|

市场调查报告书

商品编码

1644440

资料库自动化:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Database Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

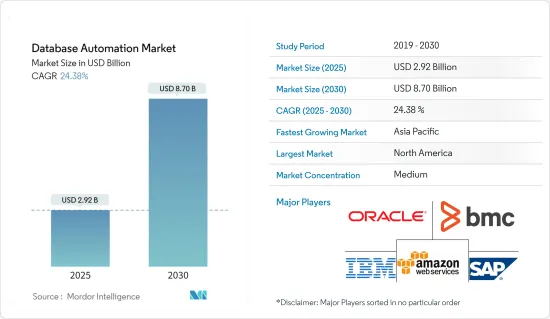

资料库自动化市场规模预计在 2025 年为 29.2 亿美元,预计到 2030 年将达到 87 亿美元,预测期内(2025-2030 年)的复合年增长率为 24.38%。

各行业资料量的不断增加、对冗余资料库库管理流程自动化的需求、自动化测试解决方案以及对上市速度的不断增长的需求预计将增加各行业对资料库自动化的需求。然而,当涉及资料建模和模式生成时,需要人工干预可能会阻碍成长。

主要亮点

- 自治资料库减少了忙于日常备份、扩展、调整、监控和保护关键资讯系统业务的技术专业人员所需的复杂性和时间。

- 当今的资料管道比以前的更加复杂。物联网等新资料来源、非结构化资料等格式以及 Apache Kafka 和 Python 等平台和语言正在创建更复杂的管道。资料库自动化利用人工智慧和机器学习为配置、安全性、更新、可用性、效能、变更管理和错误预防提供完整的端到端自动化,并包括查询最佳化、自动记忆体管理和储存管理,以提供完全自调整的资料库。

- 市场上的供应商采用灵活的计量收费模式对其产品定价,从而降低了维护内部资料仓储的成本。例如,中国运输、航运和物流公司嘉里大通就使用Oracle的自主资料库。该公司透过按使用计量收费模式,将分析超过 1 亿笔资料记录的时间从 30 分钟缩短到 10 秒,大幅降低了 IT 管理成本,并提高了投资收益。

- COVID-19 的蔓延导致世界各地实施封锁,关键任务应用程式和资料库位负载增加,给 IT 团队带来巨大压力,并导致资料库自动化的需求激增。随着需求的增加,供应商以低价提供免费工具和其他产品以吸引更多客户。由于各行各业资料的增加,资料库自动化市场预计将长期快速成长。

资料库自动化市场的趋势

IT和通讯业预计将大幅成长

- 通讯业是产生资料最多的行业之一,公司主要提供旨在大规模资料整合的云端服务。随着通讯业者对云端的需求不断增长,资料库自动化和通讯业者合作伙伴关係正在成为一种普遍趋势。例如,义大利电信业者Sielte SPA采用了Severalnines Cluster Control。 Severalnines Cluster Control 是一种运作资料库解决方案,可提供自动容错移转和復原功能,以最大限度地减少停机时间,并确保即使资料中心发生故障也能提供稳定的服务。

- 对机器学习 (ML) 和深度学习 (DL) 应用的巨大需求迫使资料库自动化供应商建立更全面的人工智慧 (AI) 产品。根据 Liquibase 所做的「应用程式交付中资料库采用状况」调查,57% 的应用程式变更都需要进行相应的资料库变更。在大型稀疏资料集上进行机器学习和深度学习,需要能够储存Terabyte资料并执行快速并行运算的资料管理系统,这使其非常适合资料自动化解决方案,因此在 IT 和通讯业迅速普及。

- 此外,软体开发人员和营运工程师越来越重视采用 DevOps 来自动化开发、部署、文件、检验和监控流程,整合开发和营运流程以有效地同步、验证、管理和应用资料库更改,这也推动了资料库自动化在行业中的成长。

