|

市场调查报告书

商品编码

1639496

工业控制系统 -市场占有率分析、产业趋势/统计、成长预测 (2025-2030)Industrial Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

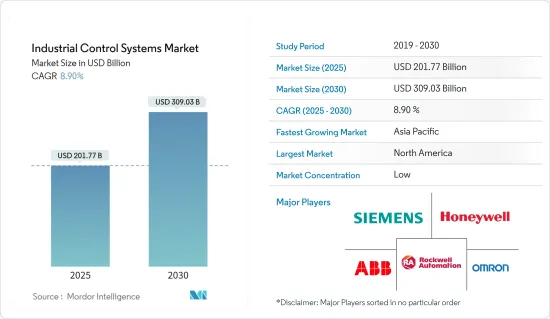

预计2025年工业控制系统市场规模为2,017.7亿美元,预估至2030年将达3,090.3亿美元,预测期间(2025-2030年)复合年增长率为8.9%。

不断上升的人事费用和製造商在紧迫的期限内面临的巨大压力正在推动工厂越来越多地采用自动化。工厂自动化正在推动 ICS 市场的发展。

主要亮点

- 连接工业设备和机械并获取即时资料在 SCADA、HMI、PLC 系统和提供可视化的软体的实施中发挥关键作用。

- 此外,系统的效率、可靠性和速度最大限度地减少了与人为错误相关的品管问题。此外,製造业大规模生产的需求正在推动对工业控制设备的需求,以满足不断增长的人口的需求。

- 此外,德国工业 4.0 和法国工业计划等政府措施可能会推动对 IIoT 解决方案的需求,并在未来增加对 ICS 安全解决方案和服务的需求。严重的网路灾难可能导致重大的财务损失、品牌损害、消费者信心丧失、智慧财产权被盗、安全问题甚至死亡。因此,ICS 可能需要安全机制来审核并确保合规性,以保护生态系统免受财务、营运和人员损失。

- 由于连网型设备和感测器的高采用率以及 M2M通讯的启用,製造业中产生的资料点正在迅速增加。根据 Zebra 最新的製造愿景报告,预计到 2022 年,基于物联网和 RFID 的智慧资产追踪解决方案将取代基于电子表格的传统方法。

- 这场大流行迫使组织遵守严格的要求,同时确保员工和客户的安全。因此,对自动化解决方案的需求激增。在可预见的未来,这可能会被视为一个显着趋势。随着世界继续对抗新冠肺炎 (COVID-19) 大流行的蔓延,机器人技术支援的工厂自动化在保障人员安全和处理最终用户所需的物资方面发挥关键作用。

工业控制系统市场趋势

工业控制系统广泛应用的食品饮料领域

- 由于经济成长和可支配收入,食品饮料行业的需求逐年增加。人口成长也对该产业做出了贡献。

- 此外,随着购买力的增加和生活方式的改变,对加工产品的需求也增加。这迫使食品製造商实施自动化并提高加工率以满足消费者的需求。此外,电脑科技的快速发展、消费者偏好的动态变化以及监管机构正在增加对食品品质和安全的需求。这就是食品业越来越多地采用自动化系统的原因。

- 2022年6月,百事印度公司宣布追加投资1,860万印度卢比,扩建位于北方邦马图拉科希卡兰的食品製造厂,生产多力多滋玉米片品牌。百事公司对百事公司最大的待开发区食品製造厂(生产乐事洋芋片)的总投资达102.2亿卢比。

- 此外,这家宠物食品製造商还计划投资 1.45 亿美元用于其位于阿肯色州史密斯堡的加工工厂的扩建和设备升级。该计划于近日核准。该计划预计将于2022年完工,将进一步推动市场成长。

- 食品和饮料行业各个自动化阶段的成功整合可以在供应链中创造价值,并确保长期竞争和高效生产。因此,食品公司正在寻找透过流程自动化来提高可靠性、提高生产力、消除浪费和降低总成本的方法。这种自动化要求也增加了公司生产控制的重要性。

- 此外,製程自动化的采用减少了每个工厂所需的工人数量,同时为工业营运商提供了产品定价的灵活性。在预测期内,控制此类关键费用的需求不断增长可能会进一步促进工业製程自动化市场的成长。

北美市场占据主导地位

- 北美正处于第四次工业革命的边缘。产生的资料在生产中大规模利用,将资料与整个供应链中的各种製造系统整合。

- 该地区也是世界上最大的汽车市场之一,拥有超过 13 家主要汽车製造商。汽车製造是该地区製造业最大的收益来源之一。由于汽车行业大量采用工业控制系统和自动化技术,该地区提供了巨大的市场成长机会。

