|

市场调查报告书

商品编码

1643053

基础设施监控:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Infrastructure Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

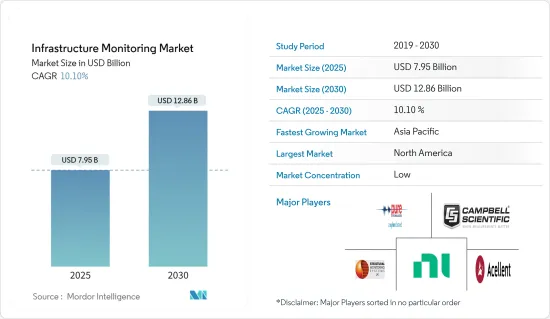

基础设施监控市场规模预计在 2025 年为 79.5 亿美元,预计到 2030 年将达到 128.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.1%。

主要亮点

- 先进感测器技术的使用不断增加、感测器成本不断下降、预防性保养的需求不断增长以及为确保最终用户行业更好地维护关键基础设施而增加的资本支出,正在推动基础设施监控市场的成长。

- 为了降低生命週期维护成本,对预测性维护的需求不断增长,这是该行业的主要驱动力之一。 MEMS(微机电系统)惯性感测器广泛用于建筑物、生产系统甚至汽车的预测状态监控。物联网和高阶分析技术的出现进一步增强了这项特性,并不断提高此类系统的功能。

- 2022 年 2 月,可观察性公司 New Relic 宣布全面推出一种新的基础设施监控体验,专门设计用于使 SRE、DevOps 和 ITOps 团队能够主动解决和识别私有、公有和混合云基础设施中的问题。这种现代化的体验使工程师能够根据关键的黄金讯号条件进行排序和过滤,立即隔离瓶颈,远端检测(包括事件、日誌、网路、警报等),在拓扑图上可视化爆炸半径,并执行历史分析以了解各种级联影响。

- 此外,使用智慧感测器远端监控关键基础设施的能力正在推动市场成长。这在采矿等终端用户领域非常有用,使用智慧感测器监控结构可以帮助公司节省金钱和挽救生命。 First Sensor 的惯性感测器能够实现 10 μg 或 0.0005°(2 角秒)的分辨率,广泛用于建筑物、桥樑和风力发电机的远端监控。

- 透地雷达(GPR)也因其成本优势而变得越来越重要。它们越来越多地被用于检查桥樑和隧道、勘测道路以及确保道路上的沥青得到充分压实。例如,肯塔基州交通中心使用 GPR 技术在连接肯塔基州和田纳西州的坎伯兰峡隧道中发现了一个大空洞。此外,GPR 确认隧道一侧无需维修,大大降低了维修成本。

- 然而,所涉及的高成本,特别是在实施和部署方面,可能是阻碍整个预测期内整体市场成长的主要问题。

- 在 COVID-19 疫情期间,基础设施监控市场中的公司因无法进入现场和供应链中断而面临暂时的营运挑战,对市场成长产生不利影响。各类协会,包括那些提供多项认证的协会,也受到了严重打击。然而,必维国际检验集团等公司报告称,自疫情爆发以来,对海上资产和设施的远端检查需求增加了 900%。

基础设施监控市场趋势

能源产业预计将占据较大的市场份额

- 由于对提高能源效率、永续性和成本效益的需求不断增加,预计能源产业将在基础设施监控市场中占据重要地位。此外,及时和预测性维护对能源部门资产的重要性日益增加,为能源部门基础设施监控的成长带来了光明的未来。

- 此外,结构安全监控系统提供的远端维护优势对于该领域的陆上和海上系统都非常有益。例如,风力发电机越来越多地使用中央资料模组来传输与不同结构条件相关的资料。此外,随着云端解决方案的引入,现在可以持续收集这些结构安全监控资料并进行评估以进行预测性维护。大多数风电场营运商使用监控和资料采集 (SCADA)资料进行远端监控和管理。

