|

市场调查报告书

商品编码

1851386

3D感测器:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030年)3D Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

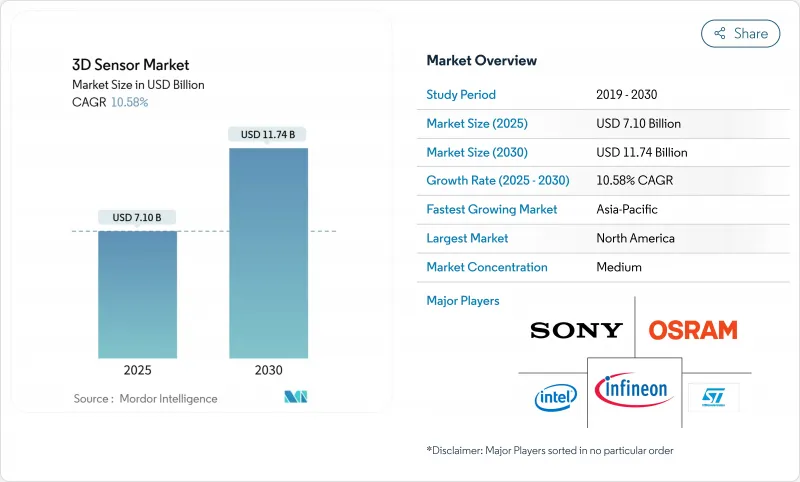

预计 3D 感测器市场将从 2025 年的 71 亿美元成长到 2030 年的 117.4 亿美元,复合年增长率为 10.58%。

家用电子电器、汽车安全、工业自动化以及新兴混合实境平台对空间感知能力的需求不断增长,推动了该技术的发展。光学元件的小型化、感测器边缘处理的整合以及单位成本的下降,正在扩大其应用范围。亚太地区的成长势头最为强劲,该地区强大的电子製造能力正在缩短从设计到生产的周期;而在中东,政府支持的智慧城市投资正在加速该技术的应用。竞争优势正从独立的硬体规格转向整合的感测+软体堆迭,以降低嵌入式环境中的延迟和功耗。

全球3D感测器市场趋势与洞察

智慧型手机人脸脸部认证的应用有助于提升本地领导力。

预计到2026年,亚洲高阶行动电话的3D脸部认证配戴率将超过65%,这将使其成为3D感测器市场中最大的单一应用领域。结构光学模组飞行时间模组如今能够在各种光照条件下产生可靠的亚毫米级深度图,从而实现安全支付、虚拟形象创建和个性化用户介面。亚洲的原始设备製造商(OEM)正在将感测器移至萤幕下方,以节省空间,同时又不牺牲其可靠性。行动电话的大规模生产正在降低穿戴式装置和智慧家居设备等相关领域的零件成本,从而形成良性循环的需求驱动机制。

汽车光达改变了汽车安全的新标准

欧洲汽车製造商正积极部署基于雷射雷达(LiDAR)的高级驾驶辅助系统(ADAS),以应对2026年新车安全评估协会(NCAP)强制实施的行人自动紧急煞车系统。固态光达设计可在200公尺范围内达到公分级精度,满足严格的汽车可靠性测试,同时降低材料成本。欧洲日益严格的监管趋势,加上北美地区的自愿性倡议,正在形成统一的要求标准,这将使全球一级感测器供应商受益。随着成本的下降,雷射雷达的应用预计将从高阶车型逐步扩展到中端车型,从而扩大其在各个细分市场的潜在应用范围。

热学挑战阻碍了VCSEL阵列的小型化

为了在更小的空间内实现更高的光输出,VCSEL发射器之间的间距越来越小,导致阵列中心元件的温度可能比环境温度高出50°C。更高的结温会降低效率,并可能导致灾难性故障。装置製造商正在尝试采用分路驱动电路和先进封装技术,将热量横向引导至铜层,然后传导至敏感光学元件。这些创新技术的应用可望缓解目前3D感测器市场面临的挑战,让紧凑型消费性电子产品也能维持高效能。