- 在该国运营的几家主要供应商已经宣布了新的更新,以帮助智慧工厂随着工业控制系统的发展而发展。这种技术进步显示该地区所研究市场的成长。

- 此外,政府的支持措施和具有竞争力的天然气价格使美国和加拿大的化学公司能够建造、扩大、自动化和控制工厂。因此,北美地区工业控制设备的成长预计也将在预测期内进一步推动调查市场。

- 2022年8月,通用汽车签署了三份电动车电池材料采购协议,这可以帮助该公司实现年产100万辆电动车的目标。根据与 LG Chem、POSCO Chemical 和 Liventwill 签订的多年协议,通用汽车将供应包括锂、镍、钴和活性阴极材料 (CAM) 在内的关键材料。该国汽车产业的扩张可能会进一步创造对 PLC 的巨大需求。

- 该国是最大的原油生产国之一,也是石油和天然气行业的领先参与企业。例如,根据 EIA 的数据,到 2030 年,该地区的产量预计将达到 3 兆英热单位。德克萨斯州占全国原油产量的大部分,预计对生产设备有庞大的需求。

工业控制系统产业概况

工业控制系统市场分散。每个参与企业都专注于研究和开发活动,以获得竞争优势。这些主要企业在创新、定价和服务的基础上竞争。向新兴市场扩张正在帮助现有的主要企业扩大销售网络。 GE Digital、西门子股份公司、施耐德电机股份公司、SAP、ABB 集团、发那科、霍尼韦尔国际公司

- 2022年9月-横河电机公司宣布并报告了OpreX电磁流量计CA系列。 OpreXField Instruments 系列发布了新产品系列来取代 ADMAG CA 系列。此新产品系列包括电容式电磁式流量计,可透过测量管测量导电流体的流量,而无需流体接触设备的电极。该产品的主要目标市场是化学品、纸浆和造纸、采矿、食品和饮料以及用水和污水处理。

- 2022 年 8 月 - 欧姆龙宣布推出 i-资料管理解决方案服务实施 (i-DMP)。这种以资料为中心的解决方案使客户能够透过简化以前不用于工厂车间改进的不同类型资料的整合来及时解决问题。 i-DMP 透过根据需要在边缘区域即时收集和储存分散在製造现场的资料(例如现有系统和 PLC)来执行集中资料管理。连接到各种网路、关联式资料库(RDB) 和工厂自动化 (FA) 设备。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 评估主要宏观经济趋势的影响

第五章市场动态

- 市场驱动因素

- 工业安全技术的进步

- 製造业量产需求

- 市场问题

- 缺乏技术纯熟劳工

第六章 市场细分

- 依操作技术

- 监控和资料采集(SCADA)

- 集散控制系统(DCS)

- 可程式逻辑控制器(PLC)

- 智慧电子设备 (IED)

- 人机介面 (HMI)

- 其他系统

- 透过软体

- 资产绩效管理(APM)

- 产品生命週期管理 (PLM)

- 製造执行系统(MES)

- 企业资源规划(ERP)

- 按最终用户产业

- 石油和天然气

- 化学/石化

- 电力/公共产业

- 饮食

- 汽车/交通

- 生命科学

- 用水和污水

- 金属/矿业

- 纸浆/纸

- 电子/半导体

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Siemens AG

- ABB Automation Company

- Omron Corporation

- Honeywell International Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Yokogawa Electric Corporation

- GLC Controls Inc.

- Mitsubishi Electric Corporation

第八章投资分析

第9章市场的未来

The Industrial Control Systems Market size is estimated at USD 201.77 billion in 2025, and is expected to reach USD 309.03 billion by 2030, at a CAGR of 8.9% during the forecast period (2025-2030).

The rising cost of labor and the immense pressure on manufacturers to meet strict deadlines are resulting in the increased deployment of automation in factories. The automation of factories has fueled the market for ICS.

Key Highlights

- Connecting the industrial equipment and machinery and obtaining real-time data have played a key role in the adoption of SCADA, HMI, PLC systems, and software that offer visualization, thus, enabling reducing the faults in the product, reducing downtime, scheduling maintenance, and switching from being in the reactive state to predictive and prescriptive stages for decision-making.

- In addition, the quality control issue involved with human error is minimized, owing to the systems' efficiency, reliability, and faster work rate. Moreover, the demand for mass production in manufacturing industries fuels the need for industrial controls to cater to the demands of growing population.

