|

市场调查报告书

商品编码

1644298

通讯管理系统:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Correspondence Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

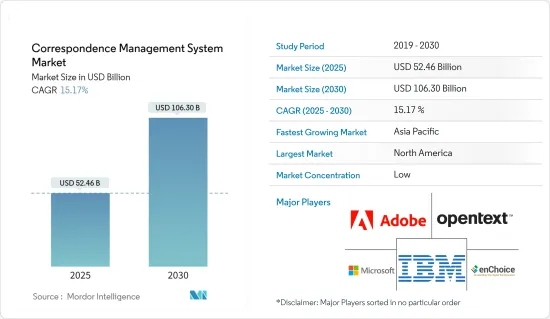

通讯管理系统市场规模预计在 2025 年为 524.6 亿美元,预计到 2030 年将达到 1063.0 亿美元,预测期内(2025-2030 年)的复合年增长率为 15.17%。

CMS 中技术采用趋势的上升,例如 CMS 中对 AI 的需求上升、基于语音的搜寻优化的使用增加以及内容管理中聊天机器人的使用增加,是预计在预测期内推动市场增长的一些因素。

主要亮点

- 自动化刺激了通信管理系统的选择,特别是在遵循基于规则的流程的企业中,减少了业务环境中的不一致性并终止通信,从而实现了高效的内部和外部通信系统。

- 由于全球各组织越来越多地采用数位化工作文化以及产业内容的扩展,通讯管理系统市场正在全球迅速扩张。此外,巨量资料和分析解决方案的发展正在提高内部和外部通讯的自动化程度。此外,企业正在迅速转向即时通讯系统来有效管理所有通讯。

- 此外,随着云端基础的技术的出现和业务数位化的日益发展,企业经常转向邮件室自动化来实现其内部和外部业务沟通流程的自动化。这使得企业能够根据通讯的内容、外观和类别对其进行分类,然后将其发送给适当的部门或个人。

- 此外,通讯管理系统可实现自动化,提供速度和灵活性,从而更好地洞察客户和内部业务。企业正在实施数位转型以更快地满足客户需求。透过定期沟通让股东和消费者了解情况可以帮助公司增加收益并提高采用率。巨量资料和进阶分析等新 IT 应用和基础设施的采用也是推动通讯管理系统市场成长的因素之一。此外,企业还可以利用具有预测能力的通讯管理系统解决方案,利用巨量资料来改善决策。

- 然而,限制和约束市场成长的挑战包括资料孤立、资料整合平台不同以及缺乏技术能力。

- COVID-19 对依赖客户互动的企业产生了深远的影响。数位化转换、互动性和收益成长现在比以往任何时候都更加重要。因此,许多企业将内容管理系统和数位体验平台(管理线上体验的平台)视为关键任务软体。

- 投资、管理和营运这些平台的个人需要重新评估他们的平台需求,并确保他们的 CMS 能够跟上延长的 WFH、增加的网路流量和不断变化的行销策略。此外,借助具有生产力、协作、效能和安全性等功能的现代云端託管 CMS,将大大减轻由于 COVID-19 导致的业务需求增加、紧迫的期限和增加的行销需求所带来的负担。

通讯管理系统市场趋势

便利、安全的内部和外部通讯推动市场成长

- 内容管理系统旨在供所有人存取。这些程式通常具有用户友好的介面并且易于操作。不需要技术或程式设计知识,但根据 CMS 平台可能需要一些协助和专业知识。这些独特的优势正是推动 CMS 采用率成长的动力。

- 私人、个人化、互动性强的商业文件的开发、编辑和分发透过通讯管理系统进行集中管理。该技术使公司能够透过从製作到归檔的简化流程,使用预先核准或自订的材料快速创建通信,从而提高客户的便利性。

- 从而,客户能够快速、准确、简单、安全且适当地收到正确的讯息。这使企业能够最大限度地提高消费者互动的价值,同时降低与复杂流程相关的成本和风险,有助于推动市场成长。

- 此外,Storyblok 进行的一项调查发现,2023 年最大量使用 CMS 的团队将是行销团队(17%),紧随其后的是销售团队(17%)和财务团队(15%)。设计团队(7%)和高阶主管(6%)是最不可能使用企业 CMS 的两个团队。如此显着的采用率可能意味着 CMS 技术提供的便利性和安全性正在促进跨组织内部和外部沟通的有效性。

