|

市场调查报告书

商品编码

1641958

软体定义储存:市场占有率分析、产业趋势和成长预测(2025-2030 年)Software-Defined Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

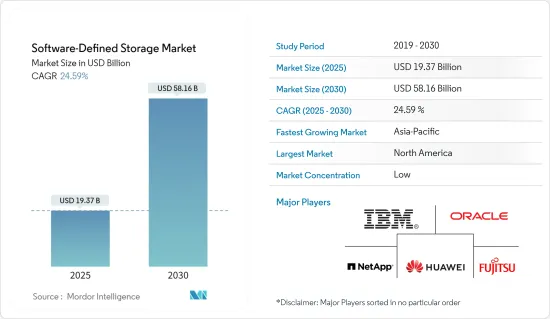

软体定义储存市场规模在2025年预估为193.7亿美元,预计到2030年将达到581.6亿美元,预测期间(2025-2030年)复合年增长率为24.59%。

软体定义储存(SDS)可让企业从硬体平台中抽像出储存资源,提供灵活性、效率和快速的可扩充性。在软体设计资料中心 (SDDC) 架构中,资源不是孤立的,而是可以轻鬆实现自动化和编配。透过资料提高效率和业务流程的需求正在推动中小企业对 SDS 解决方案的需求。

由于竞争环境,公司正在将重点转向新技术以获得竞争优势。使用 SDS 有助于透过自动化製程控制和以软体取代传统硬体来降低成本。

企业中非结构化资料的快速成长推动了对可靠、安全和可扩展的储存架构的需求。此外,随着物联网在全球的普及,边缘产生的资料量正在迅速增加。 SDS 模型透过提供更大的部署灵活性并允许透过单一介面在任何储存平台上使用该软体来满足这些需求。

由于这项技术相对于传统储存方法具有优势,正在经历数位转型的企业和 IT 组织可能会采用 SDS 来满足其资料储存需求。然而,需要熟练的操作员来管理向 SDS 的过渡以及安全问题可能会阻碍市场成长。

市场领先的供应商正在部署增强资料保护和可靠性的 SDS 软体解决方案。

新冠疫情促使私营和公共部门从传统管道转向数位管道,使公民、企业和公共部门工作人员能够从远端位置安全地存取公共服务并共用资料。事实证明,软体定义储存在疫情期间对企业至关重要,预计疫情过后资料储存将继续成长。

软体定义储存市场趋势

BFSI 领域预计将大幅成长

- 银行是受到严格监管的业务,资料呈指数级增长,需要高度安全和可用的储存功能,以便透过跨地点工作的设备进行扩展和扩展。软体定义储存解决方案可以透过处理庞大的资料集、透过加密限製檔案访问,甚至备份和復原资料来帮助改善 BFSI业务。

- BFSI 领域竞争激烈,利用科技确保IT基础设施灵活并能回应市场的动态需求。软体定义的资料中心将使银行能够推出聚合应用程序,整合零售客户经常使用的应用程式。只需使用应用程式即可轻鬆满足杂货、旅行、电子商务和整合付款选项等各种使用案例,这些优势有助于客户开展日常银行业务。

- 对 BFSI 中海量资料进行更好管理的需求日益增长,推动了软体定义储存市场的大部分份额。预计在预测期内,BFSI 部门将实现最快的成长。这是因为客户对资料分析的需求不断增加,以获得竞争优势并推动该领域持续的数位转型。

- 随着数位经济的扩张,资料已成为银行业的重要组成部分。软体定义的基础架构和储存解决方案使全球银行能够快速存取、分析和共用云端本地资料,涵盖从前台到后勤部门的业务。

亚太地区预计将经历最快成长

- 在亚太地区,整个地区的企业都经历着本地设备和云端环境中储存的非结构化资料量激增。此外,全部区域物联网 (IoT) 的普及正在推动边缘产生的资料呈指数级增长。

- 线上付款的采用呈指数级增长,每天都会产生企业需要处理的大量资料,从而推动对软体定义储存解决方案的需求。

- 此外,透过华为在中国提供SDS的FalconStor等领先供应商认为,包括中国在内的亚太地区的客户/企业是IT服务最大的潜在市场之一,并且正在向现代储存解决方案转型。对此持正面态度。迁移趋势主要受到资料安全、復原以及虚拟和非虚拟资源整合等挑战的驱动。

- 随着该国网路用户数量的不断增长,云端储存的使用量预计将大幅增长。

- 中国和印度等新兴经济体仍依赖传统硬体进行存储,迫切需要数位转型以跟上技术进步。预计这些国家将在预测期内为软体定义储存 (SDS) 供应商提供潜在机会。

软体定义储存行业概览

软体定义储存市场较为分散,主要参与者包括 IBM 公司、Oracle 公司和 NetApp 公司。市场主要企业不断创新产品、增加活性化、产能扩张等倡议,进一步加剧竞争。

