|

市场调查报告书

商品编码

1683094

非卤化阻燃剂市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Non-Halogenated Flame Retardant Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

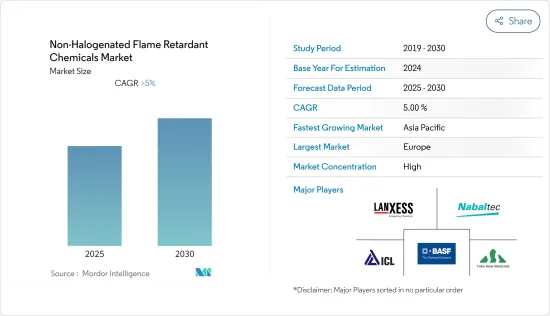

预测期内,非卤阻燃剂市场预计将以超过 5% 的复合年增长率成长

关键亮点

- 预计在预测期内,对阻燃剂(尤其是溴化阻燃剂)的环境和健康问题也将推动市场发展。

- 禁止使用卤素阻燃剂的更严格的立法似乎是未来的机会。

- 预计欧洲将在全球市场占据主导地位。不过,预计亚太地区在预测期内的成长速度最快。

无卤阻燃剂的市场趋势

建筑业的需求不断成长

- 家庭火灾是造成人员伤亡的主要原因之一。由于严格的消防安全法规,建筑材料和产品中使用非卤阻燃剂的主要原因是。在建筑物中,阻燃剂主要用于结构隔热材料。住宅和其他建筑物中使用隔热材料来保持舒适的温度并节省能源。

- 主要隔热材料包括聚苯乙烯泡沫板和硬质聚氨酯泡棉板。此外,非卤化阻燃剂在聚烯泡沫中有着广泛的应用。聚烯泡沫主要用于建筑物的暖通空调应用、隔音和管道隔热材料。

- 在全球范围内,各种防火标准正在推动无卤阻燃剂市场的发展。由于对使用阻燃剂的环境问题的日益关注,非卤化阻燃剂的应用显着增加。

- 磷基阻燃剂是主要用于聚氨酯发泡体,尤其是液体材料的非卤素阻燃剂。硬质聚氨酯泡沫中使用的阻燃剂有三种形式:添加型液体阻燃剂、反应型液体阻燃剂和固体阻燃剂。

- 全球建筑业正在健康成长,亚太地区和中东及北非地区由于市场机会众多、住宅需求不断增加以及人口不断增长,对建筑业的投资巨大。

- 因此,预计所有上述因素都将在预测期内推动对非卤阻燃剂的需求。

欧洲主导市场

- 预计欧洲将主导全球市场。德国经济是欧洲最大、世界第五大经济体。

- 德国的电子产业规模位居欧洲第一、世界第五。电气和电子产业占德国工业总产值的 10% 以上,占国内生产总值) 的 3% 左右。此外,电气和电子产业占德国总直接投资的23%左右。

- 德国汽车工业占德国工业总收益的20%左右。德国约占欧洲乘用车产量的30%。全球前100家汽车供应商中有16家位于德国。

- 德国拥有世界一流的研发基础设施和完整的产业价值链整合,汽车产业环境十分完善。这使得公司能够开发和采用最尖端科技。德国也拥有欧洲最多的OEM工厂,41个组装和引擎生产厂占欧洲汽车总产量的三分之一。

- 过去二十年,德国航太业经历了长足的发展。德国联邦经济和能源部将航太工业列为德国的重点产业,具有高成长率和强大的工业核心。

- 由于上述所有因素,预计预测期内该地区的非卤化阻燃剂市场将会成长。

无卤阻燃剂产业概况

全球非卤阻燃化学品市场正在整合,五大主要企业占据全球市场的巨大份额。主要企业包括 Nabaltec AG、Huber Engineered Materials、 BASF SE、ICL 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 关于溴化阻燃剂和其他阻燃剂的环境和健康问题

- 亚太地区基础建设活动活性化

- 消费性电子电气製造业成长

- 限制因素

- 氢氧化物不适合高温应用

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 原料分析

- 监理政策分析

第五章 市场区隔

- 类型

- 无机

- 氢氧化铝

- 氢氧化镁

- 硼化合物

- 磷光

- 氮化合物

- 其他的

- 无机

- 最终用户产业

- 电气和电子

- 建筑和施工

- 运输

- 纺织品和家具

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率/排名分析

- 主要企业策略

- 公司简介

- Apexical Inc.

