|

市场调查报告书

商品编码

1640599

对二甲苯 (PX):市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Paraxylene (PX) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

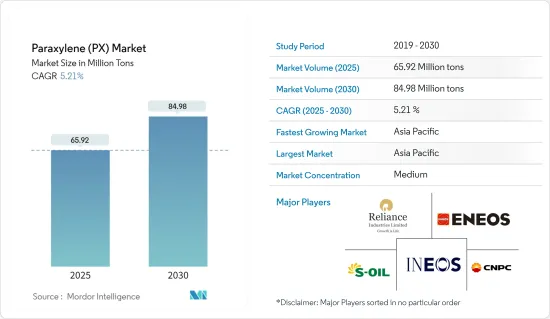

预计2025年对二甲苯市场规模为6,592万吨,2030年将达到8,498万吨,预测期间(2025-2030年)的复合年增长率为5.21%。

2020 年的市场受到了 COVID-19 的一定影响。纯对苯二甲酸是一种对二甲苯产品,用于製造汽车涂料配方中的聚酯耐腐蚀树脂。汽车产业的衰退和汽车製造的暂时停顿对市场产生了负面影响。然而,面罩、透明口罩、食品和电子商务包装的使用增加推动了对二甲苯衍生物的需求。此外,精对苯二甲酸、对苯二甲酸二甲酯和聚对苯二甲酸乙二酯也推动了对二甲苯的需求。

关键亮点

- 短期内,亚太地区塑胶产业对聚对苯二甲酸乙二醇酯 (PET) 的高需求预计将推动市场成长。

- 然而,消费者对无塑胶产品意识的不断增强以及欧洲 PET 的收集和回收率低阻碍了市场的成长。

- 生质塑胶宝特瓶(bio-PET)和其他生质塑胶产品中使用生物基对二甲苯的技术创新可能会在未来几年为市场创造机会。

- 预计亚太地区将主导市场,并在预测期内以最高的复合年增长率成长。

对二甲苯的市场趋势

塑胶产业需求不断成长

- 对二甲苯是製造聚对苯二甲酸乙二醇酯(PET)塑胶和聚酯织物等的成分。

- 精对苯二甲酸(PTA)是一种由石油二次产物对二甲苯(PX)与乙酸反应生成的有机化合物。

- PTA主要用于聚酯薄膜、宝特瓶、家具等聚酯的生产。它也用于製造高性能塑料,如聚对聚丁烯对苯二甲酸酯(PBT) 和对苯二甲酸二甲酯 (DMT)。

- 汽车、食品饮料、电子和建筑行业产量的不断增长推动了对 PET 和 PBT 等塑胶的需求。这可能会导致对高性能塑胶的需求增加和产量增加。

- 根据中国国家统计局的数据,2022年上半年塑胶製品产量约3,821万吨。 2021年塑胶製品产量与前一年同期比较%。

- 2021 年 5 月,石化製造商 Indorama Ventures Ltd 的子公司 Indo Rama Synthetics (India) Limited (IRSL) 宣布计划投资高达 60 亿印度卢比(约 7,243 万美元)扩大其 PET 树脂产能。这将涉及位于印度纳格浦尔的製造工厂每天额外增加 700 吨的产能和资本升级计划,生产将于 2022 年最后一个季度开始。

- 由于上述因素,对二甲苯(PX)市场在预测期内可能会成长。

中国主宰亚太地区

- 在亚太地区,中国已成为世界上最大的生产国之一。目前,它是全球最大的对二甲苯生产国和消费国。

- 中国石油天然气集团公司是最大的对二甲苯生产商之一,年产量达100万吨。中石油的PTA技术是一种以对二甲苯为原料生产PET的有效且经济的方法。

- 中国对 PET 的需求不断增长,正在强化 PET 价值链并快速推动对二甲苯市场的发展。 2022年,中国将占全球PET产能的约38%。包装和纺织业对 PET 的需求不断增长,促使中国多年来不断提高其生产能力。

- 中国是PET树脂主要生产国,其中中油集团和江苏三房巷是全球产量最大的生产商,产能都超过200万吨。因此,终端用户产业对 PET 的需求不断增加,推动了对二甲苯的需求。

