|

市场调查报告书

商品编码

1641999

虚拟软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Virtualization Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

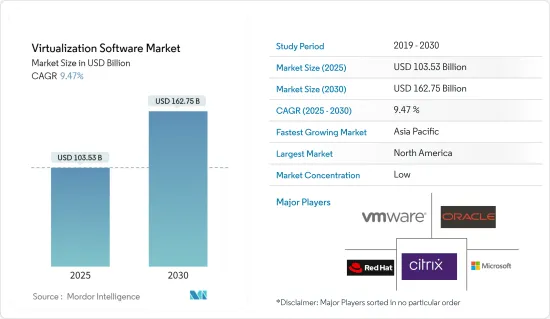

虚拟软体市场规模预计在 2025 年为 1,035.3 亿美元,预计到 2030 年将达到 1,627.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 9.47%。

虚拟软体市场是现代IT基础设施的重要组成部分,使企业能够优化资源利用率、简化管理流程并降低营运成本。虚拟软体抽象硬体系统,允许多个虚拟环境在一台实体机上运作。这种硬体和软体的分离使得创建模拟实体电脑的虚拟机器 (VM) 变得更加容易,从而提高了伺服器虚拟、云端处理和灾难復原等应用程式的灵活性。随着越来越多的企业采用资料中心虚拟和云端基础的服务来满足不断增长的运算需求,虚拟软体市场持续扩大。

主要亮点

- 透过虚拟提高效率:虚拟技术可显着提高效率,使 IT 部门能够根据需要快速部署资源和扩展基础架构。其他好处包括集中管理和增强的虚拟安全性。开放原始码虚拟软体提供了经济高效的解决方案,而专有平台则提供了全面的功能和专门的支援。然而,成功的虚拟部署通常需要设定和配置的专业知识,特别是在复杂的环境中。

- 主要产业参与者 VMware、Microsoft、Citrix Systems 和 Oracle 等大型公司正在引领该领域的创新。这些公司专注于开发支援伺服器虚拟、网路虚拟、虚拟桌面和云端原生虚拟的虚拟平台。为了保持竞争力,这些市场领导正在投资增强其虚拟机器管理程式技术、提高自动化程度并整合强大的安全功能。

透过虚拟优化IT基础设施

主要亮点

- 降低成本:虚拟透过最大限度地减少附加硬体来帮助降低营运成本。伺服器虚拟在单一伺服器上运行多个虚拟机,优化硬体利用率并降低购买和维护实体伺服器的相关成本。

- 节省硬体:传统 IT 环境需要为每个作业系统配备单独的实体伺服器,导致硬体使用率不足。透过虚拟这些系统,公司可以实现更高的伺服器利用率并减少所需的实体机总数。这减少了硬体的资本支出并降低了能源消费量。

- 扩充性:虚拟软体使IT基础设施能够快速扩展。企业可以快速建立、复製和迁移虚拟机,并尽量减少停机时间,以满足云端环境和高效能运算场景中不断变化的需求。

- 能源效率:整合实体伺服器可减少电力和冷却所需的能量,进而提高资料中心的能源效率。这不仅降低了营运成本,而且还透过减少组织的碳排放支持了公司的永续性努力。

利用虚拟简化 IT 运营

虚拟技术可让团队集中管理虚拟环境,从而大大简化了 IT 管理。单一平台可快速部署虚拟机器并解决问题,进而提高营运效率。

主要亮点

- 集中管理:虚拟平台提供的集中管理简化了虚拟机器的管理。 IT 管理员可以从单一介面部署、更新和管理多个虚拟环境,从而降低复杂性并最大限度地缩短维护时间。

- 灾难復原:虚拟解决方案增强您的灾难復原策略。虚拟机器可以轻鬆备份和恢復,大幅减少系统故障时的恢復时间。此外,许多虚拟平台都内建了灾难復原工具,减少了对第三方解决方案的依赖。

