|

市场调查报告书

商品编码

1644458

美国一次性包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)US Single Use Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

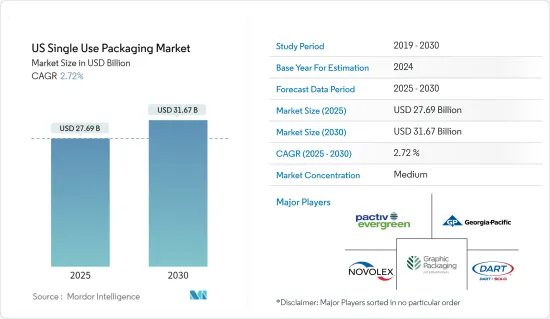

预计2025年美国一次性包装市场规模为276.9亿美元,到2030年预计将达到316.7亿美元,预测期内(2025-2030年)的复合年增长率为2.72%。

由于一次性包装的便利性和易于印刷,预计该国对一次性包装的需求将会上升。现在一些企业要求使用一次性塑胶包装,以避免交叉污染和疾病。一次性包装市场扩张预计将加速。

关键亮点

- 对小型、便利包装和强烈视觉衝击力的需求日益增长,预计将在预测期内推动一次性包装的成长。一次性包装是指仅使用一次就被丢弃或回收的产品。例如塑胶袋、吸管、咖啡搅拌棒、汽水瓶和水瓶以及大多数食品包装。

- 美国软质塑胶包装产业正在经历健康成长,因为它已经针对其面临的一些包装挑战实施了创新解决方案。据软包装协会(FPA)称,品牌所有者越来越多地采用小袋、薄膜和袋子作为包装解决方案,部分原因是美国消费者越来越接受这些产品。

- 医药产业正在推动国内一次性塑胶包装市场的扩张。医疗设备、消耗品、注射器和药品通常采用一次性塑胶包装,以减少污染的机会并保护最终用户的利益。此外,由于各种尺寸包装产量不断增加,以满足对瓶装水、软性饮料、酒精饮料、即饮饮料和牛奶日益增长的需求,一次性塑胶饮料容器的市场预计将增长。

- 然而,一次性塑胶包装的一个日益严重的问题包括废弃物和处置管理。不当处置会带来环境风险并增加塑胶废弃物。这可能会阻碍该国的一次性塑胶包装市场的发展。

- 美国电子商务发展显着加速,部分原因是新冠疫情导致的封锁。但2020年初疫情严重打击了零售业。这些因素对美国零售业软质塑胶包装的使用产生了负面影响。不过,美国零售业在2020年下半年出现了大幅成长,推动了该地区一次性软质塑胶包装使用量的復苏。此外,俄乌战争正在影响整个包装生态系统。

美国一次性包装市场的趋势

柔性、一次性塑胶包装产品提供便利和实用性

- 根据Biologicaldiversity.org报道,美国人每年使用1000亿个塑胶购物袋,生产这些塑胶袋需要1200万桶(19.785亿公升)石油。美国人平均每年使用365个塑胶购物袋。丹麦人平均每年使用四个塑胶购物袋。

- 此外,冠状病毒的传播暂时增加了一次性塑胶的采用,因为一次性塑胶具有阻隔性。主要用户是餐厅、杂货店和电子商务供应商。杂货店的塑胶购物袋使用量正在激增。家庭垃圾量比疫情前高出50%,显示需求增加。儘管如此,一旦各州恢復到接近正常的状态,并实施新冠疫情之前的法规禁止使用一次性塑料,这些包装材料的流通预计就会减少。

- 当一次性包装与快餐店(QSR)中的可重复使用的餐具进行比较时,一次性系统具有优势,特别是在碳排放和淡水消费量方面。这是因为清洗、消毒和干燥多次使用的餐具需要消耗能源和水。在基准情境下,与纸质一次性系统相比,聚丙烯基多用途系统排放的二氧化碳多 2.5 倍,使用的淡水多 3.6 倍。

- 因此,如果市场供应商推出可回收性更高的包装或加入有助于分解的材料,一次性塑胶市场就可以实现永续发展。由于上述担忧,新参与企业正在进入市场,推出生物基一次性塑胶产品。