- 纺织业是中国支柱产业之一,也是全球最大的服饰出口国。根据中国国家统计局的数据,预计2022年中国纺织品产量将达382亿公尺。 2023年前两个月,我国纺织品产量达50亿公尺。

- 电子商务的兴起和中国人口的成长使其更加註重技术,预计这将推动对塑胶树脂的需求。推动这项需求成长的主要动力将来自中国电子商务、食品生产以及食品和饮料消费等产业。

- 因此,由于终端用户产业的需求不断增加,对二甲苯市场在预测期内可能会成长。

对二甲苯产业概况

对二甲苯(PX)市场部分整合。从市场占有率来看,目前市场主要被少数几家大公司占据。市场的主要企业(不分先后顺序)包括 ENEOS Corporation、INEOS、Reliance Industries Limited、S-OIL Corporation 和中国石油天然气集团公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 聚对苯二甲酸乙二醇酯(PET)需求旺盛

- 其他驱动因素

- 限制因素

- 提高消费者对使用无塑胶产品的意识

- 欧洲的 PET 收集和回收率

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔(市场规模(基于数量))

- 应用

- 精对苯二甲酸(PTA)

- 对苯二甲酸二甲酯 (DMT)

- 其他的

- 最终用户产业

- 塑胶

- 纤维

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Braskem

- China National Petroleum Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- INEOS

- Indian Oil Corporation Limited

- Mangalore Refinery & Petrochemicals Ltd

- MITSUBISHI GAS CHEMICAL COMPANY INC.

- National Petrochemical Company

- PT Pertamina(Persero)

- Reliance Industries Limited

- Rongsheng Petrochemical Co. Ltd

- SK Innovation Co. Ltd

- China Petroleum & Chemical Corporation

- S-Oil Corporation

第七章 市场机会与未来趋势

- 生物基对二甲苯在生质塑胶宝特瓶(BioPET)和其他生质塑胶产品的创新应用。

The Paraxylene Market size is estimated at 65.92 million tons in 2025, and is expected to reach 84.98 million tons by 2030, at a CAGR of 5.21% during the forecast period (2025-2030).

The market was moderately impacted by COVID-19 in 2020. Purified terephthalic acid, a paraxylene product, was used to manufacture polyester coating resins in the formulation of automotive coatings. The declining automotive industry and the temporary shutdown of automotive manufacturing negatively impacted the market. However, face shields, transparent masks, food, and e-commerce packaging usage increased, thus boosting the demand for paraxylene derivatives. It also includes purified terephthalate acid, dimethyl terephthalate, and polyethylene terephthalate, further augmenting the demand for paraxylene.

Key Highlights

- Over the short term, the high demand for polyethylene terephthalate (PET) from the plastic industry in Asia-Pacific is expected to drive the market's growth.

- However, increasing consumer awareness regarding plastic-free products and PET collection and recycling rates in Europe are hindering the market's growth.

- Innovation in using bio-based paraxylene in bioplastic PET bottles (Bio-PET) and other bioplastic products will likely create opportunities for the market in the coming years.

- The Asia-Pacific region is expected to dominate the market and register the highest CAGR during the forecast period.

Paraxylene Market Trends

Increasing Demand from Plastic Industries

- Paraxylene is a building block for manufacturing polyethylene terephthalate (PET) plastics, polyester fabrics, and others.

- Purified terephthalic acid (PTA) is an organic compound produced by reacting secondary petroleum product paraxylene (PX) and acetic acid.

- PTA is majorly used to produce polyesters, such as polyester films, PET bottles, and furniture. It is also used in making high-performance plastics, such as polybutylene terephthalate (PBT) and dimethyl-terephthalate (DMT).

- The increasing production in the automotive, food and beverage, electronics, and construction industries is boosting the demand for plastics, such as PET and PBT. Thus, it increases demand for high-performance plastics, likely increasing their production.

- According to the National Bureau of Statistics of China, around 38.21 million metric tons of plastic products were produced in the first half of 2022. In 2021, plastic product production increased by around 5.27% over the previous year.

- In May 2021, Indo Rama Synthetics (India) Limited (IRSL), a subsidiary of petrochemical producer Indorama Ventures Ltd, announced its plans to invest up to INR 6 billion (~USD 72.43 million) for the capacity expansion of PET resin. It comes with an additional 700-ton capacity per day and an equipment upgrading program in the manufacturing facility in Nagpur, India, to start production in the last quarter of 2022.

