|

市场调查报告书

商品编码

1645043

轻质建筑材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Lightweight Construction Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

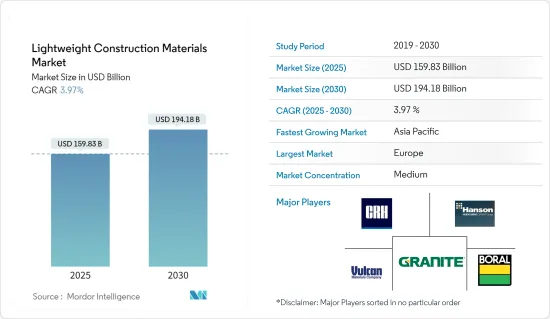

轻质建筑材料市场规模预计在 2025 年为 1,598.3 亿美元,预计到 2030 年将达到 1,941.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.97%。

关键亮点

- 随着世界人口日益都市化,高层建筑的需求日益增长。使用轻质建筑材料可以减轻这些建筑物的重量,节省地基成本并降低地震风险。例如,2022年北美城市人口为308,798,139,比2021年增加0.77%。

- 2021 年该北美城市的人口为 306,441,356,比 2020 年增加 0.44%。 2020年北美城镇人口为305,103,974人,较2019年成长1.22%。此外,到2022年,全球都市化程度将达到57%。北美洲是都市化最高的地区,超过五分之四的人口居住在都市区。

- 轻质建筑材料可以减少墙壁和屋顶散失的热量,从而提高建筑物的能源效率。例如,2023 年上半年欧洲对节能建筑的投资高于其他任何地区。中国对该市场的投资为220亿美元,略低于美国(280亿美元)。这些投资对于减少建筑物对环境的影响是必要的,建筑物占全球温室气体排放的很大一部分。这些材料使用更少的原材料并产生更少的废弃物,有助于减少建筑对环境的影响。

- 轻质建筑材料在航太和国防领域发挥关键作用,有助于开发飞机、太空船和国防车辆的高效、耐用的结构。这些材料有助于显着减轻重量、提高燃油效率、增加负载容量并提高整体性能。自2013年以来,全球对航太相关企业的股权投资总计约2,720亿美元。美国航太公司约占总投资的47%,其次是中国,占29%。

轻质建筑材料市场趋势

建筑和施工领域占全球市场的很大份额

- 建筑业是轻质建筑材料市场的主要驱动力,占全球需求的大部分。轻量材料具有多种优点,特别适合建筑应用,因此在该领域广受欢迎。

- 轻质建筑材料具有多种优势,因为它们可以显着减轻建筑物的整体重量。这最大限度地减少了地基的负荷,从而降低了地基成本并提高了抗震能力。此外,它还降低了运输建材的成本,并允许建造更高、更细长的结构。

- 据业内人士透露,未来几年全球建筑业收益预计将稳定成长。到 2030 年,预计这一数字将比 2020 年增加一倍以上。 2020年建筑市场规模为6.4兆美元,预计2030年将达到14.4兆美元。

- 轻量材料可以实现更大的设计灵活性并创造出独特的建筑特色。它的多功能性使建筑师和设计师可以尝试不同的形式、形状和饰面,从而增强建筑的美感。许多轻质建筑材料都是预製的,可以在现场快速组装,从而减少了施工时间和人事费用。这对于较大的计划或技术纯熟劳工有限的地区尤其有利。

- 轻量材料通常具有更好的绝缘性能,有助于调节室内温度并降低能源消耗。对于旨在获得能源效率认证或满足环境永续性目标的建筑来说,这一点尤其重要。

欧洲可望主导全球轻质建筑材料市场

- 预计欧洲将在全球轻质建筑材料市场占据主要市场占有率。欧洲国家正在实施严格的建筑能源效率法规,推动对具有更好隔热性能和降低能耗的轻质建筑材料的需求。交叉层压木材(CLT)、自加气混凝土(AAC)和发泡聚苯乙烯(EPS)等轻量材料具有出色的隔热性能,可减少能源消耗并降低碳排放。

- 此外,欧洲是一个高度都市化的地区,人口不断增长,对新建筑和基础设施的需求不断增加。轻量材料在优化建筑设计、缩短施工时间和减少环境影响方面发挥关键作用。欧洲拥有成熟的轻质建筑材料製造地,主要生产商在德国、义大利等国家。强大的供应链使我们能够以有竞争力的价格采购高品质的材料。

- 推动成长的因素有很多,包括对节能建筑的需求不断增长、对更轻的建筑材料以便于运输的需求、以及异地施工方法的日益普及。例如,伦敦的新办公大楼建设中正在使用 CLT。 CLT 是一种由多层木材黏合在一起製成的工程木材。它是一种防火、耐用且轻质的材料。

- 此外,AAC在德国也用于学校建设。 AAC 是一种由水泥、沙子、石灰、水和空气製成的轻质混凝土。 AAC 是一种由水泥、沙子、石灰、水和空气製成的轻质混凝土,是一种坚固、耐火的隔热材料。

