|

市场调查报告书

商品编码

1644482

欧洲工业自动化软体市场:份额分析、产业趋势与统计、成长预测(2025-2030 年)Europe Industrial Automation Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

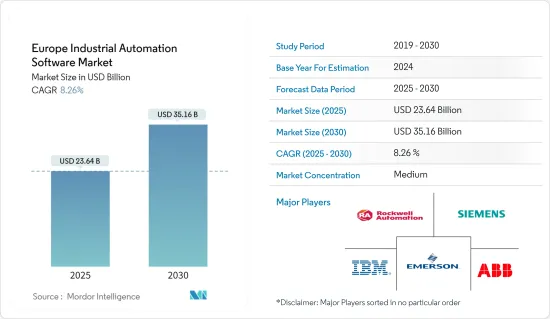

预计 2025 年欧洲工业自动化软体市场规模为 236.4 亿美元,到 2030 年将达到 351.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.26%。

工业自动化有助于减少每项任务所需的机器工作时间,但这只有透过强大的软体才有可能实现。

主要亮点

- 人工智慧(AI)和机器人技术的最新趋势旨在协助甚至完全自动化许多行政和社会任务。在市场发展迅速的欧洲,服务机器人的使用也与工业机器人一起增加。

- 欧盟的许多研究与创新 (R&I) 计画一直支持解决方案和技术的开发,使欧洲製造业能够充分利用数位机会。其中许多计划由未来工厂官民合作关係,涵盖数位自动化、製造资产流程优化、模拟和分析技术以及製造业中小企业的资讯通信技术创新等领域。

- 欧洲市场在新创企业、合作和收购方面的投资正在增加。预计各地区政府的进一步投资将推动基于客户端的软体解决方案的需求,以满足中小企业和大型组织日益增长的需求。

- COVID-19 疫情推动了工业 4.0 的广泛应用,该技术采用了多种智慧製造技术。数位化工作流程和自动化不再是一个目标,而正在成为一种要求。物联网设备为製造商提供了在疫情期间维持收益来源的方法。为应对公共卫生危机,对智慧製造产品和服务的需求不断增长,预计将推动进一步成长。

欧洲工业自动化软体市场趋势

严格的节能标准和本地加工推动欧洲市场

- 在欧洲,各国对能源消耗的监管日益加强,包括推出严格的节能标准、推广本地加工等,正在推动该地区工业自动化软体的成长。日益动态的工业需求要求复杂的操作和流程,以及日益减少特定操作所需的机器运作的需求,也正在推动欧洲对工业自动化软体的需求。

- 2022 年 5 月,欧盟委员会公布了 REPowerEU 计画的细节,该计画旨在重振欧洲并减少和结束欧洲对俄罗斯石化燃料的依赖。欧盟委员会旨在透过三大支柱加速欧洲的清洁能源转型,即能源效率、供应源多样化和石化燃料的快速替代,实现这一目标。这些区域措施正在推动所研究市场对工业自动化的需求。

- 此外,德国电网难以适应日益增长的可再生能源和分散式能源,许多大型电力计划被搁置。同时,各国政府也正在努力使电网适应新的需求。四大国家电网营运商为提高输电能力所采取的措施总额将达到 500 亿美元。这可能会增加使用 PLC 累积资料并采取进一步的连续措施,从而刺激市场研究。

- 自动化软体还帮助欧洲终端用户产业控制整个製造业务并精确地交付高品质的产品。有效实施自动化软体可以帮助最大限度地减少流程故障,降低产品故障成本和浪费。

汽车产业工业自动化应用的增加将对市场产生正面影响

- 智慧工厂为汽车产业提供了更快回应市场需求、减少製造停工时间、简化供应链和提高生产力的机会。汽车产业是全球自动化生产设施占比最大的产业之一。

- 为了保持效率,各汽车製造商的生产设施正在自动化。电动车取代传统汽车的趋势日益增长,预计将进一步增加汽车产业的需求。

- 在汽车製造厂实施工业控制系统软体,使公司能够透过工厂连接产生的资料即时追踪生产力和质量,为生产线监督和工厂高管提供缓解措施。

- 此外,汽车组装配对采用自动化的需求庞大,将使生产的汽车数量呈现成长模式,同时降低成本。此外,该领域对智慧工厂的采用显着增加,对工业自动化软体产生了巨大的需求。