- BASF SE

- Clariant

- Daihachi Chemical Industry Co. Ltd

- DIC Corporation

- Eti Maden

- Huber Engineered Materials

- ICL

- Italmatch Chemicals SpA

- Jiangsu Jacques Technology Co. Ltd

- LANXESS

- MPI Chemie BV

- Nabaltec AG

- Nippon Carbide Indestries Co. Inc.(Sanwa Chemical Industry Co. Ltd)

- NYACOL Nano Technologies Inc.

- Rin Kagaku Kogyo Co. Ltd

- Shandong Brother Sci. &Tech. Co. Ltd

- Thor

- TOR Minerals

第七章 市场机会与未来趋势

- 禁止卤素阻燃剂的立法日益增多

- 积极研发无卤阻燃剂

简介目录

Product Code: 47876

The Non-Halogenated Flame Retardant Chemicals Market is expected to register a CAGR of greater than 5% during the forecast period.

Key Highlights

- Environmental and health concerns regarding brominated and other flame retardants are also expected to drive the market during the forecast period.

- Increasing legislation banning of halogenated flame retardants is likely to act as an opportunity in the future.

- Europe is expected to dominate the market across the globe. While, Asia-Pacific region is likley to witness the fastest growth during the forecast period.

Non-Halogenated Flame Retardants Chemicals Market Trends

Increasing Demand from the Buildings and Construction Industry

- Household fires are one of the primarily causes for the loss of human life. Non-halogenated flame retardants are used in building materials and products, primarily due to strict fire safety regulations. In buildings, flame retardants are majorly used in structural insulation. Insulations are used in homes and other buildings, in order to maintain comfortable temperature, while conserving energy.

- The major insulation materials include polystyrene foam boards and rigid polyurethane foam panels. Moreover, non-halogenated flame retardants find major applications in polyolefin foams. They are used in buildings, primarily in the HVAC applications, such as sound insulation and thermal insulation for pipes.

- Globally, various fire standards are driving the market for non-halogenated flame retardants. With the increasing environment concerns related to the use of flame retardants, the applications for non-halogenated flame retardants have been increasing significantly.

- Phosphorus-based flame retardants are mostly used non-halogenated flame retardants in polyurethane foams, especially in liquid substances. The flame retardants used for rigid PU foams are available in three forms, such as additive liquid flame retardants, reactive liquid flame retardants, and solid flame retardants.

- The global construction industry is growing at a healthy rate, where the Asia-Pacific and Middle East & African regions are witnessing huge investment in the construction sector due to numerous market opportunities available in these markets, along with the increasing demand for residential houses and the growing population.

- Thus, all the aforementioned factors are expected to drive the demand for non-halogenated flame retardant chemicals, during the forecast period.

Europe to Dominate the Market

- Europe region is expected to dominate the global market. The German economy is the largest in Europe, and fifth in the world.

- The German electronic industry is the Europe's biggest, and the fifth largest worldwide. The electrical and electronics industry accounted for more than 10% of the total German industrial production and about 3% of the country's gross domestic product (GDP). Moreover, the electrical and electronics industry accounted for around 23% of the entire FDI of the country.

- The German automotive industry accounted for approximately 20% of the total revenue of the German industries. Germany accounted for approximately 30% of the total passenger cars manufactured in the European region. Sixteen of the world's 100 top automotive suppliers are based in Germany.

- The country's world-class R&D infrastructure and complete industry value chain integration create a well-established automotive environment. This enables companies to develop and adopt cutting-edge technologies. The country also has the largest number of OEM plants in Europe, with 41 assembly and engine production plants that contribute to one third of the total automobile production in Europe.

