|

市场调查报告书

商品编码

1644444

应用平台 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Application Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

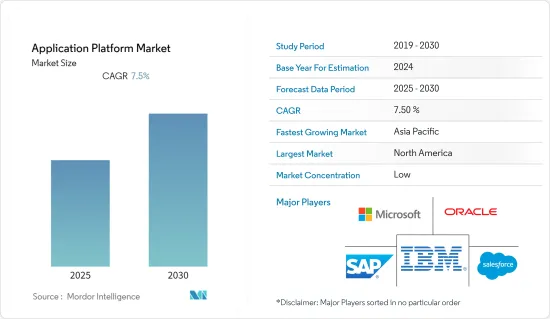

预计预测期内应用平台市场复合年增长率将达到 7.5%。

新冠疫情带来了积极影响,刺激了该行业的成长率,以满足应用开发的突然繁荣。

关键亮点

- 传统上,应用平台提供的服务有限。 IBM 大型主机等平台提供 CICS,而桌上型电脑仅提供基本的作业系统。当今的软体和硬体领域已大大扩展,为开发人员提供了多种选择。同样,应用平台现在也很广泛,支援各种各样的应用程式。它还允许您使用相同的工具和技能在不同的硬体上建立不同的应用程序,提供一致的体验。

- 应用平台在现代运算环境中发挥着至关重要的作用。这些平台利用其他应用程式和资料来记录资讯技术可以提供的所有价值。由于当今大多数组织都依赖应用程序,因此业务价值与应用程式平台之间存在着明显的关係。我们相信,案例将成为市场成长的主要驱动力之一。

- 此外,云端基础的应用平台正在推动软体产业的发展。 Workday、Salesforce 和 ServiceNow 等纯云端平台供应商都报告了强劲的成长。这些平台能够快速部署利用和融合人工智慧、自动化和分析等技术进步的应用程式。

- 此外,这些下一代平台的成功也为软体产业带来了压力。例如,Oracle、SAP和Microsoft等应用程式供应商不断投资这些新一代平台,以提供尖端的应用程式平台并留住现有客户并吸引新客户。

- 此外,在新冠肺炎疫情期间,各行各业的公司都在加快数位转型步伐。曾经预计需要数月或数年的时间的计划现在只需几天即可交付,因此快速建置、扩展和交付应用程式的能力至关重要。这对简化流程和消除耗时任务的工具和平台的需求日益增长。

应用平台市场趋势

预计云端基础服务的普及将推动市场

- 公司正逐渐致力于利用最新技术来减少整体资本支出。中小型企业正在采用云端基础的服务(例如 aPaaS 解决方案)来利用减少设定和人事费用以及最小化扩展成本等主要优势。云端基础的解决方案也使公司能够在需要的时候利用单一、通用的开发框架。

- 此外,资讯科技产业正在经历前所未有的变革,对直觉的面向客户的应用程式的需求日益增加。此外,由于需求不断增长,市场竞争日益激烈,市场速度成为许多公司的关键因素。

- 许多软体解决方案正在从本地转移到云端,到应用程式介面 (API) 和微服务的转变就是明证。随着技术堆迭的发展,PaaS 的出现也不断增加。与专注于中间件的传统 PaaS 解决方案相比,这些服务专注于应用开发和部署。

- PaaS 平台让开发人员可以存取迭代计划所需的所有工具。一些平台还提供直觉的功能,如拖放、热重加载以及第三方路径整合(如作业系统、资料库、漏洞管理等),以简化开发。此外,该平台还提供水平和垂直可扩展性,使企业有机会添加或升级资料库。

- 根据软体公司 HashiCorp 的一项调查,到 2021 年,90% 的大型企业受访者表示他们将采用多重云端。然而,中小型企业采用多重云端的速度较慢,主要是因为云端迁移预算有限。

北美占很大份额

- 由于美国等地区的技术市场已经成熟,预计北美将占据主要的市场占有率。许多私人公司正在进入混合 IT 服务的新时代,结合公共、私人和传统IT基础设施。这些公司正在采用多重云端策略来帮助他们改善业务和服务客户。

- 此外,COVID-19 疫情正加速美国各行各业公司对云端运算的采用。许多优先采用云端运算技术的美国公司表示,疫情只会让这项技术变得更加重要。

- 此外,受需求和快速交付软体服务的需求推动,技术支出也在增加。例如,美国市场强大的基础设施和平台,加上庞大的连网设备装置量和用户以及这些设备通讯的频宽,为软体和服务业的投资铺平了道路。

