|

市场调查报告书

商品编码

1644882

新加坡的网路安全:市场占有率分析、行业趋势和成长预测(2025-2030 年)Singapore Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

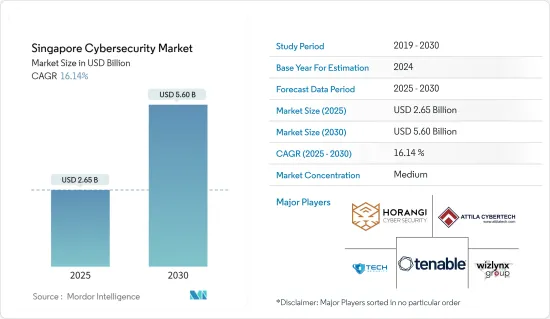

新加坡网路安全市场规模预计在 2025 年为 26.5 亿美元,预计到 2030 年将达到 56 亿美元,预测期内(2025-2030 年)的复合年增长率为 16.14%。

主要亮点

- 随着人们对安全和隐私的担忧日益加深,随着新威胁的出现,网路安全市场预计将继续扩大和多样化。此外,还需要更多整合的解决方案来满足全国各地日益增长的需求。

- 网路威胁是利用网路透过间谍软体、恶意软体和网路钓鱼造成破坏、破坏资讯系统或窃取敏感资讯的威胁。为了保护资料的机密性,网路安全解决方案可协助企业监控、侦测、报告和应对网路威胁。随着网路在开发中国家的普及率不断提高,网路安全解决方案的采用率可能会增加。

- 连网设备的增加预计将增加新威胁和攻击的出现,推动对易受网路攻击的家用电器提高安全性的需求,并进一步暴露物联网设备作为端点的脆弱性。

- 大型企业正在为安全和销售部署更多资料驱动的人工智慧解决方案。网路安全专家正在利用地理空间资料来加强他们的防线。透过将地理空间资料纳入现有的安全系统,公司可以增强紧急管理、国家情报、基础设施保护和国防平台。

- 各领域缺乏经过训练的网路安全人员是网路攻击增加的主要原因之一。特别是在亚太地区,对经验丰富的网路安全专业人员的需求,并不像对应对金融机构、政府和工业公司网路威胁所需的安全人员的需求那么大。

- COVID-19 疫情和在家工作的兴起是造成这种成长的主要原因,因为在家工作的人没有像在职场环境中那样同等程度的保护/威慑措施。网路攻击者将疫情视为利用在家工作者弱点的机会,利用公众对冠状病毒新闻的强烈兴趣来活性化他们的犯罪活动。

新加坡的网路安全市场趋势

云端部署推动市场成长

- 在新加坡,随着越来越多的企业意识到需要透过将资料迁移到云端而不是建置和维护新的资讯储存来节省成本和资源,对云端解决方案的需求日益增加,按需安全服务的采用也日益增多。

- 由于这些优势,云端基础的解决方案在全国范围内越来越多地被采用,从大型企业到中小型企业。未来几年,云端平台和生态系统有望成为数位创新速度和规模爆炸性成长的跳板。

- 网路频宽需求波动的企业需要能够在短时间内增加或减少容量。云端技术允许网路容量扩大或缩小以满足业务需求。这种方法可以帮助公司削减成本并在竞争中占据优势。作为国内中小企业的基地,保全服务云端部署近年来呈现兴起趋势。

- 云端技术使公司可以根据业务需求自由选择如何以及何时扩大或缩小网路容量。它降低了商业成本并使您比竞争对手更具优势。

- 此外,新加坡和澳洲还签署了一份谅解备忘录,以打击诈骗和垃圾通讯。随着政府注重加强网路安全以及企业加大对云端运算的采用,这一领域预计将推动市场成长。

BFSI 占最高市场占有率

- BFSI 是一个关键基础设施行业,由于其庞大的基本客群和持有的财务信息,面临多次资料外洩和网路攻击。它是该国重要的金融服务和保险业之一。

- 网路犯罪分子利用其极其有利可图的营运模式来提供惊人的回报以及相对较低的风险和可检测性,从而优化一系列邪恶的网路攻击,以破坏金融部门。这些攻击威胁包括木马、恶意软体、ATM 恶意软体、勒索软体、行动银行恶意软体、资料外洩、组织入侵、资料窃取、财务外洩等。

