|

市场调查报告书

商品编码

1642113

无伺服器运算:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Serverless Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

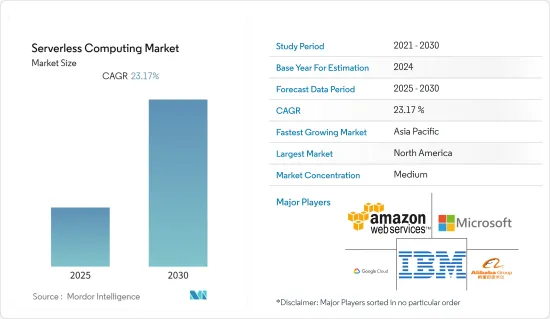

预测期内,无伺服器运算市场预计将以 23.17% 的复合年增长率成长。

主要亮点

- 透过采用无伺服器架构,企业可以有效地消除购买、安装、配置和排除新硬体组件故障的昂贵且耗时的方法。

- 随着商业环境中技术的快速变化,公司专注于缩短新产品和新功能的上市时间,以满足消费者日益增长的期望。预计预测期内此类上升趋势将推动市场发展。

- 在竞争激烈的市场中,新兴企业有望迅速扩大规模并提供增强的产品和服务能力,从而提高商业价值。因此,采用无伺服器技术来最大限度地缩短前置作业时间并对业务产生积极影响有望推动市场成长。

- 日益增长的安全性问题限制了无伺服器运算技术的采用。犹他州智慧 IT 自动化软体供应商 SaltStack 最近的一项调查发现,儘管三分之二的组织已经将超过 10% 的应用程式容器化,但 40% 的组织担心他们的容器策略需要在安全性方面进行足够的投资。此外,34% 的人表示他们公司的方法需要更详细的考虑。

- COVID-19 正在影响新技术的采用。这是因为,由于 COVID-19,其他任务被优先处理,许多组织无法跟上新技术的步伐。不过,预计这种放缓可能是暂时的。

无伺服器运算市场趋势

专业服务预计将实现强劲成长

- 数位时代正在急剧加速新产品、新服务和新经营模式的变革和发展。公司面临越来越大的压力,需要发布新功能和新产品来满足不断增长的客户期望。无伺服器架构在灵活性方面为中小型企业提供了显着的优势并降低了整体基础架构成本。

- 企业IT领域的重大创新使企业变得更加敏捷和有弹性,从而提高了成本效益。在这种情况下,无伺服器运算已经成为在不断变化的商业环境中部署云端服务和应用程式的重要元素。

- 此外,近年来,混合云端多重云端在专业服务运算中的使用有所增加。例如,如果一家公司希望释放本地资源以储存更敏感的资料和应用程序,混合云端可以帮助他们做到这一点,而无需花费大量资金来满足暂时的需求高峰。

- 此外,微服务和无伺服器运算的成长将从根本上改变 DevOps,模糊开发和营运之间的界线。企业希望透过其产品和服务提供增强的功能来提高业务价值并快速扩大规模。

- 此外,企业正在转向云端服务,从而刺激了现有竞争对手的竞争。然而,安全仍然是企业和云端服务供应商关注的主要问题,他们不断与网路安全供应商合作,以降低网路攻击的风险。

预计北美将占据最大市场占有率

- 预计北美将在收益方面占据最大的市场占有率,这得益于技术的快速进步以及零售、BFSI、製造、医疗保健、IT 和电讯等各个垂直行业的各种知名参与者的存在,并在整个全部区域拥有庞大的用户群。

- 为了在日益数位化和动态的市场中保持竞争力并快速提供新功能和新产品,企业正在积极采用新的云端处理服务。

- 此外,新兴企业正在寻求突破无伺服器运算模型的限制。该公司于去年 6 月宣布了开放原始码开发者平台「Akka Serverless」。

- 随着开发人员对管理其应用程式的责任越来越大,许多人正在采用可以代表他们自动管理IT基础设施的平台,而无需 IT 营运团队的参与。去年 6 月,提供云端服务以实现 DevOps 流程自动化的公司 Render 宣布,它增加了根据开发人员需求自动即时扩展运算和记忆体资源的功能。预计这些因素将有助于推动市场成长。

无伺服器运算产业概览

无伺服器运算市场竞争适中,有几位大型参与者。就市场占有率而言,目前少数几家公司占据主导地位。然而,随着专业服务领域的云端平台进步,新的参与者正进入市场,从而扩大其在新兴经济体的企业发展。