- 此外,软体和技术服务约占技术市场支出的一半,明显高于全球许多其他地区。这些案例显示市场前景乐观,预计将进一步推动该地区应用平台的采用。

- 此外,该地区的新兴企业正在推出新产品和服务以获得竞争优势。例如,美国新兴企业Fermyon 于 2022 年 10 月宣布已为其云端应用平台筹集了 2,000 万美元的早期资金。该新兴企业推出了其新的平台即服务 Fermyon Cloud,并宣布了其最新一轮资金筹措。它旨在让开发人员更轻鬆地使用 WebAssembly 建立云端应用程式。

- 此外,加拿大政府还采用了「云端优先」策略,该策略将在启动资讯技术投资、倡议、策略和计划时将云端服务确定并评估为主要交付选项。云端运算也使加拿大政府能够利用私人供应商的创新,并使其资讯技术更加灵活。这些努力有望为应用平台提供充足的机会。

应用平台产业概览

应用平台市场比较集中,有多家知名供应商。该市场的领先供应商正在利用其客户现有的应用程式投资并转向新的架构和程式设计范例。此外,供应商正在进行收购并增强其产品以保持市场竞争力。

2022年12月,Salesforce宣布在其基础架构上推出低程式码DevOps Center服务,为开发人员提供建置自订应用程式的意见平台。 Salesforce DevOps Center 服务是基于 Salesforce 用于建立其应用程式的相同物件模型。

2022 年 5 月,红帽宣布推出红帽应用程式基础。 Red Hat Application Foundations 与 Red Hat OpenShift 一起,是一组连接的应用程式服务,有助于加速混合和多重云端环境中容器化应用开发和交付。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 对市场的影响

第五章 市场动态

- 市场驱动因素

- 云端基础服务日益普及

- 市场限制

- 新兴国家的技能水准较低

第六章 市场细分

- 按类型

- 软体

- 服务

- 按组织规模

- 中小型企业

- 大型企业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第七章 竞争格局

- 公司简介

- International Business Machines Corporation

- Microsoft Corporation

- Oracle Corporation

- Salesforce.com Inc.

- BMC Software Inc.

- Google LLC(Alphabet Inc)

- Micro Focus International Plc

- GigaSpaces Technologies Ltd.

- SAP SE

第八章投资分析

第九章:市场的未来

The Application Platform Market is expected to register a CAGR of 7.5% during the forecast period.

The COVID-19 pandemic positively impacted the industry as it fueled its growth rate to satisfy the sudden boom in application development.

Key Highlights

- Traditionally, application platforms offered restricted services; platforms such as IBM mainframe offered CICS, and desktop PC only offered basic operating systems. Today, software and hardware environments have expanded significantly, and developers often have many options. Similarly, application platforms are now broad and support all kinds of applications. They also provide a consistent experience by enabling the same tools and skills to create different applications on diverse hardware.

- Application platforms play a vital role in modern computing environments. These platforms leverage other applications and data to provide all the value that information technology brings, and also virtually every other application depends on an application platform. Since most organizations today rely on applications, there's a clear connection between business value and application platforms. This instance vows to be one of the primary drivers for the growth of the market.

- Also, cloud-based application platforms are gaining traction in the software industry. Pure cloud platform vendors such as Workday, Salesforce, and ServiceNow have been reporting significant growth. These platforms allow for the faster deployment of applications leveraging and embedding technological advancements such as AI, automation, and analytics.

- Further, owing to the success of these next-generation platforms, the software industry is under pressure. For instance, application vendors such as Oracle, SAP, and Microsoft have been continuously investing in these generation platforms as they aim to provide state-of-the-art application platforms to help retain their existing customers and further attack new customer segments.

- Additionally, amidst the COVID-19 situation, businesses across industries have fast-tracked their digital transformation initiatives. The projects that were scoped to occur over months and years are now aimed to take place in a matter of days, and the ability to build, scale, and ship applications fast has become imperative. Thereby, there is a growing need for tools and platforms that streamline processes and eliminate time-consuming tasks.

Application Platform Market Trends

Growing Popularity of Cloud-based Services is Expected to Drive the Market

- Companies are gradually focusing on decreasing their overall capital expenditure by using modern technologies. Small and medium enterprises are adopting cloud-based services such as aPaaS solutions to leverage vital benefits, including reduced setup and labor costs and minimized expansion costs. Also, cloud-based solutions enable enterprises to use a single, all-purpose development framework as pay-per-need and pay-per-use.