轻质建筑材料产业概况

轻质建筑材料市场是一个分散的市场,由参与企业。由于都市化、永续性投资和经济成长等多种因素,预计该市场在预测期内将会成长。该市场的主要企业有:海德堡水泥、花岗岩、三一、詹姆斯哈迪和汉森。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 当前市场状况

- 市场技术趋势

- 政府的市场法规和倡议

- 洞察供应链/价值链分析

- COVID-19 市场影响

第五章 市场动态

- 市场驱动因素

- 新兴国家采用轻量材料和增加飞机产量

- 各国航太和国防领域的成长情况

- 加大应用程式研发投入

- 市场限制

- 发展中地区汽车产业放缓与萎缩

- 建筑材料高成本

- 机会

- 绿建筑倡议

- 基础设施开发

- 波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第六章 市场细分

- 依产品类型

- 木头

- 白利糖度

- 混凝土的

- 其他的

- 依结构类型

- 住宅

- 商务用

- 工业的

- 基础设施

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 东南亚国协

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 中东和非洲

- 海湾合作委员会国家

- 南非

- 其他中东和非洲地区

- 北美洲

第七章 竞争格局

- 公司简介

- Granite

- HeidelbergCement

- Hanson

- LafargeHolcim

- Trinity

- Vulcan Materials

- Dyckerhoff

- Italcementi

- Taiheiyo Cement

- CRH

- James Hardie

- Boral

第八章:未来市场展望

第 9 章 附录

- 各活动国内生产毛额分布

- 洞察资本流动

- 对外贸易统计 - 进出口(依产品)

- 了解主要出口目的地

- 了解主要进口来源地

The Lightweight Construction Materials Market size is estimated at USD 159.83 billion in 2025, and is expected to reach USD 194.18 billion by 2030, at a CAGR of 3.97% during the forecast period (2025-2030).

Key Highlights

- As the world's population becomes increasingly urbanized, there is a growing demand for high-rise buildings. Lightweight construction materials can be used to reduce the weight of these buildings, which can save on foundation costs and reduce the risk of earthquakes. For example, the North American urban population for 2022 was 308,798,139, a 0.77% increase from 2021.

- The North American urban population for 2021 was 306,441,356, a 0.44% increase from 2020. The North American urban population for 2020 was 305,103,974, a 1.22% increase from 2019. Furthermore, in 2022, the degree of urbanization worldwide was at 57 percent. North America was the region with the highest level of urbanization, with over four-fifths of the population residing in urban areas.

- Lightweight construction materials can help to improve the energy efficiency of buildings by reducing the amount of heat that is lost through the walls and roof. For instance, the value of investments in energy-efficient buildings in H1 2023 was higher in Europe than in any other region. Investments for that market in China amounted to USD 22 billion, which was somewhat lower than in the United States (USD 28 billion). These investments are necessary to reduce the environmental impact of buildings, as they were responsible for a significant share of global greenhouse gas emissions. These materials can help to reduce the environmental impact of construction by using fewer raw materials and producing less waste.

- Lightweight construction materials play a crucial role in the aerospace and defense sectors, enabling the development of highly efficient and durable structures for aircraft, spacecraft, and defense vehicles. These materials contribute to significant weight reduction, enhancing fuel efficiency, increasing payload capacity, and improving overall performance. Since 2013, a total of approximately USD 272 billion of equity investments have been made in space companies worldwide. United States space companies have accounted for almost 47 percent of the total investment, followed by China with 29 percent.

Lightweight Construction Materials Market Trends

Building & Construction segment Holds the prominent share of Global Market

- The buildings and construction segment is a major driver of the lightweight construction materials market, accounting for a significant portion of global demand. Lightweight materials offer several advantages that make them particularly well-suited for construction applications, leading to their widespread adoption in this sector.

- Lightweight construction materials significantly reduce the overall weight of a building, which has several benefits. It minimizes the load on foundations, leading to lower foundation costs and improved seismic resistance. Additionally, it reduces transportation expenses for building materials and enables the construction of taller and more slender structures.

- According to industry sources, the revenue of the global construction industry is expected to grow steadily over the next years. In 2030, it is projected to be more than twice as big as it was in 2020. The size of the construction market amounted to USD 6.4 trillion in 2020, and it is expected to reach USD 14.4 trillion in 2030.

- Lightweight materials offer greater design flexibility and enable the creation of unique architectural features. Their versatility allows architects and designers to experiment with different shapes, forms, and finishes, enhancing the aesthetic appeal of buildings. The prefabricated nature of many lightweight construction materials allows for faster assembly on-site, reducing construction time and labor costs. This is particularly beneficial for large-scale projects and in areas with limited skilled labor availability.

- Lightweight materials often possess superior thermal insulation properties, helping to regulate indoor temperatures and reduce energy consumption. This is particularly important in buildings seeking to achieve energy efficiency certifications and meet environmental sustainability goals.

