|

市场调查报告书

商品编码

1642123

融合式基础架构:市场占有率分析、产业趋势与成长预测(2025-2030 年)Hyper-Converged Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

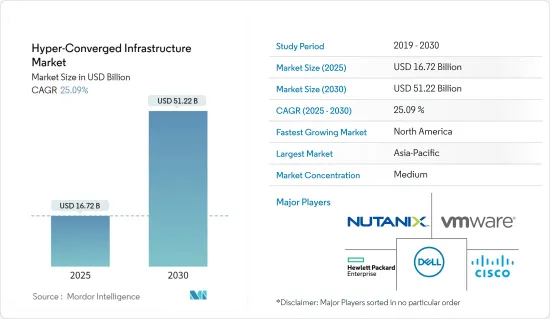

融合式基础架构市场规模在 2025 年估计为 167.2 亿美元,预计到 2030 年将达到 512.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 25.09%。

主要亮点

- 超融合基础架构 (HCI) 已成为 IT 产业的变革性解决方案,彻底改变了企业管理资料的方式。随着企业寻求简化基础设施、提高营运效率和实现数位转型,HCI 市场正在经历显着的成长和采用。

- 超融合式基础架构市场的主要驱动力是云端运算的日益普及。各行各业的企业都在将其工作负载转移到云端,以利用其扩充性、成本效益和灵活性。 HCI 解决方案透过无缝整合内部部署和云端资源来补充云端环境。 HCI 让企业能够轻鬆地在私有云端云和公共云端云之间移动工作负载,从而实现结合两种环境优势的混合云端部署。 HCI 与云端处理之间的这种协同效应正在加速市场成长,并预计将继续推动对融合式基础架构解决方案的需求。

- 对于希望优化IT基础设施并降低营运成本的组织来说,资料中心虚拟与整合已变得至关重要。融合式基础架构基础设施为资料中心管理提供了统一的方法,让企业将多个元件组合成一个整合系统。透过利用虚拟技术,HCI 能够更有效地分配和利用运算资源,从而提高效能并减少硬体占用空间。 HCI 提供的扩充性和灵活性使其成为资料中心整合和虚拟计划的理想解决方案。因此,在高效资料中心营运需求的推动下,超融合式基础架构市场正经历显着成长。

- 由于各种应用导致IT基础设施基础设施效率的提高,全球融合式基础架构市场的需求正在增加。这种需求激增的原因是融合式基础架构基础设施系统能够提供简介、复製和加密等功能来保护本地资料中心内的资料。因此,各行各业的组织都在寻找这样的解决方案。

- 然而,部署HCI解决方案的高昂初始投资成本阻碍了市场的发展。虽然 HCI 提供了许多好处,包括简化管理、提高可扩展性和降低营运成本,但部署这些解决方案所需的初始投资却相当大。硬体、软体授权和专业服务的成本可能相当高,尤其是对于 IT 预算有限的中小型企业 (SME) 而言。高昂的初始投资成本是采用的障碍并阻碍了市场成长。然而,随着市场成熟和技术进步,HCI 解决方案的成本预计会下降,使更广泛的组织能够使用它们。

- 新冠疫情大大加速了各行各业的数位转型进程。世界各地的组织已经意识到敏捷且有弹性的IT基础设施对于支援远距工作、线上协作和数位服务的重要性。融合式基础架构透过提供扩充性和灵活的基础设施基础,使这种转变成为可能。这场疫情凸显了企业对敏捷性和适应性的必要性,进而导致对 HCI 解决方案的采用增加。因此,随着企业继续投资于增强其数位化能力的技术,预计后疫情时代将进一步推动融合式基础架构市场的发展。

融合式基础架构市场趋势

对更强有力的资料保护的需求不断增长,推动了市场成长

- 现今的企业对于可靠、高效能储存的需求日益增加。融合式基础架构(HCI) 将网路、储存和运算结合到单一系统中,以提供安全且有效率的解决方案。这种资源整合简化了管理、降低了成本,对许多企业的策略 IT 重点至关重要。

- 由于 HCI 解决方案的采用日益广泛,尤其是在资料安全和灾难復原等领域,HCI 市场正在不断扩大。社群媒体、知识平台等数位科技平台的传播也促进了人机互动需求的成长。根据 IBM 最新的资料外洩报告,资料外洩的平均成本增加 2.6%,达到 435 万美元(包括罚款)。 HCI 系统透过其元件和应用程式降低资料安全漏洞的风险,并且通常采用具有内建安全功能的高安全性 AMD 处理器。

