|

市场调查报告书

商品编码

1641937

微型行动资料中心:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Micro Mobile Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

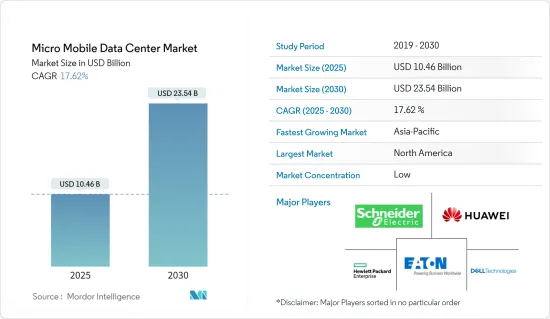

微型行动资料中心市场在 2025 年的估值为 104.6 亿美元,预计到 2030 年将达到 235.4 亿美元,2025 年至 2030 年的复合年增长率为 17.62%。

微型移动资料中心是一个盒状容器,它将传统资料中心所需的所有储存、运算能力和网路装入一个紧凑的封装中。此外,随着技术的进步,云端连接正在整合到边缘的承包包中。

主要亮点

- 微型行动资料中心的尺寸、多功能性和即插即用功能使其成为偏远地区临时部署的理想选择。它们也适合在洪水或地震风险较高的地区临时使用。换句话说,微型资料中心最大限度地减少了传统模型的实体占用空间和能耗。

- 世界数位化不断提高、互联网的普及、智慧技术的相关性、物联网设备、巨量资料以及 5G 网路的市场发展等因素预计将推动微型行动资料中心的市场趋势。爱立信预计,2019年至2028年间,全球5G用户数将大幅成长,从1,200多万增至45亿多万。

- 此外,随着企业办公室定期迁移其基础设施,对货柜型资料中心的需求也日益增长。此外,随着工作量的增加,企业在扩大微型行动资料中心投入的资金也越来越多。这些因素为未来几年的市场扩张创造了巨大的机会。

- 此外,企业正在增加其云端运算业务,因此需要部署可携式资料中心。此外,低成本和低延迟正在推动中小型企业对微型行动资料中心的需求。因此,预计未来市场成长将会加快。然而,与传统资料中心的整合阻碍了市场的成长。

- COVID-19 疫情对市场成长产生了积极影响,微型行动资料中心技术可协助组织满足大容量资料储存需求。在资料储存需求不断增长的背景下,微型行动资料中心营运商面临越来越大的压力,需要确保他们有能力和容量提供高效能微型行动资料中心。疫情过后,由于数位化技术和在家工作的增加,市场蓬勃发展。对软体即服务 (SaaS) 的需求不断增长,正在推动资料中心出现前所未有的流量。这就是玩家投资这些解决方案的原因。

微型行动资料中心市场趋势

医疗保健终端用户预计将占据主要市场占有率

- 微型行动资料中心的采用将有助于为医疗保健产业带来灵活性、有效性、安全性和低成本模式。预计全球医疗保健产业的成长将进一步推动对微型行动资料中心的需求。

- 电子健康记录(EHR)的兴起将进一步推动医疗保健提供者对微型行动资料中心的需求。许多人没有选择用伺服器室取代文件室,而是选择将其 EHR 供应商文件託管在安全的设施中。

- 巨量资料的成长是将资料迁移到云端的另一个动机。透过将不同的资料集整合到云端中,可以在巨量资料分析过程中整合业务、临床和财务资料。这些因素促使医疗保健产业越来越多地采用微型行动资料中心。

- 物联网设备(尤其是智慧型手机)的普及正在推动医疗保健产业对微型行动资料中心的需求。据爱立信预计,今年全球近距离物联网(IoT)设备数量将达166亿。未来三年,这一数字预计将成长至224亿台。预计今年广域物联网设备数量将达到32亿台,未来三年将达52亿台。患者希望按照自己的意愿获得医疗保健。这些医疗设备使丰富的资料能够安全地流经每个护理点,有助于不断改善患者体验和健康结果。

- 随着物联网和云端技术越来越多地融入医疗保健领域,区块链等概念也变得越来越普遍,增加了对资料储存和微型行动资料中心的需求。

- 由于透过区块链产生的资料在医疗保健服务中具有高度敏感性,因此区块链技术用于保护机密记录、存储和验证与用户身份相关的资料以及用于微型移动资料中心在医疗保健行业具有巨大潜力。因此,预计预测期内医疗保健产业对微型行动资料中心的采用将大幅成长。