- Moreover, government efforts such as Germany's Industry 4.0 and France's industrial plan are likely to drive demand for IIoT solutions, which may, in turn, enhance demand for ICS security solutions and services in the future. A serious cyber catastrophe may result in significant financial losses, brand damage, consumer trust loss, intellectual property theft, safety concerns, and even death. As a result, to protect its ecosystem from any financial, operational, or human losses, ICS may need security mechanisms to audit and assure compliance.

- Due to the high rate of adoption of connected devices and sensors and the enabling of M2M communication, there has been a surge in the data points generated in the manufacturing industry. According to Zebra's latest manufacturing vision report, IoT and RFID-based smart asset tracking solutions are expected to overtake traditional, spreadsheet-based methods by 2022.

- The pandemic's impact has forced organizations to adhere to strict requirements while ensuring their employees' and customers' safety. As a result, the need for automated solutions witnessed a sudden spike. This could be observed as a notable trend in the foreseeable future. As the world continues to fight the spread of the COVID-19 pandemic, factory automation with robotics plays a crucial role in helping safeguard people and processing the supplies needed by the end user.

Industrial Control Systems Market Trends

Food and Beverage Sector to Widely Use Industrial Control Systems

- The demand for the food and beverage industry is growing yearly because of the economy's growth and disposable incomes. The increasing population is also contributing to this industry.

- Moreover, the demand for processed goods is increasing, with increased buying power and changing lifestyles. This has made it necessary for food manufacturers to implement automation to improve the processing rate to meet consumers' demands. Furthermore, the rapid development of computer technology, dynamic changes in consumers' preferences, and regulatory bodies have boosted the need for food quality and safety. This has resulted in the growing adoption of automated systems in the food industry.

- In June 2022, PepsiCo India announced an additional INR 1.86 crore investment in expanding its food manufacturing plant in Kosi Kalan, Mathura, Uttar Pradesh, to produce the Doritos cornflakes brand. PepsiCo's total investment in its largest Greenfield Foods manufacturing plant, which manufactures Lay's potato chips, will reach INR 1,022 crore.

- Moreover, the Pet food manufacturer plans to invest USD145 million in a 200,000 expansion and equipment upgrades at their FORT SMITH, AR processing facility. The project has recently received approval. The project is expected to be completed in 2022, further driving the market growth.

- Successful integration of different automation stages in the food and beverage industry leads to value-creation in the supply chain, which ensures a long-term competitive edge and efficient production. Hence, food companies are finding ways to improve reliability, increase productivity, reduce waste, and decrease total costs through process automation. This automation requirement also makes controls significant to a company's production.

- In addition, the adoption of process automation has also reduced the number of workers required per plant while providing flexibility in product pricing for industrial operators. Such a rising need for controlling significant expenses is likely to further proliferate the growth of the industrial process automation market during the forecast period.

North America to Dominate the Market

- North America is on the verge of the fourth industrial revolution. The data generated is being used on a large scale for production while integrating the data with various manufacturing systems throughout the supply chain.

- The region is also one of the largest automotive markets in the world and is home to over 13 major auto manufacturers. Automotive manufacturing has been one of the largest revenue generators, in the region, in the manufacturing sector. As the automotive industry accounts for the significant adoption of industrial control systems and automation technologies, the region offers a huge opportunity for market growth.

- Multiple major key vendors operating in the country are launching new updates to help in the growth of smart factories with developments in industrial control systems. Such technological advancement is indicative of the growth of the region in the studied market.

- Moreover, supporting government policies and competitively priced natural gases are enabling the US and Canadian chemical companies to build plants, expand, automate, and control their facilities. Hence, the growth of industrial controls in the North American region is also expected to further drive the market studied over the forecast period.

- General Motors signed three sourcing agreements for EV battery materials in August 2022, potentially aiding the automaker in achieving its objective of manufacturing one million EVs annually. The multi-year contracts with LG Chem, POSCO Chemical, and Liventwill supply GM with critical materials such as lithium, nickel, cobalt, and active cathode material (CAM). Such expansion in the automotive sector in the country may further create significant demand for PLCs.

- The country is one of the largest crude oil producers and a prominent oil and gas industry player. For instance, according to EIA, by 2030, the production is expected to reach 30.01 quadrillions Btu in the region. Texas produces the major share of crude oil in the country and is expected to generate significant demand for production equipment.

Industrial Control Systems Industry Overview

The industrial control system market is fragmented. The players are focusing on R&D activities to attain a competitive advantage. These key players compete based on innovation, pricing, and service. Expansion in the emerging market helps the established key players to extend their sales networks. GE Digital, Siemens AG, Schneider Electric AG, SAP, ABB Group, Fanuc, Honeywell International Inc., Bosch, and Cisco Systems are some companies that provide the industrial internet platform.

