|

市场调查报告书

商品编码

1641850

聚硅氧烷:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Polysiloxane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

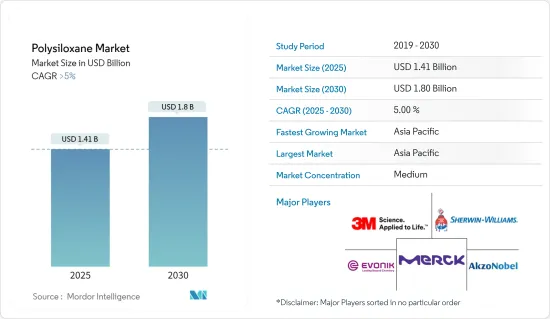

聚硅氧烷市场规模预计在 2025 年为 14.1 亿美元,预计到 2030 年将达到 18 亿美元,预测期内(2025-2030 年)的复合年增长率将超过 5%。

主要亮点

- 新冠肺炎疫情为市场带来了负面影响,减缓了生产和流动,并迫使交通运输和基础设施等行业因防控措施和经济混乱而推迟生产。现在,市场正从疫情中復苏。预计2022年市场将达到疫情前的水准并持续稳定成长。

- 推动研究市场成长的主要因素是防护涂料和工业涂料的应用日益广泛及其在医疗保健产业的广泛应用。技术缺陷和与其他材料和添加剂的不相容可能会阻碍市场成长。

- 持续研究和开发聚硅氧烷技术以实现新的应用开发可能会在未来几年为市场创造机会。预计亚太地区将主导市场,并在预测期内以最高的复合年增长率成长。

聚硅氧烷市场趋势

电子产业需求增加

- 聚硅氧烷因具有优异的溶解性、成膜性、对各种基材的适度附着力、优异的散热性、无毒、低介电常数、优异的耐热性和耐化学性而用于有机发光二极体(OLED)。

- 电气和电子行业的使用量不断增加以及广泛的应用预计将推动全球市场的成长。

- 例如,根据日本电子情报技术产业协会(JEITA)的数据,全球电子和IT产业的产值预计将从2021年的3,4159亿美元与前一年同期比较到2022年的3,4368亿美元。预计到2023年终将达到35,266亿美元,与前一年同期比较增3%。

- 此外,根据电子和资讯科技部的数据,2022财年印度全国消费电子产品(电视、配件和音讯)的产值预计将超过7,450亿印度卢比(94.6亿美元)。这就是我们支持市场成长的方式。

- 预计这种强劲的成长将在整个预测期内推动电子产业的聚硅氧烷消费量。

亚太地区占市场主导地位

- 亚太地区在市场研究中占最大份额,主要由中国、印度、日本和韩国等国家推动。这是因为该国拥有大型医疗设备、黏合剂和密封剂、合成橡胶、电子产品等生产基地。

- 2023年6月,汉高宣布将在中国增加一个新的黏合剂生产工厂。在中国山东省烟台化学工业园区建造汉高黏合剂技术新生产基地。新工厂「鲯鹏」的建设成本约为人民币8.7亿元(1.19亿美元)。新工厂将增加汉高在中国的耐衝击黏合剂产品的产能,并进一步优化供应链,以满足国内外市场日益增长的需求,从而有利于市场成长。

- 此外,2023年5月,黏合剂製造商Jowat宣布将在中国建立自己的黏合剂中心,扩大在亚太地区的业务。亚洲新黏合剂中心占地将超过 11,000平方公尺,计划于 2023年终完工。

- 此外,中国是世界上最大的电子产品製造基地。智慧型手机、 有机发光二极体电视、平板设备、电线电缆等电子产品在电子产业中成长最快。该国不仅满足国内电子产品需求,还将电子产品出口到其他国家。由于中国中产阶级的可支配收入不断增加,以及从中国进口电子产品的国家对电子产品的需求不断增加,预计预测期内电子产品产量将进一步增长。

- 中国製造商正在建立海外生产基地,以打入国际电子市场。例如,TCL正在透过在越南、马来西亚、墨西哥和印度设立海外工厂生产电视、模组和太阳能电池来扩大其在国际市场的影响力。此外,我们也与当地企业伙伴关係,共同开发生产设施、供应链和研发基础设施。