- 此外,结构健康监测解决方案透过早期检测节省了大量成本,从而鼓励对未来预测性维护解决方案的投资。杜克能源利用Schneider ElectricAvantis PRiSM 技术提前检测涡轮转子裂纹,节省了超过 750 万美元。这可确保资产优化并避免因维护而导致的成本超支。

- 此外,非侵入式结构监测对核能领域非常重要,核能领域在设计上支援此技术。核子反应炉的传感器在混凝土浇筑时安装,或插入现有结构上钻的孔中。这需要监控和维护,特别是正常运作和操作,这将极大地促进市场成长。

- 此外,据世界核能协会称,截至2022年5月,全球整体共有95座核子反应炉计画兴建。中国最多,有33起,其次是俄罗斯27起和印度12起。此外,随着核能发电厂的老化,维护的重要性预计会增加,为被调查的市场创造市场机会。

亚太地区预计将以显着的复合年增长率成长

- 最终用户行业的快速扩张以及结构安全监控系统应用的主要途径正在推动该地区的市场扩张。例如,据世界核能协会称,亚太地区的发电能力,尤其是核能正在经历显着成长。该地区约有 135 座运作中的核子反应炉,约有 35 座在建。因此,这些发电厂的维护需求也将增加,进而创造结构监测市场。

- 基础设施监控设备在航太和国防领域的应用正在进一步推动市场的发展。例如,根据斯德哥尔摩国际和平研究所(SIPRI)的数据,中国和印度去年都增加了核武库。瑞典智库指出,中国正大力现代化其核武库。根据斯德哥尔摩国际和平研究所2022年年鑑,截至2022年1月,中国、巴基斯坦和印度的核弹头数量分别为350枚、165枚和160枚。它们的存在表明有必要对核武进行监视,以确保它们不会落入坏人之手。

- 而且随着智慧城市的发展,中国推出了700多个创新城市计划,覆盖了大大小小的城市。在中国「十四五」规划(2021-2025年)中,智慧城市发展理念已被纳入几乎所有省区的发展目标。随着中国都市化进程的加快,智慧城市作为国内城市发展的现实需求,已成为城市资讯化的新浪潮。

- 此外,中国基础设施老化现像日益严重,利用基础设施监测服务来识别这些结构并确保其完整性势在必行。因此,由于对进行定期评估以保护老化基础设施的需求日益增加,以及对优化基础设施成本的需求日益增加,预计预测期内此类解决方案在该国的采用将蓬勃发展。

- 此外,智慧城市计划的扩张预计将为该国市场提供成长机会。例如,在印度,智慧城市任务预计于 2023 年结束。印度总理莫迪于 2015 年 6 月宣布了这项倡议,中央政府选择了印度全国 100 个城市参与。这些城市将采用智慧解决方案进行开发,为其公民提供核心基础设施、健康、永续的环境和体面的生活水准。该任务的实施时间表已延长至 2023 年 6 月,这使得 2023 年成为印度智慧城市的关键一年。

基础设施监控产业概况

基础设施监控市场的竞争格局仍然分散,只有几位家中小型参与者。最终用户群体不断变化的需求正在推动市场供应商提供创新产品。此外,市场的成长机会正在吸引新的参与者和投资进入市场。

- 2022 年 9 月-Equinor 和挪威科技公司 Vissim 已完成为挪威和英国大陆棚的能源营运商开发新的增强式海上空间监视系统。新的增强型海上空间监视系统融合了海底基础设施监控、具有天气预报和即时监控的海上规划以及 3D情境察觉功能。

- 2022 年 1 月-Netreo 宣布其全端IT基础设施监控解决方案「Netreo」及其全生命週期 APM 解决方案「Retrace by Netreo」已通过 Veracode 验证标准认证,证明其程式码开发流程符合 AppSec 最佳实践,进一步加强了「Netreo」和「Retrace by Netreo」的安全态势。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 产业影响评估

第五章 市场动态

- 市场驱动因素

- 能源和民用基础设施等终端用户产业将推动成长

- 先进感测器技术简介

- 市场限制

- 高成本

第六章 市场细分

- 依技术分类

- 有线

- 无线的

- 按服务

- 硬体

- 软体和服务

- 按最终用户产业

- 矿业

- 航太和国防

- 民用基础设施

- 活力

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- National Instruments Corporation

- Campbell Scientific Inc. Company

- Pure Technologies Ltd Company(Xylem Inc.)

