|

市场调查报告书

商品编码

1641943

紫外线固化黏合剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)UV-Curable Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

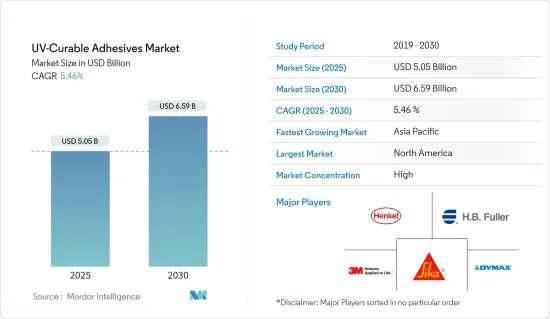

预计 2025 年紫外线固化黏合剂市场规模为 50.5 亿美元,到 2030 年将达到 65.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.46%。

2020 年,新冠疫情导致全国范围的封锁、製造活动和供应链的中断以及全球范围内的生产停顿,对市场产生了负面影响。然而,2021年情况开始好转,市场也因此恢復了成长轨迹。

主要亮点

- 推动市场发展的首要因素是汽车和航太应用对紫外线胶黏剂的需求不断增加,以及环境法规对紫外线胶合剂的需求不断增加。

- 然而,紫外线固化黏合剂的高製造成本和替代黏合剂的可用性预计会阻碍市场的成长。

- 包装行业的需求不断增长和紫外线固化黏合剂技术的改进预计将为市场研究带来机会。

- 北美占据全球市场主导地位,其中美国的消费量最高。

紫外线固化胶黏剂的市场趋势

市场区隔强劲成长

- 紫外线固化黏合剂以其耐用性、生物相容性、润滑性以及抗化学性和耐刮擦性而闻名,这使其对于满足各种医疗应用的标籤标准至关重要。其中包括药品、药物贴片、水凝胶、过滤器、试纸以及血袋和医疗用电子设备等一次性物品。

- 紫外线固化黏合剂由于其独特的性能,在医疗产业中占有一席之地。紫外线固化黏合剂在组装医疗设备时非常有用,特别是在黏合导管组件时,可以提供牢固、无洩漏的密封。

- 中国是世界上最大且成长最快的医疗保健市场之一。 2023年,国家药品监督管理局(NMPA)将总合批准第三类(国内外)和第二类(国外)医疗设备和体外诊断器材的新註册、延续註册和许可事项变更13,260件。已被接受。与2022年相比,申请数量增加了25.4%。全国药品註册申请13260件,其中国家药监局总合核准12213件,比前一年核准278件。

- 近年来,印度医疗保健和医疗设备产业经历了显着的成长。印度生产植入式医疗设备医疗设备设备等各种各样的医疗设备。印度製造的大多数医疗设备都是导管、灌溉套件、延长线、插管、餵食管、针头和注射器等消耗品,以及心臟支架、药物释放型支架、人工水晶体和整形外科植入。植入。

- 据MedTech Europe称,预计2024年欧洲医疗技术市场规模将达到约1,600亿欧元(1,772.5亿美元)。主要市场包括德国、法国、英国、义大利和西班牙。以製造商价格计算,欧洲医疗设备市场占全球市场的26.1%,是仅次于美国的47.2%的第二大股东。过去十年,欧洲医疗设备市场年均成长率为5.4%。 2024年,欧洲医疗设备贸易顺差将达到110亿欧元。与往年一样,欧洲医疗设备的主要贸易伙伴是美国、中国、日本和墨西哥。

- 所有上述因素都显示未来几年市场需求成长前景乐观。

北美占据市场主导地位

- 预计北美国家将主导紫外线固化黏合剂市场。最近,美国和加拿大对半导体生产的投资增加,推动了该地区对紫外线固化胶合剂的需求。

- 2024年8月,美国商务部宣布将向德克萨斯投资16亿美元,以提高其半导体产量。一旦全面运作,德克萨斯谢尔曼工厂每天将生产超过 1 亿个晶片。

- 2024 年 7 月,加拿大创新、科学与经济发展部 (ISED) 宣布向 FABrIC(网际网路边缘整合组件製造)网路投资 1.2 亿美元。该五年计画总额超过 2.2 亿美元,将加强加拿大半导体的製造和商业化。

