|

市场调查报告书

商品编码

1644901

德国最后一哩配送:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Germany Last Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

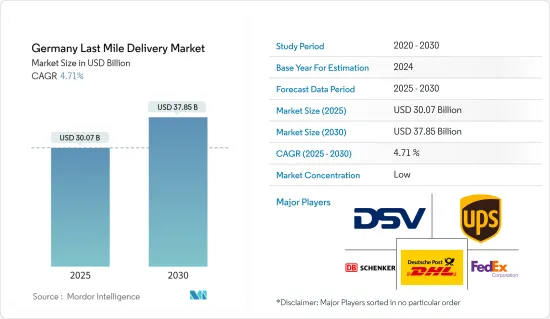

2025 年德国最后一哩配送市场规模预估为 300.7 亿美元,预计到 2030 年将达到 378.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.71%。

里程市场受到多种因素的推动,包括电子商务和全球化的活性化、贸易活动的增加、运输车辆的技术进步以及快速包裹运送的需求。

然而,基础设施差、物流成本高、製造商和零售商的物流服务管理不善以及邮政地址系统不准确等因素阻碍了市场的成长。自从德国限制社会和非必要商业活动的指令生效以来,铁路和公路货运量下降了约20%。

大多数线上零售商也受到了新冠肺炎的影响。据德国邮政称,正常情况下,平均每天递送520万件小包裹。据德国邮政称,封锁期间每天运输超过800万件小包裹和快件。冠状病毒危机导致全国对储存空间的需求增加,这并不令人意外。

在德国,与世界上几乎所有国家一样,电子商务正在经历前所未有的成长。随着电子商务的发展,小包裹储物柜和小包裹仓库等全国性宅配选择越来越受欢迎。例如,德国邮政目前营运约 8,500 台自动包裹机,并计划在 2023 年将其增加到 12,500 台。

例如,2023年6月,提供当日送达服务的DODO扩展到德国市场,增强了当日最后一哩送达的长期可行性。多年来,DODO已经开发出全面的软体和交付生态系统,为各行各业的参与者提供支援。该生态系统得到了该公司白牌解决方案的进一步支持,这些解决方案可以直接整合到公司的 IT 结构中。 DODO目前拥有超过2500名宅配业者和超过1000辆车辆。

德国最后一哩配送市场的趋势

电子商务成长推动市场

德国电子商务平台市场主要受该地区高互联网普及率和智慧设备日益增长的使用所推动。随着都市化进程的加快,许多传统企业开始转向电子商务平台来扩大客户群和市场占有率、降低管理成本并增加产品销售。

在德国,大多数网路商店接受PayPal或信用卡作为付款方式。许多网站也接受银行转帐。大多数网站还允许开立发票/先买后付,并允许线上客户在 14 天内以任何理由或无理由取消订单并退回商品或服务。由于电子商务公司提供如此多的好处,该地区的电子商务行业将在未来几年继续扩大。

德国电子商务销售最大的类别是时尚(24.1%),其次是食品和个人护理(22.2%)、家具和电器(20.2%)、电子和媒体(17.4%)和玩具、爱好和 DIY(16.0%)。

政府对交通基础设施的投资将支持最后一哩的配送

透过投资基础设施来改善交通网络、减少交通拥堵和提高物流效率,可以改善最后一哩路的交付。更好的道路、桥樑和港口使得货物运输更快、更有高效,从而缩短了交货时间。智慧交通管理系统 (TMS) 和专用送货通道可以帮助减少交通拥堵并确保及时送货。支援即时监控、优化路线并改善配送团队和客户之间沟通的数位基础设施。

德国联邦政府计划在2022年比2021年多拨出数百万欧元用于交通基础设施支出。交通基础设施支出的最大增幅将出现在2021年,届时联邦铁路将获得110亿欧元(120.1亿美元)的拨款,是2016年拨款金额的两倍多。 2022年,联邦公路的资金将超过120亿欧元,水道的资金将达到170亿欧元(180.1亿美元)。

B247扩建工程已成为图林根北部最大的基础建设计划。该计划涉及在 22.2 公里长的路段上建造两至四车道,包括两条新的绕行道路、31 座建筑(包括两座桥樑和五座铁路桥)、八个交叉口以及新增约 6 公里的州和联邦公路。该建筑将于 2025 年中期由德国 VINCI 集团(Eurovia、VINCI Construction Terrassement 和 Via Structure)的子公司与图林根州的当地公司合作完成。