- Structural Monitoring Systems plc

- Acellent Technologies Inc.

- Geocomp Corporation

- Geokon Inc.

- SISGEO SRL

- AVT Reliability Company(AES Engineering Ltd)

第八章投资分析

第九章:未来展望

The Infrastructure Monitoring Market size is estimated at USD 7.95 billion in 2025, and is expected to reach USD 12.86 billion by 2030, at a CAGR of 10.1% during the forecast period (2025-2030).

Key Highlights

- The growing use of advanced sensor technologies, declining cost of sensors, growing demand for preventive maintenance, and increasing capital investments to ensure better maintenance of critical infrastructure across the end-user industries are driving the growth of the infrastructure monitoring market.

- The growing demand for predictive maintenance to reduce life cycle maintenance costs is one of the primary drivers of this industry. The MEMS (Micro electro mechanical systems) inertial sensors are extensively used in predictive condition monitoring of buildings, production systems, and even vehicles. This has been further augmented by the emergence of IoT and advanced analytics that continually improve such systems' functionality.

- In February 2022, New Relic, the observability company, declared the general availability of a new infrastructure monitoring experience especially to empower SRE, DevOps, and ITOps teams to proactively resolve and identify issues in their private, public, and hybrid cloud infrastructure. The modernized experience mainly enables engineers to instantly isolate bottlenecks by sorting and filtering based on key golden signal conditions, analyze all related telemetry (including events, logs, network, alerts, etc.) in context, visualize blast radius with topology maps and perform historical analysis to understand the various cascading impacts.

- Moreover, the ability to remotely monitor critical infrastructure using smart sensors has led to the proliferation of the market. This is extremely helpful in the end-user segments, like mining, where structural monitoring using smart sensors enables companies to save money and lives. Inertial sensors from First Sensor that can achieve resolutions of 10 µg or 0.0005° (2 arc seconds) are extensively used for remote monitoring of buildings, bridges, and wind turbines.

- Ground-penetrating radar (GPR) is also growing in importance because of its cost advantages. It is increasingly being used for bridge and tunnel inspections, roadway investigations, and to ensure adequately compacted asphalt on roads. For instance, by utilizing the GPR technology, Kentucky Transportation Center found the location of large voids in the Cumberland Gap Tunnel, which links Kentucky and Tennessee. It also significantly reduced the repair costs by using GPR to confirm that no voids needed to be fixed on one end of the tunnel.

- However, the high-cost involvement, especially in implementation and deployment, might be a significant matter of concern that can hamper the overall market's growth throughout the forecast period.

- During the COVID-19 pandemic, the companies operating in the Infrastructure Monitoring market faced temporary operative issues due to the absence of site access and disruption in the supply chain, which negatively affected the market's growth. Various associations, including those that provide multiple certifications, have also taken a hit. However, companies such as Bureau Veritas reported a 900% rise in demand for the remote inspection of offshore assets and equipment since the pandemic outbreak.

Infrastructure Monitoring Market Trends

Energy Sector is Expected to Account for a Significant Share of the Market

- The energy segment is anticipated to get significant traction in the infrastructure monitoring market owing to the increasing demand for improving energy efficiency, sustainability, and cost-effective practices. Additionally, the growing importance of timely and predictive maintenance for energy sector assets provides a promising future for the growth of infrastructure monitoring in the energy sector.

