|

市场调查报告书

商品编码

1641862

植绒黏合剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Flock Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

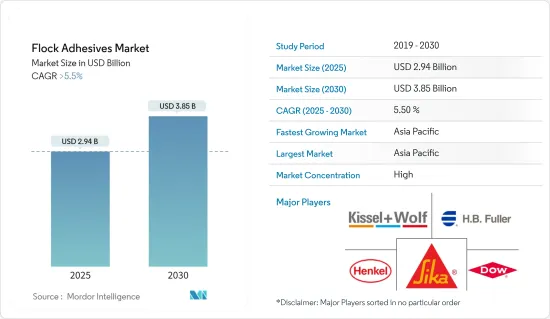

2025 年植绒黏合剂市场规模估计为 29.4 亿美元,预计到 2030 年将达到 38.5 亿美元,预测期内(2025-2030 年)的复合年增长率将超过 5.5%。

COVID-19 疫情对植绒胶市场产生了负面影响。多个国家实施了全国性的封锁和严格的社会隔离措施,导致纺织製造厂和汽车厂关闭,影响了植绒胶市场。然而,在这项限制取消之后,市场却录得了显着的成长率。由于汽车、纺织、纸张和包装应用对植绒黏合剂的需求不断增加,市场呈现成长率。

涂层织物和成品的需求不断增加、轻型和低碳排放汽车的需求不断增长以及亚太地区对植绒胶的需求不断增加,预计将推动植绒胶市场的发展。

另一方面,原材料价格的波动预计会阻碍市场成长。

预计在预测期内,对环保和永续植绒黏合剂的需求不断增长将为市场创造机会。

预计亚太地区将主导市场。此外,汽车、纺织、纸张和包装应用对植绒胶的需求不断增加,预计在预测期内将出现最高的复合年增长率。

植绒黏合剂市场趋势

纺织应用主导市场

- 市场的成长是由纺织产品所推动的。植绒胶用于纺织工业,特别是用于麂皮绒的植绒。

- 中国是世界主要纺织品生产国之一。 2022年,中国成为全球最大纺织品出口国,出口额约1,480亿美元。

- 同样,欧盟以约 710 亿美元的出口额位居第二。预计未来几年纺织品出口额将进一步增加,从而推动目前的研究市场发展。

- 欧盟委员会表示,欧盟的纺织生态系统创造了价值并提供了投资和创新的机会。纺织和服饰(T&C) 产业是欧洲规模最大、最多样化的工业产业之一,拥有 150 万名员工,营业额约 1,620 亿欧元(1,790 亿美元)。因此,纺织品市场的扩大有望推动该地区植绒胶市场的发展。

- 此外,在印度,随着过去十年来纺织业的外国直接投资(FDI)不断增加,纺织品产量不断上升,因此植绒胶的使用量也在增加。根据印度品牌资产基金会统计,2023年4月至2023年10月,印度纺织品和服装出口额(包括手工艺品)为211.5亿美元。预计到 2025-26 年将达到 1900 亿美元。

- 此外,根据美国全国纺织组织理事会(NCTO)的数据,美国是世界第三大纺织品出口国。美国纺织业提供美国军方8000多种纺织产品。此外,2022年该国的纺织品和服装出货收益将达658亿美元。

- 因此,预计纺织应用领域将在预测期内占据植绒黏合剂市场的主导地位。

亚太地区占市场主导地位

- 由于汽车、纺织、纸张和包装应用方面的需求不断增加,预计亚太地区将主导植绒黏合剂市场。

- 亚太地区的汽车产量正在成长,其中中国和印度是领先的製造商。根据OICA预测,2022年该地区汽车产量将达5,002万辆,而上一年为4,676万辆。因此,预计汽车产量的增加将推动该地区植绒胶市场的发展。

- 在印度,随着人口的成长,对汽车的需求也日益增加。因此,各製造商纷纷宣布扩张计划,以提高在该国的汽车生产能力。例如,MG Motor India 在 2023 年 1 月宣布将投资 1 亿美元扩大生产能力,并在 2023年终前实现 70% 的成长。因此,预计预测期内中国和印度汽车市场的成长将推动对植绒胶的需求。

