|

市场调查报告书

商品编码

1683165

北美聚对苯二甲酸乙二醇酯 (PET) 市场 -市场占有率分析、行业趋势和成长预测(2025-2030 年)North America Polyethylene Terephthalate (PET) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

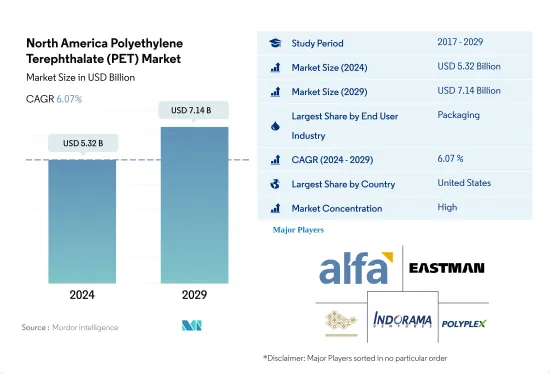

北美聚对苯二甲酸乙二醇酯 (PET) 市场规模预计在 2024 年为 53.2 亿美元,预计到 2029 年将达到 71.4 亿美元,预测期内(2024-2029 年)的复合年增长率为 6.07%。

预测期内,包装和电气电子行业不断增长的需求可能会推动 PET 的需求

- 聚对苯二甲酸乙二醇酯在包装和电气电子领域有广泛的应用,包括食品和饮料包装,特别是方便装软性饮料、果汁和水包装、线圈形式、电气封装、电气设备、螺线管和智慧电錶。 2022 年,包装和电气及电子将分别占该地区聚对苯二甲酸乙二醇酯市场收益的约 96.6% 和 2.0%。

- 由于单人家庭数量大幅增加和繁忙的生活方式推动了对功能性、预包装和方便食品的需求,包装行业是该地区最大的 PET 树脂消费者。北美是全球包装产业的主导市场之一,2022年塑胶包装产量将达2,240万。

- 电气和电子行业是该地区第二大行业,尤其是在美国。该行业占 GDP 的 1.6%,预计 2022 年将为该地区创造 5,761 亿美元的收益,推动对电气和电子设备的需求,并推动电动车、自动机器人和绝密防御技术的出现。

- 由于 PET 在电气和电子产品中塑胶复合材料的应用日益广泛,电气和电子行业预计将成为该地区成长最快的 PET 树脂消费产业,预计复合年增长率为 8.18%。

美国凭藉其在包装行业的主导地位,在 PET 市场上占据主导地位

- 以体积计算,2022 年北美占全球聚对苯二甲酸乙二醇酯 (PET) 树脂消费量的 17.3%。 PET 树脂在包装产业占据主导地位,是北美使用的主要聚合物之一。

- 由于美国在北美包装产业占据主导地位,2022年美国将占最大的市场占有率,达到90.29%,与前一年同期比较7.68%。该国占北美塑胶包装产量的80%。更忙碌的生活方式、不断上升的购买力以及对快速便携包装商品的需求不断增长,正在推动美国包装行业和 PET 市场的发展。

- 快速消费品、食品饮料和电子商务行业的成长推动了墨西哥对 PET 树脂的需求。 2022年,该国的塑胶产量将占北美市场的11.91%。 2022年与前一年同期比较增长3.87%。预计未来几年塑胶包装产量的增加将推动该国对 PET 树脂的需求。

- 此外,墨西哥是北美成长最快的 PET 树脂消费国,预计预测期内复合以金额为准为 6.25%。该国的消费者正在寻找方便、安全、便携和产品新鲜的包装。因此,预计到 2029 年,该国的塑胶包装产量将达到 357 万吨,高于 2023 年的 279 万吨。

北美聚对苯二甲酸乙二醇酯 (PET) 市场趋势

技术创新强劲成长推动全产业成长

- 2017 年至 2019 年,北美电气和电子设备产量的复合年增长率超过 1.4%,这得益于技术进步以及智慧电视、冰箱和空调等家用电子电器产品的需求不断增加。电子创新的快速步伐推动着对更新、更快的电子产品的需求。因此,该地区的电气和电子设备产量也在增加。

- 由于受新冠疫情的影响,生产设施关闭、供应链中断以及各种其他限制因素,2020 年北美电子产品销售额与 2019 年相比下降了约 9%。结果,该地区2020年电气和电子设备生产收益与前一年同期比较下降了4.7%。

