|

市场调查报告书

商品编码

1641915

自动送货机器人市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Autonomous Delivery Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

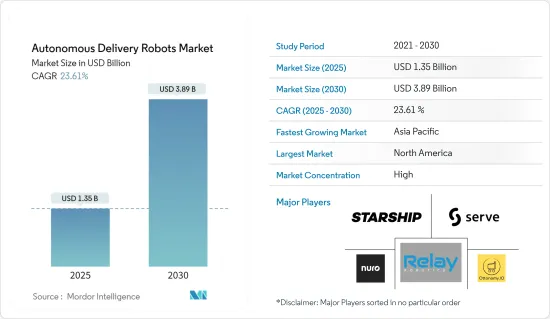

预计 2025 年自动送货机器人市场规模为 13.5 亿美元,预计到 2030 年将达到 38.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 23.61%。

由于自动送货车辆效率高而使其使用率不断提高是推动该市场成长的主要因素。 2022 年 1 月,Ottonomy 推出了 Ottobots,这是一款适用于餐厅和零售企业的室外和室内环境的全自动送货机器人。这场疫情为 Ottobots 提供了催化剂,促成了一系列伙伴关係,让该公司能够推出路边、室内和最后一英里的全自动配送。

关键亮点

- 自主送货机器人(ADR)正在彻底改变送货程序,提供更便宜、更有效的送货方式。送货机器人目前还没有广泛普及,但由于其具有许多优势,预计未来将会发展。 ADR 的日益普及主要是由于对灵活、高效的自动化履约的持续需求,以及基础设施中轻量级机器人数量的增加,以及可负担性和投资收益的提高。例如,2022 年 1 月,自动送货机器人领域的主要参与企业Starship Technologies 从欧盟投资机构获得 5,000 万欧元,用于扩大其自动送货机器人队伍。

- 人工智慧和机器学习也为食品加工行业、餐饮、餐厅和小餐馆带来了巨大的利益。除此之外,这些技术还加快了供应链流程并增强了食品配送服务。

- 此外,最后一哩的交付一直是处理供应链的主要问题之一。随着电子商务的持续成长以及消费者对更快、更规律的配送的期望越来越高,导致交通拥堵和碳污染加剧,都市区的最后一哩配送变得越来越复杂。根据世界经济论坛的数据,到 2030 年,全球整体最后一哩配送的需求预计将增加 78%。

- 根据全国零售联合会 (NRF) 统计,送货事故给零售商造成了约 3.33 亿美元的收入损失。这些配送挑战促使许多消费者和零售商寻求更好、更有效的配送方式。

- 许多零售商发现,良好的最后一哩体验可以吸引和留住消费者。同时,满足客户配送期望并不意味着更高的利润率,因为如今零售商承担了最后一哩配送的部分成本。因此,ADR 帮助这些公司实现高效的最后一英里交付。

- 此外,物流业也消耗大量自然资源来维持货物运送等各项业务。它还向大气中排放大量温室气体,导致全球暖化。自主运载系统有望透过减少大气中的二氧化碳排放来抵消这些不利的环境影响。

- 正在颁布多项法律来遏制全球暖化和保护环境。这些政府措施正在促进市场对 ADR 的需求。例如,欧盟委员会制定了2050年实现脱碳的目标,并为2020年和2030年设定了几个近期目标。

- 此外,德里政府最近共用了一份法案草案,规定到 2030 年,计程车公司、食品配送公司和电子商务平台必须使用电动车。据政府相关人员称,政府的目标是到 2024 年将电动车在汽车总销量中的比例提高到 25%。这些活动可能会进一步阻碍送货机器人市场的成长。

- 新冠肺炎疫情让全球专注于无接触包裹配送机器人,强劲的市场需求促使配送机器人开发商在美国多个城市启动大型专案。预计预测期内配送机器人技术的部署和采用将推动配送机器人市场的发展。全球物流和医疗保健支出的增加可能会进一步推动市场成长。根据世界卫生组织预测,2023年至2028年间,全球当期卫生费用占GDP比重将增加0.2个百分点,2028年将达10.81%。

自动送货机器人市场趋势

医疗领域预计将显着成长

- 医疗应用是自主配送机器人较为先进的形式之一。与户外送货机器人不同,部署在医疗应用中的自主送货机器人需要考虑其他几个参数,例如低噪音马达、卫生参数以及与常规送货相比的平稳运作。

