|

市场调查报告书

商品编码

1939051

汽车传动轴:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Drive Shaft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

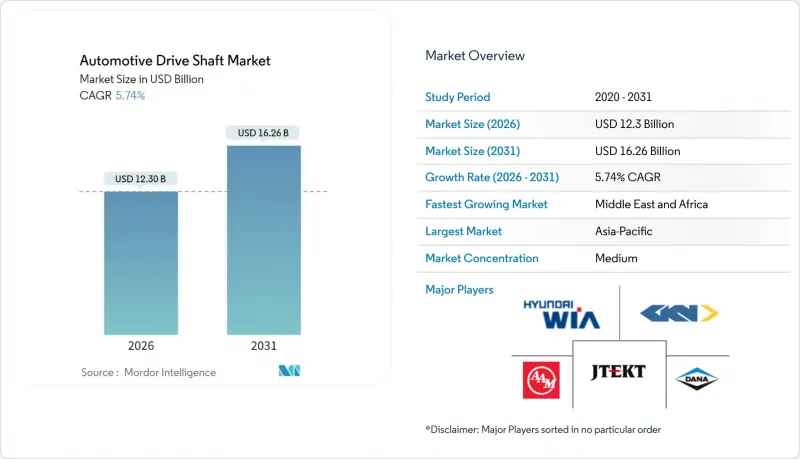

预计到 2026 年,汽车传动轴市场规模将达到 123 亿美元。

预计该产业规模将从 2025 年的 116.3 亿美元成长到 2031 年的 162.6 亿美元,2026 年至 2031 年的复合年增长率为 5.74%。

这种成长轨迹反映出市场已做好适应电气化需求的准备,同时又希望维持传统动力传动系统的强劲性能。从多部件传统传动轴转向精密轻量化替代方案的转变,在汽车製造商需要在各种车辆架构中平衡成本压力和性能要求的同时,也带来了变革和机会。

全球汽车传动轴市场趋势与洞察

E轴整合重组了轴结构

电动桥的整合从根本上改变了传动轴的要求,它摒弃了传统的多部件结构,同时对后轮驱动电动车架构中的高精度、轻量化传动轴提出了更高的需求。特斯拉 Model S Plaid 和BMW iX 就是很好的例子,它们展示了整合式马达-变速箱单元如何减少零件数量,同时又需要用于扭力向量控制的专用碳纤维传动轴。这种架构的转变解释了为什么儘管每辆车的传动轴使用量可能会下降,但纯电动车 (BEV) 市场仍将以 14.25% 的复合年增长率成长。舍弗勒计划于 2025 年 4 月为一家中国电动汽车製造商生产滚珠螺桿驱动装置,这表明供应商如何将其精密製造能力从传统的传动系统应用转移到电动动力传动系统领域。这种转变为拥有尖端材料专业知识的供应商创造了机会,同时也为以钢铁为主导的传统製造商带来了挑战。

碳纤维的应用已超越高端市场,加速普及

在对轻量化和提升NVH(噪音、振动与声振粗糙度)性能的需求驱动下,碳纤维复合材料传动轴的应用范围正从豪华车领域扩展到高性能量产车型。福特最新的F-150系列和BMW3系列车型均采用碳纤维传动轴,在实现燃油经济性目标的同时,也能在高扭力工况下保持耐用性。这种材料比钢轻60%,允许使用更长的传动轴而不会对转速造成显着限制,这使其在空间布局受限的全轮驱动(AWD)车型中尤为重要。随着生产规模的扩大,碳纤维传动轴的成本每年下降约15-20%,使得在量产车型中采用碳纤维传动轴变得经济实惠,从而摆脱了传统高端市场的限制。随着汽车製造商优先考虑轻量化策略以抵消混合动力和电动动力传动系统中电池重量的增加,这一趋势正在加速发展。