Europe to Constitute Major Share of Global Lightweight Construction Materials Market

- Europe is expected to hold a significant market share in the global lightweight construction materials market. European countries have implemented stringent energy efficiency regulations for buildings, driving the demand for lightweight construction materials that offer better thermal insulation and reduce energy consumption. Lightweight materials like cross-laminated timber (CLT), autoclaved aerated concrete (AAC), and expanded polystyrene (EPS) offer superior thermal insulation properties, reducing energy consumption and lowering carbon emissions.

- Furthermore, Europe is a highly urbanized region with a growing population and increasing demand for new buildings and infrastructure. Lightweight materials play a crucial role in optimizing building designs, reducing construction time, and minimizing environmental impact. Europe has a well-established manufacturing base for lightweight construction materials, with leading producers like Germany, Austria, and Italy. This strong supply chain ensures the availability of high-quality materials at competitive prices.

- The growth is being driven by several factors, including the increasing demand for energy-efficient buildings, the need to reduce the weight of construction materials to improve transportation efficiency, and the growing popularity of off-site construction methods. For example, CLT is being used to construct a new office building in London. CLT is a type of engineered wood that is made up of layers of timber that are glued together. It is a strong and lightweight material with fire-resistant properties.

- Furthermore, AAC is used to construct schools in Germany. AAC is a type of lightweight concrete that is made by mixing cement, sand, lime, and water with air. It is a strong and insulating material with fire-resistant properties.

Lightweight Construction Materials Industry Overview

The lightweight construction materials market is fragmented in nature, with a mix of global and regional players. The market is expected to grow during the forecast period due to several factors, such as urbanization, sustainability investments, and growing economies. The major players in this market are HeidelbergCement, Granite, Trinity, James Hardie, and Hanson.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends in the Market

- 4.3 Governemnt Regulations and Initiatives in the Market

- 4.4 Insights into Supply Chain/Value Chain Analysis

- 4.5 Impact of Covid-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Adoption of Lightweight Materials and Increase in the production of aircraft in developing countries

- 5.1.2 Growth of the Aerospace and Defence Sector in countries

- 5.1.3 Rise in investments in application-oriented research and development

- 5.2 Market Restraints

- 5.2.1 Economic slowdown and contraction of the automotive sector in developing regions

- 5.2.2 High cost of Construction Materials

- 5.3 Opportunities

- 5.3.1 Green Building Initiatives

- 5.3.2 Infrastructure Development

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Wood

- 6.1.2 Brics

- 6.1.3 Concrete

- 6.1.4 Other Product Types

- 6.2 By Constrution Type

- 6.2.1 Resdential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.2.4 Infrastructure

- 6.3 By Goegraphy

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Mexico

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 France

- 6.3.2.3 United Kingdom

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 ASEAN

- 6.3.3.5 Rest of APAC

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.5 Middle East & Africa

- 6.3.5.1 GCC

- 6.3.5.2 South Africa

- 6.3.5.3 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration, Major Players)

- 7.2 Company Profiles

- 7.2.1 Granite

- 7.2.2 HeidelbergCement

- 7.2.3 Hanson

- 7.2.4 LafargeHolcim

- 7.2.5 Trinity

- 7.2.6 Vulcan Materials

- 7.2.7 Dyckerhoff

- 7.2.8 Italcementi

- 7.2.9 Taiheiyo Cement

- 7.2.10 CRH

- 7.2.11 James Hardie

- 7.2.12 Boral

8 FUTURE OUTLOOK OF THE MARKET

9 Appendix

- 9.1 GDP Distribution, by Activity

- 9.2 Insights on Capital Flows

- 9.3 External Trade Statistics - Export and Import, by Product

- 9.4 Insights on Key Export Destinations

- 9.5 Insights on Key Import Origin Countries

轻质复合材料建筑市场分析及预测(至2035年):依类型、产品、服务、技术、应用、材料类型、製程、最终用户及功能划分

轻质复合材料建筑市场分析及预测(至2035年):依类型、产品、服务、技术、应用、材料类型、製程、最终用户及功能划分 日本轻质建筑材料市场:规模、份额、趋势和预测:按材料类型、密度、应用、最终用户和地区划分(2026-2034 年)

日本轻质建筑材料市场:规模、份额、趋势和预测:按材料类型、密度、应用、最终用户和地区划分(2026-2034 年) 轻质建筑材料市场-全球产业规模、份额、趋势、机会和预测,按类型、按材料类型、按建筑类型、按地区和竞争细分,2020-2030 年

轻质建筑材料市场-全球产业规模、份额、趋势、机会和预测,按类型、按材料类型、按建筑类型、按地区和竞争细分,2020-2030 年 美国轻型建筑紧固件市场规模、份额、趋势分析报告:按产品、屋顶系统、墙体系统、最终用途、分销管道、细分市场预测,2025-2033 年

美国轻型建筑紧固件市场规模、份额、趋势分析报告:按产品、屋顶系统、墙体系统、最终用途、分销管道、细分市场预测,2025-2033 年 2025 年至 2029 年全球轻质建筑材料市场

2025 年至 2029 年全球轻质建筑材料市场