北美占据主要市场占有率

- 由于零售、电子商务、垂直行业和政府组织等各个垂直行业对自动化的应用日益广泛,以及对有效的内部和外部沟通以提高保留率的需求日益增加,北美占据了主要的市场占有率。北美最大的两个市场—美国和加拿大,正在见证通讯管理系统解决方案等先进技术的采用。

- 例如,据微软称,由于自动化和简化的协作,该地区的时间和资源管理变得更加有效和富有成效。例如,美国透过简化任务管理和部门与团队之间的沟通,每年节省了近 140 万美元。

- 预计企业将在 IT 和电讯等关键产业中广泛使用通讯管理系统,以防止手动业务流程中断。信函管理系统可以有效管理、搜寻、追踪和报告信函和行动计划。预计各新兴产业间日益增多的通讯交流将推动整个全部区域CMS 供应商的崛起。

- 该地区着名的国际通讯管理系统供应商包括 IBM、Microsoft、Adobe、Open Text、Pitney Bowes、Micropact、Xerox 和 Top Down Systems。这些大公司的存在是该全部区域产生可观收益的主要原因。

通讯管理系统产业概况

通讯管理系统市场竞争适中,由几个主要参与者组成。全球主要供应商包括 IBM Corporation、Microsoft Corporation、OpenText Corporation 和 Adobe, Inc.服务供应商正尝试透过与软体公司合作、提供端到端解决方案以及充当通讯管理解决方案一站式商店的解决方案方式进入市场。目前,通讯管理系统市场中的参与者正在以实惠的价格提供各种云端基础的解决方案,预计将为提供这些系统的公司创造巨大的商机。

- 2023 年 2 月-数位文件和合约生命週期管理公司 SignDesk 与微软和 G7 CR Technologies 合作,以增强公司的云端部署能力。透过这种合作关係,企业将能够利用与 SignDesk 产品套件整合的 Microsoft Azure 的功能。 SignDesk 文件自动化套件也将在 Microsoft Marketplace 上亮相。产品组合中的解决方案解决数位化入职、合约生命週期管理和数位化文件执行等问题。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 对通讯系统自动化和个人化的需求日益增加

- 方便、安全的内部和外部通信

- 市场限制

- 由于卖家资料和资料系统脱节,缺乏技术专业知识影响资料集成

- 初期投资高且缺乏认知

第六章 市场细分

- 按组件

- 软体

- 按服务

- 按分销管道

- 基于网路

- 基于电子邮件

- 其他交付管道(基于 SMS/MMS 等)

- 按部署模型

- 本地

- 云

- 按组织规模

- 中小型企业

- 大型企业

- 按行业

- BFSI

- 政府及公共机构

- 电信和 IT

- 卫生保健

- 零售与电子商务

- 其他行业

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- IBM Corporation

- Adobe Inc.

- Microsoft Corporation

- OpenText Corporation

- Rosslyn Data Technologies Inc.(enChoice, Inc.)

- Pitney Bowes Inc.

- Newgen Software Technologies Limited

- Fabasoft AG

- MicroPact Inc.

- Everteam SAS

- Ademero, Inc.

- Blue Project Software Inc.

- Xerox Holdings Corporation

- Palaxo International Ltd.

- Top Down Systems Corporation

- Harvest Technology Group

第八章投资分析

第九章 市场机会与未来趋势

The Correspondence Management System Market size is estimated at USD 52.46 billion in 2025, and is expected to reach USD 106.30 billion by 2030, at a CAGR of 15.17% during the forecast period (2025-2030).

The rising trends of technology adoption in CMS, such as rising demand for AI in CMS, increasing use of Voice-based search optimization, and rising chatbot usage for content management, are a few factors anticipated to drive the market growth during the forecast period.

Key Highlights

- Automation stimulates the selection of a correspondence management system, especially for businesses that follow rule-based processes, diminishing inconsistencies and terminating correspondences in the business environment, thereby allowing efficient internal and external communication systems.

- The correspondence management system market is expanding rapidly on a global scale due to the rise in the adoption of a digital working culture in organizations worldwide and the expansion of content in industries. In addition, developing big data and analytics solutions has increased internal and external communication automation. Additionally, businesses are fast using real-time communication systems to manage all correspondences effectively.

- Moreover, businesses frequently use mailroom automation to automate their internal and external business communication processes as a result of the emergence of cloud-based technologies and the growing digitalization of businesses. This helps businesses to classify their incoming correspondence according to its content, appearance, and category and send it to the appropriate department or individual.