- 2021年该地区的消费性电子产品销售额将达到约1,130亿美元,较2020年成长4%。因此,2021年北美电气和电子设备产量与前一年同期比较增13.8%。

- 到 2027 年,北美预计将成为电气和电子设备生产的第三大地区,占全球市场份额的约 10.5%。虚拟实境、物联网解决方案和机器人等先进技术在家用电子电器产品中的出现,提高了效率并降低了成本,为家用电子电器产业带来了巨大利益。该地区的家用电子电器产业市场规模预计将从 2023 年的 1,276 亿美元成长到 2027 年的约 1,618 亿美元。因此,该地区对电气和电子产品的需求预计将会增加。

北美聚对苯二甲酸乙二醇酯 (PET) 产业概况

北美聚对苯二甲酸乙二醇酯 (PET) 市场相当集中,前五大公司占据了 97.94% 的市场。该市场的主要企业是 Alfa SAB de CV、伊士曼化学公司、台塑集团、Indorama Ventures Public Company Limited 和 Polyplex。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑和施工

- 电气和电子

- 包装

- 进出口趋势

- 聚对苯二甲酸乙二酯(PET)贸易

- 价格趋势

- 形态趋势

- 回收概述

- 聚对苯二甲酸乙二醇酯 (PET) 的回收趋势

- 法律规范

- 加拿大

- 墨西哥

- 美国

- 价值链与通路分析

第五章 市场区隔

- 最终用户产业

- 车

- 建筑和施工

- 电气和电子

- 工业/机械

- 包装

- 其他的

- 国家名称

- 加拿大

- 墨西哥

- 美国

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- Alfa SAB de CV

- Eastman Chemical Company

- Far Eastern New Century Corporation

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- JBF Industries Ltd

- Kimex SA de CV

- Polyplex

- Reliance Industries Limited

- SABIC

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The North America Polyethylene Terephthalate (PET) Market size is estimated at 5.32 billion USD in 2024, and is expected to reach 7.14 billion USD by 2029, growing at a CAGR of 6.07% during the forecast period (2024-2029).

Growing demand from packaging and electrical and electronics industry may drive the market demand for PET during the forecast period

- Polyethylene terephthalate has a wide range of applications in packaging and electrical and electronics, such as packaging foods and beverages, especially convenience-sized soft drinks, juices, and water, coil forms, electrical encapsulation, electrical devices, solenoids, and smart meters. Packaging and electrical and electronics accounted for around 96.6% and 2.0% of the revenue of the region's polyethylene terephthalate market, respectively, in 2022.

- The packaging industry is the largest consumer of PET resins in the region due to the significant increase in single-person homes and busy lifestyles, resulting in increased demand for functional, prepackaged, and convenient food products. North America is one of the dominant markets in the packaging industry at a global level, with plastic packaging production having a volume of 22.4 million in 2022.

- The electrical and electronics industry is the second largest in the region, especially in the United States. The industry accounted for 1.6% of the GDP and generated a revenue of USD 576.1 billion in 2022 in the region, increasing demand for electrical and electronics and encouraging the onset of electric vehicles, autonomous robots, and top-secret defense technologies.

- The electrical and electronics industry is expected to be the region's fastest-growing consumer of PET resins by revenue, with an expected CAGR of 8.18%, due to increasing applications of PET for plastic composites in electrical and electronics products.

United States to dominate the PET market due to the dominance of the packaging industry

- North America accounted for 17.3% of the global consumption of polyethylene terephthalate (PET) resin in 2022 by volume. PET resin is one of the key polymers used in North America due to its dominance in the packaging industry.

- The United States held the largest market share of 90.29% in 2022, a growth of 7.68% by value compared to the previous year, attributed to the country's dominance in the North American packaging industry. The country occupies 80% of North American plastic packaging production in terms of volume. Busier lifestyles, rising purchasing power, and growing demand for quick and on-the-go packaged goods are boosting the US packaging industry and the PET market.

- The growth of the FMCG, food, beverage, and e-commerce sectors drives Mexico's demand for PET resin. In 2022, the country's plastic production volume accounted for 11.91% of the North American market. In 2022, it increased at a rate of 3.87% from the previous year. The rising plastic packaging production is projected to drive the demand for PET resin in the country in the coming years.