- 此外,越来越多地采用公有和私有云端来有效管理大量资料,这也推动了对更好、更具成本效益的资料库自动化解决方案的需求。例如,Oracle 自治资料库将云端的灵活性与机器学习的强大功能结合在一起。该公司声称,该解决方案透过全面的营运自动化和调整可将管理成本降低高达 80%,并且透过仅在任何给定时间收费所需的资源费用可将运行时成本降低高达 90%。

预计北美将占很大份额

- 各大 IT 公司越来越多地采用巨量资料解决方案来简化和提高业务效率,这推动了企业办公室资料中心的扩张。因此,越来越多的公司,尤其是中小型企业,正在采用基于容器和微型资料中心,而不是传统的资料中心基础设施。由于该地区在技术采用方面的优势,这些趋势预计将进一步加速该地区资料库自动化市场的成长。

- 透过在二线城市进行模组化资料中心投资,该地区的资料中心基础设施解决方案正在持续成长。这些投资可能会推动资料中心基础设施管理解决方案提供者的崛起。美国正在采取多项措施来实现其基础设施的现代化。例如,美国计划投资约2.49亿美元用于私有云端运算服务和资料中心。

- 此外,加拿大政府还采用了「云端优先」策略,这意味着在启动任何资讯技术投资、计划、策略或计划时,云端服务将被确定和评估为主要交付选项。云端运算还有望使加拿大政府能够利用私人供应商的创新,并使其资讯技术更加灵活。

- 此外,加州的《消费者隐私法案》(CCPA)将于 2020 年初生效,这将增加资料库合规性的需求。这些因素共同推动了对自适应、安全和高效的资料库系统以及简单的资料库管理工具和流程的需求。

资料库自动化行业概览

资料库自动化市场处于半固体,主要参与者众多,竞争激烈。市场参与者正在采用合作和收购等策略,为客户提供最佳解决方案并获得竞争优势。高投资成本、现有参与者的存在以及不断发展的技术等因素对新进者构成了障碍。

- 2023 年 11 月综合资料库DevOps 供应商 Redgate 宣布推出 Redgate 测试资料管理器,它简化了测试资料管理 (TDM) 以及跨资料库的现代软体开发相关的挑战。

- 2023 年 10 月 - 无程式码、SaaS、受专利保护的文件产生、组装和工作流程自动化平台 Kim 推出应用程式产生器。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 对全球资料库自动化市场的影响

第五章 市场动态

- 市场驱动因素

- 各行业资料量不断增加

- 对自动化重复资料库管理流程的需求不断增加

- 市场挑战

- 需要人类参与

第六章 市场细分

- 按组件

- 解决方案

- 资料库补丁和发布自动化

- 自动化应用程式发布

- 资料库测试自动化

- 服务

- 解决方案

- 依部署方式

- 云

- 本地

- 按公司规模

- 大型企业

- 中小型企业

- 最终用户产业

- 银行、金融服务和保险(BFSI)

- 资讯科技和电讯

- 电子商务与零售

- 製造业

- 政府和国防

- 其他(製造、媒体和娱乐)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Oracle Corporation

- BMC Software, Inc.

- Amazon Web Services, Inc.

- SAP SE

- IBM Corporation

- IDERA, Inc.

- Quest Software Inc.

- Datavail

- CA Technologies(Broadcom Inc)

- Bryter US Inc.

第八章投资分析

第九章:市场的未来

The Database Automation Market size is estimated at USD 2.92 billion in 2025, and is expected to reach USD 8.70 billion by 2030, at a CAGR of 24.38% during the forecast period (2025-2030).

The increasing volume of data across industries, the need to automate redundant database management processes, automated testing solutions, and the growing need for faster speed to market is expected to grow the demand for database automation across industries. However, the need for human intervention when it comes to data modeling and schema generation might hinder growth.

Key Highlights

- While some technology professionals are still consumed with routine operations such as backing up, scaling, tuning, monitoring, and securing critical information systems, autonomous databases make these activities less complicated and time-consuming.

