|

市场调查报告书

商品编码

1644359

一次性塑胶包装:全球市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Global Single Use Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

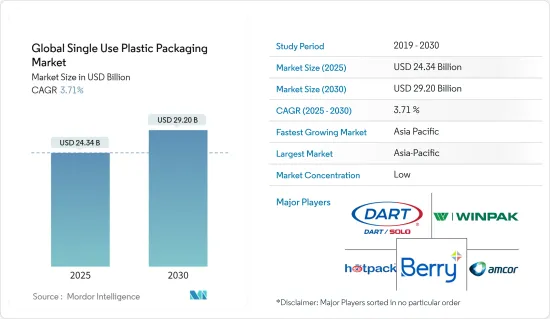

2025 年全球一次性塑胶包装市场规模预估为 243.4 亿美元,预计到 2030 年将达到 292 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.71%。

主要亮点

- 城镇人口的不断增长推动了对已调理食品的需求,极大地影响了餐饮业的包装趋势。预计这一趋势将在预测期内增加对一次性塑胶包装解决方案的需求。都市区消费者通常生活忙碌,没有时间准备饭菜,因此越来越依赖需要高效包装的方便食品。

- 都市区宅配服务和外带选择的兴起进一步推动了这种需求。在重点地区,都市化、生活方式的改变、对快节奏职场环境的适应以及对线上食品平台的日益依赖正在迅速改变餐饮业的动态,进一步推动对一次性塑胶包装解决方案的需求。总的来说,这些因素推动了包装市场的不断增长,这种包装市场优先考虑便利性、便携性和食品保鲜性——这些特点通常与食品服务行业的一次性塑胶包装有关。

- 越来越多的终端用户(如快餐店、全方位服务餐厅、咖啡店、经销店和机构)正在推动对便捷包装解决方案的需求。预计这一趋势将增加一次性包装形式的产量。随着消费者追求便利性并适应不断变化的生活方式,尤其是家庭规模变小,从硬包装到软包装的转变正在加速。因此,一次性塑胶包装在各种食品服务领域越来越受欢迎。

- 随着人口结构、就业模式和生活方式的变化,速食专利权和速食店的快速扩张正推动市场成长。速食价格实惠、准备时间短,满足了消费者对便利用餐选择的需求。全球速食消费量的增加直接支持了餐饮业一次性塑胶包装的成长。

- 消费者对便利性的需求不断增长是推动一次性塑胶包装市场发展的关键因素。製造商正在透过提供满足不断变化的需求的包装解决方案来适应不断变化的客户偏好。忙碌的上班族的生活方式推动了对便利食品包装选择的需求。此外,生产商现在正在考虑使用后的处理,从而导致了易于处理的包装物品的开发。

- 一次性塑胶的监管以及对纺织品和纸质产品等永续包装替代品的日益偏好,都对市场成长构成了阻碍。这些法规旨在减少塑胶废弃物并推广环保包装解决方案。向永续替代品的转变受到消费者需求和政府政策的共同推动。

- 消费者对一次性塑胶和不可持续做法对环境影响的认识不断提高,这导致对更高发展标准的要求,从而带来积极的生态学成果。这种意识导致许多消费者主动寻找具有环保包装的产品,迫使企业调整其包装策略。因此,各行各业的公司都在投资研发创新和永续的包装解决方案,以满足不断变化的消费者期望并遵守监管要求。

一次性塑胶包装市场的趋势

速食店市场占很大份额

- 速食店(QSR)提供平价的餐饮选择,注重快速服务。快餐店与传统餐厅的不同之处在于,它限制餐桌服务,并强调自助服务。快餐店通常提供精简的菜单,其中包含易于准备的食品,例如汉堡、三明治和油炸食品,这些食品可以快速组装和上桌。快餐店受到那些想要快速吃饭的人们的欢迎,因为他们高效的营运让他们能够快速地为大量顾客提供服务。