- 网路犯罪分子正在优化各种恶意的网路攻击,以锁定金融领域,这是一个利润丰厚的经营模式,可以带来惊人的回报以及相对低风险和低检测的好处。

- 随着各机构越来越多地采用云端运算、人工智慧 (AI) 和物联网 (IoT) 等技术,新加坡政府已承诺到 2023 年将在网路安全和资料安全系统上投资 10 亿新加坡元(7.4 亿美元)。

新加坡网路安全产业概况

新加坡的网路安全市场处于半固体。 Horangi Cyber Security、Wizlynx Pte Ltd、Attila Cybertech Pte Ltd、Tech Security 和 Tenable Singapore 等市场参与者正在透过併购、合作和新产品推出等策略性倡议来应对企业对行动安全日益增强的认识。

- 2024 年 3 月,风险管理公司 Tenable 宣布对 Tenable One 风险管理平台内的生成式 AI 功能和服务 Exposure AI 进行创新增强。新功能使客户能够快速摘要相关的攻击媒介,向AI助理提出问题,并获得具体的缓解指导,以根据情报采取行动降低风险。

- 2023年8月,Bitdefender宣布收购Horangi Cyber Security。这将使我们能够扩展我们的网路安全解决方案和服务组合,并为我们的客户提供更好的服务、创新和价值,以满足他们不断变化的需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 产业指引及政策

- COVID-19 产业影响评估

第五章 市场动态

- 市场驱动因素

- 网路安全事件和报告法规迅速增加

- 日益增加的 M2M/IoT 连线要求企业加强网路安全措施

- 市场挑战

- 网路安全专家短缺

- 高度依赖传统身分验证方法且缺乏准备

第六章 市场细分

- 依产品类型

- 解决方案

- 应用程式安全

- 云端安全

- 消费者安全软体

- 资料安全

- 身分和存取管理

- 基础设施保护

- 综合风险管理

- 网路安全设备

- 其他解决方案

- 按服务

- 解决方案

- 按部署

- 在云端

- 本地

- 按最终用户产业

- 航太和国防

- 银行、金融服务和保险

- 卫生保健

- 製造业

- 零售

- 资讯科技/通讯

- 其他最终用户产业

第七章 竞争格局

- 公司简介

- Horangi Cyber Security

- wizlynx Pte Ltd

- Attila Cybertech Pte Ltd

- Tech Security

- Tenable Singapore

- InsiderSecurity

- Ensign InfoSecurity(Singapore)Pte Ltd

- iCyberwise

- A Very Normal Company

- GROUP8

- Blackpanda

- MK Cybersecurity

- WebOrion

- i-Sprint Innovations

第八章投资分析

第九章 市场机会与未来趋势

The Singapore Cybersecurity Market size is estimated at USD 2.65 billion in 2025, and is expected to reach USD 5.60 billion by 2030, at a CAGR of 16.14% during the forecast period (2025-2030).

Key Highlights

- With increasing security and privacy concerns, the market for cyber safety is expected to keep expanding and diversifying with new threats coming upstream. More integrated solutions will also be required in order to respond to rising demand from all parts of the country.

- Cyber threats are those that exploit the Internet for damage, disrupt information systems, or steal vital information through spyware, malware, and phishing. For the protection of data confidentiality, cybersecurity solutions assist enterprises in monitoring, detecting, reporting, and dealing with cyber threats. With the increasing penetration of the Internet in developing and developed countries, there is a chance that the adoption of cybersecurity solutions will increase.

- The increasing number of connected devices is expected to increase the occurrence and emergence of new threats and attacks, thereby creating an increased demand for improved security on consumer electronics that are highly vulnerable to cyber attacks, which further reveals the vulnerabilities of IoT devices as endpoints.