德国最后一哩配送产业概况

德国最后一哩配送市场竞争激烈,既有国际参与者,也有国内参与者。德国最后一哩配送市场的领导者包括DSV(Direktor von Schwerin)、UPS(联合包裹服务公司)(UPS)、DB Schwerin(德国邮政DHL)和联邦快递。该领域的公司正专注于透过整合无人机、电子车辆、运输管理系统 (TMS) 和人工智慧 (AI) 等新技术来实现成长。由于人事费用上升以及劳动力越来越难找,德国物流公司陷入困境。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 当前市场状况

- 科技趋势

- 电子商务产业洞察

- 卡车运输业洞察

- 仓库和配送中心洞察

- 了解最后一英里冷藏配送

- 洞察退货流

- COVID-19 市场影响

第五章 市场动态

- 市场驱动因素

- 电子商务成长

- 都市化进程加速

- 市场限制/挑战

- 行李被窃或损坏的风险

- 经济高效

- 市场机会

- 电子商务整合

- 产业吸引力-波特五力分析

- 购买者/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第六章 市场细分

- 按服务

- B2B(Business-to-Business)

- B2C(Business-to-Consumer)

- C2C(Customer-to-Customer)

第七章 竞争格局

- 市场集中度概览

- 公司简介

- DSV

- UPS

- DB Schenker

- Deutsche Post DHL

- FedEx

- DPD Group

- General Logistics Systems

- Rhenes Logistics

- JJX Logistics

- CEVA Logistics

- SpeedLink Transport*

第八章 市场机会与未来趋势

第 9 章 附录

The Germany Last Mile Delivery Market size is estimated at USD 30.07 billion in 2025, and is expected to reach USD 37.85 billion by 2030, at a CAGR of 4.71% during the forecast period (2025-2030).

The mile delivery market is driven by several factors, including the development of the e-commerce sector and the rise in trading activities due to globalization, technological innovations in delivery vehicles, and the need for fast package delivery.

However, poor infrastructure, high logistics costs, a lack of control over logistics services by manufacturers and retailers, and an inaccurate postal address system will impede the market growth. Since the implementation of the directive to restrict social activities and non-essential commercial activities in Germany, freight transport by rail and road has decreased by approximately 20%.

The majority of online retailers were also affected by COVID-19. According to Deutsche Post, a daily average of 5.2 million parcels are usually delivered. Deutsche Post reported that during the lockdowns, more than 8 million packages and deliveries were transported daily. The coronavirus crisis has led to an increase in the demand for storage space in the country, which is not unexpected.

Germany has seen unprecedented growth in e-commerce, as has almost every country in the world. In parallel with the growth of e-commerce, nationwide out-of-the-home delivery options such as parcel lockers and parcel collection stations have become increasingly popular. Deutsche Post, for example, currently operates about 8500 automated parcel machines, with plans to increase that to 12,500 machines by 2023.

For instance, in June 2023, DODO, the same-day delivery service provider, expanded its operations into the German market, reinforcing the long-term viability of same-day, last-mile delivery. DODO has developed a comprehensive software and delivery ecosystem over the years to support players across a variety of industries. This ecosystem is further supported by the company's white-label solution, which allows direct integration into the company's IT structure. DODO currently employs more than 2500 couriers and 1,000 vehicles.

Germany Last Mile Delivery Market Trends

Growth in E-commerce is Driving the Market

The e-commerce platform market in Germany is mainly driven by the high internet penetration in the region and the growing use of smart devices. With increasing urbanization, many traditional businesses are turning to e-commerce platforms to increase the number of customers and market share, reduce overhead expenses, and increase the sales of their products.

In Germany, the majority of online stores accept PayPal or credit cards as the payment method. Many websites also accept bank transfers. Most websites accept invoices/buy now and pay later, and online customers can cancel their orders within 14 days and return their goods or services for any reason or no reason at all. There are so many benefits offered by e-commerce companies that the e-commerce industry in the region will continue to expand over the next few years.

Fashion makes up the biggest chunk of German e-commerce revenue (24.1%), followed by food and personal care (22.2%), furniture and appliances (20.2%), electronics and media (17.4%), and toys, and hobby and DIY (16.0%).

Government Investment in Transport Infrastructure Supports Last Mile Delivery

Last-mile delivery can be improved by investing in infrastructure that improves transportation networks, reduces congestion, and improves logistical efficiency. Roads, bridges, and ports that are upgraded will allow goods to be transported more quickly and efficiently, resulting in shorter delivery times. Smart traffic management systems (TMS) and dedicated delivery lanes can help reduce congestion and ensure timely deliveries. The digital infrastructure that supports real-time monitoring optimizes routes and improves communication between the delivery team and customers, which can also improve last-mile delivery.

