|

市场调查报告书

商品编码

1641946

碳化硅功率半导体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Silicon Carbide Power Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

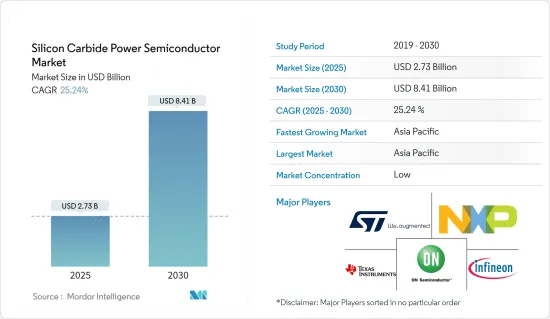

碳化硅功率半导体市场规模预计在 2025 年为 27.3 亿美元,预计到 2030 年将达到 84.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 25.24%。

疫情的爆发对全球大、中、小型产业造成了经济衝击。这是因为很大一部分製造业涉及工厂车间工作,人们在车间密切接触以提高生产率。

关键亮点

- SiC(碳化硅)具有较宽的带隙,因此可用于高功率应用。 SiC 有许多不同的多型体,但 4H-SiC 是最适合功率元件的多型体。旨在提高材料性能的研发活动的增加预计将成为市场成长的强大动力。例如,美国能源局(DOE) 高级研究计划署 (ARPA-E) 宣布为 21 个计划提供3000 万美元的资金,作为其利用创新拓扑和半导体创建创新和可靠电路(CIRCUITS) 计划的一部分。到了。而美国能源部对国家再生能源实验室主导的研究的投资,旨在降低碳化硅电力电子装置的製造成本,这些措施可能会进一步支持这一趋势,扩大更强大的碳化硅电力元件的范围。

- 电动车为汽车产业带来了某些好处,例如提高了行驶里程、充电时间以及满足客户期望的性能。然而,电动车需要在高温下高效运作的电力电子设备。因此,采用宽能带隙SiC 技术的电源模组的开发正在进行中。

- 随着价格下降和行驶里程增加,电动车如今变得越来越普遍。根据国际能源总署的报告《2021年全球电动车展望》,2020年道路上的轻型电动乘用车超过1,020万辆。此外,2020 年电动车註册量成长了 41%,为市场创造了成长机会。

- 半导体也正在使用 SiC 来减少能量损失并延长太阳能和风力发电转换器的使用寿命。例如,太阳能光电能主要需要高功率、低损耗、快速开关和高可靠的半导体装置来提高效率、功率密度和可靠性。因此,SiC 装置代表了满足光伏能源需求的一种有前途的解决方案,可满足日益增长的能源需求。

- 一些公司正在进入 SiC 功率半导体市场,以利用清洁技术需求所提供的潜力。例如,2021 年 4 月,纽约州立大学理工学院 (SUNY Poly) 的子公司 NoMIS Power Group 成立了一家业务部门,设计、製造和销售 SiC 功率半导体装置、模组,并为电力产业提供支援服务。开发商。

- 此外,在高频下工作时,SiC 功率半导体的寄生电容和电感会增加,因此无法发挥其全部潜力。由于这些原因,SiC 的广泛采用可能需要更新製造设备,而这以目前的发展速度是无法实现的。

碳化硅功率半导体市场趋势

汽车产业可望实现强劲成长

- 关于在汽车动力传动系统中使用碳化硅 (SiC) 装置的研究活动正在进行中。然而,最近的进展正在慢慢使其成为可行的解决方案。例如,采用快速充电解决方案的特斯拉如今已在其车辆架构中使用SiC。此外,随着价格下降和行驶里程增加,电动车如今变得越来越普遍。根据国际能源总署(IEA)的数据,2021年全球插电式电动车销量将达到约660万辆。

- SiC 半导体非常适合插电式混合动力汽车(PHEV) 和全电动汽车 (EV) 中使用的车载充电器和逆变器等应用。这是因为它的能源效率明显高于传统的硅。

- 此外,为了使电动车能够远距行驶并在合理的时限内充电,车辆的电力电子设备必须能够承受高温。 SiC半导体具有能源效率超过95%的优势。在电力转换过程中,例如使用高功率快速充电器充电时,只有 5% 的能量以热量的形式损失。

