|

市场调查报告书

商品编码

1640474

中东和非洲酰胺纤维:市场占有率分析、行业趋势、统计和成长预测(2025-2030 年)Middle East And Africa Aramid Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

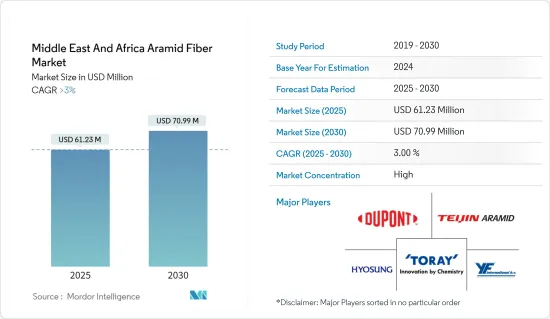

中东和非洲酰胺纤维市场规模预计在 2025 年为 6,123 万美元,预计到 2030 年将达到 7,099 万美元,预测期内(2025-2030 年)的复合年增长率将超过 3%。

由于沙乌地阿拉伯和南非政府实施了多项限制措施,COVID-19 疫情对 2020 年的市场产生了负面影响。不过,自从限制措施解除以来,酰胺纤维市场已经恢復良好。近年来,由于汽车和电子终端用户行业的需求不断增加,市场实现了显着的成长率。

主要亮点

- 酰胺纤维作为钢材的潜在替代品的使用量不断增加,以及汽车产业对轻量材料的需求不断增加,预计将推动市场的发展。

- 酰胺纤维的更好替代品的出现阻碍了市场的成长。

- 预计芳香聚酰胺材料製造技术的进步将在预测期内为市场创造机会。

- 由于汽车、航太和国防以及电气和电子终端用户产业对酰胺纤维的需求不断增长,沙乌地阿拉伯预计将占据市场主导地位。预计在预测期内,其复合年增长率也将达到最高。

中东和非洲酰胺纤维市场趋势

航太和国防占据市场主导地位

- 从热气球和滑翔机到战斗机、客机和太空梭,芳香聚酰胺被用于所有飞机和太空船的零件和结构应用中。酰胺纤维通常用于机翼组件、直升机叶轮、座椅螺旋桨以及仪器和内部组件的外壳。

- 在航太工业中,酰胺纤维在每一代新飞机的建造中都得到了越来越大的应用,以实现全天候运作并改善民航机的视觉系统。此外,温度稳定性和耐用性等特性可能会在未来几年进一步推动航太复合材料市场的成长。

- 在中东和北非地区,政府正在不断探索扩大飞机生产规模的新机会。这促使私营製造商计划在中东地区扩大生产设施。因此,一些公司宣布了在该地区建立新的飞机製造工厂的计划。

- 例如,总部位于杜拜的投资公司Markab Capital于2023年2月与义大利Super Jet International公司签署了一项协议,在阿联酋组装、安装和生产民航机。该工厂计划投资近 1.8 亿美元,生产期间每年可生产 10 至 15 架民航机。

- 同样,沙乌地阿拉伯的航空旅客数量也在增加。根据世界银行集团预测,2022年沙乌地阿拉伯航空旅客人数预计将达3,180万人次,而2021年为2,940万人次,成长率为8%。因此,预计航空客运量的增加将推动该国的飞机市场,从而推动当前的研究市场。

- 因此,预计航太和国防工业的成长将推动该地区酰胺纤维市场的发展。

沙乌地阿拉伯主导市场

- 沙乌地阿拉伯是该地区酰胺纤维的重要市场之一。酰胺纤维用于各种终端用户产业,包括航太和国防、汽车、电气和电子以及体育用品。

- 沙乌地阿拉伯致力于将自己打造为中东新的汽车中心。沙乌地阿拉伯是汽车和汽车零件的进口大国,目前正寻求吸引OEM(目标商标产品製造商)在该国设立生产工厂,以发展国内汽车工业。

- 沙乌地阿拉伯的目标是透过在地化和增加投资机会来发展汽车产业的本地生产能力,以符合该国的国家战略目标「2030愿景」。沙乌地阿拉伯有意发展汽车产业,预计未来 10 年(至 2030 年)国内轻型汽车销量将成长 2.2%。

- 工业和矿产资源部长兼沙乌地阿拉伯工业发展基金(SIDF)主席2022年5月宣布,沙乌地阿拉伯的目标是到2030年每年生产30万辆以上汽车。此外,2022 年汽车销量达到 483,240 辆,而 2021 年为 465,100 辆。

