|

市场调查报告书

商品编码

1640440

云端迁移:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Cloud Migration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

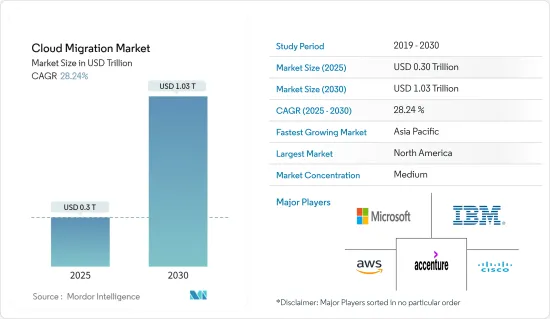

预计云端迁移市场规模在 2025 年将达到 3,000 亿美元,在 2030 年将达到 1.3 兆美元,预测期内(2025-2030 年)的复合年增长率为 28.24%。

在过去十年中,由于中小企业的投资增加,云端运算的采用率有所提高。在全球范围内,许多企业已经迁移到云端平台并正在利用其优势。近年来,云端运算采用已成为 IT 成本削减策略的重要考量。

主要亮点

- 迁移到云端的主要原因是扩充性、提高效率、快速部署、敏捷性和灾难復原。大量公司正在向其客户提供云端灾难復原功能,以帮助他们扩展业务。由于即时体验、业务因素、易于存取内部资料等原因,迁移到云端越来越受欢迎。这项技术也帮助我们在最短的时间内建立了多个业务部门。

- 云端和工业化服务的成长以及传统资料中心外包(DCO)的衰退标誌着混合基础设施服务的巨大转变。虽然传统的DCO市场正在萎缩,但主机託管和主机託管以及基础设施公共事业服务的支出却在蓬勃发展。预计这将导致向云端 IaaS 和託管的转变。近年来,从 PaaS 到 IaaS 再到 SaaS 的转变已变得至关重要。此外,随着企业采用 DevOps 功能和自动化,这些功能越来越被视为实现云端采用的技术和业务优势的关键。

- 云端迁移服务的需求不断增长,其驱动因素包括扩充性、灵活性、远端协作、任务自动化、增强的行动性和强大的资料保护。此外,不断扩大的连网设备网路正在产生大量资料。因此,对低成本资料储存解决方案的需求正在增长,预计这将推动云端迁移服务的采用。

- 与其他云端服务相比,混合云的转变在过去几年中取得了更大的整体成长。混合云允许公司扩展其运算资源,从而无需投入大量资本来满足短期需求高峰。许多云端供应商能够在世界各地快速提升基础设施,使您的业务能够快速扩展到新的地区。

- 资料安全问题和应用程式互通性问题预计会阻碍云端迁移市场的成长。网路连线数位化的不断增强为提供云端迁移服务的公司带来了机会。

云端迁移市场趋势

BFSI:预计大幅成长

- 银行和金融机构正在加速向云端解决方案迁移,因为云端解决方案具有灵活性、敏捷性以及与新兴技术和金融科技生态系统的整合等优势。云端解决方案透过大幅降低基础设施成本来帮助银行减少开支。

- 到2023年,保险和银行业将分别采用11.4和10.9个云端服务。目前,各行各业的公司使用的云端服务大约有八种类型,而且他们通常从多个供应商处采购。

- 许多供应商提供 IaaS 和 PaaS 应用程序,从而无需管理、託管、维护、更新和扩展他们为 BFSI 部门提供的服务。银行普遍认识到云端倡议,包括由人工智慧、区块链和软体容器支援的营运和麵向客户的计划。

- 银行也透过与云端服务供应商建立策略伙伴关係关係来采用云端迁移技术。例如,2022年5月,杰富瑞金融集团与亚马逊合作,将资讯科技服务迁移到云端。这是该金融企业开始进军云端基础软体和资料分析领域的最新倡议。根据这份为期四年的协议,杰富瑞将把公司的关键业务流程、内部和客户导向的应用程式、IT 资源和资料迁移到亚马逊网路服务。

- 为了向客户提供数位银行体验,银行机构正在采用云端迁移技术。例如,2024年6月,全球领先的IT基础设施服务供应商Kindrill宣布与加拿大国家银行扩大合作。目的是加速银行的数位化发展和向云端的过渡。 Kyndryl 长期以来一直致力于加强国家银行的关键基础设施,并带头努力实现银行的现代化。这包括优化工作量、降低技术债务和推动整个组织的创新。