- 此前,一些医疗机构安装了机器人来治疗幼儿。但现在它们甚至被用来协助医护人员按需取得所需资源。例如,以美国知名机器人製造商 Aethon 为例。 Aethon 提供用于医疗应用的 TUG 机器人。

- 此外,巴达洛纳市立医院和巴塞隆纳诊所医院也安装了TIAGo外送机器人和TIAGo输送机机器人。巴达洛纳医院创新计划部的 Sergio García Redondo 认为,测试的两个使用案例显示出很大的潜力,无疑将改善医院的物流。它还可以帮助医院大幅减少那些对患者没有额外价值的重复性任务。这使得医务人员能够直接关注患者。

- 这些机器人还在马哈退伍军人医疗中心用于根据需要提取和运送医疗用品。机器人还透过运送一些后勤物资和实验室样本为该设施提供支援。此外,Sheba 医疗中心最近与以色列新兴企业Seamless Vision 合作建立了创新的自主物流基础设施。未来几年,该公司计划开始自主向患者运送药物,以减轻医院工作人员的负担。

- 根据美国劳工统计局 (BLS) 的数据,到 2024 年,美国对护理人员的需求预计将增加 16%,达到 320 万人。大部分增长将由需要更多护理的老龄化婴儿潮一代推动。此外,医疗保健应用的支出日益增加,这表明人们将采用自动送货机器人。例如,根据 IBEF 的数据,印度的医疗保健支出预计将在 2022 年达到 3,720 亿美元,高于前一年的 1,940 亿美元。

- 此外,Aster DM Healthcare 宣布将在未来三年内投资 90 亿印度卢比(1.2097 亿美元),以扩大其在印度的业务,并计划在 2025 年将收益占有率提高到 40%。资本支出计划此外,在 2023-24 年联邦预算中,政府向卫生与家庭福利部 (MoHFW) 拨款 107.6 亿美元。各地区医疗保健产业的扩张可能会进一步推动所研究市场的需求。

北美:市场正在经历显着成长

- 北美是自动送货机器人的重要市场。几家主要的市场经销商都位于该地区。该地区也是许多致力于发展自动送货机器人技术的新兴企业和製造商的所在地。

- 同时,与世界其他地区相比,该地区多个终端用户对自动送货机器人的使用强度相对较高。饭店、物流和零售业对这些机器人的需求庞大。许多零售和餐旅服务业供应商正在与製造商合作以获得原型的第一手经验。例如,谷歌最近投资了 Nuro,一家专注于使用自动机器人车辆运送货物的公司。该公司在由老虎全球管理公司主导的资金筹措中筹集了总计 6 亿美元。

- 根据电子商务基金会统计,北美是全球社交网路普及率最高的地区,在电子商务产业处于领先地位。除了降低人事费用之外,引入送货机器人还将有助于获得社交网路热度并提高RevPAR。预计此项活动将保持酒店业对自动送货机器人的稳定需求。

- 各个终端用户产业都在采用自主机器人,大大扩大了该地区 ADR 市场的范围。 2022 年 8 月,Ottonomy Inc. 完成了 330 万美元的种子资金筹措,并宣布 Ottobot 2.0 是其自动送货机器人的最新版本。该公司还打算将 Otto 机器人的部署范围扩大到机场、零售店和餐厅。

- 此外,北美国家是推动该地区物流市场成长的主要力量之一。随着地区国家间贸易量的扩大,该地区对商品的需求激增。 2022年该地区物流市场与前一年同期比较增5.31%。此外,受电子商务成长等因素推动,2022与前一年同期比较商业仓库总建筑面积将年增9.77%。预计预测期内低温运输设施需求将出现强劲成长。该地区物流行业的扩张可能会在预测期内进一步推动所研究市场的成长。

- 2022年10月,美国运输部部投资约3,100万美元扩建货运基础设施并加强供应链。美国政府宣布2022年将资金筹措14亿美元用于铁路基础设施的现代化和升级。墨西哥政府在国家私营部门基础设施投资契约框架下,推出了2020-2024年440亿美元的计划,重点是交通基础设施。加拿大政府也向国家贸易走廊基金投资了超过23亿美元,以促进货运发展。

自动送货机器人产业概况

由于多个区域参与企业的存在,自动送货机器人市场竞争激烈。参与企业正在采用伙伴关係、合併、收购和产品创新等策略来扩大其地理影响力并获得相对于竞争对手的优势。市场的一些主要参与企业包括 Starship Technologies、Ottonomy.IO、Nuro Inc.、Relay Robotics 和 Serve Robotics Inc.