- 由于上述因素,预计预测期内聚硅氧烷的需求将会增加。

聚硅氧烷产业概况

聚硅氧烷市场部分整合。研究的市场中的主要企业(不分先后顺序)包括 3M、阿克苏诺贝尔公司、赢创工业集团、默克公司、宣威公司、瓦克化学公司等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 扩大防护涂料和工业涂料的应用

- 医疗产业广泛应用

- 扩大光电子领域的应用

- 限制因素

- 技术缺陷以及与其他材料和添加剂的不相容性

- 其他阻碍因素

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 按应用

- 医疗

- 油漆和涂料

- 无机聚硅氧烷

- 环氧-聚硅氧烷杂化材料

- 丙烯酸-聚硅氧烷混合物

- 黏合剂和密封剂

- 合成橡胶

- 有机电子材料

- 织物

- 其他用途(个人护理、化妆品等)

- 按最终用户产业

- 卫生保健

- 石油和天然气

- 力量

- 基础设施

- 运输

- 电子产品

- 饮食

- 纺织品

- 其他最终用户产业(膜、消泡剂等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- Akzo Nobel NV

- Asian Paints

- Biro Technology Inc.

- Dampney Company

- Evonik Industries AG

- Gelest Inc.

- Huntsman Corporation LLC

- Merck KGaA

- Restek Corporation

- The Sherwin-Williams Company

- Wacker Chemie AG

第七章 市场机会与未来趋势

- 持续研发聚硅氧烷技术,拓展新应用领域

- 其他机会

简介目录

Product Code: 59591

The Polysiloxane Market size is estimated at USD 1.41 billion in 2025, and is expected to reach USD 1.80 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

Key Highlights

- The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as transportation, infrastructure, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The major factors driving the growth of the market studied are the growing usage of protective and industrial coatings and vast applications in the healthcare industry. Technological drawbacks and incompatibility with a few other materials or additives are likely to hinder the growth of the market.

- Continuous R&D of polysiloxane technologies for the development of newer applications is likely to create opportunities for the market in the coming years. Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Polysiloxane Market Trends

Increasing Demand from Electronics Sector

- Polysiloxanes, owing to their good solubility, film-forming ability, fair adhesion to various substrates, excellent heat radiation, non-toxic characteristics, low dielectric constants, and superior thermal & chemical resistivity, are widely used to manufacture electronic items such as organic light-emitting diodes (OLEDs), solar cells, electrical memories, and liquid crystalline materials, among other products.

- The increasing usage and wide areas of application in the electrical and electronics industry are expected to drive market growth across the globe.

- For instance, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year on year, compared to USD 3,415.9 billion in 2021. Moreover, the industry was expected to reach USD 3,526.6 billion, with a growth rate of 3% year on year, at the end of 2023.

- Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022. Thus supporting the growth of the market.

- Such positive growth is expected to increase the consumption of polysiloxane in the electronics sector through the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounted for the largest share of the market studied, mainly driven by countries such as China, India, Japan, and South Korea. Owing to its large production base of medical devices, adhesives and sealants, elastomers, electronics, etc.

- In June 2023, Henkel announced the addition of a New adhesive Manufacturing Facility in China. The new manufacturing facility of Henkel Adhesive Technologies in the Yantai chemical industry park in Shandong province, China. The new plant, 'Kunpeng,' will cost approximately CNY 870 million (USD 119 million). The new plant will increase Henkel's production capacity of high-impact adhesive products in China and further optimize the supply chain to meet the increasing demand from domestic and foreign markets, which in turn is expected to benefit the market growth.

- Moreover, in May 2023, Jowat, the adhesive manufacturer, announced to expand its presence in Asia-Pacific with the establishment of its own adhesive center in China. The new adhesive center in Asia will have a surface area of more than 11,000 sq meters and is planned to be finished by the end of 2023.

- Furthermore, China has the world's largest electronics production base. Electronic products, such as smartphones, OLED TVs, tablets, wires, and cables, recorded the highest growth in the electronics segment. The country not only serves the domestic demand for electronics but also exports electronic output to other countries. Owing to the increase in the disposable incomes of the middle-class population in China and the rising demand for electronic products in the countries that import electronic products from China, the production of electronics is estimated to grow further during the forecast period.

