|

市场调查报告书

商品编码

1644411

OpenStack 服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)OpenStack Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

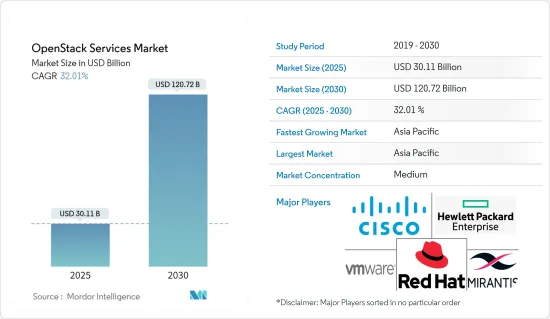

OpenStack 服务市场规模预计在 2025 年为 301.1 亿美元,预计到 2030 年将达到 1207.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 32.01%。

越来越多地采用计量收费模式以及在虚拟环境中开发具有成本效益的IT基础设施(其中所有工作负载由云端供应商承担)是预计推动全球 OpenStack 服务市场成长的因素。

主要亮点

- 世界各地的公司都倾向于采用云端服务。云端运算巨头Oracle预测,到 2025 年,80% 的企业业务功能将透过其云端相关服务转移到云端。近年来,云端服务供应商从专业服务和其他云端服务中获得了巨额收益和利润。微软是成长最快的云端服务供应商之一,2022 年其 Azure 和其他云端服务与前一年同期比较增 31%。

- 云端和工业化服务的成长以及传统资料中心外包(DCO)的衰退标誌着混合云端基础设施服务的巨大变化。这有望推动向云端 IaaS 和託管的转变。由于专业云端运算提供的优势,预计这些细分市场对专业云端运算的需求将会增加。

- 基础设施即服务 (IaaS) 被视为云端服务频谱中的第三级(最低级),其中供应商为客户提供包括付费使用制存取云端中的储存、伺服器、网路和其他运算资源的解决方案。 IaaS 硬体通常由外部提供者提供并由组织管理。

- 此外,2023 年 10 月—Ironic 宣布推出一个新的服务步骤框架,供基础设施营运商修改现有节点。使用服务步骤,操作员可以利用该步骤执行修改处于 ACTIVE 状态的已部署节点的操作,例如清理或自订配置。

- OpenStack是一个动态的、开放的云端运算解决方案,需要定期升级。定期新增功能和功能并删除旧特性和功能。如此高度动态的能力范围可能对市场成长构成挑战。

OpenStack服务市场趋势

通讯业越来越多地使用 OpenStack 服务,推动市场

- 过去几年来,通讯业经历了显着的成长。在竞争激烈的市场中,电信业者不断面临以低成本提供创新服务以留住客户的压力。 OpenStack 使通讯业者能够部署和管理云端基础设施,而无需支付专有解决方案带来的高昂成本。

- OpenStack 是一个开放原始码系统,可让您透过虚拟资源池建构和管理私有云端云和公有云。运算、网路、储存、身分和映像等云端处理服务由组成 OpenStack 平台中「计划」的工具处理。对于寻求改善服务交付和营运效率的通讯业者来说,此功能至关重要。

- OpenStack作为通讯业者的首选基础设施,是网路功能虚拟(NFV)的选择。 NFV与OpenStack是广大通讯业者和企业领导者的选择。例如 AT&T、彭博资讯、中国行动、德国电信、日本电报电话公司、SK 电讯和 Verizon。

- 此外,OpenStack 也用于支援一些最大的行动通讯网络,包括 5G 等工作负载。中国移动的行动网路拥有超过300万基地台、8亿用户,而迄今规模最大的NFV网络,拥有超过5万台伺服器,就是中国行动利用OpenStack建构的。

预计亚太地区将出现显着成长

- 大多数中国超大规模云端运算和通讯业者正在主导亚太全部区域OpenStack 服务的采用。 OSF 指出,腾讯、中国移动等公司对 OpenStack 的使用在亚太地区快速成长的 OpenStack 市场中发挥重要作用。

- 超级应用微信的营运商和超大规模云端供应商腾讯使用 OpenStack 为其跨产业的业务和公有云服务提供支援。中国移动也使用 OpenStack 提供私有云端服务以及电信云来支援其下一代通讯网路。

- 该地区的用户正在结合 OpenStack 和 Kubernetes 来解决大型开放基础架构问题。我们越来越多地利用 Airship 和 StarlingX 等计划来使用开放、可组合的基础设施来满足该地区运营的应用程式的需求。

