|

市场调查报告书

商品编码

1641873

离型膜-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Release Liners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

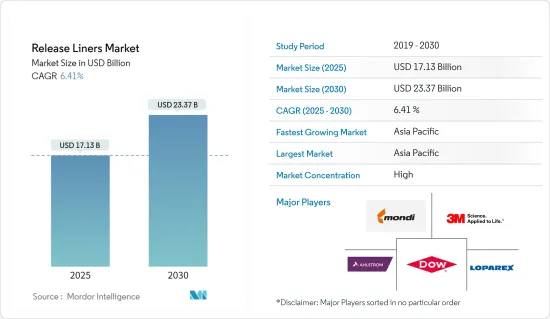

离型膜市场规模预计在 2025 年为 171.3 亿美元,预计到 2030 年将达到 233.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.41%。

关键亮点

- COVID-19 疫情对离型膜产业产生了负面影响。全球封锁和严格的政府规定导致我们大部分生产基地关闭,造成了毁灭性的打击。儘管如此,自 2021 年以来业务一直在復苏,预计未来几年将大幅成长。

- 短期内,食品和饮料行业对洁净标示的需求不断增加、对优质卫生产品的需求不断增长以及医疗领域对薄膜衬垫的采用是推动所研究市场增长的一些因素。

- 然而,有关离型膜废弃物处理的问题预计会阻碍市场的成长。

- 然而,预计新兴国家包装产业的扩张将在预测期内提供许多机会。

- 预计亚太地区将主导市场,并在预测期内以最高的复合年增长率成长。

离型膜市场趋势

标籤市场占据主导地位

- 标籤贴在包装上,以标明内容、产品规格、联络方式、健康和安全警告和指南,以及任何适用于产品的附加行销、品牌或定价资讯。

- 由于新兴国家包装食品产业的需求不断增加,预计标籤领域将占据市场主导地位。在超级市场/大卖场,冷冻食品种类繁多,有不同的成分、口味和包装样式。这有望鼓励消费者光顾超级市场和大卖场,进而增加市场销量,进而增加对离型膜的需求。

- 此外,根据美国包装公司(PCA)的年报,2022年,美国包装公司年收益约85亿美元,较2021年成长9.69%。因此,包装收益的增加预计将创造对标籤的需求,并增加标籤部分对离型膜的需求。

- 此外,世界各国零售业的扩张也增加了对标籤应用离型膜的需求。例如,根据加拿大统计局的数据,2022 年 1 月加拿大零售国内生产总值为 1,065 亿加元(818.7 亿美元),比 2021 年 1 月增长 7.44%。

- 此外,对永续包装的日益关注、大型零售连锁店的扩张、消费者对简便食品(包装食品)的需求以及生活方式的改变,正在推动标籤应用中对离型膜的需求,进而推动离型膜市场的成长。

亚太地区占市场主导地位

- 亚太地区占据离型膜市场的大部分份额,预计在预测期内将以最快的速度成长。

- 离型膜用于汽车生产的许多部分,从煞车灯、地毯、内装和门饰的感压胶带,到用于减震和隔音的各种垫圈,以及新兴的电动车电池生产(电动车( EV)汽车。离型膜的需求主要受到中国汽车和医疗领域的推动。随着该国对汽车、医疗和包装领域的投资不断增加,预计预测期内对离型膜的需求将会增加。

- 例如,根据国际汽车工业组织(OICA)的数据,2022 年该国的汽车产量为 27,026,150 辆,比 2021 年增加 3%。因此,随着汽车产量的增加,该国的离型膜市场可能会扩大。

- 此外,女性卫生棉也需要离型膜。人们对私密卫生意识的不断增强以及对卫生棉、卫生棉条和卫生护垫等卫生产品的日益偏好正在推动对离型膜的需求。印度政府在全国各地推出了多项有关女性月经卫生的宣传计画。例如,2022年1月,拉贾斯坦邦政府启动了一项名为「我是乌达安」的女性友善计划。这项耗资 20 亿卢比(2,540 万美元)的计画为该邦的每个女孩和妇女免费提供卫生棉。预计政府的这些措施将增加对离型膜的需求。

- 此外,离型膜是经皮给药系统、医疗设备、先进创伤护理敷料和其他医药包装产品等医疗产品整体开发和性能的关键组成部分。离型衬垫在医疗设备製造和药品包装中具有多种优势,因为它们有助于包装和保护各种产品。

- 医疗产品和医疗设备产业的显着成长预计将推动离型膜市场的成长。例如,根据印度品牌资产基金会 (IBEF) 的数据,2022 财年印度的医疗设备出口额为 29 亿美元,预计到 2025 年将增加至 100 亿美元。因此,预计该国医疗设备出口的增加将推动离型膜市场的需求上升。

