|

市场调查报告书

商品编码

1642038

现场可程式闸阵列(FPGA) -市场占有率分析、产业趋势与成长预测(2025-2030)Field Programmable Gate Array (FPGA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

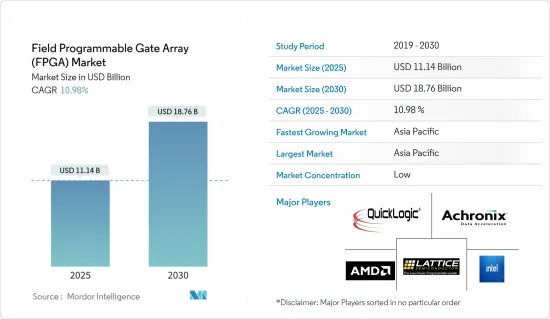

现场可程式闸阵列市场规模预计在 2025 年为 111.4 亿美元,预计到 2030 年将达到 187.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.98%。

FPGA(现场可程式闸阵列)是一种具有可程式硬体结构的积体电路。与 ASIC 和图形处理单元 (GPU) 不同,FPGA 晶片中的电路不是永久蚀刻的,可以根据需要重新编程。这种灵活性使 FPGA 成为 ASIC 的可行替代品,因为 ASIC 需要大量的开发时间和设计和製造投资。

关键亮点

- 因此,FPGA 加速了物件运动追踪、视讯串流和语音辨识等即时场景的执行。高效能运算的需求不断增长以及神经网路的日益复杂进一步凸显了 FPGA 在现代技术中的重要性。随着产业的不断发展,FPGA 在促进高阶运算任务方面发挥越来越重要的作用,使其成为各种高阶应用的必需品。

- FPGA 的节能和可自订的加速功能使其在资料中心和适应性云端运算系统中变得越来越重要。英特尔、微软、亚马逊、百度、IBM 和华为等领先公司正在将 FPGA 整合到其云端和资料中心服务中,使应用程式开发人员可以轻鬆使用它们。这种整合使开发人员能够利用 FPGA 的高效能和低功耗来提高其应用程式的效率和可扩展性。除了商业应用外,世界各地的许多学术和研究倡议在利用 FPGA 实现远端加速和提高用户灵活性。这些倡议旨在探索新的应用并增强现有的应用,利用 FPGA 的独特性能推动各个领域的创新和技术进步。

- 例如,2024 年 10 月,AMD 宣布推出 AMD Alveo UL3422,这是其破纪录的加速器系列的最新成员。 Alveo UL3422 为贸易公司、做市商和金融机构提供紧凑、机架空间和成本优化的加速器。 Alveo UL3422 采用纤薄的全高半长 (FHHL)外形规格,可无缝整合到各种伺服器和主机託管交换资料中心。与前代产品相比,Alveo UL3422 的端口密度、板载内存和连接选项有所降低,但仍由相同的 AMD Virtex UltraScale+ VU2P FPGA 提供支持,可确保超低延迟性能。

- FPGA 为各种汽车子系统提供动力,包括车载资讯娱乐系统、高级驾驶辅助系统 (ADAS) 以及混合动力汽车和电动车的充电系统。随着科技的进步,FPGA 的速度越来越快,价格也越来越便宜。 FPGA 在汽车应用领域的采用也迅速增加。例如,英特尔正在将 FPGA 整合到 HUD 显示器、主机硬体、安全功能等中,以扩大车载应用的范围。儘管存在一定的成本和性能限制,但 FPGA 越来越能满足许多驾驶员希望购买的下一代汽车即软体定义汽车的要求。

- 儘管 FPGA 具有吸引人的优势,但它们也存在效能下降和功耗增加等固有缺点。例如,由于 FPGA 具有可程式架构,因此其功耗通常比 ASIC 更高。功耗的增加是由于可配置逻辑块、互连和其他资源赋予了 FPGA 灵活性。在优先考虑能源效率的应用中,这样的功率需求可能是一个重大缺点。此外,由于 FPGA 是可程式设计的,因此它们在面积、功耗和效能方面会产生开销,因此不适合需要最高效率和速度的应用。

- 在复杂的地缘政治环境下,以色列与哈马斯之间持续的衝突有可能扰乱全球半导体产业。以色列在积体电路(IC)生产和创新中发挥关键作用,这可以影响全球 FPGA 使用的半导体装置的价格和可得性。