原材料价格波动给利润率带来压力。

碳纤维和特殊钢价格的波动正给整个传动轴供应链的利润率带来压力。碳纤维价格受航太需求週期和能源成本的影响,每季波动幅度高达25%至30%。由于碳纤维生产集中在少数几家全球供应商(东丽、SGL Carbon和Hexcel)手中,当航太需求復苏或可再生能源应用需求激增时,就会出现供应瓶颈。用于高性能应用的特殊钢也面临类似的价格波动,由于采矿业中断以及地缘政治紧张局势对原材料供应的影响,铬钼合金价格预计在2024年上涨18%。这种波动迫使供应商实施动态定价机制和避险策略,使长期OEM合约变得更加复杂。这可能会延缓尖端材料在成本敏感型应用中的推广。

细分市场分析

到2025年,中空轴将占据56.63%的市场份额,这反映了与实心轴相比,空心轴在重量减轻和製造成本效率方面实现了最佳平衡。其设计优势包括优化的壁厚,与实心轴相比,可在保持相当扭矩容量的同时,实现40-50%的减重。复合材料/碳纤维增强复合材料(CFRP)轴的市场份额将在2031年之前以12.62%的复合年增长率增长,这主要得益于其在高端车型和对性能要求极高的应用中的广泛应用,在这些应用中,减轻重量可以抵消更高的材料成本。两段式/滑入式设计满足了紧凑型车辆架构(尤其是前轮驱动车辆)的特定空间布局要求,在这些车辆中,空间限制使得安装一体式轴变得困难。

重型商用车和越野车领域对实心轴的需求持续成长,因为耐用性要求比重量因素更为重要。这一领域的稳定性反映了商用车製造商的保守态度,他们优先考虑的是久经考验的可靠性,而非尖端材料。中空轴製造技术的创新,包括液压成形和先进焊接技术,在保持成本竞争力的同时,也持续拓展其在各车型领域的适用性。

到2025年,传统钢材将维持67.32%的市场份额,这反映了其成本效益和在全球供应链中成熟的製造基础设施。然而,碳纤维/碳纤维增强复合材料(CFRP)到2031年将以14.33%的复合年增长率快速成长,这标誌着轻量化解决方案的应用范围正在从高端应用转向高端应用。高强度合金钢将用于中等强度的应用,在这些应用中,减重要求超过了传统钢材的能力,但成本限制了碳纤维的普及。铝材的应用将集中在一些特定的应用场景,在这些场景中,耐腐蚀性和适度的减重要求使得铝材的溢价高于钢材。

这种材料转变反映了汽车产业为实现轻量化所采取的策略,其驱动力源自于燃油经济性法规和优化电动车续航里程的需求。碳纤维製造规模的扩大,包括自动化纤维铺放和树脂转注成形,既降低了生产成本,也提高了品质稳定性。这项技术进步使得碳纤维得以应用于传统上由钢材主导的大批量生产领域,尤其是在传动轴等对长度和临界转速有较高要求的领域,轻量材料更受青睐。

区域分析

到2025年,亚太地区将占据全球45.72%的市场份额,这主要得益于中国大规模的汽车生产规模以及东南亚国协不断扩大的商用车产能。该地区的成长动力主要来自基础建设规划带来的商用车需求成长,尤其是产业走廊的建设,为货运需求的持续成长创造了条件,尤其是在印尼、泰国和越南。 2025年2月,中国商用车产量达到31.8万辆(年增36.6%),充分展现了该地区对轴的需求规模。由于接近性主要整车製造商的生产基地以及成熟的供应链关係,区域供应商能够降低物流成本并前置作业时间。

北美和欧洲是成熟的汽车市场,拥有完善的汽车製造地,推动各细分市场对传动轴部件的稳定需求。北美市场的成长主要集中在SUV和皮卡领域,全轮驱动(AWD)的兴起带动了对轴间传动轴的需求。同时,由于严格的排放气体法规,欧洲市场优先采用轻量化材料。这两个地区对高端应用和先进材料的关注,为拥有碳纤维技术和精密製造能力的供应商创造了机会。两国政府的奖励,例如美国的「48C条款」计画和欧盟的「绿色交易」产业政策,都支持当地製造业发展,促进了国内零件生产。