- 快餐店使用的大多数一次性塑胶食品服务由发泡聚苯乙烯 (EPS)、聚丙烯 (PP)、聚对苯二甲酸乙二醇酯 (PET) 和聚乳酸 (PLA) 製成。之所以选择这些材料,是因为它们的耐用性、成本效益以及保持食物温度的能力,有助于提高快餐服务的整体效率和客户体验。

- 快餐店(QSR)的菜单上的食物通常直接从包装中取出食用。消费者选择速食是因为其方便、准备快速、价值高且价格实惠。因此,包装是食品的重要组成部分,必须符合消费者的速食动机和期望。包装有多种用途,例如保持食品温度、保鲜、方便食用。它还在品牌形象和客户认知方面发挥着至关重要的作用。

- 随着永续性成为日益受关注的问题,许多速食店正在探索环保包装选择,以满足消费者对环境责任的需求,同时仍保持快餐顾客所期望的便利性和功能性。速食包装的设计和材料必须平衡实用性、成本效益和环境影响,同时提升消费者的整体用餐体验。

- 在当今快节奏的环境中,一次性塑胶包装已成为快餐店(QSR)的必需品。由于需要更多时间在家做饭,消费者越来越多地选择速食。消费行为的这种转变推动了对便利、随时用餐解决方案的需求。一次性塑胶包装使快餐店能够以高效、安全且经济的方式包装食品,从而满足这一需求。这些包装解决方案旨在承受各种温度并在运输过程中保持食品的品质。它们还具有不易洩漏、更易于处理等实际优势,对于经常在通勤或职场途中吃饭的顾客来说至关重要。

- 餐厅越来越受欢迎,推动了速食店(QSR)市场的扩张。随着主要 QSR 品牌开设更多门市,一次性塑胶包装的需求也随之增加。这种扩张发生在各个地区和菜系,反映了消费者对方便、实惠的餐饮选择的偏好的改变。

- 这一趋势在都市区和新兴市场尤其明显,快速的都市化和繁忙的生活方式导致 QSR 顾客数量的增加。例如,全球 QSR 品牌麦当劳正在稳步增加其在世界各地的餐厅数量,以满足日益增长的快餐需求。该公司全球门市数量将从 2017 年的 37,241 家成长到 2023 年的 41,822 家,反映了这一趋势。这种成长并不仅限于麦当劳,其他大型速食连锁店也扩大了门市,进一步推动了一次性包装的需求。

预计亚太地区将占据主要市场份额

- 亚太地区拥有许多人口密集的国家,例如中国和印度,以及新兴国家,因此外出用餐的需求很高。因此,一次性塑胶包装的需求正在上升,并且这种趋势在预测期内可能会持续下去。塑胶已成为包装产业的关键组成部分,是消费者便利文化的核心。塑胶的多功能性和耐用性使其成为从外带容器到饮料瓶等各种食品包装应用的理想选择。

- 由于塑胶包装比其他材料更具成本绩效,许多食品服务和包装应用正在从纸板、玻璃和金属等传统包装材料转向塑胶。这种转变在都市区尤其明显,那里的外卖和快餐店行业正在迅速扩张。由于塑胶包装重量轻,它还有助于降低运输成本和供应链中的碳排放,进一步支持其在亚洲各地餐饮业的采用。

- 该地区的家庭和非现场食品和饮料用包装产品的产量预计将出现增长,因为这些产品的订单通常为大批量。这一增长是由消费者习惯的改变和对方便、便携食品的需求不断增长所推动的。一次性塑胶包装在该地区被广泛使用,尤其是在速食店,用于各种用途,包括蛤壳、瓶子、托盘、杯子和盖子。这些包装解决方案的多功能性和成本效益使其成为餐饮公司的热门选择。然而,这一趋势也引发了人们对环境永续性的担忧,促使该地区关于替代包装材料和回收工作的讨论。