2023 年 11 月多重云端资料管理解决方案供应商 DDN 宣布推出其下一代软体定义储存平台 DDN Infinia。该平台利用资料编配和基于人工智慧的优化来加速运算和生成人工智慧。 DDN Infinia 结合了多租户、容器化和最高水准的速度和效率,以及易于管理和强大的安全属性。此解决方案简化了资料管理所需的工作流程。

2023年9月 加拿大投资银行TD Securities专注于外汇兑换和大额交易等批发银行业务,但其区块储存由多个储存口袋组成,维护困难。在道明证券,储存由通用基础设施专家管理。因此,道明证券决定部署软体定义储存系统 Dell PowerMax。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 评估宏观经济对市场的影响

第五章 市场动态

- 市场驱动因素

- 整个企业的资料量快速成长

- 远端系统管理流程工业对工业移动性的需求不断增加

- 市场挑战

- 高成本、安装复杂

第六章 市场细分

- 按类型

- 堵塞

- 文件

- 目的

- 融合式基础架构

- 按公司规模

- 中小企业

- 大型企业

- 按最终用户产业

- BFSI

- 通讯和 IT

- 政府

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- IBM Corporation

- Oracle Corporation

- Netapp Inc.

- Huawei Technologies Co. Ltd

- Fujitsu Limited

- Genetec Inc.

- VMWare Inc.(Dell Inc.)

- Hitachi Vantara Corp.

- Pure Storage Inc.

- Promise Technology Inc.

- FalconStor Software Inc.

- StarWind Software Inc.

第八章投资分析

第九章:市场的未来

The Software-Defined Storage Market size is estimated at USD 19.37 billion in 2025, and is expected to reach USD 58.16 billion by 2030, at a CAGR of 24.59% during the forecast period (2025-2030).

The software-defined storage (SDS) enables organizations to abstract storage resources from the hardware platform, offering flexibility, efficiency, and faster scalability. In the software-designed data center (SDDC) architecture, resources can be easily automated and orchestrated rather than residing in siloes. The need to improve efficiency and business processing with data drives the demand for SDS solutions in small and medium-sized enterprises.

Due to the competitive environment, companies have shifted their focus toward new technology to have a competitive edge. SDS usage helps minimize the cost by automating process controls and replacing traditional hardware with software.

The booming volume of unstructured data across various enterprises augments the demand for a scalable storage architecture that is reliable and secure. In addition, with the proliferation of IoT globally, the data generated at the edge is rapidly increasing. The SDS model addresses these needs by increasing deployment flexibility and enabling organizations to use the software with any storage platform through a single interface.

Due to this technology's advantages over traditional storage methods, enterprises or IT organizations undergoing digital transformation will likely adopt SDS for their data storage needs. However, the need for more skilled operators to manage the transition toward SDS and security concerns will hinder the market's growth.

The key vendors in the market have been rolling out SDS software solutions with enhanced data protection and reliability, owing to the growing requirements of large companies in the banking and telecom sectors.

The COVID-19 pandemic resulted in private and public sectors shifting from traditional channels to digital channels to enable citizens, businesses, and public sector staff to access public services and securely share data from remote locations. Software-defined storage has proven its importance for businesses during the pandemic and is anticipated to see continued growth in data storage post-pandemic.

Software-Defined Storage Market Trends

The BFSI Segment is Expected to Witness Significant Growth

- The banks are a highly regulated operational environment with exponential data growth and require highly secure and highly available storage capabilities to integrate, scale up, and out with appliances that link together across sites. The software-defined storage solutions help improve BFSI operations, including handling massive data sets, limited access to files with encryption, and even data backup and recovery.

- The BFSI segment is highly competitive, leveraging technology to ensure its IT infrastructure is highly flexible to meet dynamic market demands. Software-defined data centers enable banks to launch an aggregator app, consolidating the frequently used apps by retail customers. Benefits such as ease of operation from a single app for different use cases like food, travel, and e-commerce and integration of payment options are helping customers in everyday banking activities.

- The rising need for better managing vast data from BFSI contributes a substantial share of the software-defined storage market. The BFSI segment is anticipated to record the fastest growth during the forecast period, attributed to the increasing demand for customer data analysis to achieve a competitive advantage and boost the ongoing digital transformation in the segment.

- With the increase in the digital economy, data is an essential part of the banking industry. Software-defined infrastructure and storage solutions enable global banks to rapidly access, analyze, and share on-premises data in the cloud from front-to-back office operations.