- Further, a correspondence management system automates, providing speed and agility to generate superior customer and internal affairs insights. Organizations are using digital transformation to satisfy client demands more quickly. By keeping shareholders and consumers informed through regular contact, the solutions allow businesses to increase revenues, which raises the adoption rate. Introducing new IT applications and infrastructure, such as big data and sophisticated analytics, is another driver fueling the market's growth for correspondence management systems. Additionally, businesses may use big data to improve decision-making with solutions for a correspondence management system that has predictive capabilities.

- However, some challenges limiting and constraining the market's growth include segregated data, different platforms for data integration, and a lack of technical competence.

- COVID-19 has severely impacted businesses relying on customer interaction to generate income. Conversion, interactivity, and revenue growth through digital are being prioritized more than ever. As a result, many organizations view content management systems and digital experience platforms-platforms that govern online experiences-as mission-critical software.

- Individuals investing in, administering, and operating on these platforms need to reassess their platform needs and ensure their CMS can sustain them during prolonged WFH periods, more internet traffic, and changing marketing strategies. Moreover, the strain of increasing business requirements, tight deadlines, and increased marketing demands due to COVID-19 significantly lessened with the help of a contemporary cloud-hosted CMS with features surrounding productivity, collaboration, performance, and security.

Correspondence Management System Market Trends

Convenient and Secured Internal and External Communications to Drive the Market Growth

- Content management systems are intended to be used by everyone. The program typically has a user-friendly interface and is simple to navigate. While no technical or programming knowledge is necessary, some CMS platforms can require some assistance or expertise. Such characteristic benefits are factors responsible for the growth of CMS adoption.

- The development, compilation, and distribution of private, personalized, and interactive business correspondences are centralized and managed by correspondence management systems. The technology allows businesses to rapidly create communication using pre-approved and custom-written material in a simplified process from production to archive, thereby enhancing convenience to the clients.

- As a result, clients receive the appropriate message quickly, accurately, easily, securely, and relevantly. This enables companies to lower costs and risks related to a complicated process while maximizing the value of consumer interactions, thereby driving market growth.

- Moreover, according to a survey conducted by Storyblok, in 2023, the team that used the CMS most frequently was marketing, with 17%, closely followed by sales, 17%, and finance, 15%. Design teams and executives, with 7% and 6%, respectively, were the two teams that were least likely to use a company's CMS. Such significant adoption rates might signify the convenience and security offered by the CMS technology driving the effectiveness of internal and external communication across the organization.

North America to Hold Significant Market Share

- North America accounts for one of the significant market shares due to the growing use of automation and the increasing demand for effective internal and external communication for improved retention in several business verticals, such as retail and eCommerce, BFSI, and government. The adoption of advanced technology, such as solutions for correspondence management systems, has been increasing in the two strongest markets in North America: the United States and Canada.

- For instance, according to Microsoft Corporation, automation and simplified collaboration in the region make time and resource management more effective and productive. For example, the United States Air Force significantly saved nearly USD 1.4 million yearly by streamlining task management and communication among departments and teams.

- Businesses are expected to use the correspondence management system significantly to prevent manual business procedures from disrupting operations in crucial industry verticals like IT & telecom. The correspondence management system effectively maintains, searches, tracks, and reports correspondence and action plans. The rising communication exchange across various emerging industries are expected to create CMS vendors across the region.

- The region's prominent international providers of correspondence management systems include IBM, Microsoft, Adobe, OpenText, Pitney Bowes, MicroPact, Xerox, and Top Down Systems. The presence of such large enterprises are primarily responsible for the considerable revenue generation across the region.

Correspondence Management System Industry Overview

The Correspondence Management System Market is moderately competitive and consists of several major players. Some of the key providers across the globe include IBM Corporation, Microsoft Corporation, OpenText Corporation, and Adobe, Inc., among others. The Service Providers are trying to go to the market through a solution approach by tying up with software houses, providing it as an end-to-end solution, and behaving like a one-stop-shop for the correspondence management solution. The players operating in the correspondence management system market are now offering various cloud-based solutions at affordable prices, which are expected to provide considerable opportunities to the companies providing these systems.