- Sep 2022 - The OpreXMagnetic Flowmeter CA Series has been released and reported by Yokogawa Electric Corporation. The OpreXField Instruments family is releasing this new product series to replace the ADMAG CA Series. This new line of products includes capacitance-type magnetic flowmeters, which can measure the flow of conductive fluids via a measurement tube without the fluids touching the device's electrodes. The product's main target markets will be chemicals, paper and pulp, mining, food and beverage, water, and sewerage.

- Aug 2022 - OMRON has unveiled i-Data-Managed Solution Service Implementation (i-DMP). This data-centric solution will enable the clients to solve their issues in a timely manner by simplifying the integration of various types of data, which was never intended for the purpose of improving factory floors. The i-DMP will gather and store data, as needed, dispersed throughout the manufacturing floor, such as those from existing systems and PLCs, in the edge region in real time for uniform data management. It is connected to various networks, relational databases (RDB), and factory automation (FA) devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Advancements in Industrial Safety Technology

- 5.1.2 Demand for Mass Production in Manufacturing Sector

- 5.2 Market Challenges

- 5.2.1 Lack of Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Operational Technology

- 6.1.1 Supervisory Control and Data Acquisition (SCADA)

- 6.1.2 Distributed Control System (DCS)

- 6.1.3 Programmable Logic Controller (PLC)

- 6.1.4 Intelligent Electronic Devices (IED)

- 6.1.5 Human Machine Interface (HMI)

- 6.1.6 Other Systems

- 6.2 By Software

- 6.2.1 Asset Performance Management (APM)

- 6.2.2 Product Lifecycle Management (PLM)

- 6.2.3 Manufacturing Execution System (MES)

- 6.2.4 Enterprise Resource Planning (ERP)

- 6.3 By End-user Industry

- 6.3.1 Oil & Gas

- 6.3.2 Chemical and Petrochemical

- 6.3.3 Power & Utilities

- 6.3.4 Food & Beverages

- 6.3.5 Automotive & Transportation

- 6.3.6 Life Sciences

- 6.3.7 Water & Wastewater

- 6.3.8 Metal & Mining

- 6.3.9 Pulp & Paper

- 6.3.10 Electronics/Semiconductor

- 6.3.11 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 ABB Automation Company

- 7.1.3 Omron Corporation

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automation Inc.

- 7.1.6 Schneider Electric SE

- 7.1.7 Emerson Electric Co.

- 7.1.8 Yokogawa Electric Corporation

- 7.1.9 GLC Controls Inc.

- 7.1.10 Mitsubishi Electric Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

工业自动化光达市场分析及2034年预测:类型、产品、服务、技术、组件、应用、流程、部署及最终用户

工业自动化光达市场分析及2034年预测:类型、产品、服务、技术、组件、应用、流程、部署及最终用户 2032 年工业控制系统网路安全市场预测:按组件、部署模型、安全类型、系统类型、应用和地区进行的全球分析

2032 年工业控制系统网路安全市场预测:按组件、部署模型、安全类型、系统类型、应用和地区进行的全球分析 工业控制系统 (ICS) 安全市场:全球按产品、解决方案、服务、安全类型、垂直产业和地区划分 - 预测至 2030 年

工业控制系统 (ICS) 安全市场:全球按产品、解决方案、服务、安全类型、垂直产业和地区划分 - 预测至 2030 年 工业自动化控制市场(2025-2029)

工业自动化控制市场(2025-2029) 工业控制系统市场规模、份额及成长分析(按组件、技术、最终用途和地区)- 产业预测(2025-2032)

工业控制系统市场规模、份额及成长分析(按组件、技术、最终用途和地区)- 产业预测(2025-2032) 2025年工业控制设备全球市场报告

2025年工业控制设备全球市场报告 工业控制和工厂自动化市场按产品类型、组件、自动化类型、应用和垂直产业划分-2025-2030 年全球预测生产管理系统市场按组件、业务功能、部署模式、组织规模和最终用户行业划分 - 2025-2030 年全球预测

工业控制和工厂自动化市场按产品类型、组件、自动化类型、应用和垂直产业划分-2025-2030 年全球预测生产管理系统市场按组件、业务功能、部署模式、组织规模和最终用户行业划分 - 2025-2030 年全球预测 工业檯面市场规模、份额及成长分析(按类型、应用和地区)-2025-2032 年产业预测2025 年工业控制与工厂自动化全球市场报告

工业檯面市场规模、份额及成长分析(按类型、应用和地区)-2025-2032 年产业预测2025 年工业控制与工厂自动化全球市场报告