|

市场调查报告书

商品编码

1641921

网路切片:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Network Slicing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

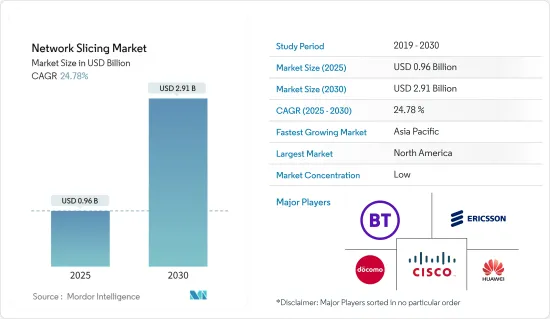

预计 2025 年网路切片市场规模为 9.6 亿美元,到 2030 年将达到 29.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 24.78%。

据 GSMA 称,网路切片与其他推动因素和功能相结合,将帮助营运商在 2025 年前获得价值 3,000 亿美元的商机。

关键亮点

- 5G网路和网路切片的结合将使企业客户能够享受根据其特定业务需求量身定制的连接和资料处理,并遵守与行动通讯业者商定的服务等级协议(SLA)。可自订的网路功能包括资料速度、延迟、品质、安全性和服务。随着高速网路覆盖需求的增加,这将为市场开闢新的途径。

- 然而,由于频宽有限和缺乏基础设施,5G 在新兴国家难以起飞。例如,印度两年前启动的智慧城市计画一直未能取得任何重大进展。除了面临众多地方监管和结构性挑战外,实现智慧城市的愿景还需要增加频谱的可用性或确保足够的频谱。

- 物联网的广泛应用以及连接各种设备、系统和服务的机器对机器(M2M)通讯网路的不断改进正在改变各个行业。 5G 网路切片将实现的众多使用案例之一就是物联网。高功率、低延迟应用(如行动视讯监控)和低功耗、低延迟、远距物联网应用(如智慧城市和智慧工厂)是两类物联网应用需求。为了满足日益增长的物联网应用的需求(其特点是大规模基于机器的通讯和关键任务应用),5G技术的演进预计将加速。

- 然而,网路切片的安全性是CIO们关注的重点,因为它可能会对企业和服务供应商造成重大损失。 SDN、NFV和云端原生架构都被用来建构新的网路基础架构。网路功能分布在本地、区域和中央资料中心,并与支援基础设施分离。云端化5G网路中大部分网路服务将透过公有云和私有云端基础设施来实现。

- 疫情极大地刺激了对宽频服务的需求,行动网路和远端存取服务正在扩展到零售、电讯、IT 和医疗保健等许多行业。此外,随着世界各地的企业开始重新开业,通讯服务供应商正在重新关注 5G 部署并加强网路切片。此外,COVID-19 增加了人们对机器人、远端医疗、远端教育和远距办公等 5G使用案例的兴趣,所有这些都为网路切片市场做出了贡献。

网路切片市场趋势

医疗领域占市场主导地位

- 数以百万计的医疗设备,从家用临床诊断设备到价值数百万美元的医院影像系统,越来越需要连接性作为关键的增值功能。爱立信预测,到 2026 年,通讯业者利用 5G 转型医疗保健将带来 760 亿美元的商机。

- 5G 将在医疗保健领域实现许多新方法,包括影像处理、诊断和资料分析。例如,医院可以透过客製化的5G网路切片使用虚拟实境来安排远端机器人手术,使外科医生看起来就像就在病人旁边一样。

- 它还可以用于医疗资料管理,例如管理电子健康记录和引入救护车无人机。医疗设备製造商可以利用5G即时监控产品功能,并提供预防性和预测性维护协助,以防止设备缺陷造成的负面后果。医疗保健领域的某些关键应用需要极低的延迟和高度一致的频宽。

- 欧洲电信网路营运商协会预测,到2025年医疗保健领域的物联网连接数量将达到103.4亿。这是透过医疗物联网 (IoMT) 实现的,医疗物联网是一个由相互连接的医疗设备、软体程式和医疗系统组成的网络,它使用边缘运算和 5G 无线技术在更靠近源头的地方处理资料。

- 根据欧洲通讯网路营运商协会(ETNO)的调查,未来几年活跃的物联网医疗连接数量预计将增加。 2016年连线数为87万个,预计到2025年将达到1,034万个连线。