- 此外,2024年6月,英特尔计划取消在以色列建造价值250亿美元的新晶片製造厂的计画。这可能会间接降低基于 FPGA 应用的解决方案的可得性和生产量,从而影响预测期内的全球市场。

现场可程式闸闸阵列(FPGA) 市场趋势

IT和通讯占据较大的市场占有率

- IT 和通讯公司正在使用 FPGA 进行人工智慧 (AI) 和机器学习 (ML) 等高效能运算应用。 FPGA 支援影像识别、自然语言处理和巨量资料分析等任务的客製化演算法,并且通常比传统的 CPU 和 GPU 更有效率。

- 5G 网路正在迅速扩张,需要高速、低延迟的资料处理才能达到最佳效能。 FPGA 非常适合满足这些需求,尤其是在 5G基地台和边缘运算领域。 FPGA 加速资料处理并专业地管理呈指数成长的流量。随着5G基础设施的不断发展,核心和边缘应用对FPGA的需求只会增加。

- GSMA预测,到2030年,中国的5G连线数将超过16亿,占全球整体的近三分之一。此外,VIAVI Solutions 强调,到 2023 年 4 月,美国将在 503 个城市的 5G网路存取方面领先全球,超过中国的 356 个城市。这些新兴市场的发展有可能创造巨大的市场机会。

- 随着资料流量不断飙升以及连网设备数量的不断增长,特别是在物联网和通讯,网路安全和快速资料处理比以往任何时候都更加重要。透过硬体加速加密和安全资料处理,FPGA 可以快速适应不断变化的安全需求。这种适应性使得 FPGA 对于网路营运商克服复杂的处理挑战并保护大量资料至关重要。

- 随着物联网领域的不断扩大,特别是在通讯领域,对能够管理来自无数设备的多样化资料流的多功能、节能的运算解决方案的需求日益增长。 FPGA 在物联网闸道和边缘运算领域占有一席之地,能够实现本地资料处理,从而减少延迟并节省频宽。

亚太地区将经历大幅成长

- 中国的现场可程式闸闸阵列市场正从高度依赖海外供应商转向培育强大的国内生态系统,以抑制对进口的依赖。地缘政治因素,特别是贸易紧张和出口管制,凸显了技术自力更生的迫切性。因此,高云半导体、深圳盘石微系统和上海安路基资讯科技有限公司等国内参与企业纷纷涌现,专注于创新,与全球企业竞争。此外,市场正在经历研发投资的激增,目的是开发用于高阶应用的尖端 FPGA。

- 5G技术的出现已成为中国采用FPGA的关键催化剂。由于其高效的资料处理和讯号传输,FPGA 已成为基地台和更广泛的网路基础设施中不可或缺的一部分。基地台数量将从2019年的15万个飙升至2023年的338万个。中国工业部资料显示,截至2024年8月底,5G基地台数量已超过404万个,占全国行动基地台总数的32.1%。工信部进一步强调,中国5G行动用户已达9.66亿。

- 日本在机器人、汽车、电子和精密製造领域占据主导地位,并利用 FPGA 技术增强其竞争地位。瑞萨电子株式会社、NEC株式会社、Socionext Inc.等国内製造商正为日本现场可编程闸阵列市场做出越来越大的贡献,并在日本先进技术生态系统中发挥着举足轻重的作用。

- 随着美国科技竞争加剧,日本正策略性地加强其半导体产业。 2022年至2025年期间,日本将向半导体领域投资257亿美元,相当于国内生产总值(GDP)的0.71%。这项投资承诺非常出色,远远超过了其他工业国家为半导体产业提供的国家补贴。

- 印度现场可程式闸闸阵列市场已经从有限的学术和小众工业用途发展到通讯、汽车和航太等领域的广泛应用。印度拥有价值 2,500 亿美元的 IT 产业,不仅是全球人工智慧生态系统的重要参与企业,也为全球许多银行、製造商和企业提供服务。

现场可程式闸阵列(FPGA) 产业概况

竞争程度取决于影响所研究市场的各种因素,例如品牌身份验证、强大的竞争策略和透明度。调查的市场包括Xilinx Inc.(AMD Corporation)、Lattice Semiconductor Corporation、Intel Corporation和Microchip Technology Incorporated等知名供应商,因此竞争高度整合。由于整合不断加强、技术进步和地缘政治情势的变化,研究市场正在发生变化。