- 此外,与传统储存解决方案相比,HCI 提供了更高的资料安全性和扩充性。随着连接设备和物联网 (IoT) 的数量不断增长,HCI 在集中系统中收集和储存分析资料的能力变得越来越有价值。此功能与 5G 网路的未来非常契合,其中 HCI 透过统一介面呈现其收集的资料的能力将被证明是有利的。根据GSMA预测,今年5G连线数将超过10亿,到2025年将达到20亿,将进一步推动HCI市场的发展。

- 与云端为基础的服务一样,HCI 针对虚拟工作负载进行了最佳化,并提供灵活的、基于消费的基础架构经济性。透过新增 HCI 建置模组,企业可以快速扩展资源,快速回应业务需求并提高 IT 服务的灵活性。透过将集中管理、运算、储存和资料安全等基本云端处理服务整合到整合系统中,HCI 成为一个全面的解决方案。

- 自动化和机器学习被广泛认为能够帮助企业提高应用程式效能、处理大量资料并提高生产力。 HCI 利用 AI 来满足工作负载需求、最佳化应用程式工作负载并最佳化储存。透过弥合私有云端、公有云和现有资料中心基础架构之间的差距,混合多重云端模型中的 HCI 使企业能够管理端到端资料工作流程,并确保轻鬆存取 AI 应用程式的资料。正如去年的人工智慧指数报告所强调的那样,企业对人工智慧的投资不断增加也推动了人机互动市场的发展,去年全球投资达到约 940 亿美元,较前一年的 678.5 亿美元大幅成长。

北美有望创下最快成长

- 北美 HCI 市场的成长主要受到该地区超大规模云端服务供应商扩张的推动。批发和零售领域的主机託管服务也正在成长。行动资料使用量的增加和自带设备 (BYOD) 法规的实施对支援虚拟桌面的基础设施提出了更高的要求。因此,预计北美的 HCI市场占有率将会成长。

- 一些资料中心公司正在对超大规模资料中心进行大量投资。例如,Equinix 已宣布计划在全球主要市场建造 32 个超大规模资料中心。 Equinix 投资超过 69 亿美元,总容量达到 600 兆瓦,旨在扩大其影响力并利用不断增长的超大规模资料中心格局。区域资料中心的兴起预计将进一步推动 HCI 市场的发展。

- 伙伴关係和联盟也正在塑造北美 HCI 市场。例如,联想和 Kindrill 扩大了合作,以开发和提供可扩展的混合运算、先进的运算实施和云端解决方案。透过利用联想在 PC、储存和伺服器效能方面的专业知识以及 Kyndryl 的IT基础设施服务,此次伙伴关係旨在为客户提供跨混合云、HCI 和高阶运算应用的全面解决方案。

- 此外,企业中 HCI 采用的激增也推动了对软体定义储存的需求。为了因应这一趋势,DataCore Software 收购了物件储存专家 Caringo Inc.此次收购使 DataCore Software 能够提供统一的区块、檔案和物件储存包。 Caringo 的 Swarm 平台专为超大规模资料存取和储存而设计,可满足资料管治需求并减少对硬体的依赖。 DataCore资料管理解决方案的最新版本扩展了跨分散式储存资源的资料存取能力。

融合式基础架构产业概览

融合式基础架构基础设施市场竞争适中,主要企业很少。目前,少数几家公司在市场占有率份额上占据主导地位。然而,随着使用云端平台的基础设施服务的进步,新参与者正在增加其在市场上的份额,并在新兴国家扩大企业发展。市场主要企业不断建立联盟、合併和投资以保持其市场地位。

2023年2月,华为宣布计画透过采用巨量资料、人工智慧、边缘运算和智慧製造等先进技术来加速企业数位转型。其中超融合式基础架构正快速演进,从传统资料中心走向边缘,从结构化资料走向非结构化资料,从单一通用算力走向多元化算力。这种演变已经成为建立资料中心的主流方法之一。

此外,为了支撑这一趋势,华为正准备推出超融合策略和新产品,包括鲯鹏超融合、蓝鲸应用商城、超融合软体、支撑工具等。这些产品全面升级生态系统发展、使用者体验和业务能力。

