|

市场调查报告书

商品编码

1644357

资料历史学家:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Data Historian - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

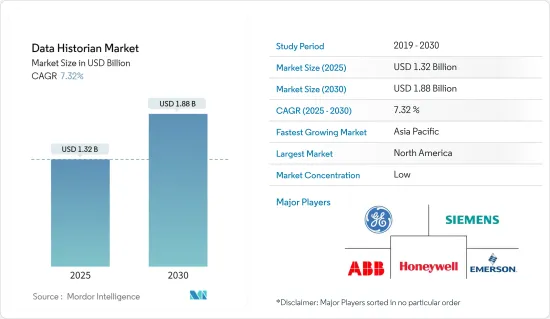

资料历史学家市场规模预计在 2025 年为 13.2 亿美元,预计到 2030 年将达到 18.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.32%。

物联网设备、云端应用程式和社交媒体等各种来源产生的资料量不断增加,推动了对资料历史学家的需求。

主要亮点

- 许多行业都有监管和合规要求,要求保留历史资料。资料历史学家提供了一种满足这些要求的方法,同时使组织能够从资料中获得见解。这对于金融服务等产业尤其重要。因此,这些行业的需求正在促进市场发展。

- 资料中心的成长提供了储存、处理和分析大量资料所需的基础设施,从而推动了资料历史学家的成长。此外,资料中心通常提供先进的处理功能,例如高效能运算资源和资料分析工具,以帮助企业从资料中提取有价值的见解和趋势。

- 因此,对资料中心的投资正在快速增加,以支持市场成长。资料历史学家在资料中心和工业控制系统(ICS)中最为常见。例如,根据印度NASSCOM的数据,印度资料中心投资预计将从2021年的38亿美元成长到2025年的46亿美元。

- 此外,随着工业 4.0、智慧工厂和智慧工厂的出现,世界各地的组织正在转向在其流程的多个层面使用大量资料。这增加了组织对资料历史解决方案的需求,以实现有效的管理、稳定且有效率的工厂运作和强大的分析。然而,资料能力和复杂性不断增加、实施成本高以及发展有限等因素阻碍了市场成长。

- COVID-19 对资料历史资料库市场产生了多种影响。资料产生的激增,加上对资料储存和分析的需求增加,导致对资料历史解决方案的需求增加。这为专门从事资料历史技术和服务的公司提供了成长机会。

- 此外,疫情也扰乱了企业和全球经济,减缓了对资料历史学家等新技术的支出。结果,资料历史资料库市场的成长放缓。此外,远距工作的转变为资料收集和管理带来了挑战,使得资料历史学家更难以提供准确和完整的资料历史。

资料历史学家市场的趋势

云端部署推动市场成长

- 云端部署的扩展是资料历史学家成长的主要驱动力。云端运算发展的进步提供了能够处理大量资料的可扩展、灵活的云端基础设施,使其成为资料历史学家的理想选择。此外,云端运算的发展使得资料历史学家与其他云端基础的工具和服务(如资料分析和视觉化)的整合变得更加容易,从而产生了对资料历史学家的需求。

- 云端部署的成长推动了采用云端服务来储存和管理消费者资料。付款闸道、线上资金转帐、数位钱包和统一客户体验等服务在 BFSI 行业中发挥着至关重要的作用,有助于全面转向云端部署。

- 2022 年 6 月,Eros Investments(由 Eros Media World、Eros Now 和 Xfinite 的 Mzaalo 组成的媒体、娱乐和技术企业投资组合)与 Wipro 签署了一项协议,以发展和扩展其基于人工智慧 (AI) 和机器学习 (ML) 的内容在地化解决方案。 Eros Investments 和 Wipro 联合提供的内容在地化服务将透过两种部署模式(平台即服务和私有云端部署)提供给媒体和娱乐公司。各行业的公司在云端部署领域利用解决方案的努力预计将进一步推动市场成长。

- 此外,云端部署允许资料史学家根据客户需求的变化轻鬆扩展其基础设施,透过消除对昂贵硬体的需求来降低资料历史学家的整体拥有成本。这使得即使是中小型企业也可以更轻鬆地使用资料历史学家。

- 自疫情爆发以来,许多企业对云端处理的需求激增。云端服务随着条件的变化提高基础设施效率、降低营运成本并优化业务运营,从而产生了各种云端部署模型。

预计北美将占据最大市场占有率

- 由于资料历史资料库市场创新研发支出的增加,北美预计将占据最高的市场占有率。此外,该地区还有霍尼韦尔国际公司、通用电气公司和罗克韦尔自动化公司等供应商持续向市场投资。

- 由于对工业自动化资料的需求不断增长以提高性能,巨量资料分析在各个经济部门的使用日益广泛,不断扩展的物联网基础设施产生越来越多的可收集和分析的资料,以及其他技术市场趋势,该地区对数据历史学家的需求正在稳步增长。

- 该地区也为 IT、BFSI、零售和医疗保健行业的全球资料中心需求做出了重大贡献。 CBRE等房地产专家报告称,美国占据了全球近90%的资料中心空间。这进一步推动了资料史学家市场的需求。