- 据ITC称,2021年塑胶废弃物和废料的进口额约为368,729,000美元,与前一年同期比较增58.28%,显示将塑胶碎片转化为一次性塑胶的需求增加。

医疗及製药领域呈现显着成长率

- 一次性包装、塑胶包装材料使用量的增加以及疫情期间对医疗产品和包装的需求增加,导致全球塑胶废弃物产生量大幅增加。出于卫生方面的考虑,主要需求之一是处理 RT-PCR 冠状病毒检测套组中的塑胶零件。

- 全球已禁止使用一次性塑料,但由于担心重复使用塑胶袋和容器会造成交叉污染,美国等国家已被迫在新冠肺炎疫情期间暂时废除或推迟对一次性塑料的禁令。此外,纽约州于2020年3月开始全面禁止使用塑胶购物袋,但受疫情影响,禁令于2020年5月被搁置。加州和奥勒冈州也暂停了塑胶袋禁令,康乃狄克州、德拉瓦、夏威夷州、新泽西州、新墨西哥州、奥勒冈州和华盛顿州均推迟了类似的禁令。

- 大多数 PPE 由聚氨酯 (PU)、聚丙烯 (PP)、聚碳酸酯 (PC)、低密度聚乙烯 (LDPE) 和聚氯乙烯(PVC) 等聚合物製成。 PS和LDPE很少被回收,而PET和HDPE被广泛回收,PVC和PP通常不会被回收。

- 需要有效的材料来最好地满足广泛的医疗需求,同时也考虑到环境影响。然而,找到合适且价格合理的塑胶替代品,同时保持保护患者和员工所需的无菌和卫生,可能是一个挑战。人口的成长给及时大规模运送医疗物资的能力带来了额外的压力。因此,一次性塑胶预计将继续在医疗保健领域占据较大份额。

- 据 CMS 称,到 2028 年,人均医疗保健支出预计将超过 17,000 美元。医疗保健支出的增加可能会推动市场采用无菌产品,一次性包装公司的数量将会增加,从而推动製药业的显着成长。

美国一次性包装产业概况

美国一次性包装市场适度整合,拥有几个主要企业,包括 Dart Container Corporation、Georgia-Pacific LLC、Graphic Packaging International Inc 和 Novolex,以及一些新参与企业。公司不断创新并建立战略伙伴关係以保持市场占有率。

2022年7月,乔治亚太平洋公司百老汇工厂获得5亿美元扩建投资。此项投资将显着改善公司的消费用纸及毛巾零售业务。我们将建造一座采用热风干燥(TAD)技术的新造纸厂,并增加相关基础设施和转换工具。乔治亚太平洋公司的高端品牌将能够发展,而且该公司的高端自有品牌产品以及其现有和未来客户的产品都将透过这项变革得到支持。预计竣工日期为 2024 年

2022 年 4 月,Georgia-Pacific 将在乔治亚麦克多诺和宾夕法尼亚州约翰斯敦破土动工建立新工厂,生产其原创的可回收纸质填充信封。加上其凤凰城地区工厂新增的第三条生产线,Georgia-Pacific 的生产能力提高了两倍多,以满足对更环保的电子商务包装解决方案日益增长的需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 工业供应链分析

- 产业吸引力-波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要标准及法规

- COVID-19 市场影响评估

- 全球一次性包装市场概览

第五章 市场动态

- 市场驱动因素

- 持续的轻量化趋势和永续解决方案的使用(例如纸杯)

- 灵活的一次性包装产品提供便利性和实用性

- 市场问题

- 严格的监管是一次性塑胶包装产品成长的主要限制因素

- 一次性塑胶是一个日益严重的环境问题

第六章 市场细分

- 按材质

- 纸和纸板

- 塑胶

- 铝

- 其他的

- 按最终用户产业

- 食物

- 饮料

- 医疗药品

- 个人护理

- 其他的

第七章 竞争格局

- 公司简介

- Dart Container Corporation

- Georgia-Pacific LLC

- Graphic Packaging International Inc.

- Novolex

- Pactiv LLC

- Snapsil Corporation

- Berry Global Inc.

- Amcor Plc

- PPC Flexible Packaging LLC

- Fuling Plastic USA, Inc.