预计北美将占据最大市场占有率

- 北美一直是云端迁移领域的主要创新者和先驱者,占据了相当大的市场。该地区还拥有强大的云端迁移供应商立足点,这推动了该市场的成长。 IBM 公司、微软公司、亚马逊网路服务公司、思科系统公司、Cognizant Technology Solutions Corporation、Google公司等。

- 将资料和应用程式等资讯迁移到云端所带来的好处正在鼓励该地区的许多组织采用云端迁移服务,从而对市场成长产生积极影响。

- 2024 年 3 月,富士通有限公司与亚马逊网路服务 (AWS) 宣布扩大伙伴关係,以加速 AWS 云端上旧有应用程式的现代化。加速现代化联合计画对关键任务应用程式从本地大型主机和 UNIX 伺服器进行评估、迁移和现代化到 AWS 云,支援金融、零售和汽车等行业。

- 此外,2022 年 8 月,总部位于多伦多的自动化云端迁移公司 Next Pathway Inc. 宣布与微软合作,加速将传统资料仓储和资料湖迁移到 Microsoft Azure。 Shift Analyzer 对来源遗留应用程式工作负载进行全面审查,以确定存在哪些程式码类型和物件。 Shift Translator 加速了复杂工作负载(如 SQL、预存程序、ETL 管道/工作流程和其他各种程式码类型)的翻译、测试和迁移。此外,Next Pathway 技术可以轻鬆且有效率地将工作负载从其他云端平台和云端资料仓储迁移到 Azure。

云端迁移产业概览

云端迁移市场适度整合并由几个主要企业组成。从市场占有率来看,目前市场主要被几家主要企业所占据。这些占据较大市场份额的大公司正致力于扩大海外基本客群。这些公司正在利用战略合作计划来增加市场占有率和盈利。

- 2023 年1 月数位解决方案公司LTI Mindtree 宣布已与智慧解决方案供应商Duck Creek Technologies 和Microsoft 合作,创建一项解决方案,让保险公司能够快速且有效率地将其本地核心系统迁移到云端。 。

- 2022 年 2 月:IBM 公司宣布与 SAP 合作,提供技术和咨询技能,帮助企业采用混合云策略,并将关键任务工作负载从 SAP 解决方案迁移到云端。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 价值链分析

- 波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 为组织增加云端运算的益处

- 增加 BYOD 使用率

- 市场挑战

- 资料安全和应用程式互通性问题

第六章 市场细分

- 依部署类型

- 公共云端

- 私有云端

- 混合云端

- 按公司规模

- 中小型企业

- 大型企业

- 按服务类型

- PaaS

- IaaS

- SaaS

- 按行业

- BFSI

- 卫生保健

- 零售

- 政府

- 资讯科技/通讯

- 製造业

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Accenture PLC

- Amazon Inc.

- Cisco Systems Inc.

- Cognizant Technology Solutions Corp

- DXC Technology

- Evolve IP LLC

- Google LLC

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Rackspace Hosting Inc.

- Rightscale Inc.(Flexera)

- Tech Mahindra Ltd

- VMware Inc.

- WSM International LLC

第八章投资分析

第九章:市场的未来

The Cloud Migration Market size is estimated at USD 0.30 trillion in 2025, and is expected to reach USD 1.03 trillion by 2030, at a CAGR of 28.24% during the forecast period (2025-2030).

Over the past decade, cloud computing adoption has risen owing to increasing investments from small and medium enterprises. Globally, many organizations have already switched to cloud platforms to take advantage of its benefits. In recent years, cloud adoption stands to be a significant consideration for IT cost reduction strategies.

Key Highlights

- The significant reasons for migrating to the cloud are scalability, increased effectiveness, faster implementation, mobility, and disaster recovery. Considerable companies are offering cloud disaster recovery features to their customers, aiding them in expanding their businesses. Cloud migration is gaining traction for its real-time experience, business elements, and accessibility to on-premise data. This technology also aids in setting up several business units in minimal time.

- The growth of cloud and industrialized services and the decline of traditional data center outsourcing (DCO) indicate a massive shift toward hybrid infrastructure services. While the conventional DCO market is shrinking, spending on colocation and hosting, along with infrastructure utility services, is increasing rapidly. This is expected to drive the shift toward cloud IaaS and hosting. Migration for PaaS, IaaS, and SaaS has been most important in recent years. Companies are also embracing DevOps capabilities and automation; hence, they are increasingly seen as critical to realizing cloud adoption's technical and business benefits.

