|

市场调查报告书

商品编码

1640427

硝基苯 -市场占有率分析、行业趋势和统计、成长预测(2025-2030)Nitrobenzene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

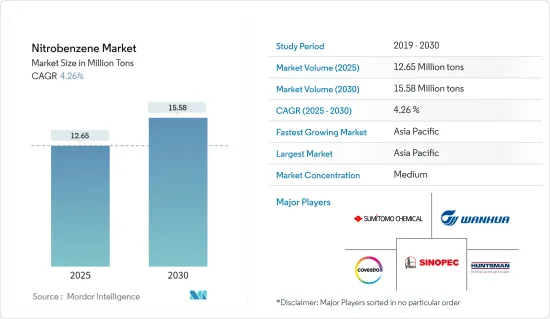

预计2025年硝基苯市场规模为1,265万吨,预计2030年将达到1,558万吨,预测期(2025-2030年)复合年增长率为4.26%。

2020 年,硝基苯市场受到了 COVID-19 的负面影响。考虑到大流行的情况,各种硝基苯衍生物产品的需求下降对市场需求产生了负面影响。但硝基苯衍生物苯胺衍生的对乙酰胺酚酚需求增加,刺激硝基苯市场需求。儘管如此,市场在疫情后时代已开始加快步伐,并预计未来将遵循相同的轨迹。

主要亮点

- 从中期来看,推动需求强劲的因素,例如生产苯胺的硝基苯需求增加、生产原材料的容易取得以及亚太地区建设活动的活性化,预计将推动市场成长。

- 相反,对生物基化学品的需求不断增长可能会阻碍市场成长。

- 世界各地建筑业的各种投资可能为所研究的市场带来机会。

- 亚太地区主导全球市场,消费量最高的国家是中国和印度等。

硝基苯市场趋势

苯胺生产需求增加

- 苯胺製造用途占硝基苯用途的最大份额,占超过90%。主要生产硝基苯催化加氢。

- 印度是最大的苯胺生产和出口国之一。根据印度化学和化学肥料部统计,2022-2023年国内苯胺产量为39,660吨,较2021-2022年成长约18.28%。

- 苯胺衍生的二苯基甲烷二异氰酸酯(MDI) 是各种最终用途行业(包括建筑和汽车领域)聚合物的重要前体。

- 根据国际汽车製造组织(OICA)的数据,2022年全球汽车产量成长约6%,达到85.01辆。这将减少对基于MDI的合成橡胶和聚氨酯等聚合物的需求,这些聚合物用于製造各种汽车零件,如转向部件、安全气囊盖、防水地板和保险桿。

- 此外,MDI也用于生产聚氨酯泡棉,聚氨酯泡沫主要用作建筑物的隔热材料。

- 英国土木工程师学会估计,到 2025 年,中国、印度和美国这三大国家将占全球建筑业成长的近 60%。

- 根据美国人口普查局统计,2023年美国建设业年度总额为19,787亿美元,较2022年成长约7.03%。

- 製药业是全球成长最快的市场之一,尤其是在美国、印度和德国。对乙酰胺酚(乙酰胺酚)是一种由苯胺製成的流行止痛药。世界上最受欢迎的学名药是乙酰胺酚。它以锭剂、锭剂和糖浆的形式出售,适合所有年龄层。

- 中国、印度、美国、德国是全球最大的製药工业国。据估计,中国製造商约占全球使用的原料药的 40%。此外,美国进口的原料药75% 至 80% 来自中国和印度。对降低成本和不太严格的环境法规的渴望正在推动中国和印度的製药业发展。

- 根据IQVIA预测,2023年全球医药市场规模为16,070亿美元,成长约8.34%。

- 因此,所有上述因素预计将对未来几年的市场成长产生重大影响。

亚太地区主导市场

- 就消费和生产而言,亚太地区是硝基苯最大的市场,预计在预测期内的调查市场中也将出现最高的成长。由于该地区基础设施不足和人事费用不足,多家外国公司已将其生产设施迁至该地区。硝基苯的生产和消费也受到主要苯胺和二苯基甲烷二异氰酸酯(MDI)生产企业扩大产能的显着影响。

- 由于对黏合剂、密封剂、合成橡胶和聚氨酯等各种基于 MDI 的产品的需求不断增加,建筑业已成为硝基苯最重要的最终用户市场。此外,它还用作木材和家具的粘合剂。为了这些用途,建筑业消耗了全球生产的硝基苯的 48% 以上,其中大部分发生在亚太地区。