第八章投资分析

第九章:市场的未来

The US Single Use Packaging Market size is estimated at USD 27.69 billion in 2025, and is expected to reach USD 31.67 billion by 2030, at a CAGR of 2.72% during the forecast period (2025-2030).

The demand for single-use packaging in the country is anticipated to increase due to its high convenience and printability. Single-use plastic packaging is required by several businesses to avoid cross-contamination and disease. It will accelerate the expansion of the market for single-use packaging.

Key Highlights

- The increasing need for small and more convenient packaging and a strong visual impact is expected to contribute to the growth of single-use packaging over the forecast period. Single-use packaging is for products used only once before they are thrown away or recycled. These items are plastic bags, straws, coffee stirrers, soda and water bottles, and most food packaging.

- The United States' flexible plastic packaging industry is witnessing healthy growth as it implemented innovative solutions for the several packaging challenges it faced. According to the Flexible Packaging Association (FPA), brand owners are adopting pouches, films, and bags as a go-to packaging solution, partly due to rising acceptance by American consumers.

- The pharmaceutical industry is driving the expansion of single-use plastic packaging in the nation's market. Medical equipment, supplies, syringes, and medications are frequently packaged in single-use plastic since it decreases the possibility of contamination, protecting the end-users interests. Further, the market for single-use plastic beverage containers is predicted to expand due to the rising production of various package sizes to meet the growing demand for bottled water, soft drinks, alcoholic beverages, ready-to-drink beverages, and milk.

- However, growing issues with single-use plastic packaging include waste and disposal management. Environmental risks and a rise in plastic waste result from improper disposal. It will probably hamper the market for single-use plastic packaging in the country.

- The United States has witnessed a significant acceleration in e-commerce, driven by lockdowns imposed due to the outbreak of COVID-19. However, the pandemic made a dent in retail sales at the start of 2020. Such factors negatively impacted the usage of flexible plastic packaging in the US retail landscape in the respective months. However, the retail sector in the United States witnessed a significant surge in late 2020, which bounced back the usage of single-use flexible plastic packaging in the region. Further, the Russia-Ukraine war has an impact on the overall packaging ecosystem.

US Single Use Packaging Market Trends

Flexible Single-use Plastic Packaging Products Offering Increased Convenience and Utility

- According to Biologicaldiversity.org, American citizens use 100 billion plastic bags annually, which require 12 million barrels (1907.85 million liters) of oil to manufacture. Americans use an average of 365 plastic bags per person per year. People in Denmark use an average of four plastic bags per year.

- Moreover, the spread of coronavirus has temporarily increased the adoption of single-use plastic due to its barrier properties. The primary users are restaurants, grocery stores, and e-commerce vendors. Grocery stores have sharply increased plastic bag usage. Households are generating up to 50% more waste by volume than pre-pandemic, indicating increased demand. Still, as soon as the state achieves near-normal scenarios, the pre-covid established regulations to ban single-use plastics are expected to subside the circulation of these packaging materials.

- In comparing single-use packaging to reusable tableware in quick-service restaurants (QSR), single-use systems have their advantages, particularly in carbon emissions and freshwater consumption. These are due to the energy and water needed to wash, sanitize, and dry multi-use tableware. In the baseline scenario, the polypropylene-based multi-use system generated over 2.5 times more CO2 emissions and used 3.6 times the amount of freshwater than the paper-based single-use system.

- As a result, the market for single-use plastics might sustain if the vendors in the market introduce packaging with higher recycling rates or include materials that help in decomposition. The above concerns have led to the entry of new players in the market that are introducing bio-based single-use plastic products.

- According to the ITC, in 2021, the value of imports of plastic waste and scrap amounted to around USD 368.729 million, a 58.28% growth in imports from the previous year, indicating the demand for an increase in the transformation of plastic debris to single-use plastic.

Healthcare and Pharmaceutical Segment to Witness Significant Growth Rates

- The growing usage of single-use packaging, plastic-based packaging materials, and the increasing demand for medical products and packaging amid the pandemic has significantly spiked plastic waste generation worldwide. One primary need was disposing plastic-based parts of the coronavirus testing kits employing RT-PCR for hygienic concerns.