- The growing demand for cloud migration services is attributed to increased scalability, flexibility, remote collaboration, task automation, improved mobility, and robust data protection. Furthermore, the growing network of connected devices has resulted in massive data growth. As a result, the growing need for a low-cost data storage solution is projected to increase the use of cloud migration services.

- The migration to the hybrid cloud has experienced significant overall growth in the past few years compared to other cloud services. Using a hybrid cloud allows companies to scale computing resources and helps eliminate the need for massive capital to handle short-term spikes in demand. Many cloud providers offer the ability to rapidly increase infrastructure in various worldwide locations, enabling a business to expand to new territories quickly.

- Data security issues and application interoperability issues are expected to hamper the growth of the cloud migration market. Increased internet connectivity and digitization provide opportunities to the cloud migration service offering companies.

Cloud Migration Market Trends

BFSI Expected to Witness Significant Growth

- Banking and financial organizations are accelerating the migration toward cloud solutions owing to benefits such as flexibility, agility, and integration of emerging technologies and the FinTech ecosystems. Cloud solutions are helping banks cut down expenses by significantly reducing infrastructure costs.

- Such instances have boosted the adoption of cloud services among the BFSI sector as well as other end-user industries, and market vendors are gaining significant traction.By 2023, the insurance and banking industries had adopted 11.4 and 10.9 cloud services each. Currently, businesses across various sectors typically utilize approximately eight cloud services, often sourced from multiple vendors.

- Many vendors are providing IaaS and PaaS applications to eliminate the need to manage, host, maintain, update, and scale service operations targeted toward the BFSI sectors. Banks widely recognize that a cloud infrastructure can help them pursue sweeping modernization initiatives, including operational and customer-facing programs supported by AI, blockchain, and software containers.

- Banks are also adopting Cloud migration technology through strategic partnerships with cloud service-providing companies. For instance, in May 2022, Jefferies Financial Group Inc. is partnering with Amazon to move its information-technology services to the cloud. This is the latest step by a financial business that has just begun to grow into cloud-based software and data analytics. Jefferies is transferring its essential business processes, internal and customer-facing apps, IT resources, and data to Amazon Web Services under a four-year arrangement.

- To provide a digital banking experience to customers, banking organizations are adopting cloud migration technology. For instance, in June 2024, Kyndryl, one of the leading global IT infrastructure service providers, has unveiled an expanded collaboration with the National Bank of Canada. The goal is to expedite the bank's digital evolution and migration to the cloud. Having long been a stalwart in bolstering the National Bank's essential infrastructure, Kyndryl is spearheading efforts to revamp the bank's setup. This includes optimizing workloads, advanced technical liabilities, and fostering innovation throughout the organization.

North America Expected to Hold the Largest Market Share

- North America is among the leading innovators and pioneers in cloud migration and holds a significant share of the market. The region also has a strong foothold on cloud migration vendors, which adds to its growth. Some companies include IBM Corporation, Microsoft Corporation, Amazon Web Services Inc., Cisco Systems Inc., Cognizant Technology Solutions Corporation, and Google Inc.

- The benefits offered by moving data and applications, among other information, to the cloud are pushing many organizations in the region to adopt cloud migration services, thereby impacting the market's growth positively, and also the companies in the North American region are making strategic collaborations, business expansion to propel the cloud migration.

- In March 2024, Fujitsu Limited and Amazon Web Services (AWS) announced an expanded partnership to accelerate the modernization of legacy applications on AWS Cloud. The Modernization Acceleration Joint Initiative will assess, migrate, and modernize mission-critical applications from on-premise mainframes and UNIX servers to AWS Cloud, supporting industries like finance, retail, and automotive.

- Furthermore, in August 2022, Next Pathway Inc., the Automated Cloud Migration company in Toronto, announced a collaboration with Microsoft to accelerate the migration from legacy data warehouses and data lakes to Microsoft Azure. Shift Analyzer provides a comprehensive review of source legacy application workloads to review the code types and objects present. Shift Translator accelerates the translation, testing, and migration of complex workloads such as SQL, Stored Procedures, ETL pipelines/workflows, and various other code types. Furthermore, Next Pathway's technology can easily and efficiently transfer workloads from other cloud platforms and cloud data warehouses to Azure.