亚太地区可望成为成长最快的市场

- 亚太地区是全球发展最快的资料中心地区之一。中小型企业对自动化和 BI 工具的采用率也很高。因此,该地区对于研究市场的成长具有巨大的潜力。

- 这种成长很大程度上可以归因于过去十年来政府机构广泛采用资料中心,尤其是在中国和澳洲等国家。政府大力投资资料中心建设,旨在推动该地区的数位经济,从而推动云端服务、巨量资料和物联网的采用。

- 中国对云端运算和其他资料服务的需求正在上升,但资料中心技术的进步将有助于将这些技术与现代製造业结合,帮助中国逐步转型为服务经济。发挥关键作用。

- 中国互联网普及率的不断提高预计也将推动微型行动资料中心需求的成长。随着企业扩大业务范围并提高品质和网路安全,中国对更快、更稳定的宽频连线的需求日益增长。

- 随着主机代管和云端服务供应商承接大型建设计划并建立越来越多的小型商业设施以准备在加速发展的数位化未来中发挥作用,澳洲资料中心的投资前景一片光明。

- 此外,医疗保健、零售、电子商务和垂直资料中心的高渗透率预计将推动市场的进一步成长。此外,随着职场越来越多地采用 BYOD 和 IoT 设备,透过多种来源产生的资料也越来越多。该地区资料量的急剧增长迫使企业投资微型资料中心。

- 在此背景下,混合云端正成为亚太地区采用云的主要途径。混合云端可让您根据应用程式需求(包括合规性和安全性)选择基础架构。

微型行动资料中心产业概况

微型行动资料中心市场高度分散,主要参与者包括Schneider ElectricSE、戴尔 EMC 公司、华为技术有限公司、惠普企业、Development LP 和伊顿公司 PLC。市场参与者正在采取联盟、合併和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2022 年 11 月 - 对于混合IT基础设施管理,Schneider Electric推出了 EcoStruxure 微型资料中心 R 系列 42U 中密度。全新微型资料中心解决方案专为工业环境中的远端 IT 应用而设计,完全整合且易于设定。它还配备了巨型工业脚轮,方便移动。

- 2022年4月-IBM公司宣布将与印度跨国电信业者Airtel合作,在印度提供边缘云端服务。两家公司将透过遍布印度 20 个主要城市的 120 个资料中心为企业提供边缘云端服务。此次合作将透过减少延迟来改善用户体验和业务绩效,同时在工作负载转移到边缘时满足关键的主权需求和资料安全。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 产业影响评估

第五章 市场动态

- 市场驱动因素

- 扩大物联网设备在企业中的使用

- 数位资料产生的速度和数量不断增加

- 市场限制

- 加密劫持威胁

第六章 市场细分

- 按类型

- 小于 25RU

- 25~40RU

- 40RU 或以上

- 按公司类型

- 中小企业

- 大型企业

- 按最终用户产业

- 零售与电子商务

- 教育

- BFSI

- 资讯科技/通讯

- 卫生保健

- 政府和国防

- 能源与公共产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Schneider Electric SE

- Dell EMC Inc.

- Huawei Technologies Co. Ltd

- Hewlett Packard Enterprise Development LP

- Eaton Corporation PLC

- Panduit Corp.

- Zellabox Pty Ltd

- Hitachi Ltd

- IBM Corporation

- Vertiv Co.

- Instant Data Centers LLC

- Dataracks

- Rittal GmbH & Co. Kg

- Canovate Group

第八章投资分析

第九章:市场的未来

The Micro Mobile Data Center Market size is estimated at USD 10.46 billion in 2025, and is expected to reach USD 23.54 billion by 2030, at a CAGR of 17.62% during the forecast period (2025-2030).

Micro mobile data centers are box-like containers filled with the same storage, compute power, and networking needed in a regular data center but delivered in a compact unit. Moreover, with technological advancements, they come with integral cloud connectivity, completing a turnkey package for the edge.

Key Highlights

- The size, versatility, and plug-and-play features of micro mobile data centers make them ideal for use in remote locations for temporary deployments. They are also well suited for temporary use by businesses in locations that are in high-risk zones for floods or earthquakes. In other words, a micro data center minimizes the traditional model's physical footprint and energy consumed.

- Factors such as increasing global digitalization, internet penetration, the relevance of smart technologies, IoT-powered devices, big data, and the development of 5G networks are likely to drive the micro-mobile data center market trends. According to Ericsson, 5G subscriptions are forecast to increase drastically worldwide from 2019 to 2028, from over 12 million to over 4.5 billion, respectively.