- The German aerospace industry witnessed a substantial growth over the past two decades. The Federal Ministry of Economic Affairs and Energy lists aerospace as a key industry in Germany, with high growth rates and a strong industrial core.

- Owing to all the aforementioned factors, the maret for non-halogenated flame retardant chemicals is projected to grow in the region during the forecast period.

Non-Halogenated Flame Retardants Chemicals Industry Overview

The global non-halogenated flame retardant chemicals market is consolidated in nature, with the top five players accounting for a significant share in the global market. The major companies include Nabaltec AG, Huber Engineered Materials, BASF SE, and ICL, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Environmental and Health Concerns Regarding Brominated and Other Flame Retardants

- 4.1.2 Increasing Infrastructure Activities in Asia-Pacific

- 4.1.3 Rising Consumer Electrical and Electronic Goods Manufacturing

- 4.2 Restraints

- 4.2.1 Non-suitability of Hydroxides to High Temperature Applications

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Raw Material Analysis

- 4.6 Regulatory Policy Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Inorganic

- 5.1.1.1 Aluminum Hydroxide

- 5.1.1.2 Magnesium Hydroxide

- 5.1.1.3 Boron Compounds

- 5.1.2 Phosphorus

- 5.1.3 Nitrogen

- 5.1.4 Other Types

- 5.1.1 Inorganic

- 5.2 End-user Industry

- 5.2.1 Electrical and Electronics

- 5.2.2 Buildings and Construction

- 5.2.3 Transportation

- 5.2.4 Textiles and Furniture

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Apexical Inc.

- 6.4.2 BASF SE

- 6.4.3 Clariant

- 6.4.4 Daihachi Chemical Industry Co. Ltd

- 6.4.5 DIC Corporation

- 6.4.6 Eti Maden

- 6.4.7 Huber Engineered Materials

- 6.4.8 ICL

- 6.4.9 Italmatch Chemicals SpA

- 6.4.10 Jiangsu Jacques Technology Co. Ltd

- 6.4.11 LANXESS

- 6.4.12 MPI Chemie BV

- 6.4.13 Nabaltec AG

- 6.4.14 Nippon Carbide Indestries Co. Inc. (Sanwa Chemical Industry Co. Ltd)

- 6.4.15 NYACOL Nano Technologies Inc.

- 6.4.16 Rin Kagaku Kogyo Co. Ltd

- 6.4.17 Shandong Brother Sci. &Tech. Co. Ltd

- 6.4.18 Thor

- 6.4.19 TOR Minerals

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Legislation Banning of Halogenated Flame Retardants

- 7.2 Active R&D in Non-halogenated Flame Retardants

02-2729-4219

+886-2-2729-4219

生物降解阻燃剂市场分析及预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、功能、形态、工艺

生物降解阻燃剂市场分析及预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、功能、形态、工艺 生物基阻燃剂市场按产品类型、树脂类型、最终用途产业、应用和分销管道划分,全球预测(2026-2032年)

生物基阻燃剂市场按产品类型、树脂类型、最终用途产业、应用和分销管道划分,全球预测(2026-2032年) 非卤化阻燃剂市场-2026-2031年预测

非卤化阻燃剂市场-2026-2031年预测 复合材料用非卤化阻燃剂市场预测(至2032年):按类型、树脂类型、复合材料材料类型、配方、应用、最终用户和地区分類的全球分析

复合材料用非卤化阻燃剂市场预测(至2032年):按类型、树脂类型、复合材料材料类型、配方、应用、最终用户和地区分類的全球分析 全球非卤阻燃剂市场规模研究(按产品、应用、最终用途划分)及区域预测(2022-2032 年)

全球非卤阻燃剂市场规模研究(按产品、应用、最终用途划分)及区域预测(2022-2032 年) 无卤阻燃剂市场规模、份额、趋势分析报告:2024-2030 年按产品、应用、最终用途、地区和细分市场进行的预测

无卤阻燃剂市场规模、份额、趋势分析报告:2024-2030 年按产品、应用、最终用途、地区和细分市场进行的预测