|

市场调查报告书

商品编码

1639503

脲醛树脂:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Urea Formaldehyde Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

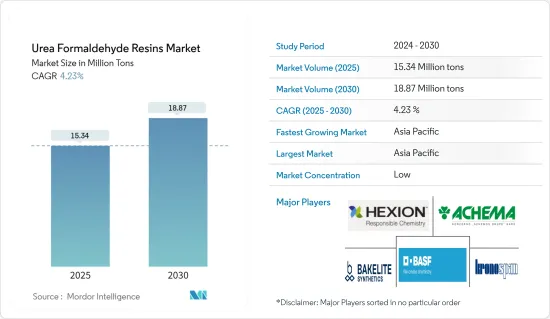

脲醛树脂市场规模预计2025年为1,534万吨,预计2030年将达到1,887万吨,预测期间(2025-2030年)复合年增长率为4.23%。

COVID-19的疫情对尿素甲醛市场产生了负面影响。全球封锁和严格的政府法规关闭了大多数生产基地,对它们造成了破坏。儘管如此,市场预计将在 2021 年復苏,并在未来几年大幅成长。

主要亮点

- 短期内,家具业对塑合板的需求增加以及对中密度纤维板(MDF)的需求增加预计将推动市场成长。

- 然而,与脲醛树脂相关的健康危害预计将阻碍市场成长。

- 汽车和电器产品对优质树脂的需求预计将为所研究的市场创造新的机会。

- 亚太地区主导全球市场,大部分消费来自中国和印度。

脲醛树脂市场趋势

建筑和施工领域预计将主导市场

- 建筑业高度依赖塑合板、胶合板和中密度纤维板等材料,是脲醛树脂市场成长的关键驱动力。

- 随着建设活动的活性化,这些建筑材料的需求和产量也将增加。脲醛在板材和胶合板中的广泛使用凸显了其重要性并推动了脲醛市场的整体成长。

- 牛津经济研究院预测,全球建筑产值将继续保持强劲成长势头,到 2037 年从超过 4.2 兆美元增至超过 13.9 兆美元。

- 亚太地区和北美的住宅建设正在蓬勃发展。在亚太地区,印度、中国、菲律宾、越南和印尼等国家则位居前列。同时,人口成长、移民增加和核心家庭趋势正在推动北美的住宅建设。

- 建筑业是韩国主要经济贡献者,也是外汇和出口收益的重要来源。韩国国内建筑市场的扩张主要得益于私人住宅的稳定成长。

- 政府还计划实施大规模再开发计划,到2025年将在首尔和其他城市提供83万住宅。该计画要求在首尔建造323,000套新住宅,在京畿道和仁川建造293,000套新住宅。釜山、大邱和大田等大城市也将受益于四年内建造的 22 万栋新住宅。

- 随着住宅市场的崛起,以中国和印度为首的亚太地区可能会引领全球住宅建设热潮。

- 占全球建筑投资20%的中国预计到2030年将在建筑上花费约13兆美元,凸显了铌市场的看涨前景。

- 印度政府意识到住房的重要性,正在加大力度建造住宅,旨在满足13亿人民的需求。

- 根据国家房地产开发公司(NAREDCO)的报告,2023年排名前七的城市将总合竣工435,000套公寓,预计2024年将大幅增加。为了进一步支持这一趋势,诺伊达着名的房地产开发商 County Group 今年将宣布三个雄心勃勃的住宅计划,超过 400 万平方英尺。

- 美国在美国的建筑业中占据主导地位,加拿大和墨西哥也进行了大量投资。根据美国人口普查局的数据,2023年美国新建住宅数量增加4.46%,从2022年的1,390,500套达到1,452,000套。此外,2023年该国年度建筑业价值达1.97兆美元,比2022年的1.84兆美元成长7%。

- 在加拿大,经济适用住房倡议(AHI)、加拿大新建筑计划 (NBCP) 和加拿大製造等政府倡议预计将显着加强建筑业。 2022 年 8 月,加拿大政府宣布对这些倡议进行超过 20 亿美元的重大投资,旨在全国开发约 17,000住宅,其中包括我开发的大量经济适用住宅。

- 鑑于这些发展,建筑业预计将在预测期内保持其市场主导地位。

亚太地区主导市场

- 以中国和印度为首的亚太地区主导全球市场。

- 中国作为世界最大的脲醛树脂生产国发挥着至关重要的作用。随着人口的成长,中国的农业部门正在不断发展,以满足日益增长的粮食需求。这种演变取决于肥料的性能和效率,从而推高了脲醛树脂的消耗。

- 中国是全球最大的建筑市场,占全球建筑投资的20%。据预测,到2030年,中国将在建筑领域投资约13兆美元,市场前景良好。住宅需求的成长将推动公共和私人住宅建设,高层建筑和酒店将显着增加。