- Large businesses are implementing more data-based AI solutions for security and sales. Cybersecurity experts have turned to geospatial data to shore up the lines of defense. By implementing geospatial data into pre-existing security systems, companies can strengthen emergency management, national intelligence, infrastructure protection, and national defense platforms.

- The lack of trained cybersecurity staff in all sectors is one of the major causes of increased cyber attacks. The demand for experienced cybersecurity professionals, particularly in Asia-Pacific, is not as great as that of security staff who are needed to tackle cyber threats related to finance institutions and governments or industrial enterprises.

- The COVID-19 pandemic and the increase in work-from-home were the primary causes of this increase, as individuals working at home do not have the same level of protection/deterrent measures from a working environment. Cyber-attackers saw the pandemic as an opportunity to exploit the employees working from home's vulnerability and exploit the public's strong interest in coronavirus news so they would step up their criminal activities.

Singapore Cyber Security Market Trends

Cloud Deployment Drives Market Growth

- The demand for cloud solutions is high, and the adoption of on-demand security services is growing as more and more companies in Singapore recognize the need to save money and resources by moving data into a cloud rather than creating or maintaining new information storage.

- Due to these advantages, large and small domestic companies are increasingly adopting cloud-based solutions. Over the next couple of years, cloud platforms and ecosystems are expected to serve as starting points for an explosive increase in the pace and scale of digital innovation.

- Within a short timeframe, enterprises that experience fluctuations in demand for network bandwidth must be able to increase or decrease their capacity. In order to cope with business needs, cloud technologies enable enterprises to increase or decrease network capacity. This approach can help businesses to stand out from the competition in terms of cost savings. In view of the country's small and medium-sized enterprises being based here, cloud deployment of cybersecurity services has tended to increase in recent years.

- With cloud technology, companies are free to choose how and when they want to boost or reduce their network capacity according to business needs. It can reduce the cost of doing business and give businesses an advantage over their competitors.

- Moreover, an MoU was signed between Singapore and Australia to battle scam and spam communications. With the government's focus on building cybersecurity strength and the companies implementing cloud deployments, the segment is forecasted to drive market growth.

BFSI Holds the Highest Market Share

- BFSI is a critical infrastructure segment that faces multiple data breaches and cyber attacks, owing to its huge customer base and the financial information that it holds. It is one of the country's significant financial services and insurance sectors.

- Being a highly lucrative operation model with phenomenal returns and the added upside of relatively low risk and detectability, cybercriminals are optimizing a plethora of diabolical cyberattacks to immobilize the financial sector. These attacks' threat landscape includes trojans, malware, ATM malware, ransomware, mobile banking malware, data breaches, institutional invasion, data thefts, and fiscal breaches.

- In order to immobilize the financial sector as a highly lucrative business model with phenomenal returns and an added advantage of relatively low risk and detection, cybercriminals optimize various diabolical cyberattacks.

- The Singaporean government stated that it would invest SGD 1 billion (0.74 USD billion) until 2023 in its cyber and data security systems, as various agencies are increasingly adopting technologies such as cloud, artificial intelligence (AI), and Internet of Things (IoT).

Singapore Cyber Security Industry Overview

The Singaporean cybersecurity market is semi-consolidated. Players in the market such as Horangi Cyber Security, Wizlynx Pte Ltd, Attila Cybertech Pte Ltd, Tech Security, and Tenable Singapore adopt cater to strategic initiatives such as mergers and acquisitions, partnerships, and new product offerings due to increasing awareness regarding mobility security among enterprises.

- March 2024: Tenable, an exposure management company, announced innovative enhancements in exposure AI, the generative AI capabilities and services within its Tenable One Exposure Management platform. The new features enable customers to quickly summarize relevant attack paths, ask questions of an AI assistant, and receive specific mitigation guidance to act on intelligence and reduce risk.