亚太地区将经历最高成长

- 预计中国、印度和日本等亚太新兴经济体的网路切片产业将快速扩张。这些国家一贯鼓励和支持工业和技术进步。此外,这些国家拥有先进的技术基础设施,正在推动各个业务领域采用网路切片解决方案。云端基础的解决方案以及物联网、巨量资料分析和行动性等最尖端科技的日益普及正在推动亚太网路产业的发展。亚太地区是最大的连网型设备市场之一。

- 由于网路基础设施的发展和 5G 成为最重要的通讯趋势,预计亚太地区将以最快的速度成长。据GSMA称,亚太地区行动电话营运商计划在2022年至2025年期间投资2,270亿美元部署5G。这笔金额庞大,很可能会产生重大影响。这些新网路不仅能实现创新的新型消费者服务,还将推动经济成长并帮助转型商业和製造业。

- 在亚太地区努力从疫情中復苏之际,连结性对于该地区的重组和增强其抵御未来衝击的能力至关重要。 5G网路、云端服务、边缘运算、人工智慧、巨量资料和物联网对于充分发挥后疫情时代数位经济的潜力都至关重要。

- 5G 的网路切片功能将使通讯业者能够为关键服务供应商提供自己的私有 5G 网络,并提供安全、即时的云端连接,满足不断变化的基础设施需求并简化营运。

- 5G 网路切片与 i.Private 网路、多接取边缘运算(MEC) 等一起添加到目前的技术堆迭中预计将是渐进且有益的。随着 5G 进入大众市场阶段,行动通讯业者的收益可能性开始透过更具适应性、即时的营运支援系统和业务支援系统 (OSS/BSS) 功能实现。

网路切片产业概况

网路切片市场是分散的,参与企业合作提供所需的可用性、指定的延迟、资料速率和安全性。网路切片管理解决方案还能帮助通讯业者实现网路切片生命週期管理,为5G做好准备。主要参与企业包括爱立信公司、华为科技公司、思科系统公司和英国电信集团。

- 2022 年11 月- 为了在无线WAN 架构中建立安全性、SD-WAN 和零信任,Cradlepoint 推出了一种新的针对5G 最佳化的SD-WAN 解决方案,该解决方案“支援网路切片”,作为其今年稍早宣布的NetCloud Exchange 解决方案的一部分。使用 NetCloud Exchange,组织现在可以建立「与 5G 独立 (SA) 网路中定义的切片实例一致的大量数据机 WAN 介面」。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 采用市场驱动因素与限制因素

- 市场驱动因素

- 对高速、大容量网路的需求不断增长,推动市场

- 市场限制

- 新兴国家5G普及率低是市场成长的挑战

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按应用

- 即时监控

- 网路功能虚拟

- 按服务

- 专业的

- 託管

- 按最终用户产业

- 医疗

- 车

- 电能

- 航空

- 媒体与娱乐

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Ericsson Inc.

- Huawei Technologies Co. Ltd

- Cisco Systems Inc.

- BT Group PLC

- NTT DOCOMO Inc.

- NEC Corporation

- ZTE Corporation

- CloudStreet Ltd(Nokia Networks)

- Mavenir Inc.

- Affirmed Networks Inc.

- Argela Technologies

- Aria Networks Ltd

第七章投资分析

第八章 市场机会与未来趋势

The Network Slicing Market size is estimated at USD 0.96 billion in 2025, and is expected to reach USD 2.91 billion by 2030, at a CAGR of 24.78% during the forecast period (2025-2030).

According to GSMA, network slicing, in combination with other enablers and capabilities, will aid operators in addressing a revenue opportunity worth USD 300 billion by 2025.

Key Highlights

- 5G networks, in combination with network slicing, allow business customers to enjoy connectivity and data processing that are tailored to the specific business requirements and adhere to a Service Level Agreement (SLA) as agreed with the mobile operator. Customizable network capabilities include data speed, latency, quality, security, and services. Thus as the demand for high-speed network coverage is progressing, it will open new avenues for the market.

- However, 5G is struggling to keep pace in emerging economies due to low bandwidth and a lack of infrastructure. For instance, India's smart city initiative launched two years ago has struggled to make significant progress. Beyond the numerous local regulatory and structural challenges, there needs to be more spectrum or even the right spectrum bands available for the smart city vision to be realized.

