|

市场调查报告书

商品编码

1639517

线圈涂布:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Coil Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

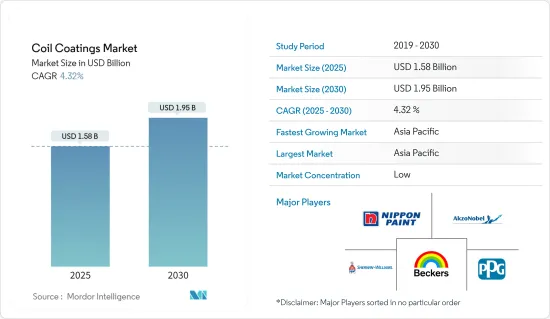

预计 2025 年线圈涂布市场规模为 15.8 亿美元,到 2030 年将达到 19.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.32%。

新冠肺炎疫情为市场带来了负面影响。疫情以各种方式使世界各地的建筑施工和工程计划面临风险,许多计划被关闭或取消,导致疫情危机期间线圈涂布市场成长放缓。但2021年,产业復苏,市场需求回归。

主要亮点

- 短期内,建设产业的需求不断增加、环境影响日益加剧、技术进步是推动市场发展的关键因素。

- 相反,汽车业对轻量材料的需求不断增加预计会阻碍市场成长。

- 然而,建筑应用对氟聚合物涂料的需求不断增加可能是一个机会。

- 由于成品钢产量高以及最终用户产品製造量大,预涂金属板的产量和出口量不断增加,亚太地区在消费量方面占据市场主导地位。

线圈涂布市场趋势

建筑和建设产业的需求增加

- 建设产业是卷材漆的最大消费者。建筑中常用的主要树脂有聚酯树脂、有机硅改质聚酯、聚二氟亚乙烯(PVDF)、氟树脂等。随着越来越多的建筑规范提倡节能建筑,住宅和消费者逐渐转向能够实现长期性能和节能的建筑策略。

- 建设产业的需求不断增长是推动线圈涂布市场发展的关键因素。全球正在进行的大型计划包括德克萨斯州的价值 10 亿美元的混合用途计划,该项目计划于 2025 年第一季完工。东京南小岩六丁目区第一类都市重建计划也预计2026年完工。因此,预计在此类计划中,捲材产品将用于屋顶、钢门、铝板、橡胶、金属层压板黏合、维修工程等。

- 此外,线圈涂布因其可塑性而被广泛应用于室内和室外建筑应用。住宅和消费者越来越多地转向能够提供高性能和长期节能的建筑技术。这就是我们专注于开发节能结构的原因。

- 线圈涂布提供红外线反射颜料技术,有助于降低建筑物的室内温度。该技术降低了冷却所消耗的能量,使线圈涂布成为建筑应用中首选的节能捲材产品。它也用于防水排水沟和落水管。

- 由于商业房地产领域的改善以及联邦和州政府对公共和机构建筑的投资增加,北美建设产业正在稳步增长。北美主要的计划包括耗资25亿美元的酵母综合用途开发计划。该计划旨在为德克萨斯州提供更好的住宅和办公设施,预计于2040年完工。因此,预计建设产业投资增加将对线圈涂布产生正面影响。

- 法国、德国、英国和义大利等西欧主要国家正积极推动线圈涂布市场的发展。随着该地区建设活动的活性化,对线圈涂布的需求也大幅增加。例如,根据 Trading Economics 的数据,2022 年 12 月法国建筑业产量与 2022 年 7 月相比成长了 3.1%。

- 此外,由于其美观度和持久价值,捲材漆也用于建设产业的天花板格栅、门、屋顶、墙板、窗户等。正在进行的计划包括美国。预计 2024 年完工。另一个正在进行的计划是位于东京、耗资 31.7 亿美元的滨松町芝浦一丁目重建计划。

- 该计划将由两栋建筑组成,预计于 2030 年完工。耗资 8.41 亿美元的澳洲伊丽莎白码头地段计划计划2025 年完工。预计这些计划将在未来几年增加住宅和商业建筑对预涂金属的需求。