- 例如,Google过去5年已在美国26个州投资超过370亿美元设立办公室和资料中心,加上2020年和2021年将在美国投资超过400亿美元的研发费用。此外,2022年4月,Google宣布计划在2022年美国办事处和资料中心投资约95亿美元。

- 此外,北美组织越来越认识到资料分析在决策中的价值,并正在寻求管理和储存大量资料的解决方案。这推动了对资料历史学家的需求。

资料历史学家产业概况

资料历史资料库市场参与者众多,因此市场较分散。为了占据最高的市场占有率,市场参与者正在采取伙伴关係、併购、新产品发布和投资研发以进一步创新等策略。市场的主要发展包括: 2022 年 10 月,Uptake Technologies Inc. 与 ADX 团队合作,使用 ADX 建构了工业资料历史学家。自从微软决定停止开发时间序列洞察 (TSI) 以来,Uptake 一直致力于将其旗舰 OT 云端资料历史产品 Fusion 重新平台化到 Azure 资料资源管理器 (ADX)。 2022 年 4 月,GE Digital 宣布在 AWS Marketplace 上推出全球首个云端原生营运资料历史学家 Proficy Historian for Cloud。这款云端基础的工业资料管理软体旨在使从设备级到企业的 OT资料到云端的转换更简单、更可靠。 Proficy Historian for Cloud 可协助公司利用现有的 IT 云端投资并将 OT资料与企业资料结合。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 对流程和效能改进的整合资料的需求不断增加

- 工业巨量资料的兴起

- 市场挑战

- 实施成本高

第六章 市场细分

- 按组件

- 软体

- 服务

- 依部署方式

- 本地

- 云

- 按最终用户产业

- 资料中心

- 石油和天然气

- 纸和纸浆

- 水资源管理

- 製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争格局

- 公司简介

- General Electric Company

- Siemens AG

- ABB

- Honeywell International Inc.

- Emerson Electric Co.

- AVEVA Group plc

- Rockwell Automation Inc.

- OSIsoft LLC

- ICONICS

- Open Automation Software

第八章投资分析

第九章:市场的未来

The Data Historian Market size is estimated at USD 1.32 billion in 2025, and is expected to reach USD 1.88 billion by 2030, at a CAGR of 7.32% during the forecast period (2025-2030).

The increasing amount of data generated by various sources, such as IoT devices, cloud applications, and social media, is driving demand for data historians.

Key Highlights

- Many industries are subject to regulations and compliance requirements that require storing historical data. Data historians provide a way to meet these requirements while enabling organizations to extract insights from the data. This is particularly important in the industries such as financial services. Thus, demand from such sectors is contributing to the market.

- The growth of data centers facilitates the growth of data historians by providing the infrastructure necessary for storing, processing, and analyzing large amounts of data. Further, data centers often offer advanced processing capabilities, such as high-performance computing resources and data analytics tools, which can help organizations extract valuable insights and trends in their data.

- As a result, investment in data centers is rising rapidly and supporting market growth, as data historians are most common in data centers and industrial control systems (ICS). For instance, according to NASSCOM (India), the investment value in data centers in India is expected to reach USD 4.6 billion by 2025 from USD 3.8 billion in 2021.

- Moreover, with the advent of Industry 4.0, smart factories, and smart plants, organizations worldwide are demonstrating a shift to the usage of massive amounts of data at several layers of their process. This leads to organizations' growing demand for data historian solutions to achieve effective management, stable and efficient plant operations, and robust analysis. However, factors such as increasing data capabilities and complexities, high deployment costs, and limited development are stifling market growth.

- COVID-19 had a mixed impact on the data historian market. The increased demand for data storage and analysis due to the surge in data generation led to an increased demand for data historian solutions. This provided growth opportunities for companies specializing in data historian technology and services.

- Furthermore, the pandemic has also disrupted businesses and the global economy, causing a slowdown in spending on new technologies, including data historians. This has resulted in a slowdown in the growth of the data historian market. Additionally, the shift to remote work has caused data collection and management challenges, making it more difficult for data historians to provide accurate and complete data history.

Data Historian Market Trends

Cloud Deployment To Drive the Market Growth

- The growth in cloud deployment has been a key factor in the growth of data historians. The growth of cloud development has led to the availability of scalable and flexible cloud infrastructure that can handle a large amount of data, making it ideal for data historians. Further, cloud development has made it easier to integrate data historians with other cloud-based tools and services, such as data analysis and visualization, and creating demand for data historians.

- Cloud services adoption for the storage and management of consumer data can be attributed to the growth of cloud deployment. Payment gateways, online transfers of the fund, digital wallets, unified customer experiences, etc. services are playing a significant role in the BFSI industry, assisting with the overall shift to cloud deployment.

- In June 2022, Eros Investments, a media, entertainment, and technology portfolio of ventures - Eros Media World, Eros Now, and Xfinite's Mzaalo signed an agreement with Wipro Ltd to evolve and scale the Artificial Intelligence (AI) and Machine Learning (ML) based content localization solution. Eros Investments and Wipro's joint content localization service will be available to media and entertainment companies in two deployment models such as platform-as-a-service and private cloud deployment. Such initiatives from companies of different sectors to avail solutions in the area of cloud deployment are further expected to support market growth.