2022 年 4 月,Equinix 和戴尔扩大了伙伴关係,以提供超融合资料中心。作为此次扩展的一部分,Equinix 正在扩展其 Equinix Metal 裸机设备系列。此外,公告还推出了多项新服务,包括 Equinix Metal 上的 Dell PowerStore、Equinix Metal 上的 Dell VxRail 和 Equinix Metal 上的 Dell EMC PowerProtect DDVE。这些新解决方案旨在透过将戴尔的先进硬体与 Equinix 的强大裸机基础设施相结合来提供增强的功能和性能。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 购买者/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 对市场的影响

第五章 市场动态

- 市场驱动因素

- 对更强有力的资料保护的需求日益增加

- 云端平台整合需求日益增长

- 市场限制

- 商业生态系中资料隐私的丧失

第六章 市场细分

- 按服务

- 专业的

- 託管

- 按组织类型

- 大型企业

- 中小型企业

- 按最终用户产业

- 资讯科技/通讯

- BFSI

- 卫生保健

- 零售

- 政府和国防

- 其他最终用户产业

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争格局

- 公司简介

- Nutanix Inc.

- Dell Inc.

- VMware Inc.

- Hewlett Packard Enterprise Development LP

- Cisco System Inc.

- Oracle Corp.

- Microsoft Corp.

- NetApp Inc.

- IBM Corp.(Red Hat Inc.)

- Huawei Technologies Co. Ltd

- StarWind Software Inc.

- Datacore Software Corp.

- Maxta Inc.

- Pivot3 Inc.

第八章投资分析

第九章 市场机会与未来趋势

The Hyper-Converged Infrastructure Market size is estimated at USD 16.72 billion in 2025, and is expected to reach USD 51.22 billion by 2030, at a CAGR of 25.09% during the forecast period (2025-2030).

Key Highlights

- Hyper-convergence infrastructure (HCI) has emerged as a transformative solution within the IT industry, revolutionizing the way organizations manage their data centers. The market for HCI has experienced significant growth and adoption as businesses seek to streamline their infrastructure, enhance operational efficiency, and embrace digital transformation.

- The increasing adoption of cloud computing has been a major driving factor for the hyper-converged infrastructure market. Enterprises across various industries are shifting their workloads to the cloud to leverage its scalability, cost-effectiveness, and flexibility. HCI solutions complement cloud environments by seamlessly integrating on-premises and cloud resources. With HCI, organizations can easily migrate workloads between private and public clouds, enabling hybrid cloud deployments that combine the benefits of both environments. This synergy between HCI and cloud computing has accelerated the market growth and is expected to continue driving the demand for hyper-converged infrastructure solutions.

- Data center virtualization and consolidation have become imperative for organizations seeking to optimize their IT infrastructure and reduce operational costs. Hyper-converged infrastructure offers a consolidated approach to data center management, enabling organizations to combine multiple components into a single, unified system. By leveraging virtualization technologies, HCI enables the efficient allocation and utilization of computing resources, leading to improved performance and reduced hardware footprint. The scalability and flexibility offered by HCI make it an ideal solution for data center consolidation and virtualization initiatives. As a result, the market for hyper-converged infrastructure is experiencing substantial growth driven by the demand for efficient data center operations.

- The global hyper-converged infrastructure market is experiencing increasing demand due to various applications, leading to greater efficiency in IT infrastructure. This surge in demand is fueled by the ability of hyper-converged infrastructure systems to safeguard data within on-premises data centers, offering features such as snapshots, replication, and encryption. Consequently, organizations across various sectors are seeking these solutions.

- However, the high initial investment cost of implementing HCI solutions is hampering the market. While HCI offers numerous benefits, including simplified management, improved scalability, and reduced operational costs, the upfront investment required to deploy these solutions can be significant. The costs of hardware, software licenses, and professional services can be challenging, particularly for small and medium-sized enterprises (SMEs) with limited IT budgets. The high initial investment cost is a barrier to adoption, hindering market growth. However, as the market matures and technology advancements occur, the cost of HCI solutions is expected to decline, making them more accessible to a broader range of organizations.

- The COVID-19 pandemic significantly accelerated digital transformation initiatives across industries. Organizations worldwide realized the importance of agile and resilient IT infrastructure to support remote work, online collaboration, and digital services. Hyper-converged infrastructure enabled these transformations by providing a scalable and flexible infrastructure foundation. The pandemic highlighted the need for businesses to be agile and adaptable, leading to increased adoption of HCI solutions. As a result, the post-COVID-19 era is expected to witness a further boost in the hyper-converged infrastructure market as organizations continue to invest in technologies that enhance their digital capabilities.