- Various industries are being transformed by the widespread use of IoT and ongoing improvements in Machine-to-Machine (M2M) communication networks, which are connecting all different kinds of equipment, systems, and services. One of the many use cases that network slicing-enabled 5G will allow is the Internet of Things, which would provide communication between a significant number of sensors and linked devices. High-power, low-latency applications (such as mobile video surveillance) and low-power, low-latency, long-range IoT applications are two categories of IoT application requirements (smart cities and smart factories). To meet these needs for growing IoT applications, which are characterized as huge machine-type communication and mission-critical applications, the evolution of 5G Technology is anticipated to pick up speed.

- However, Network slicing security, which may cause significant losses for enterprises and service providers, is a major worry for CIOs. SDN, NFV, and cloud-native architecture have all been used to construct the new network infrastructure. Network functions are spread across local, regional, and central data centers and are decoupled from supporting infrastructure. The vast majority of network services in a 5G network based on the cloud are implemented through public and private cloud infrastructure.

- With the aid of expanding mobile networking and remote access services in a number of industries, including retail, telecom, IT, and healthcare, the pandemic has considerably driven demand for broadband services. Additionally, as businesses all around the world have begun to reopen, communications service providers are refocusing on 5G rollouts and stepping up their network-slicing efforts. Additionally, COVID-19 has increased interest in 5G use cases, including robotics, telemedicine, remote education, and remote offices, all contributing to the network-slicing market.

Network Slicing Market Trends

Healthcare Sector to Dominate the Market

- Millions of medical devices, from at-home clinical diagnostic equipment to hospital-based multimillion-dollar imaging systems, increasingly demand connectivity as a key value-added feature. Ericsson estimates a USD 76 billion revenue opportunity in 2026 for operators addressing healthcare transformation with 5G.

- It will enable many new approaches in the healthcare sector in terms of imaging, diagnosis, and data analytics. For instance, hospitals could arrange remote robotic surgeries, as if the surgeon is right next to the patient, using virtual reality via a customized 5G network slice.

- Also, it can be used in medical data management by maintaining electronic health records or introducing ambulance drones. Medical device makers can utilize 5G to monitor their products' functionality in real-time, providing proactive and predictive maintenance assistance and preventing negative outcomes brought on by faulty equipment. Certain crucial applications in healthcare demand extremely low latency and highly stable bandwidth.

- European Telecommunications Network Operator's Association forecasts that the number of IoT connections in healthcare will reach 10.34 billion by 2025. This is made feasible by the Internet of Medical Things (IoMT), a network of interconnected medical equipment, software programs, and health systems that use edge computing and 5G wireless technology to process data close to the source.

- According to an ETNO-European Telecommunications Network Operators' Association survey, the number of IoT healthcare active connections was expected to increase through the years. It was at 0.87 million connections in 2016 and is expected to reach 10.34 million by 2025.

Asia-Pacific to Witness the Highest Growth

- Several developing economies in APAC, including China, India, and Japan, are anticipated to have rapid expansion in the network-slicing industry. These nations have consistently encouraged and supported the advancement of industry and technology. They also have a sophisticated technological infrastructure that is encouraging the adoption of network-slicing solutions in various business sectors. The increased use of cloud-based solutions, cutting-edge technologies like the IoT, big data analytics, and mobility are what is driving the network industry in APAC. One of the largest markets for connected devices is in APAC.

- APAC is expected to grow at the fastest rate owing to the development of network infrastructure and 5G being the biggest telecom trend. According to GSMA, the Asia Pacific area mobile operators plan to spend USD 227 billion between 2022 and 2025 on 5G deployments. That is a significant sum of money and will have a significant effect. In addition to enabling innovative new consumer services, these new networks are assisting in the transformation of business and manufacturing as well as promoting economic growth.

- Connectivity will be essential to rebuilding Asia-economies Pacific and making them more resilient to future shocks as the region attempts to recover from the pandemic. In order to fully realize the potential of a post-pandemic digital economy, 5G networks, cloud services, edge computing, artificial intelligence (AI), big data, and the Internet of Things will all be crucial.

- 5G's network slicing capabilities will allow telcos to offer critical service providers their own private 5G networks for secure and real-time connectivity to the cloud, helping to meet their ever-evolving infrastructure needs and improve operational efficiency.