在一个透过创新获得永续竞争优势相当高的市场中,由于来自终端用户产业(如物联网)的新客户需求预计将激增,竞争也将加剧,而物联网将推动对连网型设备边缘运算的需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第 3 章执行摘要和主要发现

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 宏观经济趋势对产业的影响

第五章 市场动态

- 市场驱动因素

- 物联网需求不断成长

- 汽车产业和日益增强的技术创新有望推动市场

- 市场限制

- 与 ASIC 相比功耗更高

第六章 市场细分

- 按成分

- 高阶 FPGA

- 中阶FPGA/低阶 FPGA

- 按建筑分类

- 基于 SRAM 的 FPGA

- 基于耐熔熔丝的 FPGA

- 基于快闪记忆体的 FPGA

- 按最终用户产业

- 资讯科技/通讯

- 消费性电子产品

- 车

- 工业的

- 军事和航太

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 亚洲

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 北美洲

第七章 竞争格局

- 公司简介

- Advanced Micro Devices, Inc.

- Lattice Semiconductor Corporation

- QuickLogic Corporation

- Intel Corporation

- Achronix Semiconductor Corporation

- GOWIN Semiconductor Corp.

- Microchip Technology Incorporated

- Efinix, Inc.

8.供应商市场占有率分析

第九章投资分析

第十章:投资分析市场的未来

The Field Programmable Gate Array Market size is estimated at USD 11.14 billion in 2025, and is expected to reach USD 18.76 billion by 2030, at a CAGR of 10.98% during the forecast period (2025-2030).

Field-programmable gate arrays (FPGAs) are integrated circuits featuring a programmable hardware fabric. In contrast to ASICs and graphics processing units (GPUs), the circuitry within an FPGA chip is not permanently etched; it can be reprogrammed as needed. This flexibility positions FPGAs as a viable alternative to ASICs, which demand extensive development time and substantial investment in design and fabrication.

Key Highlights

- Consequently, FPGAs accelerate execution in real-time scenarios such as object motion tracking, video streaming, and speech recognition. The growing demand for high-performance computing and the increasing complexity of neural networks further underscore the importance of FPGAs in modern technology. As industries continue to evolve, the role of FPGAs in facilitating advanced computational tasks becomes increasingly critical, making them indispensable in various high-stakes applications.

- FPGAs are becoming increasingly vital in data centers and adaptable cloud computing systems due to their energy-efficient and customizable acceleration capabilities. Major players such as Intel, Microsoft, Amazon, Baidu, IBM, and Huawei are integrating FPGAs into their cloud and data center services, making them readily available to application developers. This integration empowers developers to harness the high performance and low power consumption of FPGAs, boosting the efficiency and scalability of their applications. In addition to commercial applications, many academic and research initiatives worldwide utilize FPGAs for remote acceleration and user flexibility. These initiatives seek to explore novel applications and enhance existing ones, leveraging the distinct advantages of FPGAs to foster innovation and technological progress across diverse domains.

- For instance, in October 2024, AMD unveiled its latest addition to the record-breaking family of accelerators, the AMD Alveo UL3422, specifically designed for ultra-low latency electronic trading applications. The Alveo UL3422 offers trading firms, market makers, and financial institutions a compact accelerator optimized for rack space and cost, ensuring a swift deployment across various servers. Packaged in a slim FHHL (full height, half length) form factor, the Alveo UL3422 seamlessly integrates into diverse servers and co-location exchange data centers. While the Alveo UL3422 reduces port density, onboard memory, and connectivity options compared to its predecessor, it retains the same AMD Virtex UltraScale+ VU2P FPGA, ensuring ultra-low latency performance.

- FPGAs are enhancing various automotive subsystems, such as in-vehicle infotainment, advanced driver assistance systems (ADAS), and charging systems in hybrid and electric vehicles. Thanks to technological advancements, FPGA performance speeds are on the rise, and their prices are becoming more accessible. Their adoption in automotive applications is also witnessing a notable surge. For instance, Intel is broadening the chip's automotive applications, integrating it into HUD displays, head unit hardware, safety features, and beyond. Despite certain cost and performance constraints, FPGAs are increasingly aligning with the demand for next-generation, software-defined vehicles many drivers seek.