- 在日本,东京大学正与三菱电机公司合作提高SiC半导体装置的可靠性。此前,三菱电机发布了专为混合动力汽车设计的新型超紧凑型SiC逆变器,目标于2021年左右实现量产。

- 此外,德尔福科技与 Cree 也合作开发了采用 Cree SiC MOSFET 的德尔福科技逆变器。这显着降低了整个电源模组的温度,同时实现了支援混合动力汽车和全电动汽车扩大续航里程的高功率。这些逆变器比竞争型号重量轻 40%,体积紧凑 30%。

- 此外,英飞凌科技于 2021 年 5 月宣布推出采用汽车 CoolSiC MOSFET 技术的新型功率模组。透过使用 SiC 代替 Si,我们能够实现电动车转换器的更高效率。例如,现代汽车集团在其牵引逆变器中使用了英飞凌的CoolSiC 功率模组,由于SiC 解决方案的损耗较低,效率高于Si 基解决方案,因此将车辆续航里程延长了5% 以上。据报道那

- 此外,2021 年 3 月,英国政府宣布拨款製造碳化硅 (SiC) 功率半导体装置,以协助开发用于交通、家庭和工业的更高效的电力电子设备,这是英国研究与创新主导的工业战略挑战基金的一部分并向斯旺西大学拨款 480 万英镑用于创建该项目并帮助国家实现净零目标。

亚太地区将经历最快成长

- 亚太地区在全球 SiC 功率半导体市场中占据主导地位,这与全球半导体市场的成长息息相关,同时也受到政府措施的支持。此外,该地区的半导体产业由中国大陆、台湾、日本和韩国推动,这四个国家合计占据全球离散半导体市场的约 65%。相较之下,泰国、越南、新加坡和马来西亚等国家也对该地区的市场主导地位做出了重大贡献。

- 根据印度电子和半导体协会的数据,到 2025 年印度半导体元件市场价值预计将达到 323.5 亿美元,复合年增长率为 10.1%(2018-2025 年)。该国是全球研发中心的理想目的地。因此,印度政府的「印度製造」倡议有望带动半导体市场的投资。

- 此外,该地区也是一个电子中心,每年生产数百万台电子设备,出口到其他国家并供该地区消费。如此高的电子元件和设备产量对所研究市场的份额贡献巨大。例如,印度对家用电子电器的需求不断增长也推动了该地区市场的成长。据IBEF称,到2024财年,印度对电子硬体的需求预计将达到4,000亿美元,这将进一步推动市场成长。

- 中国是世界上最大的电力生产国。该国的能源需求预计将增加,因此能源产量也预计将增加。例如,根据国际能源总署的数据,中国的电动车销量成长了一倍多,到2021年,中国的电动车销量将比其他国家多出约330万辆。

- 中国汽车工业正在崛起,并在全球汽车市场中发挥越来越重要的作用。中国政府把汽车产业,包括零件产业定位为重点产业之一。政府预计2020年中国汽车产量将达3,000万辆,到2025年将达到3,500万辆。

- 此外,由于政府雄心勃勃的计划和倡议,印度的电动车市场正在蓬勃发展。印度公共部门机构近年来宣布了多项与电动车相关的倡议,展现了在该国广泛推广电动车的坚定承诺、具体行动和雄心勃勃的目标。

碳化硅功率半导体产业概况

碳化硅功率半导体市场竞争激烈。其中包括英飞凌科技股份公司、德州仪器公司、义法半导体公司、日立功率半导体装置有限公司、恩智浦半导体、富士电机、西米控国际有限公司、科锐公司、安森美半导体公司和三菱电机公司。这些公司正在推出新产品、建立合作伙伴关係以及进行收购以增加市场占有率。

- 2021 年 6 月-日本电子公司日立宣布计划扩大在希尔斯伯勒的现有业务,并建立一个大型半导体实验室,与美国製造业客户合作创造新技术。

- 2021年4月-英飞凌科技股份公司在其1200V产品线中推出了全新的EasyPACK 2B模组。本模组具有三级主动 NPC (ANPC) 拓扑结构,包括 CoolSiC MOSFET、TRENCHSTOP IGBT7 装置、NTC 温度感测器和 PressFIT 接触技术引脚。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 市场影响