Hyper converged Infrastructure Market Trends

Growing Need for Enhanced Data Protection Driving the Market Growth

- Organizations today have a growing need for reliable and high-performance storage. Hyperconverged infrastructure (HCI) provides a secure and efficient solution by integrating networking, storage, and computation into a single system. This consolidation of resources streamlines management, reduces costs, and is considered crucial by many enterprises for their strategic IT priorities.

- The market for HCI is expanding due to the increasing adoption of HCI solutions, particularly in areas such as data security and disaster recovery. The widespread use of digital technology platforms like social media and knowledge platforms has also contributed to the growing demand for HCI. According to the IBM Data Breach's recent report, the average cost of data breaches has increased by 2.6% to USD 4.35 million, with penalties included. HCI systems mitigate the risk of data security breaches through their components and applications, and they often incorporate high-security AMD processors with security capabilities.

- Furthermore, HCI offers improved data security and scalability compared to traditional storage solutions. As the number of connected devices and the Internet of Things (IoT) continue to rise, the ability of HCI to gather and store analytics in a centralized management system becomes increasingly valuable. This feature aligns well with the future of 5G networks, where HCI's ability to view collected data through a unified interface proves advantageous. According to the GSMA, 5G connections are expected to surpass 1 billion this year and reach 2 billion by 2025, further driving the HCI market.

- HCI is optimized for virtual workloads, similar to public cloud-based services, and offers flexible, consumption-based infrastructure economics. It enables enterprises to rapidly scale their resources by adding HCI building blocks, allowing them to respond quickly to business demands and enhance IT service agility. With essential cloud computing services such as centralized administration, computation, storage, and data security embedded into hyper-converged systems, HCI becomes a comprehensive solution.

- Automation and machine learning are widely recognized as productivity boosters for businesses, enabling improved application performance and handling large amounts of data. HCI leverages AI to handle workload demands, optimize application workloads, and optimize storage. By bridging the gaps between on-premises private cloud, public cloud, and existing data center infrastructure, HCI in a hybrid multi-cloud model allows businesses to manage end-to-end data workflows and ensure easy accessibility of data for AI applications. The increasing corporate investment in AI, as highlighted by the Artificial Intelligence Index previous year's report, also drives the HCI market forward, with last year's global investment reaching almost USD 94 billion, a significant increase from the prior year's acquisition of USD 67.85 billion.

North America is Expected to Register the Fastest Growth

- The expansion of hyper-scale cloud service providers in the region primarily drives the growth of the HCI market in North America. Colocation services have also experienced growth in both the wholesale and retail sectors. The demand for infrastructure to support virtual desktops has increased due to rising mobile data usage and the implementation of bring-your-own-device (BYOD) regulations. As a result, HCI's market share is expected to increase in North America.

- Several data center companies have made significant investments in hyperscale data centers. Equinix, for instance, has announced plans to build 32 hyperscale data centers in major global markets. With a substantial investment of over USD 6.9 billion and a total capacity of 600 megawatts, Equinix aims to expand its presence and capitalize on the growing hyper-scale data center landscape. The increasing number of regional data centers will drive the HCI market further.

- Partnerships and collaborations are also shaping the HCI market in North America. For instance, Lenovo and Kyndryl expanded their collaboration to develop and deliver scalable hybrid and advanced computing implementations and cloud solutions. Leveraging Lenovo's expertise in PCs, storage, and server performance, along with Kyndryl's IT infrastructure services, the partnership aims to provide customers with comprehensive solutions across the hybrid cloud, HCI, and advanced computing applications.

- Moreover, the surge in enterprise deployments of HCI has led to a growing demand for software-defined storage. In response to this trend, DataCore Software acquired Caringo Inc., a specialist in object storage. This acquisition enables DataCore Software to offer a unified block, file, and object storage package. Caringo's Swarm platform, designed for hyperscale data access and storage, addresses data governance needs and reduces reliance on hardware. The latest version of DataCore's data management solution expands data access capabilities across distributed storage resources.

