|

市场调查报告书

商品编码

1641866

增强塑胶:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Reinforced Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

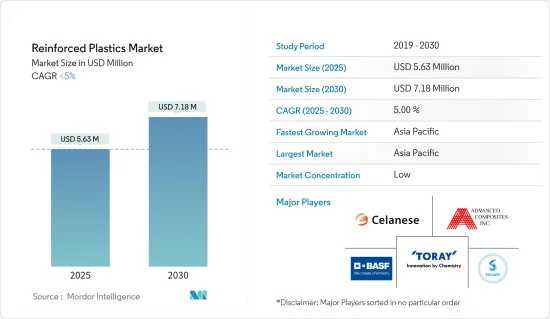

增强塑胶市场规模预计在 2025 年为 563 万美元,预计到 2030 年将达到 718 万美元,预测期内(2025-2030 年)的复合年增长率低于 5%。

COVID-19疫情对增强塑胶市场产生了负面影响。由于多个国家实施全国性停工和社交距离措施,导致劳动力短缺,汽车製造工厂关闭,对增强塑胶市场产生了负面影响。然而,在新冠疫情爆发后,由于汽车、航太、国防和建筑业的需求增加,市场恢復良好。

关键亮点

- 航太工业的需求不断增长以及对省油轻型汽车的需求不断增加预计将推动增强塑胶市场的发展。

- 增强塑胶难以分解的性质阻碍了市场的成长。

- 预计预测期内对风力发电的需求不断增加将为市场创造机会。

- 由于建筑、国防和运输业对增强塑胶的需求不断增长,预计亚太地区将占据市场主导地位。

增强塑胶市场趋势

汽车领域占据市场主导地位

- 汽车产业是全球增强塑胶的重要消费者。增强塑胶广泛用于汽车、卡车等行业的金属替代品。

- 此外,对轻量材料和比传统材料更高的故障点的需求不断增长,吸引汽车製造商转向增强塑料。应用包括歧管、加速器和离合器踏板等引擎部件。

- 预计汽车产量的增加将推动增强塑胶市场的发展。根据国际汽车製造商协会(OICA)预测,2022年全球汽车产量将达到8,502万辆,而2021年为8,020万辆,成长率为6%。中国、美国和印度是世界上最突出的汽车市场。

- 美国是继中国之后世界第二大汽车市场,占全球汽车市场的很大份额。美国是几家全球汽车製造商的总部,这些製造商向加拿大、墨西哥和韩国等国家出口汽车。根据OICA预测,2022年美国汽车产量将从2021年的915万辆达到1,006万辆,成长率为9%。因此,预计汽车产量的成长将推动目前调查市场的发展。

- 此外,德国汽车製造业是欧洲汽车整体生产的主要股东。该国是主要汽车製造品牌的所在地,例如大众、梅赛德斯-奔驰、奥迪、宝马和保时捷。根据OICA预测,2022年汽车和轻型商用车总产量将从2021年的330万辆达到367万辆,成长率为11%。

- 此外,全球电动车市场正在大幅扩张,这对所研究的市场有利。例如,2022年全球电池电动车(BEV)和插电式混合动力车(PHEV)的销量将达到约1,050万辆,比前一年的677万辆成长55%。

- 因此,由于上述因素,预计汽车终端用户产业将在预测期内主导增强塑胶市场。

亚太地区占市场主导地位

- 亚太地区占据市场主导地位,预计在预测期内将大幅成长。由于中国、印度、日本和韩国等国家的汽车、建筑、能源和航空业的成长,钢筋混凝土的消耗量正在增加。

- 中国是该地区最大的汽车製造国。根据OICA预测,2022年中国汽车产量将达2,702总合,与前一年同期比较去年同期成长3%。

- 而中国是全球最大的建筑市场,占全球整体的20%。到2030年,中国预计将在建筑业上投入近13兆美元。这有望为该国的增强塑胶带来光明的前景。

- 印度政府正在积极推动住宅建设,以便为约13亿人提供住宅。预计未来七年中国住宅投资将达 1.3 兆美元左右,新建住宅将达 6,000 万套。到 2024 年,该国的经济适用住宅供应量预计将增加 70% 左右。

- 此外,预计包括中国、东南亚和南亚在内的亚太地区航太市场将大幅成长,从而进一步推动所研究市场的需求。根据波音公司《2023-2042年商用飞机展望》,到2042年,中国将交付约8,560架新飞机,使其总机持有数量达到9,590架。

