|

市场调查报告书

商品编码

1640565

氯化钠-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Sodium Chloride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

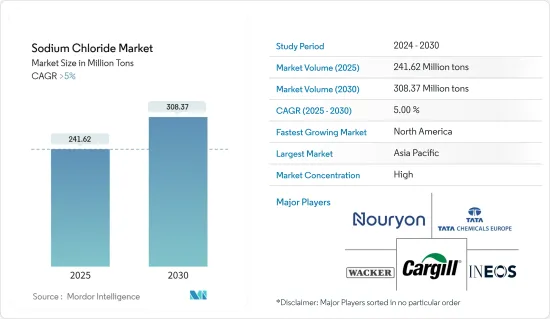

预计 2025 年氯化钠市场规模为 2.4162 亿吨,到 2030 年将达到 3.0837 亿吨,预测期内(2025-2030 年)的复合年增长率将超过 5%。

2020 年 COVID-19 疫情爆发,导致全球建筑工程暂停、化学製造设施关闭,对市场产生了不利影响。然而,预计市场将在预测期内復苏并遵循类似的路径。

关键亮点

- 在北美和欧洲,市场扩张预计将受到食品和饮料行业对氯化钠的需求增加以及对医药级氯化钠的需求的推动。

- 然而,大量性能改良、可用作防腐剂和除冰剂的替代化学品的出现可能会阻碍市场的成长。

- 钠基电池的使用和氯碱产品的生产日益增多,预计将为未来的市场成长提供各种机会。

- 预计亚太地区将主导市场,而北美预计将在整个预测期内快速发展。

氯化钠市场趋势

化学品生产领域占市场主导地位

- 氯化钠用于生产许多化学品,包括有机、无机和氯碱化合物,例如氯、碱灰和苛性钠。这些材料用于製造各种产品,包括聚氯乙烯(PVC)、清洁剂、玻璃、染料和肥皂。

- 碳酸钠(碱灰)用于清洁剂製造、冶金工业以及生产磷酸盐、硅酸盐和玻璃等重化学品。索尔维法使用廉价且广泛可用的石灰石和氯化钠。氨和二氧化碳将盐和石灰石转化为碳酸钠。

- 2023 年上半年,欧盟 27 国、挪威、瑞士和英国生产了约 3,628,468 吨氯。然而,与 2022 年上半年相比,产量下降了 19.4%。 2023 年 9 月的氯气产量与 2022 年 9 月相比增加了 2%。

- 报告称,所生产的氯大部分用于PVC和EDC/VCM应用,约占31.6%,其次是异氰酸酯和含氧酸盐(30.8%)和无机物(12.7%)。

- 根据美国人口普查局的数据,2023 年的建筑价值将达到 1.9787 兆美元,比 2022 年的 1.8487 兆美元高出 7%。这导致对硬质发泡绝缘板和聚氨酯建筑行业材料等 PVC 产品的需求增加。

- 此外,苛性钠,该製程将木材转化为木浆,而烧碱在造纸製程中仍占主导地位。根据《氯碱工业评论》预测,至2023年9月,欧盟27国、挪威、瑞士和英国将生产2,422.5千吨苛性钠,其中有机物占主要份额。

- 因此,由于上述因素,预计化学产品领域将在未来几年占据市场主导地位。

亚太地区占市场主导地位

- 由于化学工业的需求不断增长,亚太地区占据了全球市场占有率的主导地位。中国是化学加工中心,占全球化学产品产量的大部分。

- 根据中国国家统计局统计,中国生产氢氧化钠超过3,900万吨,用于化学品、水处理和金属加工。除了工业用途外,氢氧化钠也常用于家用清洁剂。

- 根据印度投资局(Invest India)发布的统计数据,预计2023-24年(截至2023年8月)印度主要化学品产量将下降至53.54吨,2022-2023年同期将成长至54.32吨以上。然而,截至 2023 年 8 月的有机化学品产量与去年同期相比成长了 4.52%。

- 氯化钠在製药工业中也有多种用途。它们用于製造原料药和其他产品,例如透析溶液、输液、生理食盐水、盐水输液和口服补液盐。

- 根据印度品牌资产基金会(IBEF)预测,到2030年,印度製药业的规模将达到1,300亿美元。中国是全球最大的疫苗生产国,约占全球疫苗总量的60%。它也是世界第三大药品生产国。