- February 2023 - SignDesk, a digital documents and contract lifecycle management player, partnered with Microsoft and G7 CR Technologies to enhance the company's cloud deployment capabilities. Through this relationship, businesses can use the Microsoft Azure features integrated with the SignDesk suite of products. The document automation suite from Sign Desk will also be featured in the Microsoft marketplace. The solutions in this portfolio address digital onboarding, contract lifecycle management, and digital document execution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Need for Automating and Personalizing Communication Systems

- 5.1.2 Convenient and Secured Internal and External Communications

- 5.2 Market Restraints

- 5.2.1 Cellar Data and Disparate Data Systems Impacting Data Integration augmented by Lack of Technical Expertise

- 5.2.2 Higher Initial Investments and Lack of Awareness

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Delivery Channel

- 6.2.1 Web-based

- 6.2.2 Email-based

- 6.2.3 Other Delivery Channels (SMS/MMS-based, etc.)

- 6.3 By Deployment Model

- 6.3.1 On-Premises

- 6.3.2 Cloud

- 6.4 By Organization Size

- 6.4.1 Small & Medium Enterprises

- 6.4.2 Large Enterprises

- 6.5 By Industry Vertical

- 6.5.1 BFSI

- 6.5.2 Government & Public Sector

- 6.5.3 Telecom & IT

- 6.5.4 Healthcare

- 6.5.5 Retail & E-commerce

- 6.5.6 Other Industry Verticals

- 6.6 Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia Pacific

- 6.6.4 Latin America

- 6.6.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Adobe Inc.

- 7.1.3 Microsoft Corporation

- 7.1.4 OpenText Corporation

- 7.1.5 Rosslyn Data Technologies Inc. (enChoice, Inc.)

- 7.1.6 Pitney Bowes Inc.

- 7.1.7 Newgen Software Technologies Limited

- 7.1.8 Fabasoft AG

- 7.1.9 MicroPact Inc.

- 7.1.10 Everteam SAS

- 7.1.11 Ademero, Inc.

- 7.1.12 Blue Project Software Inc.

- 7.1.13 Xerox Holdings Corporation

- 7.1.14 Palaxo International Ltd.

- 7.1.15 Top Down Systems Corporation

- 7.1.16 Harvest Technology Group

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026年全球数位饭店市场报告

2026年全球数位饭店市场报告 中央厨房管理软体市场按产品类型、功能和最终用户划分,全球预测(2026-2032)

中央厨房管理软体市场按产品类型、功能和最终用户划分,全球预测(2026-2032) 全球笔记管理软体市场规模、份额、趋势和成长分析报告(2026-2034)社会工作个案管理软体全球市场报告(2026年)

全球笔记管理软体市场规模、份额、趋势和成长分析报告(2026-2034)社会工作个案管理软体全球市场报告(2026年) 休閒管理软体市场-全球产业规模、份额、趋势、机会及预测(依设施类型、部署方式、最终用途、地区及竞争格局划分,2021-2031年)伺服器管理软体市场 - 全球产业规模、份额、趋势、机会、预测:按部署方式、组织规模、垂直市场、地区和竞争格局划分,2021-2031 年供应商关係管理软体市场 - 全球产业规模、份额、趋势、机会、预测(按部署模式、公司规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)中小企业的条码库存管理软体:2026-2032 年全球预测(按部署类型、公司规模、定价模式、整合、平台、设备类型、应用程式和垂直产业划分)全球一体化特许经营管理软体市场:按公司规模、定价模式、部署类型、应用程式、最终用户和分销管道划分 - 2026-2032 年预测医疗设备软体检验市场(依影像设备、监测设备、治疗设备和手术设备划分),全球预测,2026-2032年

休閒管理软体市场-全球产业规模、份额、趋势、机会及预测(依设施类型、部署方式、最终用途、地区及竞争格局划分,2021-2031年)伺服器管理软体市场 - 全球产业规模、份额、趋势、机会、预测:按部署方式、组织规模、垂直市场、地区和竞争格局划分,2021-2031 年供应商关係管理软体市场 - 全球产业规模、份额、趋势、机会、预测(按部署模式、公司规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)中小企业的条码库存管理软体:2026-2032 年全球预测(按部署类型、公司规模、定价模式、整合、平台、设备类型、应用程式和垂直产业划分)全球一体化特许经营管理软体市场:按公司规模、定价模式、部署类型、应用程式、最终用户和分销管道划分 - 2026-2032 年预测医疗设备软体检验市场(依影像设备、监测设备、治疗设备和手术设备划分),全球预测,2026-2032年