- Moreover, cloud deployments are allowing data historians to easily scale up their infrastructure as per the changing needs of their customers and eliminate the need for expensive hardware, reducing the overall cost of data historians. This makes it easier for small and medium-sized businesses to use data historians.

- Since the pandemic, the demand for cloud computing skyrocketed among many businesses as cloud services improve infrastructure efficiency, lower operating costs, and optimize business operations in response to changing conditions, giving rise to various cloud deployment models.

North America Expected to Hold Highest Market Share

- North America is expected to hold the highest market share owing to increasing spending on research and development for innovation in the data historian market in the region. Moreover, the region has vendors like Honeywell International Inc., General Electric Company, Rockwell Automation, Inc., etc., continuously investing in the market.

- The demand for data historians is expanding steadily in the region, fueled by consistently increasing demand for industrial automation data for performance improvement, rising use of Big Data analytics across various economic sectors, and constantly expanding IoT infrastructure, which generates an increasing amount of data that can be collected and analyzed, and other tech market trends.

- The region also contributes substantially to the global data center demand from the IT, BFSI, retail, and healthcare industries. Real estate experts, such as CBRE, have reported that the United States occupies almost 90% of data center space worldwide. This is further boosting the demand for data historian markets.

- For instance, in the past five years, Google has invested more than USD 37 billion in its offices and data centers in 26 states which is in addition to the more than USD 40 billion in research and development invested in the United States in 2020 and 2021. Further, in April 2022, Google announced plans to invest approximately USD 9.5 billion in its United States offices and data centers in 2022.

- Moreover, organizations in North America are increasingly recognizing the value of data analysis in decision-making and are looking for solutions to manage and store a large amount of data. This is driving the demand for data historians.

Data Historian Industry Overview

The data historian market is fragmented due to the many players in the market. Players in the market are adopting strategies like partnerships, mergers and acquisitions, new product launches, and investing in R&D for further innovations to capture the highest market share. Some of the key developments seen in the market are as such. In October 2022, Uptake Technologies Inc. collaborated with the ADX team to build an industrial data historian using ADX. Since Microsoft decided to stop the development of Time Series Insights (TSI), Uptake has been working to re-platform the flagship OT cloud data historian, Fusion, on Azure Data Explorer (ADX). In April 2022, GE Digital recently announced the availability of the world's first cloud-native operational data historian available in the AWS Marketplace, Proficy Historian for Cloud. This cloud-based industrial data management software is designed to facilitate a more simplified and reliable movement of OT data to the cloud spanning from device level to enterprise. Proficy Historian for Cloud helps companies leverage existing IT cloud investments and combine OT and enterprise data.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment on the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Consolidated Data for Process and Performance Improvement

- 5.1.2 Rising Industrial Big Data

- 5.2 Market Challenges

- 5.2.1 High Deployment Costs

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Deployment Mode

- 6.2.1 On-Premise

- 6.2.2 Cloud

- 6.3 By End-user Industry

- 6.3.1 Data Centers

- 6.3.2 Oil & Gas

- 6.3.3 Paper & Pulp

- 6.3.4 Water Management

- 6.3.5 Manufacturing

- 6.3.6 Other End-user Industry

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 General Electric Company

- 7.1.2 Siemens AG

- 7.1.3 ABB

- 7.1.4 Honeywell International Inc.

- 7.1.5 Emerson Electric Co.

- 7.1.6 AVEVA Group plc

- 7.1.7 Rockwell Automation Inc.

- 7.1.8 OSIsoft LLC

- 7.1.9 ICONICS

- 7.1.10 Open Automation Software

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球数据历史资料库市场报告

2025年全球数据历史资料库市场报告 资料历史资料库市场按组件、部署类型、组织规模、行业垂直领域和应用划分 - 全球预测 2025-2032 年

资料历史资料库市场按组件、部署类型、组织规模、行业垂直领域和应用划分 - 全球预测 2025-2032 年 资料历史学家市场 - 按组件、部署模式、最终用户、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029F

资料历史学家市场 - 按组件、部署模式、最终用户、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029F 全球资料历史学家市场 – 全球产业分析、规模、占有率、成长、趋势、预测 (2031)全球资料历史市场规模(按部署、组件、最终用户产业、地理范围和预测)

全球资料历史学家市场 – 全球产业分析、规模、占有率、成长、趋势、预测 (2031)全球资料历史市场规模(按部署、组件、最终用户产业、地理范围和预测) 资料历史学家市场规模、份额、趋势分析报告:按类型、按部署、按公司规模、按最终用途、按地区、细分市场预测,2024-2030 年

资料历史学家市场规模、份额、趋势分析报告:按类型、按部署、按公司规模、按最终用途、按地区、细分市场预测,2024-2030 年 资料历史学家市场:依产品类型、最终用户、地区 - 全球产业分析、规模、占有率、成长、趋势、预测,2024-2032 年

资料历史学家市场:依产品类型、最终用户、地区 - 全球产业分析、规模、占有率、成长、趋势、预测,2024-2032 年