- 为加速低成本住宅计划,香港住宅委员会宣布了一项计划,旨在到2030年提供301,000个公共住宅。

- 除了建筑之外,脲醛树脂在纤维板製造上也扮演着重要角色。这种纤维板用于汽车领域,形成仪表板和门壳等部件。中国工业协会(CAAM)最新公布的资料显示,2023年汽车产量将突破3,016万辆,与前一年同期比较增加11.6%。 2023年国内乘用车销量3,009万辆,与前一年同期比较成长12%。

- 印度汽车製造商协会(SIAM)公布的资料显示,2023财年汽车产量为458万辆,而2022财年产量为365万辆。 2023财年汽车产量比上年度增长约25%。

- 在政府优惠措施的支持下,印度电子製造业正稳步成长。这包括 100% 外国直接投资 (FDI)、取消工业许可要求以及转向自动化生产。 2023年8月,印度推出M-SIPS(修改激励特别计画)及EDF(电子发展基金),预算1.14亿美元,支持国内电子製造业。

- 鑑于这些动态,预计亚太地区将在预测期内保持其市场主导地位。

脲醛树脂产业概况

全球脲醛树脂市场较为分散。市场上的主要企业(排名不分先后)包括 Achema、 BASF SE、Hexion、Kronoplus Limited 和 Bakelite Synthetics。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 对中密度纤维板(MDF)的需求增加

- 家具业对塑合板的需求不断增加

- 其他司机

- 抑制因素

- 脲醛树脂对健康的危害

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模(基于数量))

- 按用途

- 塑合板

- 木胶

- 合板

- 中密度纤维板

- 其他的

- 按最终用户产业

- 车

- 电器产品

- 农业

- 建筑/施工

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Achema

- ARCL Organics Ltd

- Arclin Inc.

- Ashland

- Asta Chemicals

- Bakelite Synthetics

- BASF SE

- Hexion

- Hexza Corporation Berhad

- Jiangsu Sanmu Group Co. Ltd

- Kronoplus Limited

- Melamin kemicna tovarna dd Kocevje

- Metadynea Metafrax Group

- QAFCO

- SABIC

第七章 市场机会及未来趋势

- 汽车和家用电子电器产品对高品质树脂的需求增加

- 其他机会

The Urea Formaldehyde Resins Market size is estimated at 15.34 million tons in 2025, and is expected to reach 18.87 million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

The COVID-19 epidemic negatively impacted the urea formaldehyde market. Global lockdowns and severe government rules resulted in a catastrophic setback, as most production hubs were shut down. Nonetheless, the market recovered in 2021 and is expected to rise significantly in the coming years.

Key Highlights

- Over the short term, the growing demand for particle boards from the furniture sector and the increasing demand for medium-density fiberboard (MDF) are expected to drive the market's growth.

- However, health hazards regarding urea-formaldehyde resins are expected to hinder the market's growth.

- Nevertheless, the demand for good-quality resins in automobiles and electrical appliances is expected to create new opportunities for the market studied.

- Asia-Pacific dominates the market globally, with the most consumption from China and India.

Urea Formaldehyde Resins Market Trends

Building and Construction Segment Anticipated to Dominate the Market

- The building and construction sector, heavily dependent on materials like particle boards, plywood, and medium-density fiberboard, is a crucial driver of the urea formaldehyde resin market's growth.

- As construction activities ramp up, so does the demand and production of these building materials. The extensive use of urea-formaldehyde in boards and plywood underscores its importance and propels the overall growth of the urea-formaldehyde market.

- Oxford Economics forecasts a robust growth trajectory for global construction output, projecting an increase from over USD 4.2 trillion to a staggering USD 13.9 trillion by 2037, predominantly fueled by the construction powerhouses of China, the United States, and India.

- Both Asia-Pacific and North America are experiencing a surge in residential construction. Countries like India, China, the Philippines, Vietnam, and Indonesia are at the forefront in Asia-Pacific. Meanwhile, North America's residential construction is buoyed by a growing population, rising immigration, and the trend toward nuclear families.

- South Korea's construction industry is a major economic contributor and an essential source of foreign exchange and export earnings. The size of South Korea's local construction market is expanding mainly due to solid growth in private residential construction.

- The government has also planned to execute large-scale redevelopment projects to supply 830,000 housing units in Seoul and other cities by 2025. From the planned construction, Seoul will get 323,000 new houses, and 293,000 will be built near Gyeonggi Province and Incheon. Major cities like Busan, Daegu, and Daejeon will also benefit with 220,000 new houses in 4 years.

- With housing markets rising, the Asia-Pacific region, spearheaded by China and India, is set to lead the global surge in housing construction.