- 近年来,医疗产业也成为该地区紫外线固化黏合剂的主要消费者。紫外线固化黏合剂广泛应用于医疗领域,包括医疗设备中的注射器和电子元件的组装。

- 北美拥有全球最大的医疗设备产业,以美国为首。最近,全国各地对新的医疗保健製造设施进行了大量投资。

- 2023年11月,美国製药公司礼来公司同意投资约25亿美元在德国建造新的製药製造工厂,生产注射和医疗设备,包括治疗糖尿病和肥胖症的药物。该运作。

- 这些发展预计将促进製药和医疗设备製造领域对紫外线固化黏合剂的需求。

- 预计所有这些因素将在预测期内推动北美对紫外线固化黏合剂市场的需求。

紫外光固化胶黏剂产业概况

紫外线固化黏合剂市场分散,市场参与企业多种多样,既有大型企业,也有小型区域企业。主要市场参与者(不分先后顺序)包括汉高股份公司、HB Fuller 公司、3M 公司、西卡股份公司、Dymax 等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 紫外线固化黏合剂在汽车和航太工业中越来越受欢迎

- 由于有利的环境法规而更加受欢迎

- 其他驱动因素

- 限制因素

- 生产紫外线固化黏合剂的高成本

- 替代产品的可用性

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 依树脂类型

- 硅胶

- 丙烯酸纤维

- 聚氨酯

- 环氧树脂

- 其他树脂类型

- 按最终用户产业

- 医疗

- 电气和电子

- 运输

- 包装

- 家具

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- 3M

- Delo

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Master Bond Inc.

- Panacol-elosol Gmbh

- Parson Adhesives Inc.

- Permabond LLC

- Sika AG

第七章 市场机会与未来趋势

- 蓬勃发展的包装产业对紫外线固化黏合剂的需求不断增加

- 与尖端科技融合

The UV-Curable Adhesives Market size is estimated at USD 5.05 billion in 2025, and is expected to reach USD 6.59 billion by 2030, at a CAGR of 5.46% during the forecast period (2025-2030).

Due to the COVID-19 pandemic, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, conditions started recovering in 2021, thereby restoring the growth trajectory of the market.

Key Highlights

- The major factors driving the market studied are the rising demand for UV adhesives in automotive and aerospace applications and the increasing demand for these adhesives due to favorable environmental regulations.

- On the flip side, the high cost of producing UV-curable adhesives and the availability of alternative adhesives are expected to hinder the market's growth.

- An increase in demand from the packaging industry and a rise in the technologies for UV-curable adhesives are expected to act as opportunities for the market studied.

- North America dominated the global market, with the highest consumption registered in the United States.

UV-Curable Adhesives Market Trends

Medical Segment to Witness Strong Market Growth

- UV-curable adhesives, celebrated for their durability, biocompatibility, lubricity, and resistance to chemicals and scratches, are pivotal in meeting labeling standards for various medical applications. These include medicines, medication patches, hydrogels, filters, test strips, and disposable items like blood bags and medical electronics.

- Owing to their distinct properties, UV-curable adhesives are carving a niche in the medical industry. They are instrumental in medical device assembly, notably bonding catheter components for robust, leak-proof seals.

- China is one of the world's largest and fastest-growing healthcare markets. In 2023, the National Medical Products Administration (NMPA) received a total of 13,260 applications for initial registrations, registration renewals, and changes in licensing items of Class III (Domestic and Overseas) and Class II (Overseas) medical devices and IVDs. The number of applications represented a 25.4% increase when compared to 2022. Of the 13,260 applications, the NMPA approved a total of 12,213 applications, and an additional 278 products were approved in comparison with the previous year.

- The healthcare and medical device industries in India have experienced significant growth in recent years. A wide range of medical devices, from consumables to implantable medical devices, are manufactured in India. Most medical devices produced in India are disposables like catheters, perfusion sets, extension lines, cannulas, feeding tubes, needles, syringes, and implants like cardiac stents, drug-eluting stents, intraocular lenses, and orthopedic implants.

- As per MedTech Europe, the European medical technologies market has been projected to reach approximately EUR 160 billion (USD 177.25 billion) in 2024. The leading markets include Germany, France, the United Kingdom, Italy, and Spain. Valued at manufacturer prices, the European medical devices market constitutes 26.1% of the global market, making it the second-largest shareholder after the United States, which accounts for a 47.2% share. Over the past decade, the European medical devices market registered an average annual growth of 5.4%. In 2024, Europe boasts a positive trade balance in medical devices, standing at EUR 11 billion. Consistent with previous years, Europe's primary trade partners for medical devices have been the United States, China, Japan, and Mexico.

- All the abovementioned factors indicate a positive outlook for growth in market demand over the coming years.