- 该地区拥有大量终端用户产业,是一次性塑胶包装的重要投资者和采用者。这种采用在食品饮料、医疗保健和消费品等多个领域都有所体现。有几个因素推动了该地区的市场成长。首先,对包装餐点的需求不断增加,尤其是在高度重视便利性的都市区。其次,餐厅和超级市场的扩张推动了对保持食品新鲜和安全的包装解决方案的需求。最后,随着消费者偏好和生活习惯的改变,瓶装水和饮料的消费量不断增加,进一步推动了该地区对一次性塑胶包装的需求。总的来说,这些趋势正在促进该地区一次性塑胶包装市场的持续成长和发展。

- 印度人口众多,经济正在崛起,其瓶装水消费量大幅成长,成为该地区的强劲市场。印度铁路餐饮和旅游有限公司 (IRCTC) 推出了自己的瓶装水品牌“Rail Neer”,主要在火车上和火车站销售。随着瓶装水需求的不断增长和铁路部门的扩张,IRCTC 大幅增加了产量。预计2021年产量将达7,530万瓶,2023年产量将增加至3.577亿瓶。

- 近年来,印度和中国的包装产业都经历了显着的成长。此次扩张归因于多种因素,包括建立新的製造部门、采用环保材料和更注重研发。这些发展使得创新且外观吸引的产品能够以有竞争力的成本在当地生产。此外,印度的「印度製造」计画等政府措施预计将加速包装产业的进一步发展。

- 中国瓶装水产量和消费量的增加对市场产生了正面影响。中国消费者越来越倾向于积极、健康的生活方式,这导致对瓶装水的需求激增。人们对国家自来水污染问题的日益担忧进一步加剧了这一趋势。因此,中国各领域的瓶装水需求均大幅成长。

- 消费者的健康意识不断增强,他们寻求更安全、更方便的补水方式,瓶装水因此成为有吸引力的选择。根据东方财富网报道,这种消费行为的转变也反映在中国瓶装水零售的预测上。预计市场将经历大幅成长,零售额将从 2020 年的 2,002 亿元人民币(281.2 亿美元)成长至 2025 年的 3,536 亿元人民币(496.7 亿美元)。这一成长轨迹凸显了中国消费者对瓶装水产品的市场潜力不断扩大和偏好不断改变。

一次性塑胶包装行业概况

一次性塑胶包装市场比较分散。包括 Berry Global Inc.、Amcor Group GmbH、Huhtamaki Oyj 和 Hotpack Packaging Industries LLC 在内的多家全球和地区参与者正在争夺这个竞争激烈的市场的关注。该市场的特点是产品差异化程度低、产品渗透率高、竞争激烈。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

第五章 市场动态

- 市场驱动因素

- 快餐店和小餐馆的兴起推动了市场需求

- 市场限制

- 有关包装中使用塑胶的环境问题和政府法规

第六章 市场细分

- 按材质

- 聚乳酸(PLA)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚乙烯 (PE)

- 其他材料类型

- 依产品类型

- 瓶子

- 包包和小袋

- 翻盖

- 托盘、杯子、盖子

- 其他产品类型

- 按最终用户

- 速食店

- 全方位服务餐厅

- 机构

- 零售

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲和纽西兰

- 拉丁美洲

- 巴西

- 墨西哥

- 哥伦比亚

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 北美洲

第七章 竞争格局

- 公司简介

- Novolex

- Pactiv LLC

- Dart Container Corporation

- Winpak Ltd

- Berry Global Inc.

- Amcor Group

- Huhtamaki Oyj

- Hotpack Packaging Industries LLC

- Graphic Packaging International LLC

- Pactiv Evergreen Inc.

第八章投资分析

第九章:市场的未来

The Global Single Use Plastic Packaging Market size is estimated at USD 24.34 billion in 2025, and is expected to reach USD 29.20 billion by 2030, at a CAGR of 3.71% during the forecast period (2025-2030).