- 预计亚太地区将主导氯化钠市场,因为与市场相关的各个细分领域的需求将以某种方式继续增长。

氯化钠行业概况

氯化钠市场由主要企业主导。主要企业(不分先后顺序)包括 Nouryon、嘉吉公司、瓦克化学股份公司、INEOS 和塔塔化学欧洲公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 食品和饮料业对氯化钠的需求不断增加

- 北美和欧洲对医药级氯化钠的需求不断增加

- 限制因素

- 用作防腐剂和除冰剂的新兴替代化学品

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔(市场规模(基于数量))

- 年级

- 岩盐

- 太阳盐

- 真空製盐

- 应用

- 化学製造

- 解冻

- 水质调节

- 农业

- 食品加工

- 药品

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 越南

- 马来西亚

- 印尼

- 泰国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 土耳其

- 义大利

- 北欧的

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 卡达

- 奈及利亚

- 阿拉伯聯合大公国

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Cargill, Incorporated.

- CK Life Sciences Int'l.(Holdings)Inc.

- Compass Minerals

- INEOS

- K+S Aktiengesellschaft

- Nouryon

- Pon Pure Chemicals Group

- Rio Tinto

- Sudwestdeutsche Salzwerke AG

- Swiss Salt Works AG

- Tata Chemicals Europe

- Wacker Chemie AG

第七章 市场机会与未来趋势

- 钠基电池的使用增加

- 增加氯碱产品产量

The Sodium Chloride Market size is estimated at 241.62 million tons in 2025, and is expected to reach 308.37 million tons by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 outbreak in 2020 had a detrimental influence on the market due to the temporary halt in construction operations and the worldwide shutdown of chemical manufacturing facilities. However, the market picked up and is expected to follow a similar projection during the forecast period.

Key Highlights

- The increasing demand for sodium chloride in the food and beverage industry and the demand for pharmaceutical-grade sodium chloride in North America and Europe are expected to fuel the market expansion.

- However, the emergence of numerous alternative chemicals with improved properties that can be utilized as preservatives and deicing agents may stifle market growth.

- The increasing usage of sodium-based batteries and the production of chlor alkali products are expected to offer various opportunities for future market growth.

- Asia-Pacific dominates the market, and North America is predicted to develop quickly throughout the forecast period.

Sodium Chloride Market Trends

The Chemical Production Segment to Dominate the Market

- Sodium chloride produces many chemicals, including organic and inorganic, and chlor alkali compounds, such as chlorine, soda ash, and caustic soda. These materials are then used to make various products, including polyvinyl chloride (PVC), detergents, glass, dyes, and soaps.

- In addition to being utilized in the production of detergents and the metallurgical industry, sodium carbonate (soda ash) is employed in producing heavy chemicals, including phosphates, silicates, and glass. Limestone and sodium chloride, both of which are inexpensive and widely accessible, are used in the Solvay process. Ammonia and carbon dioxide turn salt and limestone into sodium carbonate.

- In the first half of 2023, about 3,628,468 tonnes of chlorine were produced in EU-27 countries, Norway, Switzerland, and the United Kingdom. However, this was a 19.4% decrease in production volume compared to the first half of 2022. In September 2023, an increase of 2% was observed in chlorine production volume over September 2022.

- According to the report, most chlorine produced was used in the PVC, EDC/VCM application, accounting for approximately 31.6%, followed by isocyanates and oxygenates (30.8%) and inorganics (12.7%).

- According to the US Census Bureau, the value of construction in 2023 was USD 1,978.7 billion, 7% above the USD 1,848.7 billion spent in 2022. It, in turn, enhanced the demand for PVC products and polyurethane-based construction industry materials, such as rigid foam insulation panels.

- Furthermore, caustic soda is used in the Kraft process, which converts wood into wood pulp and is still the dominant method in paper manufacturing. According to the Chlor-Alkali Industry Review, 2,422.5 kilotons of caustic soda were produced in EU-27 countries, Norway, Switzerland, and the United Kingdom till September 2023, with organics accounting for the major share.

- Therefore, based on the factors mentioned above, the chemical products segment is expected to dominate the market in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the global market share, with rising demand from the chemical industry. China is a hub for chemical processing, accounting for most chemicals produced globally.

- According to the National Bureau of Statistics of China, the country generated over 39 million metric tons of sodium hydroxide, which is used to make chemicals, water treatment, and metal processing. In addition to industrial use, sodium hydroxide is commonly found in domestic cleaning detergents.