2022 年 5 月,Uber Eats 与路边机器人配送新兴企业Serve Robotics 和自动驾驶汽车技术公司 Motional 合作,在洛杉矶启动了两项自动配送试点。

2022 年 3 月,英伟达向 Uber 分拆出来的人行道机器人送货公司 Serve Robotics 投资 1,000 万美元。 Nvidia 的这项投资预计将推动该市场的研究。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 技术简介

- 评估宏观趋势对市场的影响

第五章 市场动态

- 市场驱动因素

- 管理最后一哩配送的需求

- 物流行业自动化的兴起

- 市场问题

- 天气和安全问题

第六章 市场细分

- 按最终用户

- 医疗

- 饭店业

- 零售和物流

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第七章 竞争格局

- 公司简介

- Starship Technologies

- Relay Robotics, Inc.

- Ottonomy.IO

- Nuro Inc.

- Serve Robotics Inc

- Eliport

- TeleRetail(Aitonomi AG)

- Aethon Inc.

- Kiwibot

- Postmates Inc.

- Segway Robotics Inc.

- Neolix

第八章投资分析

第九章:市场的未来

The Autonomous Delivery Robots Market size is estimated at USD 1.35 billion in 2025, and is expected to reach USD 3.89 billion by 2030, at a CAGR of 23.61% during the forecast period (2025-2030).

The increasing use of autonomous delivery automobiles due to their efficiency is the primary element contributing to the Market's growth. In January 2022, Ottonomy launched Ottobots, a fleet of fully autonomous delivery robots for restaurant and retail industries for outdoor and indoor environments. The pandemic provided Ottobots with a catalyst enabling a series of partnerships that allowed it to launch fully autonomous delivery for curbside, indoor, and last-mile deliveries.

Key Highlights

- Autonomous delivery robots (ADR) have revolutionized delivery procedures, providing a cheaper and more efficient way of delivery. Though delivery robots did not experience high adoption in the past, they are expected to notice increased growth in the future, owing to numerous advantages. The increasing adoption of ADR is mainly driven by the growing affordability and return on investment of a rising variety of infrastructure light robots, along with continuing needs for flexible and efficient automated fulfillment. For instance, in January 2022, Starship Technologies, a significant player in autonomous delivery robots, picked up EUR 50M from the European Union (EU) investment arm to extend its fleet of autonomous delivery robots.

- AI and ML have also greatly benefited the food processing industry, eateries, restaurants, and diners. These technologies, among other things, have sped up the supply chain process and enhanced food delivery services.

- Furthermore, last-mile delivery has been one of the primary problems in handling the supply chain. Last-mile deliveries are getting increasingly complicated in cities, as continued growth in e-commerce and high consumer expectations for faster and regular deliveries are causing traffic congestion and increased carbon pollution. According to the World Economic Forum, the need for last-mile delivery is predicted to grow by 78% globally by 2030

- Losses of about USD 333m incurred due to shipping mishaps, according to the National Retail Federation (NRF). Due to such delivery issues, various consumers and retailers have been looking for better and more efficient delivery methods.

- Also, many retailers have discovered that a superior last-mile experience engages and retains consumers. However, at the same time, meeting customers' delivery expectations does not assist in increasing profit margins, as today's retailers are soaking a part of the cost of last-mile delivery. Therefore, ADR is helping these companies in achieving efficient last-mile delivery.

- Moreover, the logistics sector consumes several natural resources to sustain different operations, such as the delivery of goods. This has also contributed to global warming by disposing of large amounts of greenhouse gases into the atmosphere. Autonomous delivery systems are anticipated to counter such anti-environmental effects by reducing CO2 emissions in the atmosphere.

- Multiple laws are being put in place to control global warming and protect the environment; such initiatives undertaken by governments contribute to the demand growth of ADRs in the Market. For instance, the European Commission has set an objective of decarbonization by 2050, with a few immediate goals in 2020 and 2030.

- Moreover, the government of Delhi recently shared a draft that mandates EVs to cab aggregators, food delivery firms, and E-commerce platforms by 2030. As per officials, the government aims to increase the EV share in overall vehicle sales to 25% by the year 2024. Such activities may further hamper the growth of delivery robots in the Market.