- August 2023: Bitdefender announced the acquisition of Horangi Cyber Security, enabling it to offer customers an expanded portfolio of cybersecurity solutions and services and provide an even greater level of service, innovation, and value to meet evolving needs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Guidelines and Policies

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapidly Increasing Cybersecurity Incidents and Regulations Requiring Their Reporting

- 5.1.2 Growing M2M/IoT Connections Demanding Strengthened Cybersecurity in Enterprises

- 5.2 Market Challenges

- 5.2.1 Lack of Cybersecurity Professionals

- 5.2.2 High Reliance on Traditional Authentication Methods and Low Preparedness

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Solutions

- 6.1.1.1 Application Security

- 6.1.1.2 Cloud Security

- 6.1.1.3 Consumer Security Software

- 6.1.1.4 Data Security

- 6.1.1.5 Identity Access Management

- 6.1.1.6 Infrastructure Protection

- 6.1.1.7 Integrated Risk Management

- 6.1.1.8 Network Security Equipment

- 6.1.1.9 Other Solution Types

- 6.1.2 Services

- 6.1.1 Solutions

- 6.2 By Deployment

- 6.2.1 On-Cloud

- 6.2.2 On-Premise

- 6.3 By End-user Industry

- 6.3.1 Aerospace and Defense

- 6.3.2 Banking, Financial Services, and Insurance

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 IT and Telecommunication

- 6.3.7 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Horangi Cyber Security

- 7.1.2 wizlynx Pte Ltd

- 7.1.3 Attila Cybertech Pte Ltd

- 7.1.4 Tech Security

- 7.1.5 Tenable Singapore

- 7.1.6 InsiderSecurity

- 7.1.7 Ensign InfoSecurity (Singapore) Pte Ltd

- 7.1.8 iCyberwise

- 7.1.9 A Very Normal Company

- 7.1.10 GROUP8

- 7.1.11 Blackpanda

- 7.1.12 MK Cybersecurity

- 7.1.13 WebOrion

- 7.1.14 i-Sprint Innovations

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDs

数据二极体市场 - 全球产业规模、份额、趋势、机会和预测,按外形尺寸、类型、应用、地区和竞争细分,2020-2030 年

数据二极体市场 - 全球产业规模、份额、趋势、机会和预测,按外形尺寸、类型、应用、地区和竞争细分,2020-2030 年 全球数位免疫系统市场

全球数位免疫系统市场 2032 年网路安全市场 AI威胁侦测系统预测:按组件、部署类型、组织规模、技术、最终用户和地区进行的全球分析2032 年网路安全市场区块链预测:按组件、安全类型、平台、组织规模、部署类型、应用、最终用户和地区进行全球分析人工智慧 - 2032 年网路安全市场威胁情报预测:按组件、安全类型、部署模式、技术、应用、最终用户和地区进行的全球分析

2032 年网路安全市场 AI威胁侦测系统预测:按组件、部署类型、组织规模、技术、最终用户和地区进行的全球分析2032 年网路安全市场区块链预测:按组件、安全类型、平台、组织规模、部署类型、应用、最终用户和地区进行全球分析人工智慧 - 2032 年网路安全市场威胁情报预测:按组件、安全类型、部署模式、技术、应用、最终用户和地区进行的全球分析 全球网路安全市场,按产品、解决方案类型、安全类型、部署模式、组织规模、垂直行业和地区划分 - 预测至 2030 年

全球网路安全市场,按产品、解决方案类型、安全类型、部署模式、组织规模、垂直行业和地区划分 - 预测至 2030 年 2025年建设产业数位双胞胎全球市场报告

2025年建设产业数位双胞胎全球市场报告 网路安全中的人工智慧 (AI) 市场规模、份额、成长分析(按类型、产品、技术、产业垂直、应用、地区和预测)到 2025 年至 2032 年全球IT与通讯业网路安全市场全球加密解密解决方案市场

网路安全中的人工智慧 (AI) 市场规模、份额、成长分析(按类型、产品、技术、产业垂直、应用、地区和预测)到 2025 年至 2032 年全球IT与通讯业网路安全市场全球加密解密解决方案市场