- 总体而言,预计预测期内汽车和电子等行业的成长将推动该国酰胺纤维市场的发展。

中东和非洲酰胺纤维产业概况

中东和非洲的酰胺纤维市场高度整合。市场的主要企业(不分先后顺序)包括杜邦、晓星、帝人芳香聚酰胺、东丽工业公司和 YF International bv。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 汽车产业对轻量材料的需求不断增加

- 越来越多使用酰胺纤维作为钢材的替代品

- 其他驱动因素

- 限制因素

- 酰胺纤维的更好替代品的可用性

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 依产品类型

- 对芳香聚酰胺

- 间芳香聚酰胺

- 按最终用户产业

- 航太和国防

- 车

- 电气和电子

- 体育用品

- 其他终端用户产业(石油和天然气、通讯等)

- 按地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 中东和非洲

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Advanced Materials Technology(Pty)Ltd

- Dupont

- Huvis Corp

- HYOSUNG

- SAERTEX Group

- Tango Engineering

- Teijin Aramid BV

- TORAY INDUSTRIES, INC.

- YF International bv

第七章 市场机会与未来趋势

- 芳香聚酰胺製造技术的进步

- 其他机会

The Middle East And Africa Aramid Fiber Market size is estimated at USD 61.23 million in 2025, and is expected to reach USD 70.99 million by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The COVID-19 pandemic had negatively affected the market in 2020 owing to several restrictions imposed by the governments of Saudi Arabia and South Africa. However, the aramid fiber market recovered well since the restrictions were lifted. In the recent years, the market registered a significant growth rate due to rising demand from the automotive, electronics end-user industries.

Key Highlights

- The increase in the usage of aramid fibers as a potential substitute for steel materials and the increase in demand for lightweight materials in the automotive industry are expected to drive the market.

- The availability of better alternatives for aramid fibers is hindering market growth.

- The advancements in aramid materials manufacturing technology are expected to create opportunities for the market during the forecast period.

- The Saudi Arabia is expected to dominate the market due to the rising demand for aramid fibers from automotive, aerospace and defense, electrical, and electronics end-user industries. It is also expected to register the highest CAGR during the forecast period.

Middle East and Africa Aramid Fiber Market Trends

Aerospace and Defence Sector Dominated the Market

- Aramids are used for components and structural applications in all aircraft and spacecraft, ranging from hot air balloons and gliders to fighter planes, passenger airliners, and space shuttles. The aramid fibers are generally used in wing assemblies, helicopter rotor blades, seat propellers, and enclosures for instruments and internal parts.

- Every year, the aerospace industry uses a higher proportion of aramid fibers in constructing each new generation of aircraft due to the provision of an all-weather operation of commercial aircraft and enhanced vision systems. Moreover, characteristics such as temperature stability and durability will further fuel the growth of the aerospace composites market over the coming years.

- In the Middle East and Africa region, governments are always looking for new opportunities to scale the production of airplanes. This has led private manufacturers to plan their expansion for manufacturing facilities in the Middle East region. Thus several companies have announced the establishment of new aircraft manufacturing facilities in the region.

- For instance, in February 2023, Markab Capital, a Dubai-based investment firm, signed an agreement with Super Jet International, an Italian firm, to assemble, install, and produce civil aircraft in the UAE. The plan is to invest nearly USD 180 million, and the facility can manufacture 10 to 15 civil aircraft annually in the production phase.

- Similarly, air passenger traffic is increasing in Saudi Arabia. According to the World Bank Group, the air passenger traffic in the country registered at 31.8 million in 2022, compared to 29.4 million in 2021, at a growth rate of 8%. Thus the growth in air passenger traffic is excepted to drive the market for airplanes in the country, thereby driving the current studied market.

- Thus, the aerospace and defense industry growth is estimated to drive the region's aramid fibers market.

Saudi Arabia to Dominate the Market

- Saudi Arabia is one of the significant markets for Aramid Fibers in the region. Aramid fibers are used in various end-user industries such as aerospace and defense, Automotive, electric and electronics, and sporting goods.

- Saudi Arabia is focusing on establishing itself as the new automotive hub in the Middle East. Although Saudi Arabia is a large importer of vehicles and auto parts, it is now trying to attract original equipment manufacturers (OEMs) to open their production plants in the country to develop its domestic automotive industry.