- The COVID-19 pandemic focused attention on delivery robots for contactless package deliveries worldwide, and strong market demand has pushed delivery robot developers to launch large-scale operations in several US cities. The deployment and adoption of delivery robot technology are anticipated to strengthen the Market for delivery robots in the forecasted period. Increasing logistic and healthcare spending worldwide may further drive market growth. According to WHO, the global current health expenditure as a share of the GDP is forecasted to increase between 2023 and 2028 by 0.2% points, and the share is estimated to amount to 10.81% in 2028.

Autonomous Delivery Robots Market Trends

Healthcare Segment is Expected to Register a Significant Growth

- Healthcare applications are one of the considerably advanced forms of autonomous delivery robots. Unlike outdoor delivery robots, autonomous delivery robots deployed in healthcare applications need to consider several other parameters, such as low noise motors, sanitation parameters, and smoother travel compared to regular deliveries.

- Traditionally, robots were installed in several medical establishments for therapeutic use for kids. But now, they are even used to assist the medical staff in fetching the required resources on demand. For example, consider the case of Aethon, a prominent robotics manufacturer based in the US, which offers TUG Robots for medical applications.

- In addition, the TIAGo Delivery and TIAGo Conveyor robots were deployed at the Hospital Municipal of Badalona and Hospital Clinic Barcelona. At the Hospital of Badalona, Sergio Garcia Redondo of the Innovation and Projects Department believes that based on the two use cases they have tested, it's seen a lot of potential, and they will undoubtedly improve the hospital's logistics. And also, the hospital would drastically be able to reduce the necessity to do repetitive tasks with no added value for the patient. Therefore the healthcare staff could concentrate directly on the patient.

- Also, these robots are being utilized at Omaha VA Medical Center to fetch and drop medical supplies on demand. They also sustain the facility by delivering several logistical things and lab samples. In addition, Sheba Medical Center recently partnered with Seamless Vision, an Israeli startup, to create an innovative Autonomous Logistics Infrastructure. The firm plans to launch autonomous medication delivery to patients to ease the pressure on hospital staff in the coming years.

- According to the Bureau of Labor Statistics (BLS), the requirement for nurses is expected to increase by 16%, reaching 3.2mm in 2024 the United States. The aging baby boomers who require additional care will propel much of the growth. Moreover, the spending on healthcare applications is increasing daily, implying the adoption of autonomous delivery robots. For instance, according to IBEF, expenditure on healthcare in India amounted to USD 372 billion in 2022, an increase from the previous year, which was recorded to USD 194 billion.

- Additionally, Aster DM Healthcare declared that it is planning INR 900 crores (USD 120.97 million) capital expenditure over the next three years to enhance its presence in India as it looks at increasing the share of the revenue from the country to 40% of the total earnings by 2025. In addition, in the Union Budget 2023-24, the government allocated USD 10.76 billion to the Ministry of Health and Family Welfare (MoHFW). Such expansion in the healthcare sector in various regions may further propel the studied market demand.

North America to Experience Significant Market Growth

- North America is a substantial market for autonomous delivery robots. Multiple of the significant market dealers are based out in the region. The region also has many start-ups and manufacturers working toward the growth of autonomous delivery robotic technology.

- Along with this, the enhancement of autonomous delivery robots across several end users in the region is relatively high compared to other parts of the world. The requirement for these robots is enormous in the hospitality, logistics, and retail sectors. Many retail and hospitality vendors collaborate with manufacturers to experience the prototypes first-hand. For instance, Google recently invested in Nuro, which is focused on delivering goods using robotic autonomous vehicles. Overall, the company raised USD 600 million in the fundraising round led by Tiger Global Management.

- According to the E-commerce Foundation, North America has the world's highest social network penetration rate, driving its e-commerce industry. Despite reducing labor costs, installing delivery robots also helps hospitality establishments gain popularity on social networks, helping them improve their RevPAR. These activities are expected to keep a steady need for autonomous delivery robots from the hospitality sector.

- Various end-user industries are adopting autonomous robots, significantly expanding the ADR market's scope in the region. In August 2022, Ottonomy Inc. closed its USD 3.3 million seed funding round and declared Ottobot 2.0 the latest version of its autonomous delivery robot. In addition, the company intends to scale up its deployments of Ottobot in airports, retail stores, and restaurants.