Cloud Migration Industry Overview

The cloud migration market is moderately consolidated and consists of several major players. In terms of market share, few major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

- January 2023: Digital solutions firm LTIMindtree announced that it had partnered with Duck Creek Technologies, the intelligent solutions provider, and Microsoft to build a solution enabling insurers to migrate their on-premises core systems to the cloud quickly and efficiently.

- February 2022: IBM Corporation announced a collaboration with SAP to deliver technology and consulting skills to help clients embrace a hybrid cloud strategy and migrate mission-critical workloads from SAP solutions to the cloud in regulated and non-regulated sectors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Benefits Of Cloud To Organizations

- 5.1.2 Increasing Use of BYOD

- 5.2 Market Challenges

- 5.2.1 Data Security And Application Interoperability Issues

6 MARKET SEGMENTATION

- 6.1 By Type of Deployment

- 6.1.1 Public Cloud

- 6.1.2 Private Cloud

- 6.1.3 Hybrid Cloud

- 6.2 By Enterprise Size

- 6.2.1 Small and Medium Enterprises (SMEs)

- 6.2.2 Large Enterprises

- 6.3 By Type of Service

- 6.3.1 PaaS

- 6.3.2 IaaS

- 6.3.3 SaaS

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 Healthcare

- 6.4.3 Retail

- 6.4.4 Government

- 6.4.5 IT and Telecommunication

- 6.4.6 Manufacturing

- 6.4.7 Other End-user Verticals

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 Amazon Inc.

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Cognizant Technology Solutions Corp

- 7.1.5 DXC Technology

- 7.1.6 Evolve IP LLC

- 7.1.7 Google LLC

- 7.1.8 IBM Corporation

- 7.1.9 Microsoft Corporation

- 7.1.10 Oracle Corporation

- 7.1.11 Rackspace Hosting Inc.

- 7.1.12 Rightscale Inc. (Flexera)

- 7.1.13 Tech Mahindra Ltd

- 7.1.14 VMware Inc.

- 7.1.15 WSM International LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

云端迁移服务市场分析与预测(至 2034 年):类型、产品、服务、技术、元件、应用程式、部署、最终用户、解决方案和模式

云端迁移服务市场分析与预测(至 2034 年):类型、产品、服务、技术、元件、应用程式、部署、最终用户、解决方案和模式 云端迁移服务市场规模、份额、趋势和预测(按服务类型、企业规模、部署模式、应用程式、行业垂直和地区),2025 年至 2033 年

云端迁移服务市场规模、份额、趋势和预测(按服务类型、企业规模、部署模式、应用程式、行业垂直和地区),2025 年至 2033 年 云端迁移服务市场:按服务类型、迁移类型、部署模式、垂直产业、公司规模和服务供应商- 全球预测,2025-2032持续智慧市场:按组件、部署、用途、最终用户功能、垂直行业和组织规模划分 - 全球预测 2025-2032

云端迁移服务市场:按服务类型、迁移类型、部署模式、垂直产业、公司规模和服务供应商- 全球预测,2025-2032持续智慧市场:按组件、部署、用途、最终用户功能、垂直行业和组织规模划分 - 全球预测 2025-2032 2025-2029 年全球云端迁移服务市场

2025-2029 年全球云端迁移服务市场 云端迁移服务市场规模、份额、成长分析(按平台类型、按部署、按公司规模、按最终用户、按地区)- 产业预测 2025-2032

云端迁移服务市场规模、份额、成长分析(按平台类型、按部署、按公司规模、按最终用户、按地区)- 产业预测 2025-2032 文件迁移软体市场-按产品类型、应用、地区、预测的全球市场规模2026 年至 2032 年按部署类型、垂直产业和地区分類的云端迁移市场

文件迁移软体市场-按产品类型、应用、地区、预测的全球市场规模2026 年至 2032 年按部署类型、垂直产业和地区分類的云端迁移市场 全球云端迁移服务市场按组件、部署、公司规模、最终用途产业和地区划分

全球云端迁移服务市场按组件、部署、公司规模、最终用途产业和地区划分 全球云端迁移服务市场:市场规模、份额、趋势分析(按平台、公司规模、部署方法、最终用途产业和地区)、展望与未来预测(2024-2031 年)

全球云端迁移服务市场:市场规模、份额、趋势分析(按平台、公司规模、部署方法、最终用途产业和地区)、展望与未来预测(2024-2031 年)