- 增强的安全性:虚拟允许隔离虚拟机,从而降低安全漏洞的风险。基于角色的存取控制、加密和安全迁移等虚拟安全功能可协助企业保护敏感资料并限制潜在攻击的影响。

虚拟软体市场趋势

PC/虚拟桌面预计将占据很大份额

- 由于对可扩展、高效 IT 解决方案的需求不断增加,虚拟软体市场正在迅速扩张。虚拟技术可以创建硬体和储存设备的虚拟版本,从而提高资源利用率并降低成本。云端处理、资料中心虚拟和虚拟机器管理程式技术的进步是该市场的主要驱动力。有几种值得注意的趋势正在塑造虚拟软体的未来。

- 远端工作推动 VDI 的采用:向远端工作的转变正在推动虚拟桌面基础架构 (VDI) 的采用。 VDI 让企业可以从中央伺服器安全地部署桌面环境。这有助于降低硬体成本,同时无论员工身在何处都能提供无缝的效能。

- 应用程式虚拟的成长:随着企业寻求最大限度地减少相容性问题并保护遗留系统,应用程式虚拟越来越受欢迎。该技术允许应用程式独立于底层作业系统运行,从而降低风险并提高相容性。

- 开放原始码软体的兴起:KVM、Xen等高性价比的开放原始码虚拟平台越来越受欢迎,尤其是在中小型企业。这些平台提供强大的虚拟机器管理工具,让您无需承担昂贵的授权费用即可优化系统。

- 安全是关键:随着云端虚拟和混合 IT 的兴起,保护虚拟环境已成为当务之急。保护虚拟机器和虚拟机器管理程式层的需求推动了对先进安全解决方案的需求,使得 PC/虚拟桌面占据市场主导地位。

亚太地区预计将创下最大市场规模

- 由于工业化的快速发展、 IT基础设施投资的不断增长以及云端运算的日益普及,亚太地区预计将在虚拟软体市场中占据主导地位。中国、印度和日本等国家处于数位转型的前沿,尤其是在通讯和BFSI(银行、金融服务和保险)等行业。

- 云端虚拟的成长:该地区的企业正在迅速采用云端虚拟来提高资源效率并降低 IT 成本。随着企业从传统硬体转向虚拟环境,对云端服务的需求正在推动市场强劲扩张。

- 适合中小型企业的开放原始码解决方案:中小型企业由于其成本效益和灵活性而越来越多地采用开放原始码虚拟软体。这一趋势是由印度等国家的政府推动数位化基础设施的倡议所推动的,从而导致对经济实惠且可扩展的虚拟解决方案的需求增加。

- 容器化趋势:该地区也正在见证容器化技术的兴起。容器化技术为云端原生应用提供了比传统虚拟更高的效率。这种转变支持了结合虚拟和容器化优势的混合和多重云端环境的成长。

虚拟软体产业概况

虚拟软体市场高度分散,大公司和小众市场参与者争夺市场占有率。 VMware、Microsoft、Oracle、Citrix等公司在伺服器虚拟、网路虚拟、虚拟桌面等各个领域提供全面的虚拟解决方案,并占据全球市场主导地位。

主要产业领导者 VMware 凭藉广泛的资料中心虚拟解决方案引领市场。微软的Hyper-V平台利用该公司在云端服务方面的强势地位,而Oracle和Citrix则致力于提供高度整合的虚拟解决方案。

新兴趋势协助未来成长:随着云端原生虚拟和容器化等趋势的普及,市场正朝向更灵活、更可扩展的解决方案转变。为了保持竞争力,企业必须投资于云端整合、增强安全性以及对多重云端环境的支援。边缘运算等新兴技术也将在塑造这个充满活力的产业的未来方面发挥关键作用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 产业影响评估

第五章 市场动态

- 市场驱动因素

- 透过减少硬体支出来节省成本

- 透过虚拟提高 IT 效率

- 市场挑战

- 建构虚拟环境的复杂性

第六章 市场细分

- 按平台

- PC虚拟

- 移动虚拟

- 按类型

- 应用程式虚拟

- 网路虚拟

- 硬体虚拟

- 其他类型

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- VMware Inc

- Citrix Systems Inc.

- Oracle Corporation

- Microsoft Corporation

- Red Hat Inc.(IBM Corporation)

- Amazon Inc.

- Google LLC.

- NComupting Co. Ltd.