- Moreover, the Information Technology industry is undergoing unprecedented change with the growing demand for intuitive customer-facing applications. Further, owing to the ever-increasing demand, there is an increase in competition, and speed in the market has become a crucial factor for many businesses.

- Many software solutions have been transformed from on-premises into the cloud, evidenced by the transition towards application programming interfaces (APIs) and microservices. As technology stacks developed, there was growth in the emergence of PaaS. These services offer application development and deployment compared to traditional PaaS solutions focusing on middleware.

- aPaaS platforms provide developers access to all the necessary tools that are required to iterate projects. Some platforms also offer intuitive features such as drag and drag, hot reloading, and other 3rd path integrations like operating systems, databases, and vulnerability management, making development easier. Further, the platform also offers horizontal and vertical scalability thus, providing businesses an opportunity to additionally add and upgrade their databases.

- According to a survey by HashiCorp, a software company, in 2021, 90 percent of respondents from large enterprises indicated that they have already adopted the multi cloud. However, smaller businesses are lagging behind in terms of multi-cloud adoption mainly due to the fact that they have smaller budgets for cloud migrations.

North America to Hold Major Share

- North America is expected to hold a significant market share majorly due to the mature tech market in regions such as the United States. Many regional companies are stepping into a new era of hybrid IT services that combine public, private, and traditional IT infrastructure. These organizations have implemented a multi-cloud strategy as it is aiding them in improving their business and delivering services to customers.

- Additionally, the COVID-19 pandemic has accelerated cloud usage for US companies in every industry. Many US enterprises prioritizing cloud adoption in their organization noted the increased importance of cloud due to the pandemic.

- Also, there has been a trend of increasing technological spending driven by demand and the need for software services' speedy delivery. For instance, robust infrastructure and platforms in the US market coupled with a large installed base of users with connected devices and bandwidth for these devices to communicate have paved the way for software and service industry investments.

- Moreover, software and tech services account for around half of the technology market spending, which is significantly higher than that of most other global regions. These instances showcase the positive outlook of the market and are expected to drive further the application platform's adoption in the region.

- Further, emerging companies in the region are introducing new products or services to gain a competitive advantage. For instance, in October 2022, a United States-based start-up, Fermyon announced that is had raised USD 20 million in early-stage funding for its cloud application platform. The startup announced its latest funding round by introducing Fermyon Cloud, a new platform-as-a-service offering. It is designed to make it easier for developers to build cloud applications using WebAssembly.

- Moreover, the Government of Canada has a "cloud-first" strategy whereby cloud services are identified and evaluated as the principal delivery option when initiating information technology investments, initiatives, strategies, and projects. The cloud will also allow the Government of Canada to harness the innovation of private-sector providers to make its information technology more agile. Such initiatives are expected to provide ample opportunities for the application platform.

Application Platform Industry Overview

The Application Platform Market is moderately consolidated with the presence of prominent vendors, among others. The prominent vendors in the market are leveraging the customer's existing application investments toward the transition to emerging architectures and programming paradigms. Further, the vendors are embracing acquisitions and product enhancements to maintain their competitive position in the market.

In December 2022, Salesforce announced the availability of a low-code DevOps Center service on its infrastructure, providing developers with an opinionated platform for building custom applications. The Salesforce DevOps Center service is based on the same object model that Salesforce uses to construct its applications.

In May 2022, Red Hat announced Red Hat Application Foundations, a connected set of application services that, together with the Red Hat OpenShift, help accelerate containerized application development and delivery across hybrid and multi-cloud environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Popularity of Cloud-based Services

- 5.2 Market Restraints

- 5.2.1 Low Skillset in Emerging Economies

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Organization Size

- 6.2.1 Small and Medium-Sized Enterprises

- 6.2.2 Large Enterprises

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Business Machines Corporation

- 7.1.2 Microsoft Corporation

- 7.1.3 Oracle Corporation

- 7.1.4 Salesforce.com Inc.

- 7.1.5 BMC Software Inc.

- 7.1.6 Google LLC (Alphabet Inc)

- 7.1.7 Micro Focus International Plc

- 7.1.8 GigaSpaces Technologies Ltd.

- 7.1.9 SAP SE