中东和非洲地区预计将成为成长最快的地区,到2031年复合年增长率将达到8.77%,这主要得益于全部区域的基础设施发展计画和不断增长的汽车保有量。南非汽车製造业的扩张以及阿联酋物流枢纽的发展,正在创造对商用车零件的需求,而产油国的经济多元化计划则为汽车组装业务提供了支持。该地区的成长反映了广泛的工业化趋势,这些趋势正在创造对交通基础设施和商用车车队的持续需求。然而,各国市场发展仍然不平衡,政策支持和製造能力的差异导致了成长轨蹟的分化。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动车中整合电驱动轴减少了对多部件轴的需求,但也推动了对高精度、轻型传动轴的需求。

- 高性能和豪华车辆中碳纤维复合材料轴的快速应用

- 政府加大对国内轻质材料製造业的诱因

- 北美和欧洲的SUV车型将过渡到基于后轮驱动的全轮驱动系统

- 东协和非洲工业走廊商用车产量快速成长

- 无线传动系统分析实现预测性维护改造

- 市场限制

- 原料价格波动(碳纤维、特殊钢)

- 东亚精密管材拉拔供应链集中

- 中国和欧盟内燃机乘用车销售下滑

- 复合复合材料分层造成的保固责任风险

- 价值/价值链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 依设计类型

- 中空轴

- 实心轴

- 两件式/插入式管

- 复合材料/碳纤维轴

- 材料

- 普通钢材

- 高强度合金钢

- 铝

- 碳纤维/CFRP

- 按职位类型

- 后桥轴

- 前轴

- 四轮驱动轴间/传动轴

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 按动力传动系统/推进系统

- 内燃机(ICE)

- 混合动力汽车(HEV 和 PHEV)

- 电池式电动车(BEV)

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- GKN PLC(Melrose Industries PLC)

- Dana Incorporated

- JTEKT Corporation

- Hyundai Wia Corporation

- Nexteer Automotive Group Ltd.

- American Axle and Manufacturing Holdings Inc.

- NTN Corporation

- Showa Corporation

- IFA Rotorion Holding GmbH

- ZF Friedrichshafen AG

- Meritor Inc.

- Neapco Holdings LLC

- GSP Automotive Group

- Wanxiang Qianchao Co. Ltd.

- Hitachi Astemo Ltd.

- ElringKlinger AG(Composite Shaft Division)

- Poclain Powertrain

- Jilin Jinghua Automotive Parts

- Univance Corporation

- Yujiang Vicray Industrial Co.

第七章 市场机会与未来展望

Automotive drive shaft market size in 2026 is estimated at USD 12.3 billion, growing from 2025 value of USD 11.63 billion with 2031 projections showing USD 16.26 billion, growing at 5.74% CAGR over 2026-2031.

This growth trajectory reflects the market's adaptation to electrification demands while maintaining robust performance in traditional powertrains. The transition from multi-piece conventional shafts to high-precision lightweight alternatives creates both disruption and opportunity, as OEMs balance cost pressures with performance requirements across diverse vehicle architectures.

Global Automotive Drive Shaft Market Trends and Insights

E-axle Integration Reshapes Shaft Architecture

E-axle integration fundamentally alters drive shaft requirements by eliminating traditional multi-piece configurations while creating demand for high-precision lightweight propeller shafts in rear-wheel-drive electric architectures. Tesla's Model S Plaid and BMW iX demonstrate how integrated motor-gearbox units reduce component count yet require specialized carbon-fiber propeller shafts for torque vectoring applications. This architectural shift explains why BEV segments grow at 14.25% CAGR despite potentially reducing per-vehicle shaft content. Schaeffler's April 2025 production launch of ball screw drives for Chinese EV manufacturers illustrates how suppliers adapt precision manufacturing capabilities from traditional driveline applications to electric powertrains. The transition creates opportunities for suppliers with advanced materials expertise while challenging traditional steel-focused manufacturers.