- Further, the remote maintenance benefits that the Structural Health Monitoring Systems offer is extremely beneficial for both onshore and offshore systems in this sector. In a wind turbine, for instance, central data modules are being increasingly used to transmit data related to various structural conditions. Moreover, the introduction of cloud solutions has enabled this structural health monitoring data to be continually collected and evaluated for predictive maintenance. Most wind farm operators leverage Supervisory control and data acquisition (SCADA) data for remote monitoring and management.

- Moreover, Structural Health Monitoring solutions led to substantial cost savings through early detection, thereby facilitating higher investment in future predictive maintenance solutions. Duke Energy deployed Schneider Electric's Avantis PRiSM technology to save over USD 7.5 million through early crack detection in a turbine rotor. This has ensured the prevention of cost overruns through asset optimization and maintenance.

- In addition, non-invasive structural monitoring remains highly critical to the nuclear energy sector, which, by design, supports such technologies. The sensors in nuclear reactors are installed during concrete casting or by inserting them into holes that are drilled into the existing structures. Hence it requires monitoring and maintenance, especially for proper functioning and operations, thereby facilitating the market's growth significantly.

- Moreover, as per World Nuclear Association, as of May 2022, globally, there were 95 nuclear reactors planned worldwide. China recorded the largest figure with 33 units., followed by Russia and India with 27 and 12. Further, as nuclear power plants age, maintenance's importance increases, which is expected to create market opportunities for the market studied.

Asia-Pacific is Anticipated to Grow at a Significant CAGR

- The rapid expansion of the end-user industries that have major avenues for the application of structural health monitoring systems is leading to the expansion of the market in the region. For instance, according to World Nuclear Association, the Asia-Pacific region is witnessing significant growth in terms of electricity generating capacity and specifically nuclear power. The region is home to about 135 operable nuclear power reactors, and about 35 are under construction, with the fastest growth in nuclear generation expected in China. Thus, the need for maintenance of those power plants will also increase, which in return will create a market for structural monitoring.

- The application of infrastructure monitoring equipment within Aerospace and Defense is further driving the market. For instance, according to the Stockholm International Peace Research Institute (SIPRI), China and India have enhanced their nuclear arsenal over the last year. The Swedish think-tank pointed out that China is significantly modernizing its nuclear arsenal. According to the SIPRI Yearbook 2022, as of January 2022, China, Pakistan, and India have 350 165 and 160 nuclear warheads, respectively. Such existence mandates the need to monitor them so that they don't fall into the wrong hands.

- Further, with the development of smart cities, China has established more than 700 innovative city projects in more than 500 cities, covering big and small cities. The concept of smart city development has been incorporated in the 14th Five Year Plan (2021 to 2025) development goals of nearly all Chinese provinces and regions. With the acceleration of urbanization in China, smart city, as the internal realistic demand of urban development, has become the new wave of urban informatization.

- Moreover, there has been an increased count of aging infrastructure in China, making it essential for the usage of infrastructure monitoring services to identify and secure the integrity of these structures. As a result, the deployment of these solutions in the country is expected to grow rapidly over the forecast period due to the increasing need to conduct periodical assessment operations to preserve aging infrastructure and the need to optimize infrastructure expenses.

- Additionally, growing smart city projects are expected to provide opportunities for the growth of the market in the country. For instance, In India, The Smart City Mission is scheduled to be finished in 2023. Prime Minister Narendra Modi declared the initiative back in June 2015, and the Centre chose 100 cities from across India to participate. These cities will be developed to provide citizens with access to core infrastructure, a healthy and sustainable environment, and a decent standard of living using smart solutions. The mission's implementation timeline was extended till June 2023, making 2023 one of the most important years for India's Smart Cities.

Infrastructure Monitoring Industry Overview

The competitive landscape of the infrastructure monitoring market remains fragmented, with several small and medium-sized players operating in the market. The evolving needs of the end-user segments are driving the market vendors to offer innovative products. In addition, growing opportunities in the market are attracting new players and investments in the market.