- 此外,中国纺织业的市场成长显着。根据中国国家统计局预测,2022年中国纺织品产量将达382亿米,去年同期为235亿米。 12月份,全国服饰布料产量约34.7亿公尺。每月光纤产量持续超过30亿公尺。

- 此外,由于生活方式的改变、人们可支配收入的提高、速食,亚太地区对包装食品的需求正在增长。消费者偏好已调理食品,因为它们需要的准备时间明显较少、新鲜,包装美观且坚固,这满足了所研究市场的需求。

- 总体而言,预测期内汽车、纺织和包装等行业的成长预计将推动该地区植绒胶黏剂市场的发展。

植绒胶黏剂产业概况

植绒黏合剂市场本质上是整合的。该市场的主要企业(不分先后顺序)包括陶氏化学、富勒公司、汉高股份公司、Kissel+Wolf GmbH 和西卡股份公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 对涂层织物和最终产品的需求增加

- 对轻型、低碳车的需求不断增加

- 亚太地区对植绒黏合剂的需求不断增长

- 限制因素

- 原物料价格波动

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 树脂类型

- 丙烯酸纤维

- 聚氨酯

- 环氧树脂

- 其他树脂种类(醇酸树脂、氰基丙烯酸酯等)

- 应用

- 车

- 纺织产品

- 纸包装

- 其他用途(印刷、鞋类等)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Argent International

- Bostik(Arkema Group)

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- International Coatings

- Kissel+Wolf GmbH

- Lord Corporation

- NYATEX

- PARKER HANNIFIN CORP

- Sika AG

- Stahl Holdings BV

第七章 市场机会与未来趋势

- 对环保、永续的植绒黏合剂的需求不断增加

- 其他机会

The Flock Adhesives Market size is estimated at USD 2.94 billion in 2025, and is expected to reach USD 3.85 billion by 2030, at a CAGR of greater than 5.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the market for flock adhesives. Due to nationwide lockdowns in several countries, strict social distancing measures resulted in the closure of textile manufacturing plants and automotive plants, thereby affecting the market for flock adhesives. However, the market registered a significant growth rate well after the restrictions were lifted. The market registered a growth rate due to the increasing demand for flock adhesives in automotive, textiles, paper, and packaging applications.

Increasing demand for coated fabrics and finished products, rising demand for lightweight, low carbon-emitting vehicles, and the increasing demand for flock adhesives in the Asia-Pacific region are expected to drive the market for flock adhesives.

On the flip side, volatility in raw material prices is expected to hinder the growth of the market.

The increasing demand for green, sustainable flock adhesives is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for flock adhesives in automotive, textiles, paper, and packaging applications.

Flock Adhesives Market Trends

Textiles Application Segment to Dominate the Market

- The textile is expected to lead the growth of the market. Flock adhesives are used in the textile industry, especially for the flocking of suede fabrics.

- China is the leading producer of textiles in the world. In 2022, China was the top-ranked global textile exporter, with a value of approximately USD 148 billion.

- Similarly, the European Union ranked in second place, with an export value of around USD 71 billion. The export value of textiles is further expected to increase in the coming years, thereby driving the current studied market.

- According to the European Commission, the European Union's textiles ecosystem generates value and opens up opportunities for investment and innovation. Textiles and clothing (T&C) is one of Europe's largest and most diversified industrial sectors, with a workforce of 1.5 million and a turnover of around EUR 162 billion (USD 179 billion). Thus, the increasing market for textile products is expected to drive the market for flock adhesives in the region.

- Additionally, in India, with an increase in foreign direct investment (FDI) in the textile industry from the past decade, the production of textiles is increasing, thus resulting in increased use of flock adhesives. According to the Indian Brand Equity Foundation, India's textile and apparel exports (including handicrafts) from April 2023 to October 2023 stood at USD 21.15 billion. The industry is expected to reach USD 190 billion by 2025-26.

- Furthermore, according to the National Council of Textile Organization (NCTO), the United States is the world's third-largest exporter of textiles. The United States textile industry supplies the US military with over 8,000 textile products. Further, the textile and apparel shipments in the country reached USD 65.8 billion in 2022.

