|

市场调查报告书

商品编码

1641982

资料角力:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Data Wrangling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

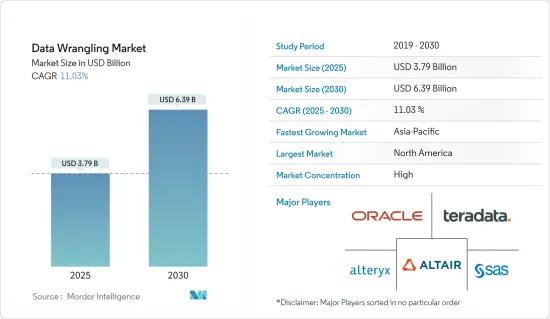

资料角力市场规模预计在 2025 年为 37.9 亿美元,预计到 2030 年将达到 63.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 11.03%。

各种自动化技术的出现已经增强和改进了资料缩减程序。预计在预测期内,该行业将提出更复杂的人工智慧解决方案来协助资料细化和资料分析过程。

主要亮点

- 随着许多行业收集的资料量和可靠性的快速发展,人们开始采用先进的分析演算法来选择可能彻底改变营业单位的见解。巨量资料使用量的快速成长也产生了大量非结构化资料。迭代和互动式资料分析应用程式可以识别分布和不一致性并提案流程改进建议。

- 资料操作可以透过提高资讯的一致性来提供对元资料的统计洞察。元资料的更高一致性使得自动化技术能够更快、更准确地查询资料,从而经常导致这样的发现。资料缩减主要是为了根据预期的市场表现开发模型,清理讯息,以便模型能够正常运作。

- 企业越来越多地使用资料角力来即时预测和监控可能影响业务绩效的大量事件。资料角力市场正在成长,因为它有潜力透过针对网路攻击和其他紧急情况等意外事件做出复杂的决策来降低风险。此外,随着网路攻击的增加,资料变得越来越容易找到和恢復,对资料角力的需求也在增加。

- 人们对资讯遗失或被盗的担忧日益增加、BYOD(自带设备)趋势日益增长以及业务敏捷性只是推动资料角力市场成长的几个因素。预计资料角力行业将从边缘运算的进步中受益匪浅。

- 然而,资料品质问题限制了市场扩张。资料角力产业预计将面临挑战,因为它尚未准备好从传统的 ETL 工具转向尖端的自动化技术。此外,扩大这一市场的主要障碍之一是中小企业缺乏有关资料角力工具的了解。

- 新冠疫情爆发带来大量资料涌入。科技公司和资料聚合商利用来自手机讯号塔和行动应用程式的本地资料来实施社会隔离,并透过仪表板解决联络人监控和追踪方面的差异。该应用程式使用蓝牙、建模工作和定位服务来预测医院需求和传染病负担。预计,由于该程式产生的资料有缺陷,数百万人将受到不利影响。资料角力用于清理、正确格式化和丰富原始资料,以帮助使用者做出更快、更准确的决策。因此,COVID-19 的资料角力要求为市场扩张提供了潜力。

资料角力市场趋势

分析:大公司占有较大的市场占有率

- 大型企业预计将在资料角力市场占据主要市场占有率,这主要是由于人工智慧和机器学习的应用增加,以及先进技术的大量采用导致资料量增加。此外,大型企业日益增加的监管压力预计将为未来几年的市场扩张提供巨大的成长机会。

- 此外,资料管理解决方案能够透过快速分析和采取行动来实现更好、更快的决策并提供竞争优势,这进一步推动了大型企业的需求。此外,大型企业正在采用资料角力来即时监控和预测可能影响大型组织绩效的各种事件。

- 此外,据 IBM 称,不同公司、国家和产业的人工智慧采用情况存在差异。大型企业在营运中积极使用人工智慧的可能性是其他企业的两倍,而中小企业的可能性较小。企业更有可能探索人工智慧,而不是积极追求人工智慧。截至英国,中国和印度超过一半的 IT 工作者预计他们的组织美国我认为他们正在积极采用人工智慧。