- 技术简介

第五章 市场动态

- 市场驱动因素

- 消费性电子产品和无线通讯的需求不断增长

- 对节能、电池供电便携式设备的需求不断增加

- 市场问题

- 硅片短缺和驱动要求的变化

第六章 市场细分

- 按最终用户产业

- 汽车(电动车和电动车充电基础设施)

- 资讯科技/通讯

- 电力(电源、UPS、光伏、风能等)

- 工业(马达驱动)

- 其他终端用户产业(铁路、石油和天然气、军事、医疗、研发等)

- 按地区

- 美洲

- 欧洲、中东和非洲

- 亚太地区

第七章 竞争格局

- 公司简介

- Infineon technologies AG

- UnitedSiC

- ST Microelectronics NV

- ON Semiconductor Corporation

- GeneSiC Semiconductor Inc.

- Danfoss A/S

- Microsemi Corporation

- Toshiba Corporation

- Mitsubishi Electric Corporation

- Fuji Electric Co. Ltd

- Semikron International

第八章投资分析

第九章:市场的未来

The Silicon Carbide Power Semiconductor Market size is estimated at USD 2.73 billion in 2025, and is expected to reach USD 8.41 billion by 2030, at a CAGR of 25.24% during the forecast period (2025-2030).

The pandemic outbreak created economic turmoil for small, medium, and large-scale industries worldwide. Adding to the woes, the country-wide lockdown inflicted by the governments across the globe (to minimize the spread of the virus) further resulted in industries taking a hit and disruption in supply chain and manufacturing operations across the world, as a large part of manufacturing includes the work on the factory floor, where people are in close contact as they collaborate to boost the productivity.

Key Highlights

- SiC (Silicon Carbide) is used for high-power applications due to the wide bandgap offered. While various polytypes (polymorphs) of SiC exist, 4H-SiC is the most ideal for power devices. The increase in R&D activities that target enhanced material capabilities is expected to provide a strong impetus for market growth. For instance, the United States Department of Energy's (DOE) Advanced Research Projects AgencyEnergy (ARPA-E) has announced a funding of USD 30 million for 21 projects as part of the Creating Innovative and Reliable Circuits Using Inventive Topologies and Semiconductors (CIRCUITS) program. Also, initiatives such as investment by US DOE for NREL-Led research with an intent to reduce SiC power electronics manufacturing costs could further support such trends and expand the scope of more robust SiC-based devices.

- Electric vehicles provide certain advantages within the automotive industry, such as increased range, charge-time, and performance, to meet customer expectations. However, they require power electronic devices capable of efficient and effective operation at elevated temperatures. Hence, power modules are being developed using wide-bandgap SiC technologies.

- Electric cars are becoming common on the road nowadays with prices coming down and range going up. As per the International Energy Agency's report Global EV Outlook 2021, over 10.2 million light-duty electric passenger cars were on the roads in 2020. In addition, electric car registration increased by 41% in 2020, which creates growth opportunities for the market.

- Semiconductors also use SiC for reduced energy loss and longer life solar and wind energy power converters. For instance, photovoltaic energy mainly requires high power, low loss, faster switching, and reliable semiconductor devices to increase efficiency, power density, and reliability. Thus, SiC devices provide a promising solution to photovoltaic energy requirements to meet the increasing energy demand.

- To tap the potential brought by the demand for cleantech, several players are entering the market for SiC power semiconductors. For instance, in April 2021, NoMIS Power Group, a spin-off from the State University of New York Polytechnic Institute (SUNY Poly), announced that it plans to design, manufacture and sell SiC power semiconductor devices, modules, and services for providing support to power management product developers.

- Moreover, parasitic capacitance and inductance become too great as soon as high frequencies are used, preventing the SiC-based power device from realizing its full potential. In such a regard, widespread usage of SiC may require updates to manufacturing facilities, something which cannot be achieved at the current pace of development.

Silicon Carbide Power Semiconductor Market Trends

Automotive Industry is Expected to Register Significant Growth

- Research activities are being conducted into the usage of silicon carbide (SiC) devices within automotive powertrains. However, due to recent advancements, it is gradually becoming a feasible solution. For instance, Tesla, which uses a rapid charging solution, is already using SiC within their vehicle architectures currently. In addition, electric cars are becoming common on the road nowadays with prices coming down and range going up. According to the International Energy Agency, plug-in electric light vehicle sales across the globe reached around 6.6 million in 2021.