- It is expected to increase and will profit from the addition of 5G network slicing to the current technology stack, i.e., together with private networks, Multi-access Edge Computing (MEC), etc. As 5G enters the mass-market phase, the monetization potential for mobile operators is beginning to take shape along with more adaptable and real-time Operations Support System and Business Support System (OSS/BSS) capabilities.

Network Slicing Industry Overview

The Network Slicing Market is fragmented, with players collaborating to provide the required availability, a specified latency, data rate, and security. Network slice management solutions can also help carriers implement network slice lifecycle management in the preparation of 5G. Some major players are Ericsson Inc., Huawei Technologies Co. Ltd, Cisco Systems Inc., and BT Group PLC.

- November 2022 - To include security, SD-WAN, and zero trust into a wireless WAN architecture, Cradlepoint unveiled a new "network slicing-ready" 5G-optimized SD-WAN as part of the company's NetCloud Exchange solution it unveiled earlier this year. Organizations can now construct "many modem WAN interfaces aligned to slice instances defined by 5G standalone (SA) networks" using NetCloud Exchange.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Demand For High-speed And Large Network Coverage is Major Driving Force

- 4.4 Market Restraints

- 4.4.1 Low 5G Penetration in Emerging Economies is Challenging the Market Growth

- 4.5 Industry Attractiveness - Porter's Five Force Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Real-Time Surveillance

- 5.1.2 Network Function Virtualization

- 5.2 By Service

- 5.2.1 Professional

- 5.2.2 Managed

- 5.3 By End-user Industry

- 5.3.1 Healthcare

- 5.3.2 Automotive

- 5.3.3 Power & Energy

- 5.3.4 Aviation

- 5.3.5 Media & Entertainment

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Latin America

- 5.4.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Ericsson Inc.

- 6.1.2 Huawei Technologies Co. Ltd

- 6.1.3 Cisco Systems Inc.

- 6.1.4 BT Group PLC

- 6.1.5 NTT DOCOMO Inc.

- 6.1.6 NEC Corporation

- 6.1.7 ZTE Corporation

- 6.1.8 CloudStreet Ltd (Nokia Networks)

- 6.1.9 Mavenir Inc.

- 6.1.10 Affirmed Networks Inc.

- 6.1.11 Argela Technologies

- 6.1.12 Aria Networks Ltd

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年网路切片市场报告(按组件、最终用户、产业垂直领域和地区)

2025 年至 2033 年网路切片市场报告(按组件、最终用户、产业垂直领域和地区) 网路切片市场按组件、切片类型、切片层级、部署模型、组织规模和最终用户垂直划分 - 全球预测,2025-2030

网路切片市场按组件、切片类型、切片层级、部署模型、组织规模和最终用户垂直划分 - 全球预测,2025-2030 网路切片市场(按产品、最终用户、公司和地区划分)- 预测至 2030 年

网路切片市场(按产品、最终用户、公司和地区划分)- 预测至 2030 年 网路切片市场:2025-2029 年全球

网路切片市场:2025-2029 年全球 网路切片市场机会、成长动力、产业趋势分析及 2025-2034 年预测

网路切片市场机会、成长动力、产业趋势分析及 2025-2034 年预测 全球网路切片市场规模、份额和成长分析:按组件、最终用户、应用、地区 - 产业预测 (2024-2031)

全球网路切片市场规模、份额和成长分析:按组件、最终用户、应用、地区 - 产业预测 (2024-2031) 到 2030 年网路切片市场预测:按组件、应用程式、最终用户和地区分類的全球分析

到 2030 年网路切片市场预测:按组件、应用程式、最终用户和地区分類的全球分析 全球网路切片市场:市场规模、份额、趋势分析 - 按产品、按最终用户、按行业、按地区、展望、预测(2024-2031 年)

全球网路切片市场:市场规模、份额、趋势分析 - 按产品、按最终用户、按行业、按地区、展望、预测(2024-2031 年) 网路切片市场 - 全球产业规模、份额、趋势、机会和预测,按组件、最终用户、按应用、地区、竞争细分,2018-2028 年

网路切片市场 - 全球产业规模、份额、趋势、机会和预测,按组件、最终用户、按应用、地区、竞争细分,2018-2028 年