Key Highlights

- The expanding urban population drives the demand for prepared and ready-to-eat food products, significantly influencing food service packaging trends. This trend is expected to increase the demand for single-use plastic packaging solutions during the forecast period. Consumers in urban areas often have busier lifestyles and less time for meal preparation, leading to a greater reliance on convenience foods that require efficient packaging.

- The rise of food delivery services and takeaway options in cities has further amplified this demand. In key regions, urbanization, lifestyle changes, adaptation to fast-paced work environments, and increased reliance on online food platforms rapidly transform the foodservice industry dynamics, further boosting the demand for single-use plastic packaging solutions. These factors collectively contribute to a growing market for packaging that prioritizes convenience, portability, and food preservation, characteristics often associated with single-use plastic packaging in the foodservice industry.

- The growth of end users, including quick-service restaurants, full-service restaurants, coffee shops, snack outlets, and institutional facilities, drives the demand for convenient packaging solutions. This trend is expected to increase the production of single-use packaging formats. The shift from rigid to flexible packaging is gaining momentum as consumers seek convenience and adapt to changing lifestyles, particularly in smaller households. Consequently, single-use plastic packaging is experiencing increased popularity across various food service segments.

- The rapid expansion of fast-food franchises and quick-service restaurants drives the market's growth, responding to changing demographics, employment patterns, and lifestyles. Fast food's affordability and quick preparation times align with consumers' demand for convenient meal options. This global increase in fast food consumption directly supports the growth of single-use plastic packaging in the food service industry.

- The growing demand for consumer convenience is a crucial factor driving the single-use plastic packaging market. Manufacturers adapt to evolving customer preferences by offering packaging solutions catering to these changing needs. The busy lifestyles of working professionals have increased the demand for convenient food packaging options. Additionally, producers are now considering post-use disposal, leading to the development of packaging items that can be easily discarded.

- Regulations on single-use plastics and the growing preference for sustainable packaging alternatives, such as fiber and paper-based products, challenge the market's growth. These regulations aim to reduce plastic waste and promote environment-friendly packaging solutions. The shift towards sustainable alternatives is driven by both consumer demand and governmental policies.

- Increasing consumer awareness about the environmental impact of single-use plastics and unsustainable practices has led to demands for higher development standards with positive ecological outcomes. This awareness has prompted many consumers to actively seek out products with eco-friendly packaging, putting pressure on companies to adapt their packaging strategies. As a result, businesses across various industries are investing in research and development of innovative, sustainable packaging solutions to meet these evolving consumer expectations and comply with regulatory requirements.

Single Use Plastic Packaging Market Trends

Quick Service Restaurants Segment to Hold a Significant Share

- Quick-service restaurants (QSRs) provide affordable food options focusing on rapid service. These establishments are characterized by limited table service and a strong emphasis on self-service, setting them apart from traditional restaurants. QSRs typically offer a streamlined menu of easily prepared items, such as burgers, sandwiches, and fried foods, which can be quickly assembled and served. The efficiency of their operations allows them to serve a high volume of customers quickly, making them popular for those seeking quick meals.

- The majority of single-use plastic food service products utilized in QSRs are made from expanded polystyrene (EPS), polypropylene (PP), polyethylene terephthalate (PET), and polylactic acid (PLA). These materials are chosen for their durability, cost-effectiveness, and ability to maintain food temperature, contributing to the overall efficiency and customer experience in quick-service settings.

- Quick-service restaurant (QSR) menu items are typically consumed directly from their packaging. Consumers opt for fast food due to its convenience, rapid preparation, value, and affordability. Consequently, packaging is an essential food product component and must align with consumers' motivations and expectations for fast food. The packaging serves multiple purposes, including maintaining food temperature, preserving freshness, and facilitating easy consumption. It also plays a crucial role in brand identity and customer perception.

- As sustainability concerns grow, many QSRs are exploring eco-friendly packaging options to meet consumer demands for environmental responsibility while maintaining the convenience and functionality that fast food customers expect. The design and materials used in fast food packaging must balance practicality, cost-effectiveness, and environmental impact, all while enhancing the overall dining experience for consumers.