- 中国、印度和越南等亚太国家的建设活动强劲成长,预计将在预测期内推动该地区苯胺衍生物的消费。

- 根据美国国际贸易管理局的数据,中国是世界上最大的建筑市场,预计到2030年将以年均8.6%的速度成长。据国家发展和改革委员会(NDRC)称,到2025年,中国已在重大建设计划上投资1.43兆美元。

- 根据中国国家统计局的数据,2023年中国建筑业总产值成长1.99%,达到712,847.2亿元人民币(108,677.8亿美元)。

- 根据住宅及城乡建设部预测,2025年中国建筑业预计将维持GDP的6%。基于这些预测,2022年1月,中国政府宣布了五年计划,透过品质主导发展提高建筑业的永续性。

- 印度的住宅产业也在成长,政府的支持和措施进一步刺激了需求。在2022-2023年预算中,住房与城市发展部(MoHUA)已拨款约98.5亿美元用于住宅建设并筹集资金以完成停滞的计划。

- 因此,所有上述因素预计将对未来几年的市场成长产生重大影响。

硝基苯产业概况

硝基苯市场部分整合。主要参与企业包括(排名不分先后)科思创股份公司、亨斯迈国际有限责任公司、住友化学、万华化学和中国石化集团公司(中石化)。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 苯胺需求增加

- 轻鬆取得原料

- 亚太地区建设活动的成长

- 抑制因素

- 对生物基化学品的需求增加

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 监理政策分析

第五章市场区隔(市场规模(基于数量))

- 目的

- 苯胺生产

- 染料/颜料

- 杀虫剂

- 医药中间体

- 其他用途(溶剂、火药等)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Aarti Industries Ltd.

- Aromsyn Co.,Ltd.

- Bann Quimica Ltda.

- Chemieorganics Chemical India Pvt.Ltd.

- China Petrochemical Corporation(Sinopec)

- Covestro AG

- Huntsman International LLC.

- Sadhana Nitro Chem Ltd.

- SP Chemicals Pte Ltd.

- Sumitomo Chemical Co., Ltd.

- Wanhua

第七章 市场机会及未来趋势

- 建筑业的各类投资

- 其他机会

The Nitrobenzene Market size is estimated at 12.65 million tons in 2025, and is expected to reach 15.58 million tons by 2030, at a CAGR of 4.26% during the forecast period (2025-2030).

The nitrobenzene market was negatively impacted by COVID-19 in 2020. Considering the pandemic scenario, the decrease in demand for various nitrobenzene derivative-based products negatively impacted the market demand. However, the demand for paracetamol derived from the nitrobenzene derivative aniline increased, stimulating the demand for the nitrobenzene market. Nevertheless, the market started to gain pace in the post-pandemic era and was expected to continue the same trajectory.

Key Highlights

- Over the medium term, factors such as the increasing demand for nitrobenzene to produce aniline, the easy availability of raw materials used for production, and the growing construction activities in the Asia-Pacific region, which are contributing to significant demand, are expected to drive the market's growth.

- On the contrary, the growing demand for bio-based chemicals will likely hinder the market's growth.

- Various investments in the construction industry across the globe are likely to act as opportunities for the market studied.

- Asia-Pacific dominated the global market, with the largest consumption from countries such as China, India, etc.

Nitrobenzene Market Trends

Increasing Demand for Aniline Production

- Aniline production applications account for the largest share of nitrobenzene applications, with a share of more than 90%. The catalytic hydrogenation of nitrobenzene majorly produces it.

- India is one of the largest manufacturers and exporters of aniline. According to the Ministry of Chemicals and Fertilizers of India, In FY 2022-2023, aniline production in the country was valued at 39.66 thousand metric tons, which is an increase of about 18.28% as compared to FY 2021-2022.

- The aniline-derived methylene diphenyl diisocyanate (MDI) is a crucial precursor for polymers in various end-use industries, including the building and automotive sectors.

- According to the Organization Internationale des Constructeurs d'Automobiles (OICA), global automotive production in 2022 increased by about 6% and was valued at 85.01 units. This will result in a decline in the demand for MDI-based elastomers and polymers like polyurethane, which are used to make various automotive parts, including steering components, airbag covers, waterproof floor materials, bumpers, and others.

- Furthermore, MDI is used for the production of polyurethane foams, mainly used in various building insulation applications, and acts as one of the significant components in construction, both in their flexible and rigid form.

- As per the estimates of the Institution of Civil Engineers, the top three countries, i.e., China, India, and the United States, will account for almost 60% of all growth in the global construction industry by 2025.