- Parallels International GmbH

- Huawei Technologies Co. Ltd.

- Datadog, Inc.

- Nutanix Inc.

- TenAsys Corporation

- Lynx Software Technologies

第八章投资分析

第九章 市场机会与未来趋势

The Virtualization Software Market size is estimated at USD 103.53 billion in 2025, and is expected to reach USD 162.75 billion by 2030, at a CAGR of 9.47% during the forecast period (2025-2030).

The virtualization software market is a pivotal component of modern IT infrastructure, enabling businesses to optimize resource utilization, streamline management processes, and reduce operational costs. Virtualization software abstracts hardware systems, allowing multiple virtual environments to operate on a single physical machine. This decoupling of hardware from software facilitates the creation of virtual machines (VMs), which emulate physical computers, enhancing flexibility for applications such as server virtualization, cloud computing, and disaster recovery. As organizations increasingly adopt data center virtualization and cloud-based services to meet rising computational demands, the virtualization software market continues to expand.

Key Highlights

- Efficiency through Virtualization: Virtualization technologies offer significant efficiency improvements, enabling IT departments to deploy resources quickly and scale infrastructure as needed. Businesses benefit from centralized management and enhanced virtualization security. Open-source virtualization software provides cost-effective solutions, while proprietary platforms offer comprehensive features and dedicated support. However, successful implementation of virtualization often requires specialized expertise for setup and configuration, particularly in complex environments.

- Key Industry Players: Major players such as VMware, Microsoft, Citrix Systems, and Oracle are leading innovation in this field. These companies are focused on developing virtualization platforms that support server virtualization, network virtualization, desktop virtualization, and cloud-native virtualization. To stay competitive, these market leaders invest in enhancing hypervisor technology, improving automation, and integrating robust security features.

IT Infrastructure Optimization through Virtualization

Key Highlights

- Cost Reduction: Virtualization helps businesses reduce operational expenses by minimizing the need for additional hardware. With server virtualization, multiple virtual machines run on a single server, optimizing hardware utilization and cutting costs associated with purchasing and maintaining physical servers.

- Hardware Savings: Traditional IT environments require separate physical servers for different operating systems, leading to hardware underutilization. By virtualizing these systems, companies achieve higher server utilization rates, reducing the overall number of physical machines required. This contributes to reduced capital expenditures on hardware and lower energy consumption.

- Scalability: Virtualization software enables rapid scaling of IT infrastructure. Businesses can quickly create, clone, or migrate virtual machines with minimal downtime, allowing them to respond to fluctuating demand in cloud environments or high-performance computing scenarios.

- Energy Efficiency: Consolidating physical servers leads to fewer energy requirements for power and cooling, enhancing the energy efficiency of data centers. This not only lowers operational costs but also supports corporate sustainability efforts by reducing the organization's carbon footprint.

Streamlining IT Operations with Virtualization

Virtualization technology dramatically simplifies IT management by allowing teams to centrally manage virtual environments. The ability to deploy virtual machines quickly and troubleshoot issues through a single platform enhances operational efficiency.

Key Highlights

- Centralized Management: Virtual machine management is simplified through centralized control offered by virtualization platforms. IT administrators can deploy, update, and manage multiple virtual environments from a single interface, reducing complexity and minimizing the time spent on maintenance.

- Disaster Recovery: Virtualization solutions enhance disaster recovery strategies. Virtual machines can be easily backed up and restored, significantly improving recovery times in case of system failure. Moreover, many virtualization platforms incorporate disaster recovery tools, reducing reliance on third-party solutions.

- Enhanced Security: Virtualization enables the isolation of virtual machines, reducing the risk of security breaches. With virtualization security features like role-based access control, encryption, and secure migration, businesses can safeguard sensitive data and limit the impact of potential attacks.

Virtualization Software Market Trends

PC/ Desktop Virtualization is Expected to hold Major Market share

- As the demand for scalable and efficient IT solutions grows, the virtualization software market is expanding rapidly. Virtualization technology, which enables the creation of virtual versions of hardware and storage devices, boosts resource utilization while cutting costs. Cloud computing, data center virtualization, and advancements in hypervisor technology are key drivers of this market. Several notable trends are shaping the future of virtualization software.