- 中国预计将占全球 OpenStack配置的近一半,是 OSF 的第三大成员国,OSF 是一个由该组织实验性主办的开放基础设施计划的使用者和贡献者组成的组织。中国移动以OpenStack作为云端部署的关键技术之一,建构了AUTO自动化测试平台。 AUTO 专注于可扩充性和效能,广泛使用 OpenStack SDK 和现有测试工具来评估和验证云端部署。

- 九九云、中国银联、烽火通讯等多家中国公司正为StarlingX计划上游做出贡献。例如,中国银联国家电子商务与电子付款工程技术研究中心正在研究由 StarlingX 支援的安全边缘基础设施,用于非接触式付款用例。随着5G的发展,多接取边缘运算(MEC)、媒体云端等技术不断涌现。

- 随着5G网路基础设施快速发展,人工智慧(AI)也蓬勃兴起。为了全面支援开发,基础设施本身必须发展为云端原生服务。总部位于韩国的 SK 电信在过去几年中一直在开发云端原生基础设施技术,并且积极参与 OpenStack 基金会 (OSF) 的两个全球计划,尤其是 OSF 的 Airship计划。

OpenStack服务产业概览

OpenStack 服务市场处于半固体状态,主要参与者如下:思科系统公司、红帽公司、惠普企业发展有限公司、Mirantis 公司等。

203年6月,全球领先的开放原始码解决方案供应商之一诺基亚与红帽公司宣布达成协议,将诺基亚的核心网路应用程式与红帽 Openstack 平台和红帽 OpenShift 紧密整合。作为协议的一部分,诺基亚和红帽公司将共同支援和发展现有的诺基亚容器服务 (NCS) 和诺基亚 CloudBand 基础设施软体 (CBIS) 客户,并随着时间的推移开发向红帽公司平台的迁移路径。此外,诺基亚将利用红帽公司的基础设施平台来快速开发和测试诺基亚广泛的核心网路产品组合。

2022 年 10 月,红帽公司在其 MWC 拉斯维加斯活动上宣布了 OpenStack Platform 17。这涵盖了以开放、混合云端架构为重点的广泛改进,以帮助服务供应商建立扩充性的下一代网路。

2022 年 6 月,爱立信和红帽公司宣布合作部署该解决方案,为服务供应商提供一个跨 vEPC、5G Core、IMS、OSS 和 BSS 网路的开放平台。团队将爱立信的网路功能解决方案与 Red Hat OpenShift 和 Red Hat OpenStack 平台结合。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- COVID-19影响评估

- 市场驱动因素

- 组织对提高业务敏捷性和效率的需求日益增加

- OpenStack 是开放原始码的,为客製化解决方案提供了灵活性

- 通讯业越来越多地使用 OpenStack 服务

- 市场限制

- 缺乏公司对资料中心所要求的稳健性,包括可用性和安全性等 IT 管理功能

- 技术简介

- 用于管理OpenStack应用程式的框架

- 由 OpenStack 基金会营运并作为试点计画营运的开放基础设施计划。

- 跨组织 OpenStack使用案例

第五章 市场区隔

- 按部署模型

- 在云端

- 本地

- 按最终用户产业

- IT

- 通讯

- 银行和金融服务

- 学术的

- 零售/电子商务

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Cisco Systems, Inc.

- Red Hat, Inc.

- Hewlett Packard Enterprise Development LP

- VMware, Inc.

- Mirantis, Inc.

- Canonical Ltd.

- Dell Inc.

- Rackspace US, Inc.

- Huawei Technologies Co., Ltd.

- NetApp, Inc.

第七章投资分析

第 8 章:市场的未来

The OpenStack Services Market size is estimated at USD 30.11 billion in 2025, and is expected to reach USD 120.72 billion by 2030, at a CAGR of 32.01% during the forecast period (2025-2030).

The growing adoption of the pay-as-you-go model and the cost-effective IT infrastructure development in a virtual environment (where every workload is taken care of by the cloud vendors) are certain factors expected to drive market growth for OpenStack services globally.

Key Highlights

- Enterprises across the world are inclined towards the adoption of cloud services. Oracle Corporation, the cloud giant, has predicted that owing to the cloud-related service offerings, 80% of the enterprise business functions will move to the cloud by 2025. In recent years, cloud service providers have experienced huge revenues and profit gains due to their professional and other cloud services. Microsoft, one of the fastest-growing cloud service providers, registered a year-on-year growth of 31% in Azure and other cloud services in 2022.