- SiC semiconductors are ideal for applications, such as onboard chargers and inverters, being used within the plug-in hybrid (PHEV) and fully electric vehicles (EVs). This is because their energy efficiency is significantly higher compared to traditional silicon.

- Also, to ensure that EVs can operate over long distances and charge within a reasonable timeframe, the vehicle's power electronics must be capable of handling high temperatures. SiC semiconductors benefit from more than 95% energy efficiency. Only 5% of energy is lost as heat during power conversion, such as recharging the vehicle with a high-power rapid-charger.

- In Japan, the University of Tokyo has been working with Mitsubishi Electric Corporation to enhance the reliability of SiC semiconductor devices. Earlier, Mitsubishi Electric revealed a new ultra-compact SiC inverter designed for hybrid vehicles, with mass commercialization targeted around 2021.

- Moreover, Delphi Technologies and Cree have partnered to create the former's inverters, combined with Cree's SiC MOSFETs. It has significantly reduced the power module's overall temperature while enabling higher power outputs to support an extended range for hybrid and fully electric automobiles. These inverters are also 40% lighter and 30% more compact than competing models.

- Further, in May 2021, Infineon Technologies launched a new power module with CoolSiC MOSFET technology for automotive applications. The use of SiC instead of Si ensures higher efficiency in converters in electric vehicles. For example, Hyundai Motor Group reported that it was able to increase the range of its vehicles by more than 5% because of efficiency gains resulting from the lower losses of this SiC solution compared to the Si-based solution, with the help of the traction inverters based on Infineon's CoolSiC power module.

- Moreover, in March 2021, as part of the Industrial Strategy Challenge Fund led by the UK Research and Innovation, the UK government awarded GBP 4.8 million to Swansea University to manufacture silicon carbide (SiC) power semiconductor devices and create more efficient power electronics for transportation, homes, and industry, and help the nation achieve its net-zero ambitions.

Asia Pacific to Witness the Fastest Growth

- The Asia Pacific dominates the global SiC power semiconductor market, pertaining to global semiconductor market growth, which is also supported by government policies. Furthermore, the region's semiconductor industry is driven by China, Taiwan, Japan, and South Korea, which together account for around 65% of the global discrete semiconductor market. In contrast, others like Thailand, Vietnam, Singapore, and Malaysia also contribute significantly to the region's dominance in the market.

- According to the Indian Electronics and Semiconductor Association, India's semiconductor component market is expected to be worth USD 32.35 billion by 2025, displaying a CAGR of 10.1% (2018-2025). The country is a lucrative destination for worldwide R&D centers. Therefore, the government's ongoing Make In India initiative is expected to result in investments in the semiconductor market.

- Moreover, the region is an electronics hub that produces millions of electronic devices every year for exporting to other countries and consumption in the area. This high production of electronic components and devices largely contributes to the market share of the studied market. For instance, the increasing demand for consumer electronics in India has also facilitated the regional market's growth. According to IBEF, demand for electronics hardware in India is expected to reach USD 400 billion by FY2024, which will further drive market growth.

- China is the world's largest producer of electricity. The country's energy demand is expected to increase, thereby resulting in growth in energy production. For instance, according to the IEA, in China, sales of electric vehicles have more than doubled; further, in 2021, it sold approximately 3.3 million more electric cars than in other countries.

- The automotive industry has been increasing in China, and the country is playing an increasingly important role in the global automotive market. The Government of China sees its automotive industry, including the auto parts sector, as one of its pillar industries. The government expects China's automobile output to reach 30 million units by 2020 and 35 million units by 2025.

- Further, the electric vehicle market is gaining momentum in India, owing to the government's ambitious plans and initiatives. Public authorities in India have made several electric vehicle-related policy announcements over the past few years, showing strong commitment, concrete action, and significant ambition to deploy electric vehicles in the country.

Silicon Carbide Power Semiconductor Industry Overview

The silicon carbide power semiconductor market is highly competitive. It consists of several significant players, including Infineon Technologies AG, Texas Instruments Inc., ST Microelectronics NV, Hitachi Power Semiconductor Device Ltd, NXP Semiconductor, Fuji Electric Co. Ltd, Semikron International GmbH, Cree Inc., ON Semiconductor Corporation, Mitsubishi Electric Corporation, and others. These companies are introducing new products, partnerships, and acquisitions, to increase their market share.