Carbon-Fiber Adoption Accelerates Beyond Premium Segments

Carbon-fiber composite shaft adoption extends beyond luxury applications into performance-oriented mainstream vehicles, driven by weight reduction mandates and NVH improvement requirements. Ford's latest F-150 variants and BMW's 3-Series incorporate carbon-fiber propeller shafts to achieve fuel economy targets while maintaining durability under high-torque conditions. The material's 60% weight reduction compared to steel enables longer shaft lengths without critical speed limitations, particularly valuable in AWD configurations where packaging constraints intensify. Manufacturing scale improvements reduce carbon-fiber shaft costs by approximately 15-20% annually, making adoption economically viable for volume applications beyond the traditional premium segment focus. This trend accelerates as OEMs prioritize lightweighting strategies to offset battery weight penalties in hybrid and electric powertrains.

Raw Material Price Volatility Pressures Margins

Carbon fiber and specialty steel price volatility creates margin pressure across the drive shaft supply chain, with carbon fiber prices fluctuating 25-30% quarterly based on aerospace demand cycles and energy costs. The concentration of carbon fiber production among few global suppliers (Toray, SGL Carbon, Hexcel) creates supply bottlenecks when demand surges from aerospace recovery and renewable energy applications. Specialty steel grades used in high-performance applications face similar volatility, with chromium-molybdenum alloy prices increasing 18% in 2024 due to mining disruptions and geopolitical tensions affecting raw material supply. This volatility forces suppliers to implement dynamic pricing mechanisms and hedge strategies that complicate long-term OEM contracts, potentially slowing adoption of advanced materials in cost-sensitive applications.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives Drive Localization

- AWD Proliferation Drives Inter-Axle Demand

- Supply Chain Concentration Creates Vulnerability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hollow shafts command 56.63% market share in 2025, reflecting their optimal balance of weight reduction and manufacturing cost efficiency compared to solid alternatives. The design's advantages include 40-50% weight reduction versus solid shafts while maintaining equivalent torque capacity through optimized wall thickness engineering. Composite/CFRP shafts accelerate at 12.62% CAGR through 2031, driven by premium vehicle adoption and performance applications where weight savings justify higher material costs. Two-piece/slip-in tube configurations serve specific packaging requirements in compact vehicle architectures, particularly in front-wheel-drive applications where space constraints limit single-piece shaft installation.

Solid shaft applications persist in heavy-duty commercial vehicles and off-road applications where durability requirements outweigh weight considerations. The segment's stability reflects commercial vehicle manufacturers' conservative approach, prioritizing proven reliability over advanced materials. Manufacturing innovations in hollow shaft production, including hydroforming and advanced welding techniques, continue to expand the design's applicability across vehicle segments while maintaining cost competitiveness against solid alternatives.

Conventional steel maintains 67.32% market share in 2025, reflecting its cost-effectiveness and established manufacturing infrastructure across global supply chains. However, carbon-fiber/CFRP materials surge at 14.33% CAGR through 2031, indicating a fundamental shift toward lightweight solutions that extends beyond premium applications. High-strength alloy steel serves intermediate applications where weight reduction requirements exceed conventional steel capabilities but cost constraints limit carbon-fiber adoption. Aluminum applications focus on specific use cases where corrosion resistance and moderate weight reduction justify the material premium over steel alternatives.

The material transition reflects broader automotive lightweighting mandates driven by fuel economy regulations and electric vehicle range optimization. Carbon-fiber manufacturing scale improvements, including automated fiber placement and resin transfer molding, reduce production costs while improving quality consistency. This technological advancement enables carbon-fiber adoption in volume applications previously dominated by steel, particularly in propeller shaft applications where length and critical speed requirements favor lightweight materials.

