|

市场调查报告书

商品编码

1641858

託管IT基础设施服务 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Managed IT Infrastructure Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

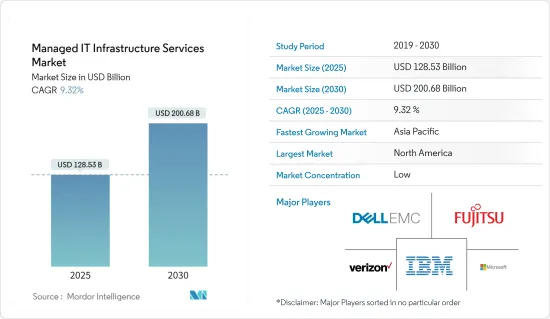

託管IT基础设施服务市场规模在 2025 年估计为 1,285.3 亿美元,预计到 2030 年将达到 2006.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 9.32%。

关键亮点

- 企业在努力维持IT基础设施以最佳效能水准运作与管理相关成本之间取得平衡,越来越多地转向供应商提供基础架构服务。託管基础设施服务可协助各行业专注于其核心业务。

- 这些服务主要应用于 IT 产业,该产业中成本优化、专注于核心竞争力和资料安全仍然是主要关注点。然而,最近云端基础的技术的广泛采用和技术进步极大地促进了这一趋势。

- 巨量资料等技术的广泛应用进一步增加了外包IT服务的需求。透过利用巨量资料和云端的结合,企业可以提供可扩展且经济高效的解决方案。例如,亚马逊的「Elastic Map Reduce」展示瞭如何利用云端的弹性运算能力进行巨量资料处理。

- 此外,更新老化硬体的需求也是市场的一个驱动因素。根据Spice works Inc. 的一项调查,在接受调查的700 家公司中,64% 的公司认为更新过时的资讯技术(IT) 基础设施的必要性和安全性问题是IT 预算过高的主要原因。答案是肯定的。

託管IT基础设施服务市场趋势

云端基础的技术的传播和发展将补充需求

- 在当前的市场情况下,对云端服务的依赖性不断增加以及基础设施升级活动是推动託管IT基础设施服务需求的关键因素。事实上,未来几年大部分基础设施开发将是为了支援日益增长的云端服务需求。

- IT基础设施本身的格局正在快速改变。随着越来越多的企业将其大部分或全部 IT 服务和应用程式迁移到云端,传统的存储伺服器正在迅速消失。因此,随着企业增加对先进云端基础设施的投资,预计预测期内甚至对传统IT基础设施的投资也会下降。

- 此外,根据思科全球云端指数报告,到今年,90% 以上的工作负载将云端基础。全球云端流量将占所有资料中心流量的95%。同时,传统资料中心的工作量和计算实例预计在同一时期内也会下降。从历史上看,单一伺服器负责一个工作负载和计算实例。然而,随着伺服器运算能力和虚拟的增加,每个实体伺服器的多个工作负载和运算实例在云端架构中变得越来越普遍。

北美占有最大市场占有率

- 由于技术采用速度快且 IT资料中心数量众多,北美仍是託管IT基础设施服务的最大市场。

- 由于强大的IT基础设施、法律、标准和技术经验,北美在过去几年中经历了云端迁移的急剧增长。此外,北美云端迁移服务市场的扩张也受到亚马逊网路服务、IBM 公司、微软公司、谷歌和思科系统公司等知名云端运算公司的推动。

- 另一个因素是多个终端使用者产业的高度自动化和 IT 应用的大规模普及,使得该地区对IT基础设施服务的需求持续存在。

管理IT基础设施服务业概况

託管IT基础设施服务市场竞争激烈,参与企业。随着市场变得更加分散,扩大策略越来越专注于收购和细分市场。随着所提供服务的性质不断演变,所有参与企业必须继续投资新时代的技能和技术,以保持相关性并在竞争中保持领先。只有透过聘用合适的研发人才或收购有可能颠覆这一领域的有趣的新兴企业才能实现这一目标。与大公司相比,中小企业的优势在于,由于他们的资料中心位于本地,因此可以更好地服务本地市场。因此,大公司被迫积极进行收购,以加强其全球企业发展。

2022年8月,戴尔科技宣布推出与VMware共同设计的全新基础架构解决方案。

2022年3月,Verizon Communications Inc.表示,将在2022年终将其5G超宽频网路扩展到1.75亿人。该公司概述了几个成长槓桿,包括5G移动性、全国宽频、行动边缘运算(MEC)、业务解决方案、价值市场和网路收益,这些将推动服务和其他收益成长。展望。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查假设和定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 拥抱市场动态

- 市场驱动因素

- 透过引入託管服务来优化成本

- 云端基础技术的传播和发展是驱动因素

- 市场限制

- 安全和隐私问题是限制因素

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按服务类别

- 虚拟

- 联网

- 贮存

- 伺服器

- 按公司规模

- 中小企业

- 大型企业

- 按部署

- 本地

- 云

- 按最终用户

- 资讯科技/通讯

- 零售

- 运输和物流

- BFSI

- 製造业

- 其他的

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Fujitsu Ltd.

- CSS Corp Pvt Ltd.

- Dell EMC(EMC Corporation)

- IBM Corporation

- Alcatel-Lucent SA(Nokia Corporation)

- Microsoft Corporation

- Verizon Communications Inc.

- Citrix Systems Inc.

- Tata Consultancy Services Limited

- Deutsche Telekom AG

第七章投资分析

第八章 市场机会与未来趋势

The Managed IT Infrastructure Services Market size is estimated at USD 128.53 billion in 2025, and is expected to reach USD 200.68 billion by 2030, at a CAGR of 9.32% during the forecast period (2025-2030).