Hyper converged Infrastructure Industry Overview

The hyper-converged infrastructure market is moderately competitive and has a few major players. Some of the players currently dominate the market in terms of market share. However, with the advancement in infrastructure services across the cloud platform, new players are increasing their market presence, expanding their business footprint across emerging economies. The Key players in the market are continuously making partnerships, mergers, and investments to retain their market position.

In February 2023, Huawei announced its plans to accelerate the digital transformation of enterprises by implementing advanced technologies such as big data, artificial intelligence, edge computing, and intelligent manufacturing. In this context, hyper-converged infrastructure is evolving rapidly, shifting from traditional data centers to the edge, from structured to unstructured data, and from single general-purpose computing power to diversified computing power. This evolution has become one of the mainstream approaches for constructing data centers.

Moreover, to support this trend, Huawei is preparing to launch its hyper-convergence strategy and new products like Kunpeng Hyperconvergence, Blue Whale Application Mall, hyper-convergence software, and supporting tools. These offerings will comprehensively upgrade ecosystem development, user experience, and business capabilities.

In April 2022, Equinix and Dell expanded their partnership to provide hyper-converged data center offerings. As part of this expansion, Equinix extended its Equinix Metal line of bare metal appliances. Moreover, the expansion includes introducing several new offerings, including Dell PowerStore on Equinix Metal, Dell VxRail on Equinix Metal, and Dell EMC PowerProtect DDVE on Equinix Metal. These new solutions aimed to deliver enhanced capabilities and performance by combining Dell's advanced hardware with Equinix's robust bare metal infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for Enhanced Data Protection

- 5.1.2 Rising Demand for Integration Over Cloud Platform

- 5.2 Market Restraints

- 5.2.1 Loss of Data Privacy Over the Business Eco-system

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Professional

- 6.1.2 Managed

- 6.2 By Organization Type

- 6.2.1 Large Enterprise

- 6.2.2 Small & Medium Enterprise

- 6.3 By End-user Industry

- 6.3.1 IT & Telecommunication

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Government and Defence

- 6.3.6 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nutanix Inc.

- 7.1.2 Dell Inc.

- 7.1.3 VMware Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Cisco System Inc.

- 7.1.6 Oracle Corp.

- 7.1.7 Microsoft Corp.

- 7.1.8 NetApp Inc.

- 7.1.9 IBM Corp. (Red Hat Inc.)

- 7.1.10 Huawei Technologies Co. Ltd

- 7.1.11 StarWind Software Inc.

- 7.1.12 Datacore Software Corp.

- 7.1.13 Maxta Inc.

- 7.1.14 Pivot3 Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

融合式基础架构市场规模、份额、趋势和预测:按组件、应用、最终用户和地区划分,2026-2034 年

融合式基础架构市场规模、份额、趋势和预测:按组件、应用、最终用户和地区划分,2026-2034 年 2026年全球融合式基础架构(HCI)解决方案市场报告2026年融合式基础架构全球市场报告

2026年全球融合式基础架构(HCI)解决方案市场报告2026年融合式基础架构全球市场报告 超融合融合式基础架构市场:市场规模、份额、成长率、全球产业分析、按类型、应用和地区分類的分析以及未来预测(2026-2034 年)

超融合融合式基础架构市场:市场规模、份额、成长率、全球产业分析、按类型、应用和地区分類的分析以及未来预测(2026-2034 年) 融合式基础架构市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和模组划分日本超融合基础设施市场报告(按组件、应用、最终用途和地区划分,2026-2034 年)

融合式基础架构市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和模组划分日本超融合基础设施市场报告(按组件、应用、最终用途和地区划分,2026-2034 年) 超融合融合式基础架构市场规模、份额和成长分析(按组件、应用、最终用户、组织规模、公司和地区划分)—2026-2033年产业预测

超融合融合式基础架构市场规模、份额和成长分析(按组件、应用、最终用户、组织规模、公司和地区划分)—2026-2033年产业预测 超融合融合式基础架构市场(按组件、部署方式、组织规模和最终用户产业)—2025-2032 年全球预测

超融合融合式基础架构市场(按组件、部署方式、组织规模和最终用户产业)—2025-2032 年全球预测 2025 年至 2029 年全球融合式基础架构市场

2025 年至 2029 年全球融合式基础架构市场 超融合基础设施 (HCI) 市场:全球产业分析、规模、占有率、成长、趋势和预测(2024-2031 年)

超融合基础设施 (HCI) 市场:全球产业分析、规模、占有率、成长、趋势和预测(2024-2031 年)