- Due to the abovementioned factors, the paraxylene (PX) market will likely grow during the forecast period.

China to Dominate the Asia-Pacific Region

- In Asia-Pacific, China emerged as one of the biggest production houses in the world. Presently, it is also the largest manufacturer and consumer of Paraxylene.

- China National Petroleum Corporation is one of the largest producers of Paraxylene, with an annual production quantity of 1 million tons. CNPC PTA technology is effective in using Paraxylene as an input to produce PET through a cost-effective method.

- Growing demand for PET in China is ramping up the PET value chain, rapidly driving the market for Paraxylene. In 2022 China accounted for around 38% of the global PET production capacity. Due to the growing demand for PET from the packaging and textile industries, China included added capacities through the years.

- China is a major producer of PET resins, with the PetroChina Group and Jiangsu Sangfangxiang among the largest global manufacturers in terms of volume, with more than 2 million ton capacities. Thus, the rising demand for PET from end-user industries is driving the demand for Paraxylene.

- China's textile industry is one of the major industries, and the country is the largest clothing exporter worldwide. According to the National Bureau of Statistics of China, textile production in the country stood at 38.20 billion m in 2022. In the first two months of 2023, the country produced 5 billion m of textiles.

- Due to rising e-commerce and increasing tech-savviness among the growing Chinese population, the demand for plastic resins is also expected to increase. This increase in demand is particularly driven by China's e-commerce, food production, and beverage consumption, among many others.

- Therefore, the market for Paraxylene will likely grow due to the rising demand from end-user industries during the forecast period.

Paraxylene Industry Overview

The paraxylene (PX) market is partially consolidated. By market share, few major players currently dominate the market. Some of the market's major players (not in any particular order) include ENEOS Corporation, INEOS, Reliance Industries Limited, S-OIL Corporation, and China National Petroleum Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Demand for Polyethylene Terephthalate (PET)

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Increase in Consumer Awareness Regarding the Use of Plastic-free Products

- 4.2.2 PET Collection and Recycling Rates in Europe

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Purified Terephthalic Acid (PTA)

- 5.1.2 Dimethyl Terephthalate (DMT)

- 5.1.3 Other Applications

- 5.2 End-user Industry

- 5.2.1 Plastics

- 5.2.2 Textile

- 5.2.3 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Braskem

- 6.4.2 China National Petroleum Corporation

- 6.4.3 ENEOS Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- 6.4.6 INEOS

- 6.4.7 Indian Oil Corporation Limited

- 6.4.8 Mangalore Refinery & Petrochemicals Ltd

- 6.4.9 MITSUBISHI GAS CHEMICAL COMPANY INC.

- 6.4.10 National Petrochemical Company

- 6.4.11 PT Pertamina (Persero)

- 6.4.12 Reliance Industries Limited

- 6.4.13 Rongsheng Petrochemical Co. Ltd

- 6.4.14 S.K. Innovation Co. Ltd

- 6.4.15 China Petroleum & Chemical Corporation

- 6.4.16 S-Oil Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation in the Use of Bio-based Paraxylene in Bioplastic PET Bottles (Bio-PET) and Other Bioplastic Products.

对二甲苯市场规模、份额及成长分析(按应用、类型、终端用户产业及地区划分)-2026-2033年产业预测

对二甲苯市场规模、份额及成长分析(按应用、类型、终端用户产业及地区划分)-2026-2033年产业预测 对二甲苯市场按应用、最终用途产业、製造流程、通路和纯度等级划分-2025-2032 年全球预测

对二甲苯市场按应用、最终用途产业、製造流程、通路和纯度等级划分-2025-2032 年全球预测 全球生物基对二甲苯市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球生物基对二甲苯市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 对二甲苯 (PX) 市场报告(按应用(精对苯二甲酸 (PTA)、对苯二甲酸二甲酯 (DMT) 等)、最终用途行业(塑料、纺织品等)和地区)2025 年至 2033 年

对二甲苯 (PX) 市场报告(按应用(精对苯二甲酸 (PTA)、对苯二甲酸二甲酯 (DMT) 等)、最终用途行业(塑料、纺织品等)和地区)2025 年至 2033 年 对二甲苯市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年

对二甲苯市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年