- 2022 年 11 月——为了更轻鬆地使用 AWS Lambda(亚马逊云端提供的无伺服器、事件驱动的运算服务)开发轻量级、可扩展的 Java 应用程序,AWS 发布了适用于 Java 的 AWS Lambda SnapStart。

- 2022年11月-在经历历史性低迷后试图恢復发展的中国电子商务巨头阿里巴巴宣布将在未来三个财年投资10亿美元为其云端运算客户提供服务。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 产业影响评估

- 技术简介

- API 网关

- Function as a Service(FaaS)

- Database as a Service(DbaaS)

- Backend as a Service(BaaS)

第五章 市场动态

- 市场驱动因素

- 透过提高扩充性、加快上市时间和降低营运成本来实现成长

- 微服务架构在组织经营模式中的普及程度

- 全球对专业服务的需求不断增长,推动市场

- 市场限制

- 受到攻击时失去安全控制

第六章 市场细分

- 按服务

- 专业的

- 託管

- 按类型

- 混合云端

- 多重云端

- 按最终用户产业

- 资讯科技/通讯

- BFSI

- 零售

- 政府

- 按行业

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Amazon Web Services Inc.

- Microsoft Corp.

- Google LLC

- Alibaba Group Holding Limited

- SAP SE

- IBM Corp.

- Iron.io

- Oracle Corp.

- Webtask.io

- VMware Inc.

第八章投资分析

第九章:市场的未来

简介目录

Product Code: 66660

The Serverless Computing Market is expected to register a CAGR of 23.17% during the forecast period.

Key Highlights

- With the adoption of serverless architecture, organizations can effectively eliminate expensive and time-consuming approaches such as purchasing new hardware components, installing, configuring, and troubleshooting, thereby shifting the responsibility of managing servers, databases, and application logic, which reduces set-up and maintenance costs.

- With the rapid technological shift in the business environment, companies are releasing new products and features, thereby focusing on reduced time-to-market to meet the exponentially growing consumer expectations. The increasing prominence of such trends is expected to drive the market during the forecast period.

- In the competitive marketplace, startups are anticipated to scale rapidly and deliver enhanced product and service features, thereby improving their business values. Hence, to achieve minimum lead time and positively impact their business, they are anticipated to adopt serverless technology, propelling the market's growth.

- The rising security concerns have been limiting the adoption of serverless computing technology. According to a recent survey by SaltStack, a Utah-based provider of intelligent IT automation software, even though two-thirds of organizations have more than 10% of their applications containerized, 40% of the organizations still need to be concerned that their container strategy needs to invest in security adequately. Another 34% reported that their approach needs more detail.

- COVID-19 has impacted the adoption of new technologies. This is because many organizations cannot deal with new technology due to the other tasks that have taken precedence due to COVID-19. However, it is also anticipated to be likely a temporary slowdown.

Serverless Computing Market Trends

Professional Services are Expected to Grow at a Significant Rate

- The digital era has dramatically accelerated the change and evolution of new products, services, and business models. Enterprises face pressure to release new features and products that meet customers' growing expectations. Serverless architecture offers significant advantages to SMEs in terms of flexibility and reduces overall infrastructure costs.

- Significant innovations in the enterprise IT space have enabled business agility and improved resiliency, thereby driving cost-effectiveness. In such scenarios, serverless computing has emerged as a vital element for deploying cloud services and applications across the everchanging business environment.

- Further, hybrid and multi-cloud use in professional service computing has increased in recent years. For example, when a company wants to free up local resources for more sensitive data or applications, using a hybrid cloud enables it to do so without spending a ton of money on handling a temporary surge in demand.

- Moreover, the growth of microservices and serverless computing is fundamentally changing DevOps by blurring the line between development and operations. Organizations are envisioned to scale rapidly in delivering enhanced features through their products and services offering, thereby improving their business values.

- Further, businesses are moving toward cloud services, adding to the existing competition. However, security remains a significant concern among adopters and cloud service providers, who continuously work with cybersecurity vendors to reduce any risk of cyber-attacks.

North America is Expected to Hold the Largest Market Share

- North America is anticipated to capture the largest market share regarding revenue, owing to rapid advancement in technologies and the presence of various prominent players across the industries such as retail, BFSI, manufacturing, healthcare, and IT & Telecom, boasting of a large user base across the region.