欧洲工业自动化软体产业概况

欧洲工业自动化软体市场被认为是一个中等整合的市场,拥有大量参与者。然而,大部分市占率被少数几家公司瓜分,例如:西门子股份公司、ABB 有限公司、IBM 公司、艾默生电气公司和罗克韦尔自动化公司。

2022年4月,ABB与Savannah Resources PLC签署了一份谅解备忘录,开始为Savannah位于葡萄牙北部的Barroso锂计划开发探索工业自动化和智慧电气化解决方案。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 全球工业自动化软体市场分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 推出严格节能标准,推动各地就地加工

- 大规模生产的需求不断增加,同时营运成本也不断降低

- 在工业环境中采用物联网和人工智慧等新技术

- 市场挑战

- 贸易紧张局势与货币政策收紧

- 实施工厂自动化解决方案的成本高

第六章 COVID-19 对市场的影响

第七章 市场区隔

- 依软体类型

- 製造执行系统(MES)

- 资产绩效管理 (APM)

- 先进製程控制 (APC)

- 产品生命週期管理 (PLM)

- 操作员训练模拟器(OTS)

- 工业控制系统软体(营运和网路安全)

- 按最终用户产业

- 石油和天然气

- 化工和石化

- 力量

- 用水和污水

- 饮食

- 汽车与运输

- 其他最终用户产业

- 按国家

- 德国

- 法国

- 英国

- 义大利

- 东欧(包括俄罗斯和土耳其)

- 其他欧洲国家

第八章 竞争格局

- 公司简介

- Siemens AG

- ABB Ltd

- IBM Corporation

- Emerson Electric Co.

- Rockwell Automation Inc.

- OMRON Corporation

- Yokogawa Electric Corporation

- Koyo Electronic Industries Co. Ltd

- Daifuku Co. Ltd

- Honeywell International Inc.

第九章投资分析

第十章:市场的未来

The Europe Industrial Automation Software Market size is estimated at USD 23.64 billion in 2025, and is expected to reach USD 35.16 billion by 2030, at a CAGR of 8.26% during the forecast period (2025-2030).

Industrial automation helps in reducing the machine hours required for the respective operations, which can be made possible only through robust software.

Key Highlights

- Recent developments in artificial intelligence (AI) and robotics aim to assist, or even completely automate, many clerical and social interaction tasks. Along with industrial robots, the use of service robots is increasing in the fast-developing market of the European region.

- Many of the EU's research & innovation (R&I) programs have constantly supported the development of solutions and technologies that enable the European manufacturing sector to utilize digital opportunities fully. Many of the projects are financed by the Factories of the Future Public-Private Partnership as they cover areas such as digital automation, process optimization of manufacturing assets, simulation and analytics technologies, and ICT innovation for manufacturing SMEs.

- The market in Europe experiences high investments in terms of new developments, partnerships, and acquisitions. Further investment by various regional governments is expected to increase the need for client-based software solutions to meet the rising demands of SMEs and larger organizations.

- The COVID-19 pandemic brought significant adoption of Industry 4.0, which utilizes several smart manufacturing technologies. Digital workflows and automation are no longer goals; they are becoming necessary requirements. IoT devices offered manufacturers a path toward preserving revenue streams during the pandemic. Rising demand for smart manufacturing products and services in response to the public health crisis is expected to drive further growth.

Europe Industrial Automation Software Market Trends

Launch of Stringent Energy Conservation Standards and the Drive for Local Processing is Driving the Market in Europe

- The growing regulations on energy consumption across the country, with the launch of strict energy conservation standards and the drive for local processing in Europe, are driving the growth of industrial automation software in the region. The increasingly dynamic needs of the industry, demanding complex operations and processes, and the need to reduce machine hours required for a specific operation are also driving the demand for industrial automation software in Europe.

- In May 2022, the European Commission presented details of its plan, the REPowerEU Plan to repower Europe and reduce and end Europe's reliance on Russian fossil fuels. The European Commission aims to make it possible with three pillars of energy conservation, diversifying supplies, and quickly substituting fossil fuels by accelerating Europe's clean energy transition. Such regional initiatives drive the demand for industrial automation in the market studied.