- Furthermore, there is a rising need for containerized data centers as corporate offices migrate their infrastructure regularly. Furthermore, corporations spend more on micro-mobile data center growth as workloads increase. Such factors create significant chances for market expansion in the next years.

- Furthermore, businesses are increasing their cloud presence, necessitating the deployment of portable data centers and rising demand for micro mobile data centers for SMEs organizations due to low cost and lower latency. As a result, there would be more prospects for market growth in the future. However, integration with traditional data centers hampers the growth of the market.

- The COVID-19 outbreak positively impacted market growth, and micro-mobile data center technologies are assisting organizations in meeting the high capacity need for data storage. There is a rising requirement to guarantee that micro-mobile data center operators have the ability and capacity to offer high-performance micro-mobile data centers during periods of elevated data storage demand. After the pandemic, the market is growing rapidly with the increased digitization technologies and permanent work from home jobs. Increased demand for software as a service (SaaS) has driven traffic to data centers like never. Hence, players are investing in these solutions.

Micro Mobile Data Center Market Trends

Healthcare End User Vertical is Expected to Hold a Significant Market Share

- Adopting a micro mobile data center helps the healthcare industry bring flexibility, effectiveness, security, and a low-cost model to the healthcare sector. The global healthcare industry's growth is estimated further to drive the demand for micro mobile data centers.

- The growth of electronic health records (EHRs) further increases healthcare providers' demand for micro mobile data centers. Rather than replacing file rooms with server rooms, many opt to have documents hosted by the EHR vendor at a secure facility.

- The growth of Big Data is another motivational factor for transferring data to the cloud. Pulling different datasets together in the cloud allows operational, clinical, and financial data to be aggregated in Big Data analytics processes. These factors contribute to the growing adoption of micro mobile data centers in the healthcare industry.

- The penetration of IoT devices, especially smartphones, boosts the demand for micro mobile data centers in the healthcare industry. According to Ericsson, the number of short-range internet of things (IoT) devices reached 16.6 billion worldwide in the current year. That number is forecast to increase to 22.4 billion by the next three years. The wide-area IoT devices amounted to 3.2 billion in the current year and are predicted to reach 5.2 billion by the next three years. Patients want access to their health organization on their terms. These devices for Healthcare enable enriched data to flow securely through every point of care to help continuously improve the patient experience and health outcomes.

- With IoT and cloud technologies integration into Healthcare, concepts like blockchain are also gaining traction, increasing the demand for data storage and micro mobile data centers.

- Blockchain technology is being used to protect sensitive records and store and authenticate the data related to a user's identity as data generated through blockchain is extremely confidential in healthcare services, like micro mobile data centers have a great healthcare industry scope. Hence, the adoption of micro mobile data centers in the healthcare industry is expected to grow significantly over the forecast period.

Asia-Pacific is Expected to be the Fastest Growing Market

- Asia-Pacific is one of the world's fastest-growing areas for data centers. The adoption of automation and BI tools among SMEs is also high in the region. Hence, the region offers significant potential for the growth of the market studied.

- Much of this growth can be attributed to government agencies' widespread adoption of data centers during the last decade, especially in countries like China and Australia. Major government investments in data center advances, targeted at stimulating the region's digital economy, are boosting the adoption of cloud services, Big Data, and IoT.

- While the demand for cloud computing and other data services continues to increase in China, advancements in data center technology are expected to play a vital role in the integration of these technologies with modern manufacturing and China's gradual transition to a service economy.

- Increasing internet penetration in China would also help increase the demand for micro mobile data centers. Demand for faster, more stable broadband connections is growing in China as companies look to enhance their presence and provide enhanced quality and cybersecurity.

- The Australian investment outlook for data centers remains positive as colocation and cloud providers launch major construction projects and an armada of smaller enterprise facilities to prepare for a role in the accelerating digital future.

- In addition, factors, including high penetration rates in healthcare, retail, e-commerce, and BFSI verticals, are expected to drive the market's growth further. Moreover, the data generated through multiple sources is high due to the high adoption of BYOD and IoT devices in the workplace. The exponential growth of data proliferation in the region is forcing enterprises to invest in micro data centers.

- In the backdrop of current trends, hybrid cloud is emerging as a popular way forward for cloud adoption in Asia-Pacific, as it offers a choice of infrastructure depending on application requirements for compliance and security.