细分市场分析

到2024年,影像感测器将占总收入的62%,巩固其在3D感测器市场的基础地位。智慧型手机、工业检测和机器人等应用领域对高解析度深度图的需求强劲,这些应用需要亚毫米级精度和5公尺探测范围的深度图。多层背照式架构及片上HDR管线不断提升讯号杂讯比。领先的供应商正在向300毫米晶圆生产线转型,从而提高产量比率,并降低每百万像素成本。

随着非接触式介面在资讯娱乐主机、互动式服务站和医疗设备中的普及,手势姿态辨识感测器将以14.8%的复合年增长率快速成长至2030年。新型模组将飞行时间深度感测器、毫米波雷达和人工智慧推理整合于单块基板,即使在光线变化的环境下也能识别复杂的手势。亚太地区经验丰富的OEM设计团队正在进一步缩短开发週期,协助该领域占据3D感测器市场的大部分份额。

位置感测器、惯性测量单元和热电堆元件可满足光学解决方案无法满足的特定精度和环境要求,供应商之间的交叉授权已整合 IP,使其可供多个供应商的系统设计人员使用。

影像感测器子类别将在2024年成为最大的市场,规模达44亿美元,并在2030年之前保持中等个位数的复合年增长率。背照式堆迭CMOS架构将占该类别出货量的约50%,这主要得益于对更高动态范围和更低功耗的需求。儘管基数较小,但随着公共和私人场所寻求减少与物体表面的共用,手势姿态辨识模组预计到2030年将贡献16亿美元的收入。这一增长表明,多样化的外形规格正在推动整个3D感测器市场的成长势头。

飞行时间感测器将在2024年占总收入的46%,这反映了其成本和精度方面的优势平衡。间接飞行时间感测器在消费性电子设备领域占据主导地位,这得益于成熟的垂直腔面发射雷射(VCSEL)发射器和简单的单光子Avalanche二极体(SPAD)接收器。直接飞行时间感测器具有皮秒级的时间分辨率,在机器人和工业自动化领域占据领先地位,这些领域需要更长的操作距离。将电容式深度运算引擎整合到与光电二极体相同的晶粒上,可降低延迟,并可为边缘人工智慧模型提供动力,而无需与主机处理器进行往返通讯。

儘管目前雷射雷达解决方案的出货量较小,但在汽车自动驾驶项目和基础设施数位双胞胎计划的推动下,预计到2030年将以13.61%的复合年增长率成长。固态扫描、微电子机械光束控制和调频连续波架构等技术在提升侦测距离的同时,减少了运动部件的数量。这些进步将降低每个点云的成本,进而推动3D感测器市场从豪华车领域拓展到其他领域。

结构光光源仍然是近距离高清影像撷取的首选,例如人脸解锁和工业计量。立体视觉和超音波在某些特定领域也占有一席之地。立体视觉提供了一种基于镜头的替代方案,无需主动照明;而超音波在光路被灰尘或液体阻挡时表现出色。

3D感测器市场份额报告按产品(例如,位置感测器、影像感测器)、技术(例如,结构光、飞行时间)、终端用户产业(例如,消费性电子、汽车)、组件(例如,红外线VCSEL发射器)和地区(例如,北美、欧洲、亚洲)进行细分。市场预测以美元计价。

区域分析

到2024年,亚太地区将占全球收入的38%,这反映了该地区半导体製造厂密度高、光学技术人员技术娴熟以及垂直整合的供应链。中国将占该地区销售额的约40%,主要得益于国内智慧型手机OEM厂商积极采用自主研发的深孔模组。日本在精密玻璃模塑和晶圆级光学领域拥有卓越的实力,为工业机器人提供高精度感测器。韩国正利用其先进的封装技术,将逻辑电路和感测电路整合到单一基板上,从而提升微型模组的散热性能。