- Thus, the textiles application segment will dominate the market for flock adhesives during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for flock adhesives due to rising demand from the automotive, textile, paper, and packaging applications in the region.

- The production volume of automotive vehicles is increasing in the Asia-Pacific region, with China and India being the major manufacturers. According to OICA, in 2022, the total production volume of automotive vehicles in the area reached 50.02 million, compared to 46.76 million units manufactured in the previous year. Thus, the increase in the production volume of automotive vehicles will drive the market for flock adhesives in the region.

- In India, the demand for automotive vehicles is increasing with the rising population. Thus, various manufacturers have announced their expansion plans to increase the production capacity of automotive vehicles in the country. For instance, in January 2023, MG Motor India announced to invest USD 100 million to expand capacity and register a growth of 70% by the end of 2023. Thus, the growing markets for automotive vehicles in China and India are expected to drive the demand for Flock adhesives during the forecast period.

- Furthermore, in China, the textile industry registered significant market growth. According to the National Bureau of Statistics of China, the textile production volume in China accounted for 38.2 billion meters in 2022, compared to 23.5 billion meters during the same period in the previous year. In December, approximately 3.47 billion meters of clothing fabric were produced in China. Monthly textile production volume was consistently above three billion meters.

- Furthermore, in the Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food. Consumers prefer ready-to-consume foods because they require considerably less time for cooking, are fresh, and have attractive and sturdy packaging, supporting the demand for the market studied.

- Overall, the growth of industries such as automotive, textiles, and packaging will likely drive the market for flock adhesives in the region during the forecast period.

Flock Adhesives Industry Overview

The flock adhesives market is consolidated in nature. Some of the major players in the market (not in any particular order) include Dow, H.B. Fuller Company, Henkel AG & Co. KGaA, Kissel + Wolf GmbH, and Sika AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand of Coated Fabrics and Finished Products

- 4.1.2 Rising Demand for Light weight Low Carbon Emitting Vehciles

- 4.1.3 Increasing Demand for Flock Adhesives in the Asia-Pacific Region

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Acrylic

- 5.1.2 Polyurethane

- 5.1.3 Epoxy resin

- 5.1.4 Other Resin Types (Alkyd, Cyanoacrylate, etc.)

- 5.2 Application

- 5.2.1 Automotive

- 5.2.2 Textiles

- 5.2.3 Paper and Packaging

- 5.2.4 Other Applications (Printing, Footwear, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Argent International

- 6.4.2 Bostik (Arkema Group)

- 6.4.3 Dow

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 International Coatings

- 6.4.7 Kissel + Wolf GmbH

- 6.4.8 Lord Corporation

- 6.4.9 NYATEX

- 6.4.10 PARKER HANNIFIN CORP

- 6.4.11 Sika AG

- 6.4.12 Stahl Holdings B.V

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Demand for Green Sustainable Flock Adhesives

- 7.2 Other Opportunities

植绒黏合剂市场(按产品类型、最终用途产业、应用和形式)—2025-2032 年全球预测

植绒黏合剂市场(按产品类型、最终用途产业、应用和形式)—2025-2032 年全球预测 2025年植绒黏合剂全球市场报告

2025年植绒黏合剂全球市场报告 全球植绒黏合剂市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

全球植绒黏合剂市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年 植绒黏合剂市场规模、份额、成长分析,按树脂类型、应用、基材类型、地区 - 产业预测,2024-2031 年

植绒黏合剂市场规模、份额、成长分析,按树脂类型、应用、基材类型、地区 - 产业预测,2024-2031 年 2024-2028年全球植绒黏剂市场

2024-2028年全球植绒黏剂市场 植绒黏合剂市场,按产品类型、树脂类型、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

植绒黏合剂市场,按产品类型、树脂类型、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 2023-2030年全球植绒黏剂市场规模、份额、趋势分析报告、按树脂类型、应用、地区分類的前景和预测

2023-2030年全球植绒黏剂市场规模、份额、趋势分析报告、按树脂类型、应用、地区分類的前景和预测 全球植绒黏合剂市场评估:依树脂类型、应用基材、最终用途产业、地区、机会、预测(2016-2030)

全球植绒黏合剂市场评估:依树脂类型、应用基材、最终用途产业、地区、机会、预测(2016-2030)