- 而且随着巨量资料的发展,大公司也不断发现新的资料类型。然而,随着科技创造越来越多的资料来源,资料管理对企业来说继续成为更大的挑战。这些公司认识到资料管理在大型企业中的重要性,从而推动了市场成长。

预计北美将占很大份额

- 预计北美将在预测期内主导资料角力市场,因为它是对资料角力工具和服务采用贡献最大的地区之一。此外,预计主要供应商的存在和终端用户行业的日益采用将在预测期内推动该地区的市场成长。

- 随着工业 4.0 服务的出现以及巨量资料的应用,该地区预计将经历显着的成长。此外,巨量资料在美国是一个巨大的现象,各行各业的公司都透过收集、分析和处理来自多个来源的大量资料来获利。

- 持有大量股份的公司主要位于北美,并透过在该地区进行大量投资和发展,大力推动市场发展。 Trifacta、Altair Engineering, Inc、TIBCO Software Inc、Oracle Corporation 和 SAS Institute Inc 等公司都位于美国,并活跃于该地区的资料管理业务。

- 该地区日益兴起的技术趋势,例如各种技术的投资、采用和集成,可能会为资料角力技术创造巨大的商机,以帮助企业高效地处理大量资料。此外,疫情过后云端运算采用趋势的上升正在推动该地区市场的成长。

资料角力产业概览

资料角力市场因 Alteryx, Inc.、Oracle Corporation 和 Teradata Corporation 等几家主要参与者的存在而变得更加巩固。有几家主要企业,包括 Alteryx、Oracle 和 Teradata,他们正在透过不断的技术创新来获得竞争优势。透过研发、策略伙伴关係和併购,这些参与者在市场上占据了更大的份额。

2023 年 3 月,Simplebim 发布了其 BIM资料管理软体的第 10 版,供建设公司、BIM 经理、建筑师、结构和设计工程师使用。据该公司称,其最新版本开闢了使用 IFC 文件中资料的新方法,以增强生产计画和调度、采购、竞标、成本估算、监控、安装操作以及 BIM资料的其他下游用途。可能会让你这样做。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 资料量不断增加

- 人工智慧和巨量资料技术的进步

- 对资料可靠性的担忧日益增加

- 市场限制

- 公司缺乏对资料管理工具的认识

- 显式资料存取权限

第六章 市场细分

- 按组件

- 工具

- 服务

- 按部署

- 云端基础

- 本地

- 按公司类型

- 小型至中型

- 大规模

- 按最终用户产业

- 资讯科技/通讯

- 零售

- 政府

- BFSI

- 卫生保健

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 新加坡

- 其他亚太地区

- 拉丁美洲

- 墨西哥

- 巴西

- 其他拉丁美洲国家

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东和非洲地区

- 北美洲

第七章 竞争格局

- 公司简介

- Alteryx, Inc.

- TIBCO Software Inc.(Cloud Software Group, Inc.)

- Altair Engineering Inc.

- Teradata Corporation

- Oracle Corporation

- SAS Institute Inc.

- Datameer, Inc.

- DataRobot, Inc.

- Cloudera, Inc.

- Cambridge Semantics, Inc.

第八章投资分析

第九章 市场机会与未来趋势

The Data Wrangling Market size is estimated at USD 3.79 billion in 2025, and is expected to reach USD 6.39 billion by 2030, at a CAGR of 11.03% during the forecast period (2025-2030).

The creation of various automated technologies has already enhanced and improved the data-wrangling procedure. The industry would create more complex AI solutions during the forecast period to assist the processes of data wrangling and data analysis.

Key Highlights

- The adoption of sophisticated analytics algorithms to choose insights that might revolutionize a business entity results from the rapid development in the quantity and reliability of data collected throughout many industrial verticals. Massive amounts of unstructured data have also been produced due to the surge in Big Data usage. Applications for iterative and interactive data wrangling may identify distributions and inconsistencies and suggest process improvement.

- Data manipulation can offer statistical insights into the metadata by making the information more consistent. Increased metadata consistency makes it possible for automated technologies to examine the data more quickly and precisely, frequently leading to these findings. Data wrangling would clean the information to enable a model to operate without problems, mainly in developing a model about expected market performance.