中东地区虽然起步较晚,但预计到2030年将达到12.87%的复合年增长率。各国智慧城市蓝图正在资助安装深度感知街道设施、自动化零售亭和人工智慧医疗影像处理。海湾合作波湾合作理事会)的本土系统整合商正与欧洲和亚洲的组件供应商伙伴关係,以实现解决方案的本地化,从而满足气候和语言要求。零售业快速的采购週期正在加快从试点到量产的进程,为3D感测器市场带来短期成长潜力。

北美仍然是雷射雷达研发的中心,这得益于其充满活力的创投生态系统和国防部门主导的研究津贴。北美汽车零件製造商正主导晶片级光束控制技术的发展。儘管欧洲拥有严格的资料保护法律,但汽车和工业自动化领域的需求仍然旺盛,推动了边缘个人资料处理感测器的设计。南美洲在安防和农业技术领域已开始早期应用雷射雷达技术,而非洲的应用主要限于需要强大感测解决方案的物流枢纽和采矿作业。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧型手机脸部认证的普及(亚洲)

- 欧洲汽车光达辅助高阶驾驶辅助系统的部署

- AR/ VR头戴装置中深度感知摄影机的兴起(美国)

- 协作机器人在电子产品组装上的应用(韩国、台湾)

- 3D感测器在安防监控系统中的集成

- 面向智慧零售的边缘人工智慧驱动的3D视觉(海湾合作委员会)

- 市场限制

- 小型化VCSEL阵列的温度控管挑战

- 出于隐私主导,欧盟加强了对深度摄影机的监管(欧盟人工智慧法)。

- 传统飞行时间模组的高功耗

- 氮化镓雷射半导体供应链的紧缩

- 价值/供应链分析

- 监理与技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 专利情况

第五章 市场规模与成长预测

- 副产品

- 位置感测器

- 影像感测器(3D相机)

- 温度感测器

- 加速计和惯性测量单元感测器

- 环境光和接近感测器

- 手势姿态辨识感应器

- 透过技术

- 结构光

- 飞行时间(dToF 和 iToF)

- 立体视觉

- 光达(闪光式和FMCW式)

- 超音波

- 按行业

- 消费性电子产品

- 汽车与运输

- 医疗保健和医疗设备

- 工业自动化与机器人

- 安全与监控

- 航太/国防

- 按组件

- 红外线VCSEL发送器

- 深度影像感测器

- 系统晶片处理器

- 光学元件/滤光片

- 照明模组

- 软体和演算法

- 按地区

- 北美洲

- 美国

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 欧洲

- 英国

- 德国

- 法国

- 北欧国家(瑞典、挪威、丹麦、芬兰)

- 中东

- GCC

- 土耳其

- 非洲

- 南非

- 奈及利亚

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Intel Corp.

- Sony Group Corp.

- ams OSRAM AG

- STMicroelectronics NV

- Infineon Technologies AG

- Lumentum Holdings Inc.

- Apple Inc.(PrimeSense)

- Samsung Electronics Co. Ltd.

- OmniVision Technologies Inc.

- Panasonic Holdings Corp.

- Cognex Corp.

- Sick AG

- LMI Technologies Inc.

- Teledyne e2v

- Qualcomm Inc.

- SoftKinetic(Sony DepthSense)

- Melexis NV

- Himax Technologies Inc.

- Velodyne Lidar Inc.

- XYZ Interactive Technologies

第七章 市场机会与未来展望

The 3D sensor market is valued at USD 7.1 billion in 2025 and is forecast to reach USD 11.74 billion by 2030, advancing at a 10.58% CAGR.

Growth is anchored in rising demand for spatial awareness across consumer electronics, automotive safety, industrial automation, and emerging mixed-reality platforms. Miniaturization of optical components, integration of on-sensor edge processing, and falling unit costs are enlarging the addressable base of applications. Regional momentum is strongest in Asia-Pacific, where deep electronics manufacturing capacity shortens design-to-production cycles, while government-backed smart-city spending is accelerating adoption in the Middle East. Competitive differentiation is now moving from discrete hardware specifications toward complete sensing-plus-software stacks that reduce latency and power consumption in embedded environments.