- The growth of cloud and industrialized services and the decline of traditional data center outsourcing (DCO) indicate a massive shift toward hybrid cloud infrastructure services. This is expected to drive the shift toward cloud IaaS and hosting. Owing to its benefits, professional cloud deployment is expected to experience an improved demand for these market segments.

- Infrastructure-as-a-Service (IaaS) is considered the third (lowest) level in the spectrum of cloud services, where a vendor provides clients with solutions such as pay-as-you-go access to storage, servers, networking, and other computing resources in the cloud. IaaS hardware is usually offered and managed by the organization by an external provider.

- Moroever , October 2023 - Ironic has announced the launch of infrastructure operators to modify existing nodes using the "service steps" framework. Servicing allows operators to leverage steps, like you would for cleaning or customized deployments, to perform actions to modify deployed nodes in an ACTIVE state.

- OpenStack is a dynamic and open cloud-computing solution that needs to be upgraded regularly. The new functions & features are added regularly, and other old functions are removed. This high-dynamic range of functions may create challenges for market growth.

OpenStack Services Market Trends

Increasing use of OpenStack Services Across Telecommunication Sector is Driving the Market

- The telecom industry has observed extensive growth during the past few years. Telecommunication companies are encountering constant pressure to deliver innovative services at lower costs to retain their customers in the competitive market. It allows telecom companies to deply and manage their cloud infrastructure without the high costs associated with proprietary solutions.

- OpenStack is an open source system that allows private and public clouds to be built and managed through a pooling of virtual resources. The core clouds computing services, such as compute, networking, storage, identities and images are handled by tools that comprise the OpenStack platform 'projects'. This capability is crucial for telecom operators looking to enhance their service offerings and operational efficiency.

- As a base of choice for operators, OpenStack has been chosen as their Network Function Virtualization NFV. NFV with OpenStack has been chosen by a wide range of telecom operators and business leaders. AT&T, Bloomberg LP., China Mobile, Deutsche Telekom, Nippon Telegraph & Telephone Corporation, SK Telecom and Verizon are among them.

- Moreover, OpenStack, including workloads such as 5G, has been used to power the biggest mobile telecommunications network. The mobile network of China Mobile has over 3 million base stations and 800 million subscribers an With over 50,000 servers, the largest Network of NFV today is built by China Mobile using OpenStack.

Asia-Pacific is Expected to Hold Significant Growth

- The majority of hyperscale cloud and telecom organizations in China are taking charge of adopting OpenStack services across the Asia Pacific region. Citing the use of OpenStack by companies such as Tencent and China Mobile, the OSF said these companies play a critical role in the rapidly growing OpenStack market in Asia-Pacific.

- Tencent, the company behind the WeChat super app and hyperscale cloud supplier, has been using OpenStack to power its operations and public cloud services that are being used by different industries. Also, at China Mobile, OpenStack is being used to deliver public and private cloud services and its telecom cloud to power its next-generation telco network.

- Users throughout the region are combining OpenStack and Kubernetes to solve big open infrastructure problems. They're increasingly leveraging projects like Airship and StarlingX, using open, composable infrastructure to meet the demands of applications operating in the region.

- China, which is expected to account for almost half of the world's OpenStack deployments, has the third-highest number of members in the OSF, an organization comprising users and contributors to the open infrastructure projects piloted and hosted by the organization. China Mobile has created an automated testing platform dubbed AUTO with OpenStack as one of its primary cloud deployment technologies. With an emphasis on scalability and performance, AUTO extensively utilized the OpenStack SDK and pre-existing testing tools to evaluate and confirm the cloud deployment.

- Multiple Chinese companies contribute upstream to the StarlingX project, including 99cloud, China UnionPay, and FiberHome. For instance, the Electronic Commerce and Electronic Payment National Engineering Laboratory of China UnionPay has researched a secured edge infrastructure powered by StarlingX for a contactless payment use case; with the evolution of 5G, technologies such as Multi-Access Edge Computing (MEC), Media Cloud.

- Artificial Intelligence (AI) has strongly emerged along with rapid growth in 5G network infrastructure. The infrastructure itself must evolve as a cloud-native service to fully support the development. Korea-based SK Telecom has been developing cloud-native infrastructure technology for the past few years and actively participates in global projects both in OpenStack Foundation (OSF), especially the Airship project in OSF.