- September 2022 - Equinor and Norwegian technology Vissim have completed the development of a new and expanded ocean space surveillance system for energy operators on the Norwegian and UK continental shelves. The new and expanded ocean space surveillance system incorporates subsea infrastructure monitoring, marine planning through weather forecasts and real-time monitoring, and 3D situational awareness.

- January 2022 - Netreo announced that both the Netreo full-stack IT infrastructure monitoring and Retrace by Netreo full lifecycle APM solutions earned Veracode Verified Standard recognition proving that code development processes meet AppSec best practices and further boosting the security posture of the Netreo and Retrace by Netreo solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Covid-19 on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The End-user Segments like Energy and Civil Infrastructure will Drive Growth

- 5.1.2 Introduction of Advanced Sensor Technologies

- 5.2 Market Restraints

- 5.2.1 High Cost of Implementation and Deployment

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Wired

- 6.1.2 Wireless

- 6.2 By Offering

- 6.2.1 Hardware

- 6.2.2 Software and Services

- 6.3 By End-user Industry

- 6.3.1 Mining

- 6.3.2 Aerospace and Defense

- 6.3.3 Civil Infrastructure

- 6.3.4 Energy

- 6.3.5 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 National Instruments Corporation

- 7.1.2 Campbell Scientific Inc. Company

- 7.1.3 Pure Technologies Ltd Company (Xylem Inc.)

- 7.1.4 Structural Monitoring Systems plc

- 7.1.5 Acellent Technologies Inc.

- 7.1.6 Geocomp Corporation

- 7.1.7 Geokon Inc.

- 7.1.8 SISGEO SRL

- 7.1.9 AVT Reliability Company (AES Engineering Ltd)

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK

基础设施监控市场:按类型、组件、技术和最终用户产业划分-2026-2032年全球市场预测

基础设施监控市场:按类型、组件、技术和最终用户产业划分-2026-2032年全球市场预测 2026年全球基础设施监测市场报告无线起重机监控系统市场:按组件、部署类型、设备类型、连接技术、监控类型、计划规模、应用、最终用户划分,全球预测,2026-2032年

2026年全球基础设施监测市场报告无线起重机监控系统市场:按组件、部署类型、设备类型、连接技术、监控类型、计划规模、应用、最终用户划分,全球预测,2026-2032年 基础设施监控市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及解决方案划分

基础设施监控市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及解决方案划分 基础设施监控市场-全球产业规模、份额、趋势、机会及预测(按组件、技术、应用、垂直产业、地区和竞争格局划分,2021-2031年)

基础设施监控市场-全球产业规模、份额、趋势、机会及预测(按组件、技术、应用、垂直产业、地区和竞争格局划分,2021-2031年) 基础设施监测市场-2026-2031年预测

基础设施监测市场-2026-2031年预测 基础设施监控市场规模、份额和成长分析(按组件、技术、应用、垂直产业和地区划分)-2026-2033年产业预测

基础设施监控市场规模、份额和成长分析(按组件、技术、应用、垂直产业和地区划分)-2026-2033年产业预测 无线状态监测系统市场规模、份额和趋势分析报告:按组件、监测技术、连接类型、部署方式、最终用途、地区和细分市场预测(2025-2033 年)

无线状态监测系统市场规模、份额和趋势分析报告:按组件、监测技术、连接类型、部署方式、最终用途、地区和细分市场预测(2025-2033 年) 中国无线基础设施(2025 年 7 月):中国凭藉其经济和 5G 超级大国的地位,正在部署 5G-A(5G-Advanced),为新的国家重点发展项目 6G 奠定基础。智慧基础设施监控市场规模、份额、趋势分析报告:按组件、部署、行业垂直、应用、地区和细分市场预测,2025 年至 2030 年

中国无线基础设施(2025 年 7 月):中国凭藉其经济和 5G 超级大国的地位,正在部署 5G-A(5G-Advanced),为新的国家重点发展项目 6G 奠定基础。智慧基础设施监控市场规模、份额、趋势分析报告:按组件、部署、行业垂直、应用、地区和细分市场预测,2025 年至 2030 年