- Modern data pipelines are more complex than traditional ones. New data sources like IoT, formats such as unstructured data, and platforms and languages such as Apache Kafka and Python are creating more complex pipelines. Database automation leverages AI and machine learning to provide full, end-to-end automation for provisioning, security, updates, availability, performance, change management, and error prevention and includes query optimization, automatic memory management, and storage management to provide a completely self-tuning database.

- Vendors in the market are pricing their products on flexible pay-as-you-go pricing models, which reduces the costs of maintaining on-premises data warehouses. For instance, Kerry EAS, a Logistics, shipping, and logistics company in China, uses Oracle's autonomous database. The company reduced the time taken to analyze its 100 million-plus data records from 30 minutes to 10 seconds and significantly reduced IT management costs, and increased return on investment by leveraging the pay-as-you-go model.

- The spread of COVID-19 led to lockdowns in various parts of the globe, putting the IT teams under tremendous pressure due to increased digital loads on mission-critical applications and databases, spiking the demand for database automation. To acquire more customers during this increased demand, the vendors offered free tools and other offerings at a lower cost. The market is expected to grow rapidly in the long term as data grows across industries.

Database Automation Market Trends

IT and Telecommunication industry is Expected to Witness Significant Growth

- Telecom is among the sectors with the highest rate of data generation, and companies are offering cloud services mainly oriented to large-scale data integration. As the need for cloud is expanding among telecom clients, the partnership between database automation and telecom companies is becoming a common trend. For instance, Sielte S.P.A., an Italian Telecommunications company located in Italy, opted for Severalnines Cluster Control, a database solution that can operate 24x7 and offered automatic failover and recovery to minimize downtime and ensure a stable service even in the event of a data center going down.

- The increasing demand for applications leveraging machine learning (ML) and deep learning (DL) on a gigantic scale is anticipated to increasingly push database automation vendors to establish a more comprehensive array of artificial intelligence (AI). According to the State of Database Deployments in Application Delivery survey conducted by Liquibase, 57% of all application changes require a corresponding database change. Machine learning and deep learning on large, sparse data sets require a data management system that can store terabytes of data and perform fast parallel computations-tasks for which data automation solutions are ideally suited; hence is growing more rapidly in the IT and telecommunications industry.

- Moreover, increasing emphasis on implementing DevOps to automate the development, deployment, documentation, testing, and monitoring processes between software developers and operations engineers for integrating the development and operations processes to synchronize efficiently, validate, manage, and apply database changes is also proliferating the growth of database automation in the industry.

- Furthermore, the increasing adoption of public and private clouds to efficiently manage humongous data also increases the need for better and cost-effective database automation solutions. For instance, Oracle Autonomous Database combines the cloud's flexibility with machine learning's power. The company claims the solution can reduce administration costs by up to 80% with full operations automation and tuning and runtime costs by up to 90% by billing only for resources needed at any given time.

North America is Expected to Hold Major Share

- The increasing deployment of Big Data solutions by major IT enterprises to enhance efficiency and streamline their business operations is driving the expansion of data centers in corporate offices. Hence, these enterprises, mainly small and medium enterprises, are adopting containerized and micro data centers over conventional data center infrastructures. These trends are expected to augment further the growth of the database automation market in the region, owing to the dominance of the area in technology adoption.

- The region has maintained continued growth in data center infrastructure solutions through modular data center investments in tier-2 cities. These investments will enable data center infrastructure management solutions providers to rise. The United States has made several efforts to modernize its infrastructure. For instance, the US Army plans to invest approximately USD 249 million to deploy private cloud computing services and data centers.

- Moreover, the Government of Canada has a 'cloud-first' strategy, whereby cloud services are identified and evaluated as the principal delivery option when initiating information technology investments, initiatives, strategies, and projects. The cloud is also expected to allow the Government of Canada to harness the innovation of private-sector providers to make its information technology more agile.