The Automotive Drive Shaft Market Report is Segmented by Design Type (Hollow Shaft, Solid Shaft, Two-piece/Slip-in Tube, and More), Material (Conventional Steel, and More), Position Type (Rear Axle Shafts, and More), Vehicle Type (Passenger Cars, and More), Powertrain/Propulsion (ICE, Hybrid, BEV), Sales Channel (OEM, Aftermarket), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominates with 45.72% market share in 2025, driven by China's massive vehicle production scale and ASEAN's expanding commercial vehicle manufacturing capabilities. The region's growth stems from infrastructure development programs that boost commercial vehicle demand, particularly in Indonesia, Thailand, and Vietnam where industrial corridor development creates sustained freight transportation requirements. China's February 2025 commercial vehicle production of 318,000 units, representing 36.6% year-over-year growth, demonstrates the scale of demand driving regional shaft requirements. Regional suppliers benefit from proximity to major OEM production facilities and established supply chain relationships that reduce logistics costs and lead times.

North America and Europe represent mature markets with established automotive manufacturing bases that drive steady demand for drive shaft components across diverse vehicle segments. North American growth focuses on SUV and pickup truck segments where AWD proliferation creates demand for inter-axle propeller shafts, while European markets emphasize lightweight materials adoption driven by stringent emissions regulations. The regions' focus on premium applications and advanced materials creates opportunities for suppliers with carbon-fiber expertise and precision manufacturing capabilities. Government incentives in both regions support local manufacturing development, with the U.S. Section 48C program and European Union's Green Deal industrial policy encouraging domestic component production.

Middle-East and Africa emerges as the fastest-growing region at 8.77% CAGR through 2031, driven by infrastructure development programs and increasing vehicle ownership rates across the region. South Africa's automotive manufacturing expansion and UAE's logistics hub development create demand for commercial vehicle components, while oil-rich nations economic diversification programs support automotive assembly operations. The region's growth reflects broader industrialization trends that create sustained demand for transportation infrastructure and commercial vehicle fleets. However, the market is uneven across countries, with differing policy support and manufacturing capacity shaping growth trajectories.

- GKN PLC (Melrose Industries PLC)

- Dana Incorporated

- JTEKT Corporation

- Hyundai Wia Corporation

- Nexteer Automotive Group Ltd.

- American Axle and Manufacturing Holdings Inc.

- NTN Corporation

- Showa Corporation

- IFA Rotorion Holding GmbH

- ZF Friedrichshafen AG

- Meritor Inc.

- Neapco Holdings LLC

- GSP Automotive Group

- Wanxiang Qianchao Co. Ltd.

- Hitachi Astemo Ltd.

- ElringKlinger AG (Composite Shaft Division)

- Poclain Powertrain

- Jilin Jinghua Automotive Parts

- Univance Corporation

- Yujiang Vicray Industrial Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-axle integration in BEVs reduces need for multi-piece shafts but drives demand for high-precision lightweight prop-shafts

- 4.2.2 Rapid adoption of carbon-fiber composite shafts in performance and premium vehicles

- 4.2.3 Increasing government incentives for local lightweight-material manufacturing

- 4.2.4 Shift toward rear-wheel-based AWD for SUVs in North America and Europe

- 4.2.5 Booming CV production in ASEAN and Africa industrial corridors

- 4.2.6 Over-the-air driveline analytics unlocking predictive-maintenance retrofits

- 4.3 Market Restraints

- 4.3.1 Raw-material (carbon fiber, specialty steel) price volatility

- 4.3.2 Supply-chain concentration of precision tube-drawing in East Asia

- 4.3.3 Declining ICE passenger-car sales in China and EU

- 4.3.4 Warranty-liability risks from composite shaft delamination

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Design Type

- 5.1.1 Hollow Shaft

- 5.1.2 Solid Shaft

- 5.1.3 Two-piece/Slip-in Tube

- 5.1.4 Composite/Carbon-Fiber Shaft

- 5.2 By Material

- 5.2.1 Conventional Steel

- 5.2.2 High-Strength Alloy Steel

- 5.2.3 Aluminum

- 5.2.4 Carbon-Fiber/CFRP

- 5.3 By Position Type

- 5.3.1 Rear Axle Shafts

- 5.3.2 Front Axle Shafts

- 5.3.3 Inter-axle/Propeller Shafts for AWD

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.5 By Powertrain / Propulsion

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Hybrid (HEV and PHEV)

- 5.5.3 Battery Electric Vehicle (BEV)

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle-East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Egypt

- 5.7.5.4 South Africa

- 5.7.5.5 Rest of Middle-East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 GKN PLC (Melrose Industries PLC)

- 6.4.2 Dana Incorporated

- 6.4.3 JTEKT Corporation

- 6.4.4 Hyundai Wia Corporation

- 6.4.5 Nexteer Automotive Group Ltd.