- 由于这些因素,预计预测期内建设产业的线圈涂布市场将稳定成长。

亚太地区占市场主导地位

- 亚太地区占据全球市场占有率的主导地位。由于其美观度和持久价值,捲材漆被用于建设产业的天花板格栅、门、屋顶、墙板和窗户。

- 预计预测期内亚太线圈涂布市场将大幅成长,其中中国将因建筑扩张和工业快速发展而引领市场。该地区的建筑施工和维修活动正在增加,预计将推动线圈涂布消费量的激增。

- 例如,亚太地区正在进行的建筑工程计划包括日本东京价值 31.7 亿美元的滨松町芝浦一丁目重建计划,预计于 2030 年完工。另一个例子是计划在中国武汉建设的武汉佛山外滩中心T1计划。因此,预计该地区建筑施工计划数量的增加将推动线圈涂布的成长。

- 此外,对运输车辆的需求不断增加,推动了线圈涂布市场的发展。由于需求强劲且消费者更喜欢私家车而非公共交通,预计印度汽车产业将在 2023 年成为亚太地区最强劲的产业。例如,根据OICA的数据,2022年该国的汽车产量将达到5,456,857辆,比2020年增加24%。因此,由于汽车整体产量的增加,该地区的线圈涂布产业可能会扩大。

- 由于这些因素,该地区对线圈涂布的需求预计会增加。

线圈涂布产业概况

线圈涂布市场比较分散。该市场的主要企业(不分先后顺序)包括阿克苏诺贝尔公司、贝克斯集团、PPG工业公司、宣威威廉斯公司和日本涂料控股公司。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 建筑和建设产业的需求不断增加

- 日益增加的环境影响和技术进步

- 其他驱动因素

- 限制因素

- 汽车产业对轻量材料的需求不断增加

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 依树脂类型

- 聚酯纤维

- 聚二氟亚乙烯(PVDF)

- 聚氨酯 (PU)

- 塑性溶胶

- 其他树脂类型

- 按最终用户产业

- 建筑和施工

- 工业和消费性电器产品

- 运输

- 家具

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率分析(%)**/排名分析

- 主要企业策略

- 公司简介

- 捲材涂布机

- ArcelorMittal

- Arconic

- BDM Coil Coaters

- CENTRIA

- Chemcoaters

- Dura Coat Products

- Goldin Metals Inc.

- Jupiter Aluminum Corporation

- Norsk Hydro ASA

- Novelis

- Ralco Steels

- Rautaruukki Corporation

- Salzgitter Flachstahl GmbH

- Tata Steel

- Tekno Kroma

- thyssenkrupp AG

- UNICOIL

- United States Steel Corporation

- 油漆供应商

- Akzo Nobel NV

- Axalta Coatings System LLC

- Beckers Group

- Brillux GmbH & Co. KG

- Hempel A/S

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd

- NOROO Coil Coatings Co., Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Yung Chi Paint & Varnish Mfg Co. Ltd

- 预处理、树脂、颜料、设备

- Arkema

- Bayer AG

- Covestro AG

- Evonik Industries AG

- Henkel AG & Co. KgaA

- Solvay

- Wacker Chemie AG

- 捲材涂布机

第七章 市场机会与未来趋势

- 建筑用氟树脂涂料需求不断增加

- 其他机会

The Coil Coatings Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 1.95 billion by 2030, at a CAGR of 4.32% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. The pandemic jeopardized building construction and engineering projects worldwide in numerous ways, and many projects were closed or halted, decelerating the growth of the coil coatings market during the pandemic crisis. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, rising demand from the building and construction industry and growing environmental influences, and advancing technology are the major factors driving the market studied.

- Conversely, increasing demand for lightweight materials in the automobile industry is expected to hinder the studied market's growth.

- However, increasing demand for fluoropolymer coatings for architectural applications will likely act as an opportunity.

- Asia-Pacific dominated the market in terms of consumption due to the rise in the production and export of pre-coated metal sheets in the region due to the high production of finished steel and the high manufacturing of end-user products.

Coil Coatings Market Trends

Rising Demand from the Building and Construction Industry

- The building and construction industry is by far the largest consumer of coil coatings. The main resins used extensively in construction are polyester resin, silicone-modified polyester, polyvinylidene fluorides (PVDF), or fluoropolymer. With the rising number of building codes that promote energy-efficient structures, home builders and consumers are gradually moving toward building strategies that deliver performance and energy savings in the long run.