- FPGAs offer compelling advantages, but they also come with inherent drawbacks, such as lower performance and higher power consumption. For example, FPGAs, due to their programmable architecture, generally consume more power than ASICs. This increased power consumption stems from the configurable logic blocks, interconnects, and other resources that provide FPGAs with their flexibility. Such power demands can be a significant drawback in applications prioritizing energy efficiency. Furthermore, the very programmability of FPGAs introduces overheads in area, power consumption, and performance, rendering them less ideal for applications demanding peak efficiency and speed.

- The ongoing conflict between Israel and Hamas, amid geopolitical complexities, threatens to disrupt the global semiconductor industry. Israel plays a significant role in Integrated Circuit (IC) production and innovation, which can impact the price and availability of semiconductor devices worldwide used in FPGAs.

- Additionally, in June 2024, Intel Corporation plans to stop building a new chip manufacturing plant worth USD 25 billion in Israel. This could indirectly lower the availability and production volume of solutions based on FPGA applications and impact the global market during the forecast period.

Field Programmable Gate Array (FPGA) Market Trends

IT and Telecommunication Holds Significant Market Share

- IT and telecommunication companies leverage FPGAs for high-performance computing applications, such as artificial intelligence (AI) and machine learning (ML). FPGAs support customized algorithms for tasks like image recognition, natural language processing, and big data analytics, often more efficiently than traditional CPUs and GPUs.

- 5G networks are rapidly expanding, necessitating high-speed and low-latency data processing for optimal performance. FPGAs are ideally positioned to fulfill these demands, especially in 5G base stations and edge computing. They accelerate data processing and adeptly manage the surge in traffic. With the continuous evolution of 5G infrastructure, the appetite for FPGAs in core and edge applications is on the rise.

- According to projections by GSMA, by 2030, China will boast over 1.6 billion 5G connections, representing nearly a third of the global tally. In addition, VIAVI Solutions highlights that by April 2023, the U.S. led globally with 5G network access spanning 503 cities, outpacing China's 356 cities. These developments are poised to unlock significant market opportunities.

- As data traffic surges and the number of connected devices, particularly in IoT and telecommunications, continues to grow, the importance of network security and swift data processing has never been more pronounced. FPGAs, with their capability for hardware-accelerated encryption and secure data processing, adapt swiftly to evolving security demands. This adaptability makes them indispensable for network operators safeguarding vast data while navigating intricate processing challenges.

- The expanding realm of IoT, especially within telecommunications, underscores the demand for versatile, energy-efficient computing solutions adept at managing diverse data streams from myriad devices. FPGAs are carving a niche in IoT gateways and edge computing, enabling local data processing that curtails latency and conserves bandwidth.

Asia Pacific to Register Major Growth

- China's field programmable gate array market has transitioned from heavy reliance on international suppliers to cultivating a robust domestic ecosystem, all in a bid to curtail import dependency. Geopolitical factors, notably trade tensions and export controls, have accentuated the urgency for technological self-reliance. Consequently, domestic players like GOWIN Semiconductor, Shenzhen Pango Microsystems Co., Ltd, and Shanghai Anlogic Infotech Co., Ltd, among others, have risen to prominence, channeling their efforts into innovations to rival established global entities. Furthermore, the market has witnessed a surge in R&D investments, aiming to craft sophisticated FPGAs tailored for high-end applications.

- The advent of 5G technology has emerged as a pivotal catalyst for FPGA adoption in China. With their prowess in efficient data processing and signal transmission, FPGAs have become indispensable in base stations and broader network infrastructures. The count of base stations skyrocketed from 0.15 million in 2019 to 3.38 million in 2023. Data from China's Ministry of Industry and Information Technology reveals that by the close of August 2024, the nation had eclipsed 4.04 million 5G base stations, accounting for 32.1% of the country's total mobile base stations. Additionally, the ministry highlighted that China's 5G mobile subscriber count reached an impressive 966 million.

- Japan, renowned for its leadership in robotics, automotive, electronics, and high-precision manufacturing, has harnessed FPGA technology to bolster its competitive edge. Local manufacturers, including Renesas Electronics Corporation, NEC Corporation, and Socionext Inc., have increasingly contributed to the country's field programmable gate array market, which plays a pivotal role in Japan's advanced technology ecosystem.

- Amid the escalating technological rivalry between the United States and China, Japan is strategically bolstering its semiconductor industry. The nation is channeling 0.71% of its gross domestic product (GDP), equating to USD 25.7 billion, into the semiconductor sector from 2022 to 2025. This investment commitment stands out, being notably more substantial than the state subsidies provided by other industrial nations to their semiconductor sectors.