- 此外,印度政府也推出多项措施加强医疗设备产业,重点强调医疗设备的研发和开发以及 100% 的 FDI,从而促进了市场的发展。例如,根据 IBEF 的数据,2022 年 8 月,医药部将在 21-25 财年向「医疗设备园区促进」计画投资 4,897 万美元,该计画为每个医疗设备园区提供的最高援助为 1,224 万美元. 以美元计算。

- 因此,在政府支持下这些产业的进一步成长可能会在预测期内增加对离型膜的需求,从而促进中国和印度等新兴市场的成长。

离型膜产业概览

离型膜市场已趋于整合。该市场的主要企业(不分先后顺序)包括 Mondi、Dow、3M、Loparex 和 Ahlstrom。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 食品和饮料行业对洁净标示的需求

- 高阶卫生产品的需求增加以及医疗领域对薄膜衬垫的采用

- 其他驱动因素

- 限制因素

- 离型膜废弃物的处理问题

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 应用

- 标籤

- 形象的

- 磁带

- 医疗

- 工业的

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率分析(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- Ahlstrom

- Dow

- Eastman Chemical Company

- Elkem ASA

- Felix Schoeller

- Gascogne Group

- LINTEC Corporation

- Loparex

- Mondi

- Sappi Group

- SJA Film Technologies Ltd

- The Griff Network

- UPM Global

第七章 市场机会与未来趋势

- 新兴国家包装产业的成长

- 其他机会

简介目录

Product Code: 61134

The Release Liners Market size is estimated at USD 17.13 billion in 2025, and is expected to reach USD 23.37 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic had a negative impact on the release liners sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business has been recovering since 2021 and is expected to rise significantly in the coming years.

- Over the short term, increasing demand for clean labels from the food and beverage industry and rising demand for premium hygiene products, and adoption of film-based liners in the medical sector are some of the factors driving the growth of the market studied.

- On the flip side, issues related to the disposal of release liner waste are expected to hinder the market's growth.

- However, expanding the packaging sector in emerging economies is anticipated to provide numerous opportunities over the forecast period.

- Asia Pacific region is expected to dominate the market and will also witness the highest CAGR during the forecast period.

Release Liners Market Trends

Labels Segment to Dominate the Market

- Labels are applied to packaging to indicate the contents, product specifications, contact details, health and safety warnings and guidelines, and any additional marketing, branding, or pricing information that applies to a product.

- The labels segment is expected to dominate the market majorly due to the increased demand from the packaged foods sector in emerging economies. In supermarkets/hypermarkets, frozen-food meals are available in a wide range with a variety of ingredients and flavors in different packaging styles. This further attracts consumers to supermarkets and hypermarkets, driving the net sale in the market, in turn, is expected to create an upside demand for release liners.

- Moreover, according to the Packaging Corporation of America (PCA) annual report, in 2022, the annual revenue of the packaging corporation of America was approximately USD 8.5 billion, which shows an increase of 9.69% compared with 2021. Therefore, an increase in the revenue of packaging is expected to create demand for labels, which is expected to augment the demand for release liners from the labels segment.

- Additionally, the expanding retail sector in several countries across the world has increased the demand for release liners in labeling applications. For instance, according to StatCan, in Jan 2022, the gross domestic product for the retail trade industry in Canada amounted to CAD 106.5 billion (USD 81.87 billion), which showed an increase of 7.44% compared to Jan 2021.

- Moreover, the focus on sustainable packaging, the expansion of large retail chains, consumer demand for convenience foods (packaged foods), and lifestyle changes have driven the demand for release liners in labeling applications, in turn, boosting the growth of release liners market.

Asia-Pacific to Dominate the Market

- Asia-Pacific holds a significant share of the release liners market, and it is expected to witness the fastest growth during the forecast period.

- Release liners are found in many components of vehicle production, from pressure-sensitive tapes for brakes lights, carpets, upholstery, and door trim, to the wide variety of gaskets used for vibration reduction and sound dampening and the emerging production of batteries for EV vehicles. The demand for release liners majorly arises from the automotive and medical sectors in China. With the increasing investments in the country's automotive, medical, and packaging sectors, the demand for release liners is expected to increase during the forecast period.

- For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, automobile production in the country amounted to 2,70,20,615 units, which showed an increase of 3% compared to 2021. Therefore, the release liners market in the country is likely to expand as a result of the rise in overall automobile manufacturing.