North America to Dominate the Market

- North American countries are expected to dominate the UV-curable adhesives market. In recent times, there have been growing investments in semiconductor production in the United States and Canada, which has propelled demand for UV-curable adhesives in the region.

- In August 2024, the US Department of Commerce announced a USD 1.6 billion investment to enhance semiconductor production at Texas Instruments. Once fully operational, TI's Sherman facilities are projected to churn out over 100 million chips daily.

- In July 2024, Innovation, Science and Economic Development Canada (ISED) unveiled a USD 120 million investment into the FABrIC (Fabrication of Integrated Components for the Internet's Edge) network. This five-year initiative, with a total commitment exceeding USD 220 million, is set to strengthen Canada's semiconductor manufacturing and commercialization landscape.

- The medical industry has been another major consumer of UV-curable adhesives in the region in recent times. UV-curable adhesives are used in a wide range of medical applications, including syringe assembly and electronic components in medical devices.

- North America boasts the largest medical devices industry globally, spearheaded by the United States. In recent times, significant investments have been made in new healthcare manufacturing facilities across the country.

- In November 2023, Eli Lilly, a US pharmaceutical company, invested around USD 2.5 billion to build a new pharmaceutical manufacturing facility in Germany for producing injectable pharmaceutical products and medical devices, including those for diabetes and obesity. The construction began in 2024, and the facility is expected to be operational by 2027.

- Such developments are expected to boost the demand for UV-curable adhesives in pharmaceutical products and medical device manufacturing.

- All such factors are expected to boost the demand in the North American UV-curable adhesives market during the forecast period.

UV-Curable Adhesives Industry Overview

The UV-curable adhesives market is fragmented and features diverse participants, ranging from major corporations to smaller regional entities. The major market players (not in any particular order) include Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Sika AG, and Dymax.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 UV-curable Adhesives Gaining Traction in the Automotive and Aerospace Sectors

- 4.1.2 Growing Popularity Due to Favorable Environmental Regulations

- 4.1.3 Others Drivers

- 4.2 Restraints

- 4.2.1 High Costs Associated With the Production of UV-curable Adhesives

- 4.2.2 Availability of Substitutes

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Silicone

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.1.4 Epoxy

- 5.1.5 Other Resin Types

- 5.2 End-user Industry

- 5.2.1 Medical

- 5.2.2 Electrical and Electronics

- 5.2.3 Transportation

- 5.2.4 Packaging

- 5.2.5 Furniture

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Delo

- 6.4.3 Dymax

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Master Bond Inc.

- 6.4.7 Panacol-elosol Gmbh

- 6.4.8 Parson Adhesives Inc.

- 6.4.9 Permabond LLC

- 6.4.10 Sika AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand for UV-curable Adhesives in the Booming Packaging Industry

- 7.2 Integration With Advanced Technologies

紫外线固化胶合剂市场-全球产业规模、份额、趋势、机会和预测,按树脂类型、应用、地区和竞争情况细分,2020-2030 年

紫外线固化胶合剂市场-全球产业规模、份额、趋势、机会和预测,按树脂类型、应用、地区和竞争情况细分,2020-2030 年 紫外线黏合剂市场 - 预测 2025-2030

紫外线黏合剂市场 - 预测 2025-2030 紫外线黏合剂市场(按产品类型、应用和地区)

紫外线黏合剂市场(按产品类型、应用和地区) 2025年全球紫外线固化胶合剂市场报告

2025年全球紫外线固化胶合剂市场报告 2025-2030 年全球紫外光固化胶合剂市场(按树脂类型、配方、应用和最终用户划分)预测

2025-2030 年全球紫外光固化胶合剂市场(按树脂类型、配方、应用和最终用户划分)预测 2025-2033年紫外光固化胶黏剂市场报告(依树脂类型、基材、最终用户和地区)2025年紫外线黏合剂全球市场报告

2025-2033年紫外光固化胶黏剂市场报告(依树脂类型、基材、最终用户和地区)2025年紫外线黏合剂全球市场报告 紫外线黏合剂市场规模、份额和成长分析(按产品类型、应用和地区)- 产业预测 2025-2032

紫外线黏合剂市场规模、份额和成长分析(按产品类型、应用和地区)- 产业预测 2025-2032 UV硬化型黏剂的全球市场:树脂类型·基材·终端用户·不同地区的预测 (~2032年)

UV硬化型黏剂的全球市场:树脂类型·基材·终端用户·不同地区的预测 (~2032年) 全球紫外线固化黏剂市场(2024-2028)

全球紫外线固化黏剂市场(2024-2028)