- Moreover, the electricity grid in Germany is struggling to cope with the extent of renewable and distributed energy in the country, and many major power projects are on hold. At the same time, the government has attempted to adapt the grid to the new demands placed upon it. The measures by the four national grid operators to boost power transmission capacity sufficiently add up to a cost of USD 50 billion. This is likely to escalate the usage of PLC to accumulate data and further take successive measures, thereby fueling the market studied.

- Automation software also helps end-user industries in Europe control the overall manufacturing operations and deliver high-quality products with high precision. The effective deployment of automation software minimizes process failures and reduces product failure costs and waste.

Increasing Use of Industrial Automation in the Automotive Sector Positively Impacts the Market

- Smart factory offers the automotive industry opportunities to react faster to market requirements, reduce manufacturing downtimes, enhance the efficiency of supply chains, and expand productivity. The automotive industry is among the prominent sectors that hold a significant share of the world's automated manufacturing facilities.

- The production facilities of various automakers are automated to maintain efficiency. The growing trend of replacing conventional vehicles with EVs is expected to augment the automotive industry's demand further.

- The implantation of industrial control systems software in auto manufacturing plants allows companies to keep real-time track of productivity and quality through the data generated through plant connectivity and provides mitigating actions to the line supervisors and plant executives.

- Moreover, auto assembly witnessed substantial demand employing automation, showing a growth pattern in the number of cars manufactured while simultaneously cutting costs. Furthermore, the smart factory implementation in this sector has increased considerably, creating significant demand for industrial automation software.

Europe Industrial Automation Software Industry Overview

The Europe industrial automation software market is considered a moderately consolidated market with many players. However, a majority share of the market is divided among a few players such as Siemens AG, ABB Ltd., IBM Corporation, Emerson Electric Co., and Rockwell Automation. Innovations in the market require the developers to understand the industrial process better to deliver a suitable solution and drive close collaboration among the stakeholders during development and customization to suit the end users' needs.

In April 2022, ABB signed a memorandum of understanding (MOU) with Savannah Resources PLC to explore industrial automation and smart electrification solutions for developing Savannah's Barroso Lithium Project in northern Portugal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Global Industrial Automation Software Market Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Launch of Stringent Energy Conservation Standards and Drive for Local Processing Across Various Geographies

- 5.1.2 Growing Need for Mass Production with Reduced Operating Costs

- 5.1.3 Adoption of Emerging Technologies such as IoT and AI in Industrial Environments

- 5.2 Market Challenges

- 5.2.1 Trade Tensions and Monetary Policy Tightening

- 5.2.2 High Cost of Implementing Factory Automation Solutions

6 IMPACT OF COVID-19 ON THE MARKET

7 MARKET SEGMENTATION

- 7.1 Type of Software

- 7.1.1 Manufacturing Execution Systems (MES)

- 7.1.2 Asset Performance Management (APM)

- 7.1.3 Advanced Process Control (APC)

- 7.1.4 Product Lifecycle Management (PLM)

- 7.1.5 Operator Training Simulator (OTS)

- 7.1.6 Industrial Control Systems Software (Operational and Cybersecurity)

- 7.2 End-user Industry

- 7.2.1 Oil and Gas

- 7.2.2 Chemical and Petrochemical

- 7.2.3 Power

- 7.2.4 Water and Wastewater

- 7.2.5 Food and Beverage

- 7.2.6 Automotive and Transportation

- 7.2.7 Other End-user Industries

- 7.3 Country

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 United Kingdom

- 7.3.4 Italy

- 7.3.5 Eastern Europe (Including Russia and Turkey)

- 7.3.6 Rest of Western Europe

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Siemens AG

- 8.1.2 ABB Ltd

- 8.1.3 IBM Corporation

- 8.1.4 Emerson Electric Co.

- 8.1.5 Rockwell Automation Inc.

- 8.1.6 OMRON Corporation

- 8.1.7 Yokogawa Electric Corporation

- 8.1.8 Koyo Electronic Industries Co. Ltd

- 8.1.9 Daifuku Co. Ltd

- 8.1.10 Honeywell International Inc.