- 此外,波音和空中巴士是中国最着名的民航机製造商。为了削弱这些公司的主导地位,中国商用航空公司(COMAC)开始在国内生产民航机。 2022年9月,公司交付中国首架国产客机。此外,中国商用飞机有限责任公司(COMAC)5年内已形成年产约150架国产C919飞机的生产能力。因此,提高飞机生产能力可能会增加该国对增强塑胶的需求。

- 此外,印度航空业预计未来四年将吸引3,500亿印度卢比(约49.9亿美元)的投资。印度航空巨头印度航空于 2023 年 2 月下达了近期历史上最大的新飞机订单之一。印度历史最悠久的航空公司,现在由塔塔集团拥有,宣布计划从飞机製造商空中巴士和波音公司购买 470 架飞机。交易总合价值估计约800亿美元。

- 由于所有这些因素,预计预测期内该地区的增强塑胶市场将会成长。

增强塑胶产业概况

增强塑胶市场比较分散。市场上的主要企业(不分先后顺序)包括BASF SE、Celanese Corporation、Present Advanced Composites Inc.、Solvay 和 Toray Industries Inc.

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 航太工业的需求不断成长

- 省油、轻量化汽车的需求日益增加

- 其他驱动因素

- 限制因素

- 不可降解增强塑料

- 其他限制因素

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 类型

- 玻璃纤维增强塑料

- 碳纤维增强塑料

- 酰胺纤维增强塑料

- 其他类型(木纤维强化塑胶、石棉纤维强化塑胶)

- 最终用户产业

- 车

- 海洋

- 航太和国防

- 能源动力

- 建筑和施工

- 其他最终用户产业(电气、化工等)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Ahlstrom

- BASF SE

- Cabot Corporation

- Celanese Corporation

- Dow

- Formosa Plastics Corporation

- Gulf Reinforced Plastics

- Hexcel Corporation

- Jiangsu QIYI Technology Co., Ltd.

- Nikkiso Co., Ltd.

- PPG Industries Inc

- Present Advanced Composites Inc.

- RBJ Reinforced Plastics Ltd

- Relaince Industries Ltd.

- Solvay

- Teijin Limited

- Toray Industries, Inc

第七章 市场机会与未来趋势

- 风力发电需求不断成长

- 其他机会

The Reinforced Plastics Market size is estimated at USD 5.63 million in 2025, and is expected to reach USD 7.18 million by 2030, at a CAGR of less than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the market for reinforced plastics. The nationwide lockdowns in several countries and the labour shortage due to social distancing measures had negatively resulted in the closure of manufacturing facilities of automotive vehicles, thereby affecting the market for reinforced plastics. However, post-COVID pandemic, the market recovered well due to increasing demand from the automotive, aerospace, defense, and construction industries.

Key Highlights

- The growing demand from the aerospace industry and the rising demand for fuel-efficient and lightweight vehicles are expected to drive the market for reinforced plastics.

- The non-degradable nature of reinforced plastic is hindering market growth.

- The increasing demand for wind energy is expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market due to the rising demand for reinforced plastics from the construction, defense, and transportation industries.

Reinforced Plastics Market Trends

Automotive Segment Dominated the Market

- The automotive industry is a critical consumer of reinforced plastics globally. Reinforced plastics are widely used as metal substitutes in automobiles, trucks, etc.

- Additionally, increasing demand for lightweight materials and higher fracture points than traditional materials attracts automotive manufacturers toward reinforced plastics. Some of the areas of the application include engine components such as manifold, gas, clutch pedals, etc.

- The increase in the production volume of automotive vehicles is expected to drive the market for reinforced plastics. According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), global automotive vehicle production reached 85.02 million in 2022, compared to 80.2 million manufactured in 2021, at a growth rate of 6%. China, the United States, and India are the most prominent automotive vehicle markets globally.

- The United States is the second-largest automotive market in the world after China, which occupies a significant share of the global automotive vehicles market. The United States is the headquarters for some global automotive vehicle manufacturers, exporting vehicles to countries such as Canada, Mexico, and South Korea. According to OICA, in 2022, the United States automotive vehicle production reached 10.06 million compared to 9.15 million units manufactured in 2021, at a growth rate of 9%. Thus, the rise in vehicle production will drive the current studied market.

- Furthermore, the automobile manufacturing industry in Germany is a prominent shareholder of the overall automotive production in the European region. The country hosts major car-making brands, including Volkswagen, Mercedes-Benz, Audi, BMW, Porsche, etc. According to OICA, the total production volume of cars and light commercial vehicles reached 3.67 million units in 2022, compared to 3.30 million units manufactured in 2021, at a growth rate of 11%.