- Businesses are increasingly using data wrangling for real-time forecasting and monitoring of numerous events that may impact their performance. The market for data wrangling is expanding due to the potential to mitigate risks by executing complicated judgments concerning unplanned occurrences, such as cyberattacks and other emergencies. Also, as more cyberattacks occur, there is a growing demand for data wrangling since it makes data simpler to find and recover.

- Growing concerns about information loss and theft, expanding Bring Your Own Device (BYOD) trends, and business mobility are just a few factors that are significantly accelerating the growth of the data wrangling market.The industry of data wrangling is predicted to benefit significantly from advances in edge computing.

- However, issues with data quality are limiting the market's ability to expand.The data-wrangling industry is anticipated to face challenges due to a lack of readiness to switch from conventional ETL tools to cutting-edge automated technologies. Further, one of the key obstacles to this market's expansion is the lack of knowledge about data-wrangling tools among small and medium-sized businesses.

- The COVID-19 epidemic brought on a considerable data influx. Technological firms and data aggregators exploited local data from cell towers and mobile applications to impose social segregation and close the gaps using dashboards that monitored and tracked contacts. Applications predicted hospital requirements and epidemic burden using Bluetooth, modeling efforts, and geolocation services. As a result of the flawed data produced throughout this procedure, millions of people were expected to be negatively impacted. Data wrangling is used to clean, arrange, and enhance raw data into the appropriate format for users to make better decisions more quickly and accurately. As a result, COVID-19's requirement for data wrangling provided market potential for expansion.

Data Wrangling Market Trends

Large Enterprises are Analyzed to Hold Significant Market Share

- Large enterprises are expected to hold significant market share in the data wrangling market primarly due to increasing adoption of AI and ML, growing volume of data owing to the substantial adoption of advanced technologies. Furthermore, increasing regulatory pressure among the large enterprises is expected to present major growth opportunities for the expansion of the market in future.

- Additionally, the ability of data-wrangling solutions to deliver better and faster decision-making and to offer a competitive advantage by analyzing and acting upon information promptly further boosts the demand among large enterprises. Furthermore, large enterprises are adopting data wrangling for real-time monitoring and forecasting of various occasions that may affect the performance of large organizations.

- Moreover, according to IBM, the adoption of AI varies amongst businesses, countries, and sectors. While larger firms are twice as likely to have actively used AI as part of their company operations, smaller businesses are less likely. Companies are more likely to investigate AI than actively pursue it. As of 2022, a majority of IT workers in China and India, compared to markets like South Korea (22%), Australia (24%), the United States (25%), and the United Kingdom (26%), believe their organization is already actively employing AI.

- Further, large businesses are constantly discovering new data kinds as big data continues to progress. Data management, however, keeps becoming a more significant challenge for firms as technology produces more and more data sources. Such companies significantly recognize the importance of data wrangling in the large businesses, thereby driving market growth.

North America is Expected to Hold the Significant Share

- North America is expected to dominate data wrangling during the forecast period, as the region remains one of the most significant contributors to the adoption of data wrangling tools and services. Further, the presence of major market vendors coupled witg growing adoption among end-user industries is analyzed to boost the market growth in the region over the forecast period.

- The region is expected to witness massive growth along with the application of big data due to the emergence of Industry 4.0 services. Moreover, big data is an enormous phenomenon in the United States, and companies from various industries benefit from collecting, analyzing, and manipulating vast amounts of data from multiple sources.

- The significant shareholding firms are considerably based in the North America region, which significantly drives the market with considerable investments and developments in the region. Companies such as Trifacta, Altair Engineering, Inc., TIBCO Software Inc., Oracle Corporation, SAS Institute Inc., etc., are based in the United States and are actively engaged in the operation of data wrangling in the region.

- The rising technological trends in terms of investments, adoption, and integration of various technologies in the region would significantly create opportunities for data wrangling technology in assisting firms to work effectively in handling huge amounts of data. Further, the increased trends of cloud adoption in the region post-pandemic boosted market growth in the region.