- Saudi Arabia aims to localize its automotive sector and increase investment opportunities to help the industry develop local manufacturing capacity and align with the Kingdom's Vision 2030 goals to meet its national strategic goals. The kingdom is interested in developing the sector as domestic light vehicle sales are expected to increase by 2.2% over the next decade by 2030.

- The Minister of Industry and Mineral Resources and Chairman of the Saudi Industrial Development Fund (SIDF) announced in May 2022 that Saudi Arabia is targeting to manufacture more than 300,000 cars annually by 2030. Furthurmore, in 2022 the automotive vehicle sales in the country reached 483.24 thousand units compared to 465.10 thousand units in 2021.

- Overall, the growth of industries such as automotive and electronics will likely drive the market for aramid fibers in the country during the forecast period.

Middle East and Africa Aramid Fiber Industry Overview

The Middle East and Africa aramid fiber market is highly consolidated.Some of the key players in the market (not in any particular order) include Dupont, HYOSUNG, Teijin Aramid, TORAY INDUSTRIES, INC, and YF International bv.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 The Increase in Demand for Light Weight Materials in Automotive Industry

- 4.1.2 The Increase in Usage of Aramid Fibers as a Potential Substitute for Steel Materials

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 The Availability of Better Alternatives For Aramid Fibers

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Para-aramid

- 5.1.2 Meta-aramid

- 5.2 End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Electrical and Electronics

- 5.2.4 Sporting Goods

- 5.2.5 Other End-user Industries (Oil & Gas, Telecommunication, etc.)

- 5.3 By Geography

- 5.3.1 Middle East and Africa

- 5.3.1.1 Saudi Arabia

- 5.3.1.2 South Africa

- 5.3.1.3 Nigeria

- 5.3.1.4 Qatar

- 5.3.1.5 Egypt

- 5.3.1.6 UAE

- 5.3.1.7 Rest of Middle East and Africa

- 5.3.1 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Advanced Materials Technology (Pty) Ltd

- 6.4.2 Dupont

- 6.4.3 Huvis Corp

- 6.4.4 HYOSUNG

- 6.4.5 SAERTEX Group

- 6.4.6 Tango Engineering

- 6.4.7 Teijin Aramid B.V.

- 6.4.8 TORAY INDUSTRIES, INC.

- 6.4.9 YF International bv

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Aramid Materials Manufacturing Technology

- 7.2 Other Opportunities

间位芳香聚酰胺纤维市场规模、份额和成长分析(按等级、应用、纤维类型、终端用户产业和地区划分)-2025-2032年产业预测

间位芳香聚酰胺纤维市场规模、份额和成长分析(按等级、应用、纤维类型、终端用户产业和地区划分)-2025-2032年产业预测 全球芳纶纤维市场(至 2035 年):依产品、生产流程、形态、销售通路、环境因素、应用领域、最终用户、公司、主要地区、产业趋势及预测

全球芳纶纤维市场(至 2035 年):依产品、生产流程、形态、销售通路、环境因素、应用领域、最终用户、公司、主要地区、产业趋势及预测 橡胶输送带用酰胺纤维:全球市占率及排名、总收入及需求预测(2025-2031年)

橡胶输送带用酰胺纤维:全球市占率及排名、总收入及需求预测(2025-2031年) 对位芳香聚酰胺纤维市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2025-2033 年)聚对苯二甲酰对苯二甲酰胺-2025-2031年全球市占率及排名、总营收及需求预测全球间位酰胺纤维市场-市场占有率和排名、总收入和需求预测(2025-2031 年)

对位芳香聚酰胺纤维市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2025-2033 年)聚对苯二甲酰对苯二甲酰胺-2025-2031年全球市占率及排名、总营收及需求预测全球间位酰胺纤维市场-市场占有率和排名、总收入和需求预测(2025-2031 年) 按应用、终端用途产业、产品类型和製造商分類的间位酰胺纤维市场—2025-2032年全球预测酰胺纤维市场按应用、最终用途产业、类型、形式、製造流程和产品划分-2025-2032 年全球预测

按应用、终端用途产业、产品类型和製造商分類的间位酰胺纤维市场—2025-2032年全球预测酰胺纤维市场按应用、最终用途产业、类型、形式、製造流程和产品划分-2025-2032 年全球预测 芳纶纤维市场

芳纶纤维市场 2025年酰胺纤维全球市场报告

2025年酰胺纤维全球市场报告