- Additionally, the global electric vehicle market is expanding signifiantly, which is benefitting the market studied. For instance, in 2022, around 10.5 million units of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold across the globe, witnessing a growth rate of 55% compared to 6.77 million units sold in the previous year.

- Hence, owing to the factors mentioned above, the automotive end-user industry is expected to dominate the market for reinforced plastics during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the market and is expected to significantly increase over the forecast period. With the growing automotive, construction, energy, and aviation sectors in countries like China, India, Japan, and South Korea, the consumption of reinforced concrete is increasing.

- China is the largest automotive vehicle manufacturer in the region. According to OICA, automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

- Furthermore, China is the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings and construction by 2030. This is anticipated to create a positive outlook for reinforced plastics in the country.

- The Indian government has been actively boosting housing construction to provide houses to about 1.3 billion people. The country is likely to witness around USD 1.3 trillion of investment in housing over the next seven years, to witness the construction of 60 million new houses in the country. The availability of affordable housing in the country is expected to increase by around 70% by 2024.

- Furthermore, in the Asia-Pacific region, including China, Southeast Asia, and South Asia, the aerospace market is expected to rise significantly, further supporting the demand for the market studied. According to the Boeing Commercial Outlook 2023-2042, around 8,560 new deliveries in China will be made by 2042, taking the total fleet to 9,590.

- Additionally, Boeing and Airbus are the most prominent civil aircraft manufacturers in China. To decrease the dominance of these companies, the Commercial Aviation Corp of China (COMAC) started to manufacture civil aircraft in the country. In September 2022, the company delivered its first homemade passenger jet in China. Furthermore, the annual production capacity of Commercial Aviation Corp of China (COMAC) is around 150 domestically produced C919 planes in five years. Thus, the increased aircraft production capacity will likely drive the demand for reinforced plastics in the country.

- Moreover, India's aviation industry is expected to witness INR 35,000 crore (~USD 4.99 billion) investment in the next four years. India's airline giant, Air India, in February 2023, placed one of the biggest orders for new aircraft in recent history. India's oldest airline, now firmly under the ownership of the Tata Group, announced that it is purchasing 470 aircraft from airline manufacturers Airbus and Boeing. The combined value of the deals is estimated at some USD 80 billion.

- Due to all such factors, the market for reinforced plastics in the region is expected to grow during the forecast period.

Reinforced Plastics Industry Overview

The reinforced plastics market is fragmented in nature. Some of the major players in the market (not in any particular order) include BASF SE, Celanese Corporation., Present Advanced Composites Inc., Solvay, and Toray Industries, Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Aerospace Industry

- 4.1.2 Rising Demand for Fuel Efficient and Light-weight Vehicles

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Non-Degradable Nature of Reinforced Plastic

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Glass Fiber Reinforced Plastics

- 5.1.2 Carbon Fiber Reinforced Plastics

- 5.1.3 Aramid Fiber Reinforced Plastics

- 5.1.4 Other Types (Wood Fiber Reinforced Plastics, Asbestos Fiber Reinforced Plastics)

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Marine

- 5.2.3 Aerospace and Defence

- 5.2.4 Energy and Power

- 5.2.5 Building and Construction

- 5.2.6 Other End-user Industries (Electrical, Chemicals, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Ahlstrom

- 6.4.2 BASF SE

- 6.4.3 Cabot Corporation

- 6.4.4 Celanese Corporation

- 6.4.5 Dow

- 6.4.6 Formosa Plastics Corporation

- 6.4.7 Gulf Reinforced Plastics

- 6.4.8 Hexcel Corporation

- 6.4.9 Jiangsu QIYI Technology Co., Ltd.

- 6.4.10 Nikkiso Co., Ltd.

- 6.4.11 PPG Industries Inc

- 6.4.12 Present Advanced Composites Inc.

- 6.4.13 RBJ Reinforced Plastics Ltd

- 6.4.14 Relaince Industries Ltd.

- 6.4.15 Solvay

- 6.4.16 Teijin Limited

- 6.4.17 Toray Industries, Inc

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand from Wind Energy

- 7.2 Other Opportunities

全球玻璃纤维增强塑胶市场规模、份额、趋势和成长分析报告(2026-2034)纤维强化塑胶(FRP)桥樑市场:现状分析与预测(2024-2032年)

全球玻璃纤维增强塑胶市场规模、份额、趋势和成长分析报告(2026-2034)纤维强化塑胶(FRP)桥樑市场:现状分析与预测(2024-2032年) 增强塑胶市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2024-2030 年

增强塑胶市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2024-2030 年