- Remote Work Boosting VDI Adoption: The shift to remote work has driven adoption of virtual desktop infrastructure (VDI), which enables businesses to securely deploy desktop environments from central servers. This ensures seamless performance regardless of the employee's location while reducing hardware costs.

- Application Virtualization Growth: As companies look to minimize compatibility issues and secure legacy systems, application virtualization is gaining traction. This technology allows applications to run independently from the underlying operating system, reducing risks and enhancing compatibility.

- Open-Source Software Expansion: Cost-effective open-source virtualization platforms such as KVM and Xen are gaining popularity, particularly among SMEs. These platforms provide powerful virtual machine management tools, helping businesses optimize their systems without incurring high licensing costs.

- Focus on Security: With the rise of cloud virtualization and hybrid IT setups, securing virtual environments has become a priority. The need to protect virtual machines and hypervisor layers drives demand for advanced security solutions, ensuring PC/desktop virtualization remains a dominant force in the market.

Asia Pacific is Expected to Register the Largest Market

- The Asia-Pacific region is expected to dominate the virtualization software market due to rapid industrialization, growing IT infrastructure investments, and the increasing adoption of cloud computing. Countries such as China, India, and Japan are spearheading this digital transformation, especially within industries like telecommunications and BFSI (Banking, Financial Services, and Insurance).

- Cloud Virtualization Growth: Businesses in the region are rapidly adopting cloud virtualization to enhance resource efficiency and cut IT costs. As companies shift from traditional hardware to virtualized environments, the demand for cloud services is driving robust market expansion.

- Open-Source Solutions for SMEs: Small and medium-sized enterprises (SMEs) are increasingly adopting open-source virtualization software due to its cost-efficiency and flexibility. This trend is bolstered by government initiatives to promote digital infrastructure in countries like India, leading to a higher demand for affordable, scalable virtualization solutions.

- Containerization Trends: The region is also witnessing a rise in containerization technologies, which offer more efficiency for cloud-native applications compared to traditional virtualization. This shift supports the growth of hybrid and multi-cloud environments, blending the benefits of both virtualization and containerization.

Virtualization Software Industry Overview

The virtualization software market is highly fragmented, with major corporations and niche players competing for market share. Companies like VMware, Microsoft, Oracle, and Citrix dominate the global landscape by offering comprehensive virtualization solutions across various sectors, including server virtualization, network virtualization, and desktop virtualization.

Key Industry Leaders: VMware remains a market leader with a wide range of solutions for data center virtualization. Microsoft's Hyper-V platform leverages the company's strong position in cloud services, while Oracle and Citrix focus on providing advanced, integrated virtualization solutions.

Emerging Trends for Future Growth: As trends like cloud-native virtualization and containerization gain traction, the market is shifting toward more agile and scalable solutions. Companies must invest in cloud integration, enhanced security, and support for multi-cloud environments to stay competitive. Emerging technologies like edge computing will also play a crucial role in shaping the future of this dynamic industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Assessment of Impact Of Covid-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Cost Reductions due to Reduced Hardware Spending

- 5.1.2 Improved IT Efficiency due to Virtualization

- 5.2 Market Challenges

- 5.2.1 Complexity in Setting up a Virtual Environment

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 PC Virtualization

- 6.1.2 Mobile Virtualization

- 6.2 By Type

- 6.2.1 Application Virtualization

- 6.2.2 Network Virtualization

- 6.2.3 Hardware Virtualization

- 6.2.4 Other Types

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 VMware Inc

- 7.1.2 Citrix Systems Inc.

- 7.1.3 Oracle Corporation

- 7.1.4 Microsoft Corporation

- 7.1.5 Red Hat Inc. (IBM Corporation)

- 7.1.6 Amazon Inc.

- 7.1.7 Google LLC.

- 7.1.8 NComupting Co. Ltd.

- 7.1.9 Parallels International GmbH

- 7.1.10 Huawei Technologies Co. Ltd.

- 7.1.11 Datadog, Inc.

- 7.1.12 Nutanix Inc.

- 7.1.13 TenAsys Corporation

- 7.1.14 Lynx Software Technologies