OpenStack Services Industry Overview

The OpenStack Services Market is semi-consolidated due to the presence of significant players such as Cisco Systems, Inc., Red Hat, Inc., Hewlett Packard Enterprise Development LP, Mirantis, Inc., etc. The players in the market are frequently launching innovative solutions, forming partnerships, and mergers to increase their market share and expand their geographical presence.

In June 203, Nokia and Red Hat, Inc., one of the leading global providers of open-source solutions, announced that they had agreed to tightly integrate Nokia's core network applications with Red Hat Openstack Platform and Red Hat OpenShift. As part of the agreement, Nokia and Red Hat would jointly support and evolve existing Nokia Container Services (NCS) and Nokia CloudBand Infrastructure Software (CBIS) customers while developing a path to migrate to Red Hat's platforms over time. Additionally, Nokia would leverage Red Hat's infrastructure platforms to enable faster development and testing of Nokia's extensive core network portfolio.

In October 2022, RedHat announced the launch of OpenStack Platform 17 at the MWC Las Vegas event, covering a wide range of improvements with a focus on open hybrid cloud architectures that are meant to aid service providers as they construct expansive next-generation networks.

In June 2022, Ericsson and Red Hat announced the partnership to deploy solutions, empowering service providers with an open platform that extended across a network for vEPC, 5G Core, IMS, OSS, and BSS. The team integrated Ericsson's network function solutions with Red Hat OpenShift and Red Hat OpenStack Platform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment on the Impact due to COVID-19

- 4.4 Market Drivers

- 4.4.1 Increasing Need for Organizations to Improve Their Business Agility and Efficiency

- 4.4.2 OpenStack Being Open Source Provides the Flexibility for Customized Solution

- 4.4.3 Increasing use of OpenStack Services in Telecommunication Sector

- 4.5 Market Restraints

- 4.5.1 Lack of Robustness that Enterprises Desire for Their Data Centers, Including IT Management Features, Such as Availability and Security

- 4.6 Technology Snapshot

- 4.6.1 Frameworks Utilized to Manage OpenStack Applications

- 4.6.2 Open Infrastructure Projects Hosted and Piloted by OpenStack Foundation

- 4.6.3 Use Cases of OpenStack Across Organizations

5 MARKET SEGMENTATION

- 5.1 By Deployment Model

- 5.1.1 On-Cloud

- 5.1.2 On-Premise

- 5.2 By End-user Industry

- 5.2.1 Information Technology

- 5.2.2 Telecommunication

- 5.2.3 Banking and Financial Services

- 5.2.4 Academic

- 5.2.5 Retail/E-Commerce

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems, Inc.

- 6.1.2 Red Hat, Inc.

- 6.1.3 Hewlett Packard Enterprise Development LP

- 6.1.4 VMware, Inc.

- 6.1.5 Mirantis, Inc.

- 6.1.6 Canonical Ltd.

- 6.1.7 Dell Inc.

- 6.1.8 Rackspace US, Inc.

- 6.1.9 Huawei Technologies Co., Ltd.

- 6.1.10 NetApp, Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

2026年全球託管OpenShift服务市场报告2026年全球託管OpenStack服务市场报告OpenStack 服务全球市场报告 2026

2026年全球託管OpenShift服务市场报告2026年全球託管OpenStack服务市场报告OpenStack 服务全球市场报告 2026 OpenStack 服务市场规模、份额、趋势和预测:按组件类型、组织规模、平台、应用和地区划分,2026-2034 年

OpenStack 服务市场规模、份额、趋势和预测:按组件类型、组织规模、平台、应用和地区划分,2026-2034 年 OpenStack 服务市场 - 全球产业规模、份额、趋势、机会、预测:按部署方式、组织规模、产业垂直领域、区域和竞争格局划分,2021-2031 年

OpenStack 服务市场 - 全球产业规模、份额、趋势、机会、预测:按部署方式、组织规模、产业垂直领域、区域和竞争格局划分,2021-2031 年 OpenStack 服务市场 - 2025 年至 2030 年预测

OpenStack 服务市场 - 2025 年至 2030 年预测 OpenStack 服务市场规模、份额、按服务类型、部署类型、最终用户和地区分類的成长分析 - 产业预测,2025 年至 2032 年

OpenStack 服务市场规模、份额、按服务类型、部署类型、最终用户和地区分類的成长分析 - 产业预测,2025 年至 2032 年