Global 3D Sensor Market Trends and Insights

Smartphone facial recognition adoption fuels regional leadership

Premium handsets in Asia are expected to pass a 65% attachment rate for 3D facial recognition by 2026, consolidating the 3D sensor market's largest single application base. Structured-light and Time-of-Flight modules now generate sub-millimeter depth maps reliable under varied lighting, enabling secure payments, avatar creation, and personalized UI. Asian OEMs have moved sensors beneath the display to save frontage without sacrificing robustness. Volume scaling in handset production is lowering component costs for adjacent sectors such as wearables and smart-home devices, reinforcing a virtuous demand cycle.

Automotive LiDAR transforms vehicle-safety benchmarks

European automakers are installing LiDAR-based ADAS ahead of the 2026 NCAP mandate for pedestrian automatic emergency braking. Solid-state designs deliver centimeter-level accuracy at up to 200 m, meeting stringent automotive reliability tests while shrinking bill-of-materials. The regulatory push in Europe is echoed by voluntary commitments in North America, creating a homogeneous requirements profile that benefits global tier-one sensor suppliers. As cost curves decline, LiDAR uptake is expected to cascade from premium models into mid-segment vehicles, enlarging the 3D sensor market addressable volume.

Thermal challenges hinder VCSEL array miniaturization

As VCSEL emitters are packed closer to achieve higher optical power in ever-smaller footprints, central elements in an array can run 50 °C hotter than ambient. Elevated junction temperatures degrade efficiency and risk catastrophic failure. Device makers are experimenting with segmented drive circuits and advanced packaging that routes heat laterally to copper layers before it reaches sensitive optics. Adoption of these innovations will moderate the current drag on the 3D sensor market by preserving performance inside compact consumer devices.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of depth-sensing cameras in mixed-reality headsets

- Collaborative robots advance precision electronics assembly

- EU AI Act creates compliance burdens for biometric sensing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Image Sensors accounted for 62% of 2024 revenue, confirming their foundational role in the 3D sensor market. Robust demand arises from smartphones, industrial inspection, and robotics that depend on high-resolution depth maps spanning 5 m ranges with sub-millimeter precision. Multi-stack backside-illuminated architectures and on-chip HDR pipelines continue to improve signal-to-noise ratios. Leading suppliers have shifted to 300 mm wafer lines, driving yield improvements that lower cost per megapixel.

Gesture-Recognition Sensors record the fastest expansion, advancing at a 14.8% CAGR to 2030 as touchless interfaces penetrate infotainment consoles, interactive kiosks, and healthcare devices. New modules fuse ToF depth, millimeter-wave radar, and AI inference on a single substrate, enabling recognition of complex hand poses under variable lighting. Upskilled OEM design teams in Asia-Pacific further shorten development cycles, helping this segment accumulate a higher share of the 3D sensor market.

Position Sensors, Inertial Measurement Units, and Thermopile elements round out the portfolio, each addressing specific accuracy or environmental requirements where optical methods face limits. Cross-licensing among suppliers is consolidating IP, ensuring multi-vendor availability for system designers.

The image-sensor subcategory represents the largest 3D sensor market size at USD 4.4 billion in 2024 and is on course for a mid-single-digit CAGR through 2030. Within this category, back-illuminated stacked CMOS architectures commanded roughly 50% of shipments, underscoring the move toward higher dynamic range at lower power. Gesture-recognition modules, despite a smaller base, are set to contribute USD 1.6 billion incremental revenue by 2030 as public and private spaces look to minimize shared-surface contact. This surge illustrates how diversified form factors collectively reinforce growth momentum across the 3D sensor market.

Time-of-Flight sensors generated 46% of total revenue in 2024, reflecting their favorable cost-to-accuracy balance. Indirect ToF dominates consumer devices thanks to mature VCSEL emitters and simple single-photon avalanche diode (SPAD) receivers. Direct ToF variants, with picosecond timing resolution, lead in robotics and industrial automation requiring longer working distances. Integration of capacitive depth-computation engines on the same die as photodiodes slashes latency, feeding edge-AI models without round-trips to host processors.