- June 2021 - Hitachi, a Japanese electronics company, announced plans to extend its existing presence in Hillsboro by building a big semiconductor research lab to cooperate with manufacturing clients in the United States to create new technologies.

- April 2021 - Infineon Technologies AG launched a new EasyPACK 2B module to its 1200 V product line. The module offers a three-level Active NPC (ANPC) topology, including CoolSiC MOSFETs, TRENCHSTOP IGBT7 devices, NTC temperature sensor, and PressFIT contact technology pins.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in the Demand for Consumer Electronics and Wireless Communications

- 5.1.2 Growing Demand for Energy-Efficient Battery-Powered Portable Devices

- 5.2 Market Challenges

- 5.2.1 Shortage of Silicon Wafers and Variable Driving Requirements

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Automotive (xEVs and EV Charging Infrastructure)

- 6.1.2 IT and Telecommunication

- 6.1.3 Power (Power Supply, UPS, PV, Wind etc.)

- 6.1.4 Industrial (Motor drives)

- 6.1.5 Other End-user Industries (Rail, Oil & Gas, Military, Medical, R&D etc.)

- 6.2 By Geography

- 6.2.1 Americas

- 6.2.2 Europe, Middle East and Africa

- 6.2.3 Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon technologies AG

- 7.1.2 UnitedSiC

- 7.1.3 ST Microelectronics NV

- 7.1.4 ON Semiconductor Corporation

- 7.1.5 GeneSiC Semiconductor Inc.

- 7.1.6 Danfoss A/S

- 7.1.7 Microsemi Corporation

- 7.1.8 Toshiba Corporation

- 7.1.9 Mitsubishi Electric Corporation

- 7.1.10 Fuji Electric Co. Ltd

- 7.1.11 Semikron International

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

碳化硅 (SiC) 电晶体市场分析及预测(至 2035 年):按类型、产品、技术、应用、材料类型、装置、最终用户、功能、安装类型和解决方案划分

碳化硅 (SiC) 电晶体市场分析及预测(至 2035 年):按类型、产品、技术、应用、材料类型、装置、最终用户、功能、安装类型和解决方案划分 电动汽车以碳化硅功率装置市场:依元件类型、额定功率、应用、车辆类型和销售管道,全球预测(2026-2032年)碳化硅肖特基二极体市场按额定电压、额定电流、封装类型、技术、终端用户产业和应用划分-全球预测,2026-2032年

电动汽车以碳化硅功率装置市场:依元件类型、额定功率、应用、车辆类型和销售管道,全球预测(2026-2032年)碳化硅肖特基二极体市场按额定电压、额定电流、封装类型、技术、终端用户产业和应用划分-全球预测,2026-2032年 2026-2034年超高压碳化硅功率元件全球市场规模、份额、趋势与成长分析报告

2026-2034年超高压碳化硅功率元件全球市场规模、份额、趋势与成长分析报告 日本碳化硅(SiC)功率元件市场规模、份额、趋势及预测(按类型、电压范围、应用和地区划分,2026-2034年)

日本碳化硅(SiC)功率元件市场规模、份额、趋势及预测(按类型、电压范围、应用和地区划分,2026-2034年) 2026年全球碳化硅功率半导体市场报告GaN 和 SiC 功率元件市场:按材料、电压范围、装置类型和应用划分-2026 年至 2032 年全球预测SiC功率分离式元件元件市场按封装类型、电压等级、装置类型、功率等级和最终用途产业划分 - 全球预测 2026-2032分离式碳化硅功率元件市场(依产品类型、功率等级、封装类型及应用划分)-2026-2032年全球预测功率型碳化硅市场:2026-2032年全球预测(依元件类型、额定电压、应用和销售管道)

2026年全球碳化硅功率半导体市场报告GaN 和 SiC 功率元件市场:按材料、电压范围、装置类型和应用划分-2026 年至 2032 年全球预测SiC功率分离式元件元件市场按封装类型、电压等级、装置类型、功率等级和最终用途产业划分 - 全球预测 2026-2032分离式碳化硅功率元件市场(依产品类型、功率等级、封装类型及应用划分)-2026-2032年全球预测功率型碳化硅市场:2026-2032年全球预测(依元件类型、额定电压、应用和销售管道)