Asia-Pacific is Expected to Witness Fastest Growth

- Asia-Pacific is experiencing rapid growth in the volume of unstructured data across various enterprises, which is being stored in on-premises devices and cloud environments. Also, with the proliferation of the internet of things (IoT) across the region, the data generated at the edge is drastically increasing.

- The adoption of online payments is rising exponentially, generating a huge amount of data daily, which the companies need to process, propelling the demand for software-defined storage solutions.

- Moreover, the key vendors, such as FalconStor, which provides SDS in China through Huawei, indicated that customers/enterprises in Asia-Pacific, including China, are one of the greatest potential markets for IT services and are positive about switching to modern storage solutions. The propensity to shift is mainly to overcome challenges such as data security, recovery, and the integration of virtual and non-virtualized resources.

- The use of cloud storage is poised to increase aggressively, driven by the country's rising number of internet users.

- Emerging economies like China and India are still dependent on traditional hardware for storage and the need for digital transformation to stay up with technological advancements; these countries are expected to provide a potential commercial opportunity for software-defined storage (SDS) suppliers during the forecast period.

Software-Defined Storage Industry Overview

The software-defined storage market is fragmented, with major players like IBM Corporation, Oracle Corporation, and NetApp Inc. The key players in the market are continuously innovating new products and rising activities such as mergers and acquisitions and capacity expansion, further increasing the competition.

November 2023: DDN, a provider of multi-cloud data management solutions, has announced DDN Infinia, a next-generation software-defined storage platform. This platform leverages data orchestration and AI-based optimization to accelerate computing and generative AI. DDN Infinia combines multi-tenancy, containerization, and the highest levels of speed and efficiency with ease of management and powerful security attributes. The solution simplifies workflows for the data management demands.

September 2023: TD Securities, a Canadian investment bank that focuses on wholesale banking such as currency conversion and large trades, introduced its TD Securities' block storage setup made up of several storage pockets, making it hard to maintain. General infrastructure specialists managed storage at TD Securities. TD Securities has thus selected to move forward with a software-defined storage system, Dell PowerMax.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macroeconomic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapidly Growing Volume of Data Across Enterprises

- 5.1.2 Increased Demand for Industrial Mobility for Remotely Managing the Process Industry

- 5.2 Market Challenges

- 5.2.1 High Cost and Compliacted in Installation

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Block

- 6.1.2 File

- 6.1.3 Object

- 6.1.4 Hyper-converged Infrastructure

- 6.2 By Size of Enterprise

- 6.2.1 Small and Medium Enterprise

- 6.2.2 Large Enterprise

- 6.3 By End-user Industries

- 6.3.1 BFSI

- 6.3.2 Telecom and IT

- 6.3.3 Government

- 6.3.4 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Oracle Corporation

- 7.1.3 Netapp Inc.

- 7.1.4 Huawei Technologies Co. Ltd

- 7.1.5 Fujitsu Limited

- 7.1.6 Genetec Inc.

- 7.1.7 VMWare Inc. (Dell Inc.)

- 7.1.8 Hitachi Vantara Corp.

- 7.1.9 Pure Storage Inc.

- 7.1.10 Promise Technology Inc.

- 7.1.11 FalconStor Software Inc.

- 7.1.12 StarWind Software Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球软体定义储存市场报告

2026年全球软体定义储存市场报告 软体定义储存 (SDS) 市场规模、份额和成长分析(按组件、组织规模、部署类型、应用、最终用途和地区划分)—2026-2033 年行业预测

软体定义储存 (SDS) 市场规模、份额和成长分析(按组件、组织规模、部署类型、应用、最终用途和地区划分)—2026-2033 年行业预测 美国的软体定义製造业(SDM)市场:各解决方案,各部署模式,各用途,各终端用户产业,各地区,机会,预测,2018年~2032年

美国的软体定义製造业(SDM)市场:各解决方案,各部署模式,各用途,各终端用户产业,各地区,机会,预测,2018年~2032年 全球软体定义储存(SDS)市场

全球软体定义储存(SDS)市场 软体定义储存 (SDS) 市场:全球 2025-2029

软体定义储存 (SDS) 市场:全球 2025-2029 软体定义储存市场规模、份额、趋势分析报告:2024 年至 2031 年按组件、部署、组织规模、最终用途、应用和地区分類的展望和预测

软体定义储存市场规模、份额、趋势分析报告:2024 年至 2031 年按组件、部署、组织规模、最终用途、应用和地区分類的展望和预测 软体定义储存市场 - 按类型、企业规模、最终用户产业、地区和竞争细分的全球产业规模、份额、趋势、机会和预测。 2019-2029F

软体定义储存市场 - 按类型、企业规模、最终用户产业、地区和竞争细分的全球产业规模、份额、趋势、机会和预测。 2019-2029F