- The Chinese manufacturers are setting up overseas production bases in order to expand in the electronics international markets. For instance, TCL has broadened its presence in international markets by establishing factories abroad, producing televisions, modules, and photovoltaic cells in Vietnam, Malaysia, Mexico, and India. In addition, it has formed partnerships with local companies in Brazil to collaboratively develop production facilities, supply chains, and an R&D infrastructure.

- The factors above are expected to boost the demand for polysiloxane in the region during the forecast period.

Polysiloxane Industry Overview

The polysiloxane market is partially consolidated in nature. The major players in the studied market (not in any particular order) include 3M, Akzo Nobel N.V., Evonik Industries AG, Merck KGaA, The Sherwin-Williams Company, and Wacker Chemie AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Protective and Industrial Coatings

- 4.1.2 Vast Applications in the Healthcare Industry

- 4.1.3 Augmenting Usage in Optoelectronic Applications

- 4.2 Restraints

- 4.2.1 Technological Drawbacks and Incompatibility with Few Other Materials or Additives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Medical

- 5.1.2 Paints and Coatings

- 5.1.2.1 Inorganic Polysiloxane

- 5.1.2.2 Epoxy-Polysiloxane Hybrids

- 5.1.2.3 Acrylic-Polysiloxane Hybrids

- 5.1.3 Adhesives and Sealants

- 5.1.4 Elastomers

- 5.1.5 Organo Electronic Materials

- 5.1.6 Fabrics

- 5.1.7 Other Applications (Personal Care, Cosmetics, Etc.)

- 5.2 End-user Industry

- 5.2.1 Healthcare

- 5.2.2 Oil and Gas

- 5.2.3 Power

- 5.2.4 Infrastructure

- 5.2.5 Transportation

- 5.2.6 Electronics

- 5.2.7 Food and Beverage

- 5.2.8 Textile

- 5.2.9 Other End-user Industries (Membranes, Antifoaming Agents, Etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Asian Paints

- 6.4.4 Biro Technology Inc.

- 6.4.5 Dampney Company

- 6.4.6 Evonik Industries AG

- 6.4.7 Gelest Inc.

- 6.4.8 Huntsman Corporation LLC

- 6.4.9 Merck KGaA

- 6.4.10 Restek Corporation

- 6.4.11 The Sherwin-Williams Company

- 6.4.12 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Continuous R&D of Polysiloxane Technologies for Development of Newer Applications

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

环戊硅氧烷市场规模、份额和成长分析(按配方类型、最终用途、分销管道和地区划分)-2026-2033年产业预测

环戊硅氧烷市场规模、份额和成长分析(按配方类型、最终用途、分销管道和地区划分)-2026-2033年产业预测 环氧官能化硅氧烷市场按类型、物理形态、应用和最终用途产业划分,全球预测(2026-2032年)聚醚型消泡剂市场依产品类型、化学类型、物理形态、终端用户产业及通路划分,全球预测(2026-2032年)聚醚改质消泡剂市场:按配方、产业应用和最终用途划分,全球预测(2026-2032年)

环氧官能化硅氧烷市场按类型、物理形态、应用和最终用途产业划分,全球预测(2026-2032年)聚醚型消泡剂市场依产品类型、化学类型、物理形态、终端用户产业及通路划分,全球预测(2026-2032年)聚醚改质消泡剂市场:按配方、产业应用和最终用途划分,全球预测(2026-2032年) 聚硅氧烷市场-2026-2031年预测

聚硅氧烷市场-2026-2031年预测 全球十甲基环戊硅氧烷市场:市场规模、份额、趋势分析(按等级、应用和地区划分)、细分市场预测(2025-2033 年)

全球十甲基环戊硅氧烷市场:市场规模、份额、趋势分析(按等级、应用和地区划分)、细分市场预测(2025-2033 年) 全球聚硅氧烷市场

全球聚硅氧烷市场 2032年聚醚改质聚硅氧烷市场预测:按形态、等级、最终用户和地区分類的全球分析全球聚醚改质聚硅氧烷市场

2032年聚醚改质聚硅氧烷市场预测:按形态、等级、最终用户和地区分類的全球分析全球聚醚改质聚硅氧烷市场 聚醚改质聚硅氧烷市场报告:趋势、预测与竞争分析(至2031年)

聚醚改质聚硅氧烷市场报告:趋势、预测与竞争分析(至2031年)