- The rising demand from the construction industry is a key factor driving the coil coatings market. Some of the large ongoing building construction projects worldwide include the Magnolia Mixed-Use Complex project worth USD 1 billion in Texas, which is expected to be completed in Q1 2025. The Minamikoiwa 6-Chome District Type One Urban Redevelopment project in Tokyo, Japan, is another project expected to be completed in 2026. Thus, such construction projects are estimated to use coil products for roofing, steel doors, aluminum panels, rubber, metal lamination bonding, renovation work, and others.

- Furthermore, coil coatings are also widely used for interior and exterior construction applications due to their malleability. Home builders and consumers increasingly shift towards building techniques that impart performance and long-term energy savings. Hence, they are focusing on developing energy-efficient structures.

- Coil coatings provide infrared reflective pigment technology that helps in lowering the indoor temperature of the building. This technique reduces the energy consumed for cooling, making coil coatings energy efficient and the preferred choice for coil products used in building and construction work. It is also utilized to construct gutters and downspouts for waterproof installations.

- The construction industry in North America is growing steadily due to the improving commercial real estate sector and increased federal and state investment in public construction and institutional buildings. Some of North America's major building construction projects include the East River Mixed-Use Development project worth USD 2.5 billion. The project aims to provide better residential and office facilities in Texas, which is expected to be completed in 2040. Therefore, increasing building and construction industry investments are expected to create an upside for coil coatings.

- The major Western European countries, including France, Germany, the United Kingdom, and Italy, are actively contributing to the coil coatings market. With growing building construction activities in the region, the demand for coil coatings increased significantly. For instance, according to Trading Economics, construction output in France increased by 3.1% in December 2022 compared to July 2022.

- Moreover, due to its high-end aesthetics and long-lasting value, coil coatings are used in the building and construction industry in ceiling grids, doors, roofing and siding, windows, etc. Some of the ongoing construction projects include the Eight Office Tower project worth USD 476 million, which involves the construction of a 25-story office tower in Bellevue, Washington, United States. It is expected to be completed in 2024. The Hamamatsucho Shibaura 1 Chome Redevelopment Project, worth USD 3.17 billion in Tokyo, Japan, is another ongoing project.

- The project involves the construction of two buildings and is expected to be finished by 2030. The Elizabeth Quay Lot V and Lot VI Mixed-Use Complex construction project worth USD 841 million in Australia is yet another project likely to be completed in 2025. These projects are expected to increase the demand for pre-coated metals in the construction of residential and commercial buildings in the coming years.

- Due to all such factors, the building and construction industry's coil coatings market is expected to grow steadily during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market share. Due to their high-end aesthetics and long-lasting value, coil coatings are used in the building and construction industry in ceiling grids, doors, roofing and siding, windows, etc.

- The Asia-Pacific coil coatings market is anticipated to grow significantly during the forecast period, with China leading the market owing to expanding construction and rapid industrial development. The growing building construction and renovation activities in the region are expected to surge the consumption of coil coatings.

- For instance, some of the ongoing building construction projects in the Asia-Pacific include the Hamamatsucho Shibaura 1 Chome Redevelopment project worth USD 3.17 billion, expected to be completed in 2030 in Tokyo, Japan. Another such project is the Wuhan Fosun Bund Center T1 project, which involves the construction of the Fosun Bund Center T1 in Wuhan, China. Therefore, increasing building construction projects are expected to drive the growth of coil coatings in the region.

- Furthermore, the growing demand for transport vehicles is driving the coil coatings market. In 2023, India's automotive sector is predicted to be the strongest in the Asia-Pacific region, owing to strong demand and consumers' preference for personal vehicles over public transportation. For instance, according to OICA, in 2022, automobile production in the country amounted to 5,456,857 units, which showed an increase of 24% compared to 2020. Therefore, the region's coil coatings industry will likely expand due to the rise in overall automobile manufacturing.

- All such factors are expected to increase the demand for coil coatings in the region.

Coil Coatings Industry Overview

The coil coatings market is fragmented in nature. The major players in this market (not in a particular order) include Akzo Nobel N.V., Beckers Group, PPG Industries, Inc., The Sherwin-Williams Company, and Nippon Paint Holdings Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Building and Construction Industry

- 4.1.2 Growing Environmental Influences and Advancing Technology

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Demand for Lightweight Materials in Automotive Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Polyester

- 5.1.2 Polyvinylidene Fluorides (PVDF)

- 5.1.3 Polyurethane(PU)

- 5.1.4 Plastisols

- 5.1.5 Other Resin Types

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Industrial and Domestic Appliances

- 5.2.3 Transportation

- 5.2.4 Furniture

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Coil Coaters

- 6.4.1.1 ArcelorMittal

- 6.4.1.2 Arconic

- 6.4.1.3 BDM Coil Coaters

- 6.4.1.4 CENTRIA

- 6.4.1.5 Chemcoaters

- 6.4.1.6 Dura Coat Products

- 6.4.1.7 Goldin Metals Inc.