LiDAR solutions, though smaller in today's shipment volumes, are growing at a 13.61% CAGR through 2030, propelled by automotive autonomy programs and infrastructure digital-twin projects. Solid-state scanning, micro-electro-mechanical beam steering, and frequency-modulated continuous-wave architectures are improving range while lowering moving-part counts. These advances reduce cost per point cloud and, by extension, broaden the 3D sensor market beyond premium vehicles.

Structured-light remains a preferred choice for close-range, high-detail capture such as facial unlocking and industrial metrology. Stereo vision and ultrasound maintain footholds in specific niches-stereo offers a lens-based alternative without active illumination, while ultrasound succeeds where optical paths are obstructed by dust or fluid.

3D Sensor Market Share Report is Segmented by Product (Position Sensors, Image Sensors and More), Technology (Structured Light, Time-Of-Flight and More), End-User Vertical (Consumer Electronics, Automotive and More), Component (IR VCSEL Emitters, and More), and Geography (North America, Europe, Asia and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 38% of global revenue in 2024, reflecting the region's dense semiconductor fabs, skilled optics workforce, and vertically integrated supply chains. China accounts for about 40% of regional sales, bolstered by domestic smartphone OEMs that are aggressively adopting in-house depth modules. Japan excels in precision glass molding and wafer-level optics, feeding high-accuracy sensors for industrial robotics. South Korea leverages advanced packaging know-how to integrate logic and sensing into single substrates, improving thermal performance in compact modules.

The Middle East, though starting from a low base, is on course for a 12.87% CAGR through 2030. National smart-city roadmaps fund installations of depth-sensing street furniture, automated retail kiosks, and AI-enabled healthcare imaging suites. Domestic system integrators in the Gulf Cooperation Council are forging partnerships with European and Asian component vendors to localize solutions that meet climatic and linguistic requirements. Rapid procurement cycles in the retail sector are accelerating pilot-to-production timelines, providing near-term upside for the 3D sensor market.

North America remains the epicenter of LiDAR RandD, supported by a vibrant venture ecosystem and defense-driven research grants. Tier-one automotive suppliers here lead the push toward chip-scale beam steering. Europe sustains demand in automotive and industrial automation despite rigorous data-protection laws, spurring sensor designs that process personal data at the edge. South America shows early adoption in security and agritech, while Africa's deployments are mainly confined to logistics hubs and mining operations that require rugged sensing solutions.

- Intel Corp.

- Sony Group Corp.

- ams OSRAM AG

- STMicroelectronics N.V.

- Infineon Technologies AG

- Lumentum Holdings Inc.

- Apple Inc. (PrimeSense)

- Samsung Electronics Co. Ltd.

- OmniVision Technologies Inc.

- Panasonic Holdings Corp.

- Cognex Corp.

- Sick AG

- LMI Technologies Inc.

- Teledyne e2v

- Qualcomm Inc.

- SoftKinetic (Sony DepthSense)

- Melexis N.V.

- Himax Technologies Inc.

- Velodyne Lidar Inc.

- XYZ Interactive Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone Facial Recognition Adoption (Asia)

- 4.2.2 Automotive LiDAR-Assisted ADAS Roll-outs (Europe)

- 4.2.3 Proliferation of Depth-Sensing Cameras in AR/VR Headsets (US)

- 4.2.4 Deployment of Collaborative Robots in Electronics Assembly (South Korea, Taiwan)

- 4.2.5 Integration of 3D Sensors in Security and Surveillance Systems

- 4.2.6 Edge-AI Powered 3D Vision for Smart Retail (GCC)

- 4.3 Market Restraints

- 4.3.1 Thermal Management Challenges in Miniaturised VCSEL Arrays

- 4.3.2 Privacy-Led Regulatory Scrutiny on Depth Cameras (EU AI Act)