Key Highlights

- Companies struggling to strike a balance between ensuring their IT infrastructure functions at optimal performance levels and simultaneously managing the associated costs are increasingly hiring vendors offering infrastructure services. Managed infrastructure services help different industry verticals to focus only on their core business.

- These services are mostly being adopted in the IT industry, where cost optimization, emphasis on core competencies, and data security remain significant concerns. However, the recent proliferation of cloud-based technology and technological advancements is the major contributor to this trend.

- The proliferation of technologies like big data has further added to the need for outsourcing IT services. Companies can leverage the combination of both Big Data and the Cloud to provide scalable and cost-effective solutions. For example, Amazon's "Elastic Map Reduce" demonstrates how the power of cloud elastic computes is leveraged for big data processing.

- Further, the need to update outdated hardware is another major market driver. According to a survey conducted by Spice works Inc., 64% of the 700 companies involved in the study reported that the need to update outdated information technology (IT) infrastructure and security concerns are the major factors leading to high IT budgets.

Managed IT Infrastructure Services Market Trends

Technological Proliferation and Advancement of Cloud Based Technology Complement the Demand

- In the current market scenario, the increasing dependency on cloud services and infrastructure upgrading activities are the major factors driving the demand for managed IT infrastructure services. In fact, most of the infrastructure developments in the next few years are dedicated to supporting the increasing demand for cloud services.

- The landscape of IT infrastructure itself is changing rapidly. Traditional racks of servers stored in cages are quickly disappearing as more companies migrate most or all of their IT services and applications to the cloud. As a result, even investments in traditional IT infrastructure are expected to decline over the forecast period as companies increasingly invest in advanced cloud infrastructure.

- Moreover, according to the Cisco Global Cloud Index Report, more than 90 percent of all workloads will be cloud-based by this year. Global cloud traffic will represent 95 percent of total data center traffic. Whereas traditional data center workloads and compute instances are expected to decline during the same period. Historically, one server carried one workload and computed instance. But with increasing server computing capacity and virtualization, multiple workloads and compute instances per physical server are common in cloud architectures.

North America Region to Hold the Largest Market Share

- North America remains the largest market for managed IT infrastructure services because of the early adoption of technology and numerous IT data centers.

- North America has seen a dramatic increase in cloud migration over the years, mostly because of the region's strong IT infrastructure, laws, standards, and access to technological experience, among other factors. Additionally, the expansion of the cloud migration services market in North America has been aided by the existence of illustrious cloud firms like Amazon Web Services, IBM Corporations, Microsoft Corporation, Google, and Cisco Systems.

- The other factor is the high degree of automation and immense penetration of IT applications in several end-user industries, creating a constant demand for IT infrastructure services in the region.

Managed IT Infrastructure Services Industry Overview

The managed IT infrastructure services market is highly competitive due to the presence of many large and small players. The fragmented nature of the market is leading to acquisitions or a growing focus on niche segments as strategies to scale up. The continuously evolving nature of the services offered has made it imperative for all players to keep investing in new-age skills and technologies to stay relevant and ahead of the competition. This can only be achieved by hiring the right R&D talent and/or by acquiring any interesting start-ups that have the potential to disrupt the space. The major advantage that the smaller players have over the bigger ones is their ability to serve the local markets better because of the presence of their data centers locally. This forces bigger players to go for aggressive acquisitions to enhance their global footprint.

In August 2022, Dell Technology announced the launch of new infrastructure solutions, co-engineered with VMware, these new infrastructure solutions increase automation and performance for businesses adopting multi-cloud and edge strategies.

In March 2022, Verizon Communications Inc. announced the expansion of its 5G Ultra Wideband network to an expected 175 million people by year-end 2022. The company outlined several growth avenues, including 5G mobility, nationwide broadband, mobile edge computing (MEC), business solutions, the value market, and network monetization, with the expectation that these will help the company achieve service and other revenue growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Dynamics

- 4.3 Market Drivers

- 4.3.1 Cost Optimization with the Adoption of Managed Services

- 4.3.2 Technological Proliferation and Advancement of Cloud Based Technology will Act as a Driver

- 4.4 Market Restraints

- 4.4.1 Concerns Over Security and Privacy will Act as a Restraint

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Service Category

- 5.1.1 Virtualization

- 5.1.2 Networking

- 5.1.3 Storage

- 5.1.4 Servers

- 5.2 By Enterprise Size

- 5.2.1 Small & Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Deployment

- 5.3.1 On-premises

- 5.3.2 Cloud

- 5.4 By End-User

- 5.4.1 IT & Telecommunication

- 5.4.2 Retail

- 5.4.3 Transportation & Logistics

- 5.4.4 BFSI

- 5.4.5 Manufacturing

- 5.4.6 Other End-Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fujitsu Ltd.

- 6.1.2 CSS Corp Pvt Ltd.

- 6.1.3 Dell EMC (EMC Corporation)

- 6.1.4 IBM Corporation

- 6.1.5 Alcatel-Lucent SA (Nokia Corporation)

- 6.1.6 Microsoft Corporation

- 6.1.7 Verizon Communications Inc.

- 6.1.8 Citrix Systems Inc.

- 6.1.9 Tata Consultancy Services Limited

- 6.1.10 Deutsche Telekom AG

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026年全球託管IT基础设施基础设施服务市场报告

2026年全球託管IT基础设施基础设施服务市场报告 託管IT基础设施服务市场规模、份额和成长分析(按类型、最终用户、企业规模、服务类别和地区划分)-2026-2033年产业预测

託管IT基础设施服务市场规模、份额和成长分析(按类型、最终用户、企业规模、服务类别和地区划分)-2026-2033年产业预测 2025-2029年全球託管IT基础设施服务市场

2025-2029年全球託管IT基础设施服务市场