- 6.4.1.8 Jupiter Aluminum Corporation

- 6.4.1.9 Norsk Hydro ASA

- 6.4.1.10 Novelis

- 6.4.1.11 Ralco Steels

- 6.4.1.12 Rautaruukki Corporation

- 6.4.1.13 Salzgitter Flachstahl GmbH

- 6.4.1.14 Tata Steel

- 6.4.1.15 Tekno Kroma

- 6.4.1.16 thyssenkrupp AG

- 6.4.1.17 UNICOIL

- 6.4.1.18 United States Steel Corporation

- 6.4.2 Paint Suppliers

- 6.4.2.1 Akzo Nobel N.V.

- 6.4.2.2 Axalta Coatings System LLC

- 6.4.2.3 Beckers Group

- 6.4.2.4 Brillux GmbH & Co. KG

- 6.4.2.5 Hempel A/S

- 6.4.2.6 Kansai Paint Co.,Ltd.

- 6.4.2.7 Nippon Paint Holdings Co., Ltd

- 6.4.2.8 NOROO Coil Coatings Co., Ltd.

- 6.4.2.9 PPG Industries, Inc.

- 6.4.2.10 The Sherwin-Williams Company

- 6.4.2.11 Yung Chi Paint & Varnish Mfg Co. Ltd

- 6.4.3 Pretreatment, Resins, Pigments, Equipment

- 6.4.3.1 Arkema

- 6.4.3.2 Bayer AG

- 6.4.3.3 Covestro AG

- 6.4.3.4 Evonik Industries AG

- 6.4.3.5 Henkel AG & Co. KgaA

- 6.4.3.6 Solvay

- 6.4.3.7 Wacker Chemie AG

- 6.4.1 Coil Coaters

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Fluoropolymer Coatings for Architectural Applications

- 7.2 Other Opportunities

环氧线圈涂布市场规模、份额及成长分析:依产品类型、应用方法、配方类型、最终用途产业及地区划分-2026-2033年产业预测

环氧线圈涂布市场规模、份额及成长分析:依产品类型、应用方法、配方类型、最终用途产业及地区划分-2026-2033年产业预测 全球线圈涂布市场规模、份额、趋势及成长分析报告(2026-2034)

全球线圈涂布市场规模、份额、趋势及成长分析报告(2026-2034) 2026年全球线圈涂布市场报告

2026年全球线圈涂布市场报告 日本卷材涂料市场规模、份额、趋势及预测(按类型、应用、最终用途行业和地区划分),2026-2034年

日本卷材涂料市场规模、份额、趋势及预测(按类型、应用、最终用途行业和地区划分),2026-2034年 线圈涂布市场规模、份额及成长分析(依树脂类型、应用、终端用户产业及地区划分)-2026-2033年产业预测

线圈涂布市场规模、份额及成长分析(依树脂类型、应用、终端用户产业及地区划分)-2026-2033年产业预测 线圈涂布市场规模、份额和趋势分析报告:按树脂、应用、最终用途、地区和细分市场预测(2026-2033 年)

线圈涂布市场规模、份额和趋势分析报告:按树脂、应用、最终用途、地区和细分市场预测(2026-2033 年) 全球线圈涂布市场(按类型、应用、最终用途行业和地区划分)- 预测至 2030 年2025 年至 2033 年卷材涂料市场报告(按类型、应用、最终用途行业和地区)

全球线圈涂布市场(按类型、应用、最终用途行业和地区划分)- 预测至 2030 年2025 年至 2033 年卷材涂料市场报告(按类型、应用、最终用途行业和地区) 技术线圈涂布市场:按材料、按技术、按产品类型、按最终用途行业、按地区划分

技术线圈涂布市场:按材料、按技术、按产品类型、按最终用途行业、按地区划分 2025 年至 2029 年全球线圈涂布市场

2025 年至 2029 年全球线圈涂布市场