- Additionally, release liners are also required in sanitary pads for female hygiene. The increasing awareness about intimate hygiene and increasing preference for menstrual products, such as sanitary pads, tampons, and panty liners, are boosting the demand for release liners. The Government of India has launched several awareness programs across the country about women's menstrual hygiene. For instance, in January 2022, the Rajasthan government started "I am Udaan," a women-friendly project. This plan, which will cost INR 200 crore (USD 25.4 million), will provide free sanitary napkins to every girl and woman in the state. Such government initiatives are expected the increase the demand for release liners.

- Moreover, release liners are a critical component in the overall development and performance of medical products such as transdermal drug delivery systems, medical devices, advanced wound care dressings, and other pharmaceutical packaging products. Release liners provide several benefits in medical device manufacturing and pharmaceutical packaging as they help package and protect a wide range of products.

- The significant growth in the medical products and devices industry is expected to propel the growth of the release liners market. For instance, according to India Brand Equity Foundation (IBEF), the export of medical devices from India stood at USD 2.90 billion in FY22 and is expected to rise to USD 10 billion by 2025. Therefore, an increase in the exports of medical devices from the country is expected to create an upside demand for the release liners market.

- Furthermore, the government of India has commenced various initiatives to strengthen the medical devices sector, with emphasis on research and development (R&D) and 100% FDI for medical devices to boost the market. For instance, according to IBEF, in August 2022, the Department of Pharmaceuticals greenlit the "Promotion of Medical Devices Parks" program from FY21-25 with a total financial investment of USD 48.97 million, with a maximum support under the program of USD 12.24 million for each Medical Device Park.

- Hence, further growth in these industries, owing to the government's support, is likely to increase the demand for release liners during the forecast period, thus, boosting the market growth in developing nations such as China and India.

Release Liners Industry Overview

The release liners market is consolidated in nature. The major players in this market (not in a particular order) include Mondi, Dow, 3M, Loparex, and Ahlstrom, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand for Clean Labels in Food and Beverage Industry

- 4.1.2 Rising Demand from Premium Hygiene Products and Adoption of Film-Based Liners in Medical Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Issues Related to the Disposal of Release Liner Waste

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Labels

- 5.1.2 Graphics

- 5.1.3 Tapes

- 5.1.4 Medical

- 5.1.5 Industrial

- 5.1.6 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 United Kingdom

- 5.2.3.2 France

- 5.2.3.3 Germany

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Ahlstrom

- 6.4.3 Dow

- 6.4.4 Eastman Chemical Company

- 6.4.5 Elkem ASA

- 6.4.6 Felix Schoeller

- 6.4.7 Gascogne Group

- 6.4.8 LINTEC Corporation

- 6.4.9 Loparex

- 6.4.10 Mondi

- 6.4.11 Sappi Group

- 6.4.12 SJA Film Technologies Ltd

- 6.4.13 The Griff Network

- 6.4.14 UPM Global

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth in Packaging Sector in Emerging Economies

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

离型纸市场(按材料类型、标籤技术、厚度范围、技术、产品形式和最终用途)—2025-2030 年全球预测

离型纸市场(按材料类型、标籤技术、厚度范围、技术、产品形式和最终用途)—2025-2030 年全球预测 SCK 离型膜市场 - 全球产业规模、份额、趋势、机会和预测,按材料类型、离型膜类型、基材类型、最终用途产业、地区和竞争细分,2020 年至 2030 年

SCK 离型膜市场 - 全球产业规模、份额、趋势、机会和预测,按材料类型、离型膜类型、基材类型、最终用途产业、地区和竞争细分,2020 年至 2030 年 全球离型膜市场(2025年)

全球离型膜市场(2025年) 标籤·离型纸的未来(~2030年)

标籤·离型纸的未来(~2030年) 白色玻璃纸离型纸市场报告:趋势、预测与竞争分析(至 2031 年)

白色玻璃纸离型纸市场报告:趋势、预测与竞争分析(至 2031 年) 离型纸市场:依基材、标籤技术、应用与地区划分

离型纸市场:依基材、标籤技术、应用与地区划分 2025-2033 年按材料类型、基材类型、标籤技术、应用和地区分類的离型纸市场纸本离型纸市场报告:2030 年趋势、预测与竞争分析

2025-2033 年按材料类型、基材类型、标籤技术、应用和地区分類的离型纸市场纸本离型纸市场报告:2030 年趋势、预测与竞争分析 离型纸市场规模、份额和成长分析(按类型、材质、标籤技术、应用、最终用途、地区):产业预测(2024-2031)

离型纸市场规模、份额和成长分析(按类型、材质、标籤技术、应用、最终用途、地区):产业预测(2024-2031) 全球离型纸市场 (2024-2028)

全球离型纸市场 (2024-2028)

▼