- In today's fast-paced environment, single-use plastic packaging has become integral to Quick Service Restaurants (QSRs). Consumers need more time for meal preparation at home, so they increasingly rely on fast food options. This shift in consumer behavior has led to a greater demand for convenient, on-the-go meal solutions. Single-use plastic packaging allows QSRs to meet this demand by packaging food efficiently, safely, and cost-effectively. These packaging solutions are designed to withstand various temperatures and maintain food quality during transportation. They also offer practical benefits such as leak resistance and easy handling, which are crucial for customers who often consume their meals while commuting or at their workplaces.

- The growing popularity of restaurants drives the expansion of the fast-food and quick-service restaurant (QSR) market. As major QSR brands increase their outlets, they create demand for single-use plastic packaging. This expansion is evident across various regions and cuisines, reflecting changing consumer preferences for convenient and affordable dining options.

- The trend is particularly noticeable in urban areas and emerging markets, where rapid urbanization and busier lifestyles contribute to the increased patronage of QSRs. For example, McDonald's, a global QSR brand, has been steadily growing its store count worldwide in response to the rising demand for quick meals. The company's global store count grew from 37,241 in 2017 to 41,822 in 2023, illustrating this trend. This growth was not limited to McDonald's alone; other major QSR chains expanded their footprints, further driving the demand for single-use packaging.

Asia-Pacific Expected to Hold Significant Share in the Market

- In Asia-Pacific, many densely populated countries and emerging economies, such as China and India, have a high demand for food services. Consequently, the need for single-use plastic packaging is increasing and will remain elevated during the forecast period. Plastic has been a crucial component of the packaging sector, which is central to consumer convenience culture. The versatility and durability of plastic make it an attractive option for various food packaging applications, from takeaway containers to beverage bottles.

- Due to plastic packaging's favorable cost-performance ratio compared to other materials, many food service and packaging applications have transitioned from traditional packaging materials like corrugated paper boards, glass, and metal to plastics. This shift is particularly noticeable in urban areas where the food delivery and quick-service restaurant sectors are rapidly expanding. The lightweight nature of plastic packaging also contributes to reduced transportation costs and lower carbon emissions in the supply chain, further driving its adoption in the food service industry across Asia.

- The region is expected to grow in terms of producing packaging products for domestic and off-premise food and beverage items, often ordered in bulk. This increase is driven by changing consumer habits and the growing demand for convenient, portable food options. Single-use plastic packaging is widely used in the region for various applications, including clamshells, bottles, trays, cups, and lids, particularly in fast-food establishments. The versatility and cost-effectiveness of these packaging solutions make them popular choices for businesses in the food service industry. However, this trend also raises concerns about environmental sustainability, prompting discussions about alternative packaging materials and recycling initiatives in the region.

- Due to its numerous end-user industries, the region is a significant investor and adopter of single-use plastic packaging. This adoption is evident across various sectors, including food and beverage, healthcare, and consumer goods. Several factors drive the regional market growth. Firstly, there is an increasing demand for packaged meals, particularly in urban areas where convenience is highly valued. Secondly, the expansion of restaurants and supermarkets has created a need for more packaging solutions to maintain food freshness and safety. Lastly, the rising consumption of bottled water and beverages, fueled by changing consumer preferences and lifestyle habits, has further boosted the demand for single-use plastic packaging in the region. These trends collectively contribute to the sustained growth and development of this area's single-use plastic packaging market.

- India stands out as a robust market in the region due to its large population and developing economy, leading to a significant increase in bottled water consumption. The Indian Railway Catering and Tourism Corporation Limited (IRCTC) has introduced its own bottled water brand, "Rail Neer," primarily sold on trains and at railway stations. With the rising demand for bottled water and the expanding railway sector, IRCTC has substantially increased production. In 2021, the corporation produced 75.30 million bottles, which grew to 357.70 million bottles in 2023.