- Moreover, Consumer Privacy Act (CCPA) takes effect at the start of 2020 in California, adding to the need for database compliance. The combination of all these factors indicates that companies will need adaptable, secure, efficient database systems, and simple database management tools and processes.

Database Automation Industry Overview

The database automation market is semi-consolidated owing to the presence of big players in the market and intense competition. The players in the market are adopting strategies such as partnerships and acquisitions to offer the best solutions to the customers and gain a competitive advantage. Factors such as high investment, the presence of established players, and continuously evolving technology act as barriers for new entrants in the market.

- November 2023: Redgate, the comprehensive database DevOps provider, launched Redgate Test Data Manager, which simplifies the challenges that come with Test Data Management (TDM) and modern software development across various databases.

- October 2023 - Kim, the no-code, SaaS, patent-protected document generation, assembly, and workflow automation platform, launched its Application Generator to allow individuals in organizations to generate complete web applications from their existing documents without IT development or coding skills and no false positive errors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 IMPACT OF COVID-19 ON THE GLOBAL DATABASE AUTOMATION MARKET

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Continuously Growing Volumes of Data Across Verticals

- 5.1.2 Increasing Demand for Automating Repetitive Database Management Processes

- 5.2 Market Challenges

- 5.2.1 The Need for Human Involvement

6 MARKET SEGMENTATION

- 6.1 Component

- 6.1.1 Solution

- 6.1.1.1 Database Patch and Release Automation

- 6.1.1.2 Application Release Automation

- 6.1.1.3 Database Test Automation

- 6.1.2 Services

- 6.1.1 Solution

- 6.2 Deployment Mode

- 6.2.1 Cloud

- 6.2.2 On-Premises

- 6.3 Enterprise Size

- 6.3.1 Large Enterprises

- 6.3.2 Small and Medium-Sized Enterprises

- 6.4 End-user Industry

- 6.4.1 Banking, Financial Services and Insurance (BFSI)

- 6.4.2 IT and Telecom

- 6.4.3 E-commerce and Retail

- 6.4.4 Manufacturing

- 6.4.5 Government and Defense

- 6.4.6 Others (Manufacturing, Media and Entertainment)

- 6.5 Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oracle Corporation

- 7.1.2 BMC Software, Inc.

- 7.1.3 Amazon Web Services, Inc.

- 7.1.4 SAP SE

- 7.1.5 IBM Corporation

- 7.1.6 IDERA, Inc.

- 7.1.7 Quest Software Inc.

- 7.1.8 Datavail

- 7.1.9 CA Technologies (Broadcom Inc)

- 7.1.10 Bryter US Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

资料库自动化市场:2026-2032年全球市场预测(依产品类型、部署模式、最终用户、销售管道和应用划分)

资料库自动化市场:2026-2032年全球市场预测(依产品类型、部署模式、最终用户、销售管道和应用划分) 2026年全球资料库自动化市场报告

2026年全球资料库自动化市场报告 资料库自动化市场规模、份额和成长分析(按组件、部署类型、资料库类型、组织规模、最终用户产业和地区划分)-2026-2033年产业预测

资料库自动化市场规模、份额和成长分析(按组件、部署类型、资料库类型、组织规模、最终用户产业和地区划分)-2026-2033年产业预测 全球资料库自动化市场:市场规模、份额、趋势分析(按组件、应用、最终用途和地区)、展望和预测(2025-2032 年)

全球资料库自动化市场:市场规模、份额、趋势分析(按组件、应用、最终用途和地区)、展望和预测(2025-2032 年) 资料库自动化市场规模、份额、趋势分析报告:按组件、应用、最终用途、地区和细分市场预测:2025 年至 2030 年

资料库自动化市场规模、份额、趋势分析报告:按组件、应用、最终用途、地区和细分市场预测:2025 年至 2030 年 资料库自动化市场:市场规模、市场占有率分析、趋势、推动因素、竞争格局和预测(2025-2030 年)

资料库自动化市场:市场规模、市场占有率分析、趋势、推动因素、竞争格局和预测(2025-2030 年)