- Furthermore, North American countries act as one of the significant forces catalyzing the growth of the logistics market in the region. As a result of extending trade volumes in the countries across the region, the need for goods in the region noticed a steep rise. In 2022, the region's logistics market grew by 5.31% on a YoY basis. In addition, the total commercial warehousing space witnessed a YoY increase of 9.77% in 2022, driven by growth in e-commerce and other factors. The need for cold chain facilities will witness robust growth during the forecast period. Such expansion in the region's logistic sector may further propel the studied market growth in the forecasted period.

- In October 2022, the US Department of Transportation invested around USD 31 million to expand cargo infrastructure and strengthen the supply chain. To modernize and upgrade rail infrastructure, the US government announced a funding amount of USD 1.4 billion in 2022. The Government of Mexico initiated a USD-44-billion plan for 2020-2024, focusing on transportation infrastructure under the National Private Sector Infrastructure Investment Agreement framework. The Government of Canada also invested over USD 2.3 billion in the National Trade Corridors Fund to enhance freight transportation.

Autonomous Delivery Robots Industry Overview

The Autonomous Delivery Robots Market is favorably competitive due to the presence of multiple regional players. The players are adopting strategies like partnerships, mergers, acquisitions, and product innovation to expand their geographic presence and stay ahead of the competitors. Some of the significant players in the Market are Starship Technologies, Ottonomy.IO, Nuro Inc., Relay Robotics, and Serve Robotics Inc., among others.

In May 2022, Uber Eats launched two autonomous delivery pilots in Los Angeles in collaboration with Serve Robotics, a robotic sidewalk delivery startup, and Motional, an autonomous car technology company.

In March 2022, Nvidia invested USD 10 million in Uber spinout Serve Robotics, a sidewalk robot delivery company. This investment by Nvidia will drive the studied Market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat Of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Assessment Of Impact of Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need to Manage Last-mile Deliveries

- 5.1.2 Growing Automation in the Logistics Industry

- 5.2 Market Challenges

- 5.2.1 Weather Conditions and Security Issues

6 MARKET SEGMENTATION

- 6.1 By End Users

- 6.1.1 Healthcare

- 6.1.2 Hospitality

- 6.1.3 Retail & Logistics

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Starship Technologies

- 7.1.2 Relay Robotics, Inc.

- 7.1.3 Ottonomy.IO

- 7.1.4 Nuro Inc.

- 7.1.5 Serve Robotics Inc

- 7.1.6 Eliport

- 7.1.7 TeleRetail (Aitonomi AG)

- 7.1.8 Aethon Inc.

- 7.1.9 Kiwibot

- 7.1.10 Postmates Inc.

- 7.1.11 Segway Robotics Inc.

- 7.1.12 Neolix

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球宅配机器人市场报告

2025年全球宅配机器人市场报告 配送机器人市场承重能力、组件、机器人类型、车轮数量、分销管道和应用划分 - 2025-2030 年全球预测

配送机器人市场承重能力、组件、机器人类型、车轮数量、分销管道和应用划分 - 2025-2030 年全球预测 全球餐厅配送机器人市场

全球餐厅配送机器人市场 2032 年自动送货机器人市场预测:按机器人类型、组件、推进力、车轮数量、负载容量、应用、最终用户和地区进行的全球分析2025年自动送货车辆全球市场报告

2032 年自动送货机器人市场预测:按机器人类型、组件、推进力、车轮数量、负载容量、应用、最终用户和地区进行的全球分析2025年自动送货车辆全球市场报告 全球送货机器人市场(按车轮数量、负载容量、类型、速度限制、最终用途行业和地区划分)—预测至 2030 年

全球送货机器人市场(按车轮数量、负载容量、类型、速度限制、最终用途行业和地区划分)—预测至 2030 年 全球无人包裹递送市场:市场规模(按类型、应用和地区)及未来预测2025年自动送货机器人全球市场报告

全球无人包裹递送市场:市场规模(按类型、应用和地区)及未来预测2025年自动送货机器人全球市场报告 配送机器人市场规模、份额、成长分析(按负载容量、产品、速度限制、车轮、最终用户产业和地区)—产业预测,2025 年至 2032 年全球医疗废弃物处理机器人市场按机器人类型、废弃物类型、技术、应用和最终用户划分 - 预测 2025-2030 年

配送机器人市场规模、份额、成长分析(按负载容量、产品、速度限制、车轮、最终用户产业和地区)—产业预测,2025 年至 2032 年全球医疗废弃物处理机器人市场按机器人类型、废弃物类型、技术、应用和最终用户划分 - 预测 2025-2030 年