- 6.4.6 American Axle and Manufacturing Holdings Inc.

- 6.4.7 NTN Corporation

- 6.4.8 Showa Corporation

- 6.4.9 IFA Rotorion Holding GmbH

- 6.4.10 ZF Friedrichshafen AG

- 6.4.11 Meritor Inc.

- 6.4.12 Neapco Holdings LLC

- 6.4.13 GSP Automotive Group

- 6.4.14 Wanxiang Qianchao Co. Ltd.

- 6.4.15 Hitachi Astemo Ltd.

- 6.4.16 ElringKlinger AG (Composite Shaft Division)

- 6.4.17 Poclain Powertrain

- 6.4.18 Jilin Jinghua Automotive Parts

- 6.4.19 Univance Corporation

- 6.4.20 Yujiang Vicray Industrial Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

汽车传动轴市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车传动轴市场机会、成长要素、产业趋势分析及2026年至2035年预测 电机轴市场按应用、类型、材料、直径范围、涂层、销售管道和最终用途行业划分,全球预测(2026-2032年)

电机轴市场按应用、类型、材料、直径范围、涂层、销售管道和最终用途行业划分,全球预测(2026-2032年) 汽车传动轴市场规模、份额和成长分析(按设计类型、地点类型、车辆类型、销售管道和地区划分)-2026-2033年产业预测

汽车传动轴市场规模、份额和成长分析(按设计类型、地点类型、车辆类型、销售管道和地区划分)-2026-2033年产业预测 轴带式发电机市场-2025年至2030年预测汽车传动轴市场(按车辆类别、材料、应用和最终用户划分)—2025-2032 年全球预测

轴带式发电机市场-2025年至2030年预测汽车传动轴市场(按车辆类别、材料、应用和最终用户划分)—2025-2032 年全球预测 2025年全球汽车传动轴市场报告

2025年全球汽车传动轴市场报告![汽车传动轴市场 - [传动轴类型:单件式、多件式;驱动系统:两轮驱动(全轴、半轴)、四轮驱动] - 全球产业分析、规模、份额、成长、趋势及预测,2025-2035 年](/sample/img/cover/42/default_cover_6.png) 汽车传动轴市场 - [传动轴类型:单件式、多件式;驱动系统:两轮驱动(全轴、半轴)、四轮驱动] - 全球产业分析、规模、份额、成长、趋势及预测,2025-2035 年

汽车传动轴市场 - [传动轴类型:单件式、多件式;驱动系统:两轮驱动(全轴、半轴)、四轮驱动] - 全球产业分析、规模、份额、成长、趋势及预测,2025-2035 年 汽车用驱动轴的全球市场的评估:各车辆类型,不同设计,位置,各地区,机会,预测(2018年~2032年)

汽车用驱动轴的全球市场的评估:各车辆类型,不同设计,位置,各地区,机会,预测(2018年~2032年) 汽车传动轴市场报告(按传动轴类型、设计类型、位置类型、材料、车辆类型、销售管道(原始设备製造商、售后市场)和地区)2025 年至 2033 年

汽车传动轴市场报告(按传动轴类型、设计类型、位置类型、材料、车辆类型、销售管道(原始设备製造商、售后市场)和地区)2025 年至 2033 年 汽车传动轴市场 - 全球产业规模、份额、趋势、机会和预测,按设计类型、位置类型、车辆类型、地区和竞争细分,2019-2029F

汽车传动轴市场 - 全球产业规模、份额、趋势、机会和预测,按设计类型、位置类型、车辆类型、地区和竞争细分,2019-2029F