- The packaging industry in India and China has experienced significant growth in recent years. This expansion is attributed to several factors, including establishing new manufacturing units, adopting eco-friendly materials, and increasing focus on research and development. These developments have led to the creation of innovative and visually appealing products, all manufactured locally at competitive costs. Additionally, government initiatives such as India's 'Make in India' program are expected to accelerate these further advancements in the packaging industry.

- The increasing production and consumption of bottled water in China have positively influenced the market. Chinese consumers are increasingly adopting more active and healthier lifestyles, which has led to a surge in demand for bottled water. This trend is further fueled by rising concerns about water contamination in the country's tap water supply. As a result, China has experienced a significant increase in demand for bottled water across various demographics.

- The growing health consciousness among consumers has prompted them to seek safer and more convenient hydration options, making bottled water an attractive choice. According to Eastmoney.com, this shift in consumer behavior is reflected in the projected retail sales figures for bottled water in China. The market is expected to show substantial growth, with retail sales projected to reach CNY 353.6 billion (USD 49.67 billion) in 2025, a notable increase from CNY 200.2 billion (USD 28.12 billion) in 2020. This growth trajectory underscores the expanding market potential and the changing preferences of Chinese consumers toward bottled water products.

Single Use Plastic Packaging Industry Overview

The single-use plastic packaging market is fragmented. Several global and regional players, such as Berry Global Inc., Amcor Group GmbH, Huhtamaki Oyj, and Hotpack Packaging Industries LLC, are vying for attention in this contested space. This market is characterized by low product differentiation, growing product penetration, and high competition.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industrial Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Increasing Number of Quick-Service Restaurants and Food Establishments has Driven Market Demand

- 5.2 Market Restraints

- 5.2.1 Environmental Concerns and Government Regulations Regarding Use of Plastic in Packaging

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Polylactic Acid (PLA)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polyethylene (PE)

- 6.1.4 Other Material Types

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Bags and Pouches

- 6.2.3 Clamshells

- 6.2.4 Trays, Cups, and Lids

- 6.2.5 Other Product Types

- 6.3 By End User

- 6.3.1 Quick Service Restaurants

- 6.3.2 Full Service Restaurants

- 6.3.3 Institutional

- 6.3.4 Retail

- 6.3.5 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Columbia

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Novolex

- 7.1.2 Pactiv LLC

- 7.1.3 Dart Container Corporation

- 7.1.4 Winpak Ltd

- 7.1.5 Berry Global Inc.

- 7.1.6 Amcor Group

- 7.1.7 Huhtamaki Oyj

- 7.1.8 Hotpack Packaging Industries LLC

- 7.1.9 Graphic Packaging International LLC

- 7.1.10 Pactiv Evergreen Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

塑胶包装市场分析及预测(至2035年):依类型、产品类型、应用、材料类型、技术、最终用户、功能及工艺划分

塑胶包装市场分析及预测(至2035年):依类型、产品类型、应用、材料类型、技术、最终用户、功能及工艺划分 德国塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

德国塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球PCR塑胶包装市场报告2026年全球塑胶替代包装市场报告2026年全球瓦楞塑胶包装市场报告2026年全球硬质热成型塑胶包装市场报告

2026年全球PCR塑胶包装市场报告2026年全球塑胶替代包装市场报告2026年全球瓦楞塑胶包装市场报告2026年全球硬质热成型塑胶包装市场报告 聚苯乙烯包装市场-2026-2031年预测全球塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)全球氧化生物分解袋市场规模、占有率、成长及产业分析:依类型、应用、区域洞察与预测(2026-2034年)全球包装废弃物管理市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034)

聚苯乙烯包装市场-2026-2031年预测全球塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)全球氧化生物分解袋市场规模、占有率、成长及产业分析:依类型、应用、区域洞察与预测(2026-2034年)全球包装废弃物管理市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034)