- Although single-use plastics are increasingly banned worldwide, concerns of cross-contamination by reusing plastic bags and containers have forced countries like the United States to temporarily revoke or defer bans on single-use plastics during the COVID-19 pandemic. Further, a statewide ban on plastic bags in New York initiated in March 2020 was put on hold in May 2020 owing to the pandemic. California and Oregon also suspended their bans on plastic bags, while Connecticut, Delaware, Hawaii, New Jersey, New Mexico, Oregon, Washington, etc., postponed similar prohibitions.

- The majority of PPEs are made up of polymers like polyurethane (PU), polypropylene (PP), polycarbonate (PC), low-density polyethylene (LDPE), and polyvinyl chloride (PVC). PS and LDPE are rarely recycled plastics; PET and HDPE are widely recycled, while PVC and PP are often not recycled.

- An effective material is needed to meet the vast healthcare needs best while considering its influence on the environment. However, maintaining the degree of sterility and sanitation necessary for protecting patients and employees while identifying appropriate and reasonably priced alternatives to plastic is difficult. The growing population puts extra strain on the ability to provide medical supplies on a large scale and on time. Thus, it is anticipated that single-use plastics will continue contributing significant shares in the healthcare sector.

- According to the CMS, national health expenditure per capita is expected to exceed USD 17,000 in 2028. The increase in the health expenditure values may drive the market by necessitating the adoption of sterilizing products increasing the number of single-use packaging companies to witness significant growth in the pharmaceutical sector.

US Single Use Packaging Industry Overview

The single-use packaging market in the United States is moderately consolidated, with new firms entering the market as well as the entry of a few dominant firms, including Dart Container Corporation, Georgia-Pacific LLC, Graphic Packaging International Inc, Novolex, and others. The firms keep innovating and entering strategic partnerships to retain their market share.

In July 2022, Georgia-Pacific's Broadway mill received an investment of USD 500 million for expansion. The expenditures will significantly improve the company's retail consumer tissue and towel business. Through-air-dried (TAD) technology is being used to construct a new paper mill and add related infrastructure and conversion tools. Georgia-Pacific's premium brands will be able to grow, and their premium private label products, as well as those of present and future clients, will be supported by the changes. 2024 is the projected completion date.

In April 2022, Georgia-Pacific constructed new facilities in McDonough, Georgia, and Jonestown, Pennsylvania, where they will manufacture an original, recyclable paper-padded envelope. Georgia-Pacific has more than tripled its capacity to help satisfy the rising demand for more environmentally friendly e-commerce packaging solutions when paired with the newly increased manufacturing capacity of a third production line at the company's factory in the Phoenix region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Standards and Regulations

- 4.5 Assessment of Impact of COVID-19 on the Market

- 4.6 Overview of the Global Single-use Packaging Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Ongoing Trend Toward Lightweight and Use of Sustainable Solutions (such as Paper-based Cups)

- 5.1.2 Flexible Single-use Packaging Products Offering Increased Convenience and Utility

- 5.2 Market Challenges

- 5.2.1 Stringent Regulations as Major Impediment to the Growth of Single-use Plastic Packaging Products

- 5.2.2 Rising Environmental Concerns due to Single-use Plastic

6 Market Segmentation

- 6.1 By Material

- 6.1.1 Paper and Paperboard

- 6.1.2 Plastics

- 6.1.3 Aluminium

- 6.1.4 Other Materials

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare and Pharmaceutical

- 6.2.4 Personal Care

- 6.2.5 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dart Container Corporation

- 7.1.2 Georgia-Pacific LLC

- 7.1.3 Graphic Packaging International Inc.

- 7.1.4 Novolex

- 7.1.5 Pactiv LLC

- 7.1.6 Snapsil Corporation

- 7.1.7 Berry Global Inc.

- 7.1.8 Amcor Plc

- 7.1.9 PPC Flexible Packaging LLC

- 7.1.10 Fuling Plastic USA, Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球一次性包装市场报告

2026年全球一次性包装市场报告 一次性包装:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

一次性包装:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年) 一次性包装市场按材料类型、最终用户行业和地区划分

一次性包装市场按材料类型、最终用户行业和地区划分 2025-2034 年一次性包装市场机会、成长动力、产业趋势分析与预测

2025-2034 年一次性包装市场机会、成长动力、产业趋势分析与预测