- The field programmable gate array market in India has transitioned from limited academic and niche industrial applications to widespread adoption in sectors like telecommunications, automotive, and aerospace. With a USD 250 billion IT industry, India is not only a significant player in the global AI ecosystem but also caters to many of the world's banks, manufacturers, and firms.

Field Programmable Gate Array (FPGA) Industry Overview

The degree of competition depends on various factors affecting the market studied, such as brand identity, powerful competitive strategy, and degree of transparency. The market studied has prominent vendors, including Xilinx Inc. (AMD Corporation), Lattice Semiconductor Corporation, Intel Corporation, and Microchip Technology Incorporated, which makes it highly consolidated and competitive. With growing consolidation, technological advancement, and geopolitical scenarios, the market studied is witnessing changes.

In a market where sustainable competitive advantage through innovation is considerably high, the competition will only increase, considering the anticipated surge in demand from new customers from the end-user industries, such as IoT, in which edge computing in connected devices has been witnessing increasing demand.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of Macro Economic trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for IoT

- 5.1.2 Automotive Industry and Increasing Innovations are Expected to Drive the Market

- 5.2 Market Restraints

- 5.2.1 High Power Consumption Compared to ASIC

6 MARKET SEGMENTATION

- 6.1 By Configuration

- 6.1.1 High-end FPGA

- 6.1.2 Mid-range FPGA/Low-end FPGA

- 6.2 By Architecture

- 6.2.1 SRAM-based FPGA

- 6.2.2 Anti-fuse based FPGA

- 6.2.3 Flash-based FPGA

- 6.3 By End-user Industry

- 6.3.1 IT and Telecommunication

- 6.3.2 Consumer Electronics

- 6.3.3 Automotive

- 6.3.4 Industrial

- 6.3.5 Military and Aerospace

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 South Korea

- 6.4.3.5 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Advanced Micro Devices, Inc.

- 7.1.2 Lattice Semiconductor Corporation

- 7.1.3 QuickLogic Corporation

- 7.1.4 Intel Corporation

- 7.1.5 Achronix Semiconductor Corporation

- 7.1.6 GOWIN Semiconductor Corp.

- 7.1.7 Microchip Technology Incorporated

- 7.1.8 Efinix, Inc.

8 VENDOR MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

FPGA主机市场预测(至 2032 年):按产品类型、核心相容性、分销管道、技术、应用、最终用户和地区进行的全球分析

FPGA主机市场预测(至 2032 年):按产品类型、核心相容性、分销管道、技术、应用、最终用户和地区进行的全球分析 2025年全球嵌入式FPGA市场报告

2025年全球嵌入式FPGA市场报告 现场可程式闸阵列(FPGA) 市场:全球预测(2025-2030 年)

现场可程式闸阵列(FPGA) 市场:全球预测(2025-2030 年) 现场可程式闸阵列(FPGA) 市场 2025-2029

现场可程式闸阵列(FPGA) 市场 2025-2029 全球可程式设计硅市场

全球可程式设计硅市场 嵌入式 FPGA 市场报告,按技术(EEPROM、反熔丝、SRAM、快闪记忆体等)、应用(资料处理、消费性电子、工业、军事和航太、汽车、电信等)和地区划分,2025 年至 2033 年全球嵌入式 FPGA 市场低端现场可程式闸阵列(FPGA)的全球市场

嵌入式 FPGA 市场报告,按技术(EEPROM、反熔丝、SRAM、快闪记忆体等)、应用(资料处理、消费性电子、工业、军事和航太、汽车、电信等)和地区划分,2025 年至 2033 年全球嵌入式 FPGA 市场低端现场可程式闸阵列(FPGA)的全球市场 现场可程式闸阵列 (FPGA) 市场规模、份额、成长分析(按配置、按节点大小、按技术、垂直产业和按地区)- 产业预测(2025 年至 2032 年)2025 年至 2033 年现场可程式闸阵列 (FPGA) 市场报告(按架构、配置、最终用途产业和地区)

现场可程式闸阵列 (FPGA) 市场规模、份额、成长分析(按配置、按节点大小、按技术、垂直产业和按地区)- 产业预测(2025 年至 2032 年)2025 年至 2033 年现场可程式闸阵列 (FPGA) 市场报告(按架构、配置、最终用途产业和地区)