- According to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which is an increase of about 7.03% compared to that of 2022.

- The pharmaceutical sector is one of the global markets with the highest growth, particularly in the United States, India, and Germany. Acetaminophen, or paracetamol, is a popular painkiller produced from aniline. The most popular generic medicine worldwide is paracetamol. For people of all ages, it is commercially offered in tablet, pill, and syrup formulations.

- China, India, the United States, and Germany are the largest pharmaceutical industries in the world. Chinese manufacturers are estimated to make up around 40% of all the APIs used worldwide. Additionally, China and India source 75% to 80% of the APIs imported to the United States. The desire for cost savings and less stringent environmental regulations has driven the pharmaceutical industries in China and India.

- According to IQVIA, the global pharmaceutical market in 2023 was valued at USD 1,607 billion, which is an increase of about 8.34%.

- Therefore, all the abovementioned factors are expected to impact the market's growth significantly in the coming years.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is the largest market for nitrobenzene in terms of consumption and production and is also expected to have the highest growth during the forecast period in the market studied. Various foreign corporations have relocated their manufacturing facilities in the area due to the region's inadequate infrastructure and labor expenses. Production and consumption of nitrobenzene have also been significantly influenced by major aniline and methylene diphenyl diisocyanate (MDI) manufacturing companies expanding their production capacities.

- Due to the increased need for various MDI-based products such as adhesives, sealants, elastomers, and polyurethanes, the construction sector is the most important end-user market for nitrobenzene. Moreover, it is used as a binding agent for wood and furniture. Due to these uses, the construction industry consumes over 48% of the nitrobenzene produced globally, with a significant portion of this consumption occurring in the Asia-Pacific area.

- Asia-Pacific countries, such as China, India, and Vietnam, are registering strong growth in construction activities, which will drive the consumption of these aniline-based derivatives in the region over the forecast period.

- As per the U.S. International Trade Administration, China is the largest market for construction globally and is expected to grow at an annual average rate of 8.6% till 2030. According to the National Development and Reform Commission (NDRC), China is investing USD 1.43 trillion in significant construction projects till 2025.

- According to the National Bureau of Statistics of China, the gross output value of the construction industry in China in 2023 increased by 1.99% and was CNY 71,284.72 billion (USD 10,086.78 billion).

- According to the Ministry of Housing and Urban Rural Development's forecast, China's construction sector is projected to remain at 6 % of its GDP in 2025. In view of these forecasts, in January 202, the Chinese government announced a five-year plan to improve sustainability in the construction industry through quality and driven development.

- In addition, the residential sector in India is growing, and government support and initiatives are further boosting demand. In the budget of 2022-2023, the Ministry of Housing and Urban Development (MoHUA) allocated about USD 9.85 billion to construct houses and create funds to complete the halted projects.

- Therefore, all the abovementioned factors are expected to impact the growth of the market in the coming years significantly.

Nitrobenzene Industry Overview

The Nitrobenzene Market is partially consolidated in nature. Some major players include (not in any particular order) Covestro AG, Huntsman International LLC., Sumitomo Chemical Co., Ltd., Wanhua, and China Petrochemical Corporation (Sinopec), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Aniline

- 4.1.2 Easy Availability of Raw Materials

- 4.1.3 Growing Construction Activities in the Asia-Pacific Region

- 4.2 Restraints

- 4.2.1 Growing Demand for Bio-based Chemicals

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Aniline Production

- 5.1.2 Dyes and Pigments

- 5.1.3 Pesticides

- 5.1.4 Intermediate in Pharmaceuticals

- 5.1.5 Other Applications (including Solvent, Explosives, etc.)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Malaysia

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 NORDIC

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Nigeria

- 5.2.5.4 Qatar

- 5.2.5.5 Egypt

- 5.2.5.6 United Arab Emirates

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aarti Industries Ltd.

- 6.4.2 Aromsyn Co.,Ltd.

- 6.4.3 Bann Quimica Ltda.

- 6.4.4 Chemieorganics Chemical India Pvt.Ltd.

- 6.4.5 China Petrochemical Corporation (Sinopec)

- 6.4.6 Covestro AG

- 6.4.7 Huntsman International LLC.

- 6.4.8 Sadhana Nitro Chem Ltd.

- 6.4.9 SP Chemicals Pte Ltd.

- 6.4.10 Sumitomo Chemical Co., Ltd.

- 6.4.11 Wanhua

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Various Investments in Construction Industry

- 7.2 Other Opportunities