- Due to high digitalization and high adoption of new cloud computing services by enterprises to remain competitive in the dynamic market and deliver new features and products quickly, they are constantly innovating and adopting new technologies, thereby fueling the market's demand across the region.

- Further, a startup called Lightbend Inc. is trying to get around the limitations of the serverless computing model that often prevent its adoption for more complex, data-hungry applications. In June last year, the company announced a new, open-source developer platform called Akka Serverless, which it said would set a new standard for cloud-native application development.

- As developers assume more responsibility for managing their applications, many are starting to embrace platforms that automate IT infrastructure management on their behalf without intervention from an IT operations team. In June last year, Render, a provider of cloud services that automates DevOps processes, announced it is adding the ability to automatically scale compute and memory resources up and down in real-time as developers require. Such factors would cater to the market growth adoptions.

Serverless Computing Industry Overview

The serverless computing market is moderately competitive and consists of several significant players. In terms of market share, some of the players are currently dominating the market. However, with the advancement in the cloud platform across professional services, new players are increasing their market presence, thereby expanding their business footprint across emerging economies.

- November 2022 - To make it simpler to develop nimble, scalable Java apps using AWS Lambda, the serverless, event-driven computing service in the Amazon cloud, AWS has released AWS Lambda SnapStart for Java.

- November 2022 - Alibaba, the Chinese e-commerce behemoth looking to restart development after a historical slump, announced that it would invest $1 billion over the next three fiscal years to serve its cloud computing customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of COVID-19 impact on the industry

- 4.4 Technology Snapshot

- 4.4.1 API Gateway

- 4.4.2 Function as a Service (FaaS)

- 4.4.3 Database as a Service (DbaaS)

- 4.4.4 Backend as a Service (BaaS)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Enhanced Scalability, Decreased in Time-To-Market Along with Reduced Operational Cost

- 5.1.2 Proliferation of the Microservices Architecture Across Organization's Business Model

- 5.1.3 Increase in demand of Professional services globally to drive the market

- 5.2 Market Restraints

- 5.2.1 Loss of Control on Security in Case of Attack

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Professional

- 6.1.2 Managed

- 6.2 By Type

- 6.2.1 Hybrid Cloud

- 6.2.2 Multi-Cloud

- 6.3 By End-user Industyr

- 6.3.1 IT & Telecommunication

- 6.3.2 BFSI

- 6.3.3 Retail

- 6.3.4 Government

- 6.3.5 Industrial

- 6.3.6 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amazon Web Services Inc.

- 7.1.2 Microsoft Corp.

- 7.1.3 Google LLC

- 7.1.4 Alibaba Group Holding Limited

- 7.1.5 SAP SE

- 7.1.6 IBM Corp.

- 7.1.7 Iron.io

- 7.1.8 Oracle Corp.

- 7.1.9 Webtask.io

- 7.1.10 VMware Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

无伺服器运算市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032)

无伺服器运算市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032) 全球无伺服器运算市场

全球无伺服器运算市场 2025年无伺服器运算平台全球市场报告

2025年无伺服器运算平台全球市场报告 无伺服器计算全球市场规模、份额、趋势分析报告,按服务模式、公司规模、部署、行业、地区、展望和预测,2024 年至 2031 年无伺服器运算市场规模、份额、趋势分析报告:按服务模式、部署、企业规模、最终用途、地区和细分市场预测,2025 年至 2030 年

无伺服器计算全球市场规模、份额、趋势分析报告,按服务模式、公司规模、部署、行业、地区、展望和预测,2024 年至 2031 年无伺服器运算市场规模、份额、趋势分析报告:按服务模式、部署、企业规模、最终用途、地区和细分市场预测,2025 年至 2030 年 到 2030 年无伺服器运算市场预测:按服务类型、使用类型、部署模型、公司规模、应用程式、最终用户和地区进行的全球分析

到 2030 年无伺服器运算市场预测:按服务类型、使用类型、部署模型、公司规模、应用程式、最终用户和地区进行的全球分析 无伺服器计算市场,按服务类型、按部署模型、按组织规模、按最终用户、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

无伺服器计算市场,按服务类型、按部署模型、按组织规模、按最终用户、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 无伺服器运算市场:按服务类型、按服务模型、按部署模型、按组织规模、按行业、按地区 - 到 2029 年的预测

无伺服器运算市场:按服务类型、按服务模型、按部署模型、按组织规模、按行业、按地区 - 到 2029 年的预测