- According to the statistics presented by Invest India, the production of major chemicals in India decreased to 53.54 lakh tonnes during 2023-24 (up to August 2023), with over 54.32 lakh tonnes produced during the corresponding period of 2022-2023. However, the production of organic chemicals up to August 2023, as compared to the corresponding period of the previous year, recorded an increase of 4.52%.

- Sodium chloride also serves its purpose in various applications in the pharmaceutical industry. It is used in manufacturing APIs and other products, such as dialysis and infusion solutions, injections, saline drips, and oral rehydration salts.

- According to the India Brand Equity Foundation (IBEF), the Indian pharmaceutical industry is expected to reach ~USD 130 billion by 2030. The country is the largest producer of vaccines worldwide, accounting for around 60% of the total vaccines globally. Additionally, the country ranks third across the globe for pharmaceutical production by volume.

- With the ever-increasing demands in the different sectors related to the sodium chloride market in one way or another, the market for the same is expected to be dominated by Asia-Pacific.

Sodium Chloride Industry Overview

The sodium chloride market is consolidated among the top players. The key players (not in a particular order) include Nouryon, Cargill Incorporated, Wacker Chemie AG, INEOS, and Tata Chemicals Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Sodium Chloride from Food and Beverage Industry

- 4.1.2 Increasing Demand for Pharmaceutical-grade Sodium Chloride in North America and Europe

- 4.2 Restraints

- 4.2.1 Emergence of Numerous Alternative Chemicals that can be Utilized as Preservatives and Deicing Agents

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Grade

- 5.1.1 Rock Salt

- 5.1.2 Solar Salt

- 5.1.3 Vacuum Salt

- 5.2 Application

- 5.2.1 Chemical Production

- 5.2.2 Deicing

- 5.2.3 Water Conditioning

- 5.2.4 Agriculture

- 5.2.5 Food Processing

- 5.2.6 Pharmaceutical

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Vietnam

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Thailand

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 Italy

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Cargill, Incorporated.

- 6.4.2 CK Life Sciences Int'l. (Holdings) Inc.

- 6.4.3 Compass Minerals

- 6.4.4 INEOS

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Nouryon

- 6.4.7 Pon Pure Chemicals Group

- 6.4.8 Rio Tinto

- 6.4.9 Sudwestdeutsche Salzwerke AG

- 6.4.10 Swiss Salt Works AG

- 6.4.11 Tata Chemicals Europe

- 6.4.12 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Sodium-based Batteries

- 7.2 Increasing Production of Chlor-alkali Products

2026-2034年全球亚硫酸钠市场规模、份额、趋势和成长分析报告

2026-2034年全球亚硫酸钠市场规模、份额、趋势和成长分析报告 2026年全球氯化钠市场报告

2026年全球氯化钠市场报告 氯化钠注射液市场按产品类型、包装类型、给药途径、应用、最终用途和分销管道划分,全球预测(2026-2032年)

氯化钠注射液市场按产品类型、包装类型、给药途径、应用、最终用途和分销管道划分,全球预测(2026-2032年) 氯化钠市场规模、份额及成长分析(按类型、等级、应用及地区划分)-2026-2033年产业预测

氯化钠市场规模、份额及成长分析(按类型、等级、应用及地区划分)-2026-2033年产业预测 氯酸钠市场规模、份额及成长分析(按类型、应用、最终用户和地区划分)-2026-2033年产业预测

氯酸钠市场规模、份额及成长分析(按类型、应用、最终用户和地区划分)-2026-2033年产业预测 全球药用级氯化钠市场按等级、应用和地区划分-预测至2030年全球氯化钠市场(按形态、纯度、来源、最终用户、应用和分销管道划分)预测 2025-2032

全球药用级氯化钠市场按等级、应用和地区划分-预测至2030年全球氯化钠市场(按形态、纯度、来源、最终用户、应用和分销管道划分)预测 2025-2032 亚硫酸钠市场:全球2025-2029全球氯化钠市场规模(按来源、应用、地区和预测)

亚硫酸钠市场:全球2025-2029全球氯化钠市场规模(按来源、应用、地区和预测) 2032 年氯化钠市场预测:按原料、形态、等级、製造流程、应用、最终用户和地区进行的全球分析

2032 年氯化钠市场预测:按原料、形态、等级、製造流程、应用、最终用户和地区进行的全球分析