Data Wrangling Industry Overview

The data wrangling market is consolidated owing to the presence of a few key players, such as Alteryx, Inc., Oracle Corporation, and Teradata Corporation, amongst others. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over others. Through research and development, strategic partnerships, and mergers and acquisitions, these players have gained a stronger footprint in the market.

In March 2023, Simplebim released version 10 of its BIM data wrangling software used by construction firms, BIM managers, architects, and structural and design engineers. According to the company, the latest release by the company opens up new ways to use data in IFC files to enable enhanced production planning and scheduling, procurement, tendering, cost estimation, monitoring, installation work, and other downstream BIM data usage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Volumes of Data

- 5.1.2 Advancement in AI And Big Data Technologies

- 5.1.3 Growing Concern about Data Veracity

- 5.2 Market Restraints

- 5.2.1 Lack Of Awareness Of Data Wrangling Tools Among Enterprises

- 5.2.2 Explicit Data Access Permission

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Tools

- 6.1.2 Service

- 6.2 By Deployment

- 6.2.1 Cloud-Based

- 6.2.2 On-premises

- 6.3 By Enterprise Type

- 6.3.1 Small and Medium Sized

- 6.3.2 Large

- 6.4 By End-user Industry

- 6.4.1 IT and Telecommunication

- 6.4.2 Retail

- 6.4.3 Government

- 6.4.4 BFSI

- 6.4.5 Healthcare

- 6.4.6 Other End-user Industries

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 Singapore

- 6.5.3.4 Rest of Asia-Pacific

- 6.5.4 Latin America

- 6.5.4.1 Mexico

- 6.5.4.2 Brazil

- 6.5.4.3 Rest of Latin America

- 6.5.5 Middle East and Africa

- 6.5.5.1 United Arab Emirates

- 6.5.5.2 Saudi Arabia

- 6.5.5.3 Rest of Middle-East & Africa

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Alteryx, Inc.

- 7.1.2 TIBCO Software Inc. (Cloud Software Group, Inc.)

- 7.1.3 Altair Engineering Inc.

- 7.1.4 Teradata Corporation

- 7.1.5 Oracle Corporation

- 7.1.6 SAS Institute Inc.

- 7.1.7 Datameer, Inc.

- 7.1.8 DataRobot, Inc.

- 7.1.9 Cloudera, Inc.

- 7.1.10 Cambridge Semantics, Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年资料整理市场规模、份额、趋势及预测(按组件、部署模式、组织规模、业务功能、产业垂直领域及地区划分)

2025 年至 2033 年资料整理市场规模、份额、趋势及预测(按组件、部署模式、组织规模、业务功能、产业垂直领域及地区划分) 资料角力市场规模、份额和趋势分析报告:按组件、部署、公司规模、最终用户、地区和细分市场进行预测,2025 年至 2033 年

资料角力市场规模、份额和趋势分析报告:按组件、部署、公司规模、最终用户、地区和细分市场进行预测,2025 年至 2033 年 全球资料整理市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球资料整理市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 资料角力市场规模、份额及成长分析(按组件、部署模型、垂直产业、组织规模、业务功能和地区)-2025 年至 2032 年产业预测

资料角力市场规模、份额及成长分析(按组件、部署模型、垂直产业、组织规模、业务功能和地区)-2025 年至 2032 年产业预测 2025年资料整理全球市场报告

2025年资料整理全球市场报告 全球资料角力市场规模、份额、趋势分析报告:按部署模式、组件、业务功能、组织规模、垂直和地区分類的展望和预测,2024 年至 2031 年全球资料整理市场规模:按业务功能、按组件、按部署模型、按组织规模、按最终用户、按地区、范围和预测

全球资料角力市场规模、份额、趋势分析报告:按部署模式、组件、业务功能、组织规模、垂直和地区分類的展望和预测,2024 年至 2031 年全球资料整理市场规模:按业务功能、按组件、按部署模型、按组织规模、按最终用户、按地区、范围和预测 全球资料整理市场:按元件、业务功能、部署类型、组织规模和最终用户 - 预测 2025-2030

全球资料整理市场:按元件、业务功能、部署类型、组织规模和最终用户 - 预测 2025-2030 全球资料角力市场,2024-2028

全球资料角力市场,2024-2028