- 4.3.3 High Power Consumption in Continuous Time-of-Flight Modules

- 4.3.4 Semiconductor Supply-Chain Tightness for Gallium-Nitride Lasers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Patent Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Position Sensors

- 5.1.2 Image Sensors (3D Cameras)

- 5.1.3 Temperature Sensors

- 5.1.4 Accelerometer and IMU Sensors

- 5.1.5 Ambient-Light and Proximity Sensors

- 5.1.6 Gesture-Recognition Sensors

- 5.2 By Technology

- 5.2.1 Structured Light

- 5.2.2 Time-of-Flight (dToF and iToF)

- 5.2.3 Stereo Vision

- 5.2.4 LiDAR (Flash and FMCW)

- 5.2.5 Ultrasound

- 5.3 By End-User Vertical

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive and Transportation

- 5.3.3 Healthcare and Medical Devices

- 5.3.4 Industrial Automation and Robotics

- 5.3.5 Security and Surveillance

- 5.3.6 Aerospace and Defence

- 5.4 By Component

- 5.4.1 IR VCSEL Emitters

- 5.4.2 Depth Image Sensors

- 5.4.3 System-on-Chip Processors

- 5.4.4 Optics and Filters

- 5.4.5 Illumination Modules

- 5.4.6 Software and Algorithms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 Turkey

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.6 Asia-Pacific

- 5.5.6.1 China

- 5.5.6.2 Japan

- 5.5.6.3 South Korea

- 5.5.6.4 India

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Intel Corp.

- 6.4.2 Sony Group Corp.

- 6.4.3 ams OSRAM AG

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Lumentum Holdings Inc.

- 6.4.7 Apple Inc. (PrimeSense)

- 6.4.8 Samsung Electronics Co. Ltd.

- 6.4.9 OmniVision Technologies Inc.

- 6.4.10 Panasonic Holdings Corp.

- 6.4.11 Cognex Corp.

- 6.4.12 Sick AG

- 6.4.13 LMI Technologies Inc.

- 6.4.14 Teledyne e2v

- 6.4.15 Qualcomm Inc.

- 6.4.16 SoftKinetic (Sony DepthSense)

- 6.4.17 Melexis N.V.

- 6.4.18 Himax Technologies Inc.

- 6.4.19 Velodyne Lidar Inc.

- 6.4.20 XYZ Interactive Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球3D感测技术市场报告

2026年全球3D感测技术市场报告 全球3D感测技术市场规模、份额、趋势和成长分析报告(2026-2034年)3D感测器市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)2026年全球3D感测器市场报告

全球3D感测技术市场规模、份额、趋势和成长分析报告(2026-2034年)3D感测器市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)2026年全球3D感测器市场报告 3D感测器市场-全球产业规模、份额、趋势、机会及预测(按类型、技术、连接方式、最终用途、地区和竞争格局划分,2021-2031年)

3D感测器市场-全球产业规模、份额、趋势、机会及预测(按类型、技术、连接方式、最终用途、地区和竞争格局划分,2021-2031年) TMR磁性IC市场按产品类型、功率类型、技术、应用和最终用户产业划分-2026-2032年全球预测

TMR磁性IC市场按产品类型、功率类型、技术、应用和最终用户产业划分-2026-2032年全球预测 3D感测器市场规模、份额和成长分析(按连接方式、测量方法、类型、技术、最终用途产业和地区划分)-2026-2033年产业预测

3D感测器市场规模、份额和成长分析(按连接方式、测量方法、类型、技术、最终用途产业和地区划分)-2026-2033年产业预测 3D影像感测器市场规模、份额和成长分析(按类型、技术、最终用途产业、性别和地区划分)-产业预测(2026-2033年)

3D影像感测器市场规模、份额和成长分析(按类型、技术、最终用途产业、性别和地区划分)-产业预测(2026-2033年) 3D感测技术的全球市场

3D感测技术的全球市场 3D 感测和成像:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

3D 感测和成像:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)