Germany's federal government plans to allocate several million euros more in transport infrastructure spending in 2022 compared to 2021. The largest increase in transport infrastructure spending occurred in 2021 when EUR 11 billion (USD 12.01 billion) was allocated to federal railways, which was more than double the amount allocated in 2016. Over EUR 12 billion will be allocated to federal highways in 2022, and EUR 17 billion (USD 18.01 billion) will be allocated to waterways.

The expansion of the B247 became the largest infrastructure project in Northern Thuringia. The project consists of building two to four new lanes on a 22.2 km road section, including two new bypasses, 31 structures, including two bridges and five railway bridges, eight junctions, and around 6 km of additional state and federal roads. The works will be completed by mid-2025 by subsidiaries of the VINCI Group in Germany (Eurovia, VINCI Construction Terrassement, and Via Structure) in local partnership with Thuringian companies.

Germany Last Mile Delivery Industry Overview

Germany's Last Mile Delivery market is highly competitive as it is made up of a mix of international and domestic players. Some of Germany's leading players in the last-mile delivery market are DSV (Direktor von Schwerin), UPS (United Parcel Service) (UPS), DB Schwerin (Deutsche Post DHL), and FedEx (FedEx). Companies in the sector are focusing on growth through the integration of new technologies such as drones, e-vehicles, transport management systems (TMS), and artificial intelligence (AI). Germany's logistics players are struggling as labor costs are on the rise and labor availability is decreasing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights into E-Commerce Industry

- 4.4 Insights into Trucking Industry

- 4.5 Insights into Warehousing and Distribution Centers

- 4.6 Insights into Refrigerated Last Mile Delivery

- 4.7 Insights into Return Logistics

- 4.8 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise In eCommerce

- 5.1.2 Rise In Urbanization

- 5.2 Market Restraints/Challenges

- 5.2.1 The Risk of Package Theft or Damage

- 5.2.2 Cost Efficiency

- 5.3 Market Opportunities

- 5.3.1 E- commerce Integration

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Buyers/Consumers

- 5.4.2 Bargaining Power of Suppliers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 B2B (Business-to-Business)

- 6.1.2 B2C (Business-to-Consumer)

- 6.1.3 C2C (Customer-to-Customer)

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 DSV

- 7.2.2 UPS

- 7.2.3 DB Schenker

- 7.2.4 Deutsche Post DHL

- 7.2.5 FedEx

- 7.2.6 DPD Group

- 7.2.7 General Logistics Systems

- 7.2.8 Rhenes Logistics

- 7.2.9 JJX Logistics

- 7.2.10 CEVA Logistics

- 7.2.11 SpeedLink Transport*

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

2026-2030年全球最后一公里配送市场

2026-2030年全球最后一公里配送市场 法国最后一公里配送:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

法国最后一公里配送:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本最后一公里配送市场规模、份额、趋势及预测(按服务类型、技术、应用和地区划分,2026-2034年)

日本最后一公里配送市场规模、份额、趋势及预测(按服务类型、技术、应用和地区划分,2026-2034年) 2032年全球自动驾驶城市最后一公里配送市场预测:按车辆类型、经营模式、企业规模、技术、最终用户和地区分類的分析全球都市区最后100公尺配送市场:未来预测(至2032年)-依车辆类型、配送范围、配送方式、企业规模、技术、最终用户及地区进行分析

2032年全球自动驾驶城市最后一公里配送市场预测:按车辆类型、经营模式、企业规模、技术、最终用户和地区分類的分析全球都市区最后100公尺配送市场:未来预测(至2032年)-依车辆类型、配送范围、配送方式、企业规模、技术、最终用户及地区进行分析 末端配送市场:依服务类型、车辆类型、配送方式及应用程式划分-全球预测至2035年

末端配送市场:依服务类型、车辆类型、配送方式及应用程式划分-全球预测至2035年 最后一公里配送市场规模、份额和成长分析(按配送方式、目的地、服务类型、车辆类型、营运类型、应用和地区划分)-2026-2033年产业预测2032年末端物流市场预测:按配送类型、车辆类型、履约模式、技术、最终用户和地区分類的全球分析2032年末端配送机器人市场预测:全球分析(按产品、车辆类型、续航里程、负载容量、自主程度、应用、最终用户和地区划分)

最后一公里配送市场规模、份额和成长分析(按配送方式、目的地、服务类型、车辆类型、营运类型、应用和地区划分)-2026-2033年产业预测2032年末端物流市场预测:按配送类型、车辆类型、履约模式、技术、最终用户和地区分類的全球分析2032年末端配送机器人市场预测:全球分析(按产品、车辆类型、续航里程、负载容量、自主程度、应用、最终用户和地区划分) 最后一公里配送车辆市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

最后一公里配送车辆市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)