Micro Mobile Data Center Industry Overview

The micro mobile data center market is highly fragmented, with the presence of major players like Schneider Electric SE, Dell EMC Inc., Huawei Technologies Co. Ltd, Hewlett Packard Enterprise, Development LP, and Eaton Corporation PLC. Players in the market are adopting strategies such as partnerships, mergers, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2022 - For hybrid IT infrastructure management, Schneider Electric launched the EcoStruxure Micro Data Center R-Series 42U Medium Density. The new Micro Data Center solution is designed for IT applications in distant locations with industrial conditions, and it delivers fully integrated for easy setup. It also has a hefty weight capacity and huge industrial casters for convenient mobility.

- April 2022 - IBM Corporation announced a collaboration with Airtel, an Indian multinational telecommunications company, to provide edge cloud services in India. Together companies would supply edge cloud services to enterprises through 120 data centers spread across 20 major Indian cities. The collaboration improves the user experience and company performance by reducing latency while fulfilling sovereignty needs and data security, which is crucial as workloads travel to the edge.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Penetration of IOT Devices Enterprises

- 5.1.2 Increasing Speed and Volume of Digital Data Generation

- 5.2 Market Restraints

- 5.2.1 Cryptojacking Threats

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Up to 25 RU

- 6.1.2 25-40 RU

- 6.1.3 Above 40 RU

- 6.2 By Enterprise Type

- 6.2.1 Small and Medium Enterprise (SME)

- 6.2.2 Large Enterprise

- 6.3 By End-user Vertical

- 6.3.1 Retail and E-commerce

- 6.3.2 Education

- 6.3.3 BFSI

- 6.3.4 IT and Telecommunication

- 6.3.5 Healthcare

- 6.3.6 Government and Defense

- 6.3.7 Energy and Utilities

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Dell EMC Inc.

- 7.1.3 Huawei Technologies Co. Ltd

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Eaton Corporation PLC

- 7.1.6 Panduit Corp.

- 7.1.7 Zellabox Pty Ltd

- 7.1.8 Hitachi Ltd

- 7.1.9 IBM Corporation

- 7.1.10 Vertiv Co.

- 7.1.11 Instant Data Centers LLC

- 7.1.12 Dataracks

- 7.1.13 Rittal GmbH & Co. Kg

- 7.1.14 Canovate Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

微型移动资料中心市场规模、份额、成长分析、按组件、按类型、按框架单位、按外形规格、按组织规模、按应用、按垂直行业和按地区 - 2025 年至 2032 年行业预测

微型移动资料中心市场规模、份额、成长分析、按组件、按类型、按框架单位、按外形规格、按组织规模、按应用、按垂直行业和按地区 - 2025 年至 2032 年行业预测 2025年微型资料中心全球市场报告

2025年微型资料中心全球市场报告 微型资料中心市场 - 成长、未来展望、竞争分析,2025 年至 2033 年

微型资料中心市场 - 成长、未来展望、竞争分析,2025 年至 2033 年 微型资料中心市场规模、份额和成长分析(按组件、应用、框架单位、组织规模、外形规格、类型、垂直和地区)- 产业预测 2025-20322025 年全球微型移动资料中心市场报告

微型资料中心市场规模、份额和成长分析(按组件、应用、框架单位、组织规模、外形规格、类型、垂直和地区)- 产业预测 2025-20322025 年全球微型移动资料中心市场报告 微型移动资料中心市场:按框架单位、组织规模、应用、产业 - 2025-2030 年全球预测

微型移动资料中心市场:按框架单位、组织规模、应用、产业 - 2025-2030 年全球预测 微型移动资料中心市场规模、份额、趋势分析报告:按框架单位、按公司规模、按应用、按行业、按地区、细分市场预测,2025-2030 年

微型移动资料中心市场规模、份额、趋势分析报告:按框架单位、按公司规模、按应用、按行业、按地区、细分市场预测,2025-2030 年 微型行动资料中心市场 - 全球产业规模、份额、趋势、机会和预测,按类型、企业类型(中小企业、大型企业)、最终用户、地区、竞争进行细分,2019- 2029F

微型行动资料中心市场 - 全球产业规模、份额、趋势、机会和预测,按类型、企业类型(中小企业、大型企业)、最终用户、地区、竞争进行细分,2019- 2029F 微型资料中心市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按机架类型、组织规模、应用程式和地理位置

微型资料中心市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按机架类型、组织规模、应用程式和地理位置 微型资料中心市场报告:2030 年趋势、预测与竞争分析

微型资料中心市场报告:2030 年趋势、预测与竞争分析