- China, commanding 20% of the world's construction investments, is projected to channel nearly USD 13 trillion into buildings by 2030, underscoring a bullish outlook for the niobium market.

- Recognizing its significance, the Indian government is ramping up housing construction efforts, aiming to cater to the needs of its 1.3 billion citizens.

- Highlighting India's momentum, the National Real Estate Development Corporation (NAREDCO) reports that the top 7 cities collectively completed 4.35 lakh units in 2023, with 2024 poised for a substantial uptick. Further underscoring this trend, County Group, a prominent Noida-based real estate developer, is set to unveil over 4 million sq. ft across three ambitious housing projects this year.

- The United States dominates the construction industry in North America, with Canada and Mexico also making substantial investments. According to the US Census Bureau, the United States saw a 4.46% increase in new housing units in 2023, reaching 1,452 thousand units, up from 1,390.5 thousand in 2022. Additionally, the annual construction value in the country hit USD 1.97 trillion in 2023, marking a 7% rise from USD 1.84 trillion in 2022.

- In Canada, government initiatives like the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada are poised to bolster the construction sector significantly. In August 2022, the Canadian government unveiled a major investment exceeding USD 2 billion for these initiatives, aiming to develop around 17,000 homes nationwide, including a substantial number of affordable units.

- Given these dynamics, the building and construction segment is poised to retain its leading position in the market during the forecast period.

Asia-Pacific to Dominate the Market

- With China and India at the forefront, the Asia-Pacific region dominates the global market.

- China plays a pivotal role as the world's top producer of urea formaldehyde resins. With its growing population, China's agricultural sector is evolving to meet rising food demands. This evolution hinges on fertilizer performance and efficiency, boosting the consumption of urea formaldehyde resins.

- Boasting the world's largest construction market, China accounts for 20% of global construction investments. Projections indicate that by 2030, China is expected to invest nearly USD 13 trillion in buildings, signaling a robust market outlook. The nation's escalating housing demand is set to bolster public and private residential construction, with a notable uptick in tall buildings and hotels.

- To accelerate low-cost housing projects, Hong Kong's housing authorities have unveiled initiatives targeting the delivery of 301,000 public housing units by 2030.

- Beyond construction, urea formaldehyde resin plays a pivotal role in fiberboard production. This fiberboard finds its application in the automotive sector, shaping components like dashboards and door shells. According to the latest data released by the China Association of Automobile Manufacturers (CAAM), car production in the country it exceeded 30.16 million units in the year 2023, registering an 11.6% increase compared to the previous year. A total of 30.09 million units of passenger cars were sold in the country in 2023, registering a 12% increase compared to last year.

- According to the data released by the Society of India Automotive Manufacturing (SIAM), 4.58 million automotive vehicles were manufactured in the FY2023, compared to 3.65 million vehicles produced in 2022. The country saw a rise of around 25% in automotive production in 2023 compared to the previous year.

- India's electronics manufacturing sector is growing steadily and is driven by favorable government policies. These include 100% Foreign Direct Investment (FDI), no industrial license requirements, and a shift to automated production. In August 2023, India launched the Modified Incentive Special Package Scheme (M-SIPS) and the Electronics Development Fund (EDF), with a budget of USD 114 million to support domestic electronics manufacturing.

- Given these dynamics, the Asia-Pacific region is set to uphold its market dominance throughout the forecast period.

Urea Formaldehyde Resins Industry Overview

The global urea formaldehyde resins market is fragmented in nature. The major players in the market (not in a particular order) include Achema, BASF SE, Hexion, Kronoplus Limited, and Bakelite Synthetics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Medium Density Fiberboard (MDF)

- 4.1.2 Rising Demand for Particle Board in the Furniture Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Health Hazards Regarding Urea Formaldehyde Resins

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Application

- 5.1.1 Particle Board

- 5.1.2 Wood Adhesives

- 5.1.3 Plywood

- 5.1.4 Medium Density Fiberboard

- 5.1.5 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Electrical Appliances

- 5.2.3 Agriculture

- 5.2.4 Building and Construction

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Achema

- 6.4.2 ARCL Organics Ltd

- 6.4.3 Arclin Inc.

- 6.4.4 Ashland

- 6.4.5 Asta Chemicals

- 6.4.6 Bakelite Synthetics

- 6.4.7 BASF SE

- 6.4.8 Hexion

- 6.4.9 Hexza Corporation Berhad

- 6.4.10 Jiangsu Sanmu Group Co. Ltd

- 6.4.11 Kronoplus Limited

- 6.4.12 Melamin kemicna tovarna d.d. Kocevje

- 6.4.13 Metadynea Metafrax Group

- 6.4.14 QAFCO

- 6.4.15 SABIC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rise in Demand for Good Quality Resins in Automobile and Electrical Appliances

- 7.2 Other Opportunities