internet, and mobile users have all seen a drastic rise in recent years, contributing to the region's strong growth in cybersecurity. This is expected to fuel the market growth opportunity within the region throughout the forecast period.

- Moreover, the region's various governments are imposing new cybersecurity laws to reduce the impact of cyber phishing, malware, and other cybersecurity threats. For instance, South Korea's ICT ministry announced the plan to spend KRW 670 billion (USD 607 million) by 2023 to bolster the country's cybersecurity capabilities to respond to growing new digital threats. The country plans to develop infrastructure to quickly respond to cybersecurity threats by collaborating with major cloud and data center companies to collect threat information in real time, compared to the current system that relies on individual reports.

- Recently, there have been multiple attacks on Indian power grids by China. In April 2022, India's power sector was targeted by hackers in a long-term operation. The group primarily utilized the trojan ShadowPad, which is believed to have been developed by the contractors for China's Ministry of State Security.

- Also, due to the rise in technological advancements, there is an increase in the number of connected devices in China. It is a significant Internet of Things (IoT) market globally. Furthermore, 5G and 5G-enabled devices exponentially increase the devices' interconnectivity. As a result, it increases the overall adaptability of the connected devices, thereby directly augmenting the need for security products in the market. Moreover, the websites are thereby prone to be manipulated and impersonated by third parties, and sensitive user data communicated with the website can be intercepted more easily by foreign intelligence agencies.

- In July 2023, Sangfor Technologies Co., Ltd., a provider of IT infrastructure solutions specializing in Cloud Computing & Network Security, and Cloudsec Asia Co., Ltd., a provider of cloud security and cyber security services in Thailand, formed a strategic partnership primarily to deliver comprehensive managed services for cyber threat detection. The collaboration between Sangfor Technologies and Cloudsec Asia targets to address the rising demand for effective cyber threat management within business organizations. By leveraging their expertise, the companies would deliver a managed service that empowers organizations to proactively mitigate and detect cyber threats while overcoming challenges like time constraints, limited resources, and technological complexities associated with cybersecurity management.

Cloud Security Software Industry Overview

The market for cloud security software is fragmented due to the rise in cyber-attacks over the years. Enterprises have become more aware and careful regarding their data stored in the cloud. Thus, they offer offerings from NortonLifeLock Inc. (Broadcom Inc.), CA Technologies (Broadcom Inc.), Microsoft Corporation, Armor Defense Inc., etc.

In April 2023, Uptycs, the provider of the first unified CNAPP and XDR platform, declared the ability to collect and analyze GitHub audit logs and user identity information from Okta and Azure Active Directory to reveal suspicious behavior as the developer moves code in and out of repositories and into production. The result is an "early warning system" that enables the security teams to identify and stop threat actors before they can access the cloud's crown jewel data and services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Deliverables

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of the Impact and Recovery from COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Digital Transformation Practices

- 5.1.2 Growing Use of Digital Services Through Mobile and Other Devices

- 5.2 Market Challenges

- 5.2.1 Integration Complexities with Legacy Infrastructure

- 5.3 Analysis of Key Innovations and Advancements in Cybersecurity Related Practices

- 5.4 Key Industry Standards & Frameworks

- 5.5 Key Use Cases

6 MARKET SEGMENTATION

- 6.1 By Software

- 6.1.1 Cloud IAM

- 6.1.2 Web and Email Security

- 6.1.3 SIEM

- 6.1.4 CASB

- 6.1.5 Vulnerability and Risk Management

- 6.1.6 Other Software

- 6.2 By Organization Size

- 6.2.1 SME

- 6.2.2 Large Enterprises

- 6.3 By End User

- 6.3.1 IT & Telecom

- 6.3.2 BFSI

- 6.3.3 Retail & Consumer Goods

- 6.3.4 Healthcare

- 6.3.5 Manufacturing

- 6.3.6 Government

- 6.3.7 Other end-users

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Gemany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Symantec (Broadcom)

- 7.1.3 Palo Alto Networks

- 7.1.4 Cisco

- 7.1.5 McAfee

- 7.1.6 HPE

- 7.1.7 Checkpoint

- 7.1.8 Zscaler

- 7.1.9 Fortinet

- 7.1.10 Sophos

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年云端安全态势管理全球市场报告2025年全球云端安全市场报告

2025年云端安全态势管理全球市场报告2025年全球云端安全市场报告 云端安全市场:按产品供应、服务模式、安全类型、组织规模、部署类型和产业 - 2025-2030 年全球预测云端安全态势管理市场(按组件、垂直产业、部署模型和组织规模)—2025 年至 2030 年全球预测混合事件软体市场:按组件、事件类型、部署模式、最终用户、组织规模和定价模式- 2025-2030 年全球预测

云端安全市场:按产品供应、服务模式、安全类型、组织规模、部署类型和产业 - 2025-2030 年全球预测云端安全态势管理市场(按组件、垂直产业、部署模型和组织规模)—2025 年至 2030 年全球预测混合事件软体市场:按组件、事件类型、部署模式、最终用户、组织规模和定价模式- 2025-2030 年全球预测 2025 年至 2033 年云端安全软体市场报告(按类型、部署、最终用户、垂直产业和地区)

2025 年至 2033 年云端安全软体市场报告(按类型、部署、最终用户、垂直产业和地区) 全球云端安全态势管理市场

全球云端安全态势管理市场 2025-2029年全球人工智慧模型託管市场

2025-2029年全球人工智慧模型託管市场 云端安全市场:2025-2030 年预测云端安全态势管理市场规模、份额、趋势分析报告:按组件、云端服务、企业规模、云端、产业垂直、地区、细分预测,2025 年至 2030 年

云端安全市场:2025-2030 年预测云端安全态势管理市场规模、份额、趋势分析报告:按组件、云端服务、企业规模、云端、产业垂直、地区、细分预测,2025 年至 2030 年