- Mexico is also expected to be the fastest-growing consumer of PET resin in North America, with a CAGR of 6.25% in terms of value during the forecast period. Consumers in the country are looking for packaging that provides convenience and safety, portability, and product freshness. Thus, plastic packaging production in the country is expected to reach 3.57 million tons by 2029 from 2.79 million tons in 2023.

North America Polyethylene Terephthalate (PET) Market Trends

Strong growth of technological innovations to augment the overall growth of the industry

- Electrical and electronics production in North America witnessed a CAGR of over 1.4% between 2017 and 2019 owing to the advancement of technology, coupled with the increasing demand for consumer electronics products, such as smart TVs, refrigerators, air conditioners, and other products. The rapid pace of electronic technological innovation is driving the demand for newer and faster electronic products. As a result, it has also increased the electrical and electronics production in the region.

- Electronic device sales in North America fell by around 9% in 2020 compared to 2019, owing to the COVID-19 impact, because of the production facility shutdowns, supply chain disruptions, and various other constraints. As a result, revenue from electrical and electronics production in the region decreased by 4.7% in 2020 compared to the previous year.

- In 2021, the sales of consumer electronics in the region reached around USD 113 billion, 4% higher than in 2020. As a result, North America's electrical and electronics production grew by 13.8% in 2021 in terms of revenue compared to the previous year.

- By 2027, North America is projected to be the third-largest region for electrical and electronics production and account for a share of around 10.5% of the global market. The emergence of advanced technologies such as virtual reality, IoT solutions, and robotics into consumer electronic products to achieve efficiency and low cost has provided a significant advantage to the consumer electronics industry. The consumer electronics industry in the region is projected to reach a market volume of around USD 161.8 billion by 2027 from USD 127.6 billion in 2023. As a result, the demand for electrical and electronic products in the region is projected to increase.

North America Polyethylene Terephthalate (PET) Industry Overview

The North America Polyethylene Terephthalate (PET) Market is fairly consolidated, with the top five companies occupying 97.94%. The major players in this market are Alfa S.A.B. de C.V., Eastman Chemical Company, Formosa Plastics Group, Indorama Ventures Public Company Limited and Polyplex (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polyethylene Terephthalate (PET) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polyethylene Terephthalate (PET) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Canada

- 4.6.2 Mexico

- 4.6.3 United States

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Automotive

- 5.1.2 Building and Construction

- 5.1.3 Electrical and Electronics

- 5.1.4 Industrial and Machinery

- 5.1.5 Packaging

- 5.1.6 Other End-user Industries

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 United States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Eastman Chemical Company

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 Formosa Plastics Group

- 6.4.5 Indorama Ventures Public Company Limited

- 6.4.6 JBF Industries Ltd

- 6.4.7 Kimex SA de CV

- 6.4.8 Polyplex

- 6.4.9 Reliance Industries Limited

- 6.4.10 SABIC

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

按应用、来源类型、形态、等级、加工技术和颜色分類的再生聚对苯二甲酸乙二醇酯市场-2025-2032年全球预测

按应用、来源类型、形态、等级、加工技术和颜色分類的再生聚对苯二甲酸乙二醇酯市场-2025-2032年全球预测 2025年聚对苯二甲酸乙二醇酯(PET)杯全球市场报告

2025年聚对苯二甲酸乙二醇酯(PET)杯全球市场报告 聚对苯二甲酸乙二酯(PET) 织物市场规模、份额、趋势及预测(按来源、织物类型、形式、应用和地区),2025 年至 2033 年

聚对苯二甲酸乙二酯(PET) 织物市场规模、份额、趋势及预测(按来源、织物类型、形式、应用和地区),2025 年至 2033 年 聚对苯二甲酸乙二醇酯(PET)市场依产品种类、应用及地区划分2025年再生聚对苯二甲酸乙二酯全球市场报告2025年聚对苯二甲酸乙二酯全球市场报告2025年聚对苯二甲酸乙二醇酯(PET)及聚丁烯对苯二甲酸酯(PBT)树脂全球市场报告

聚对苯二甲酸乙二醇酯(PET)市场依产品种类、应用及地区划分2025年再生聚对苯二甲酸乙二酯全球市场报告2025年聚对苯二甲酸乙二酯全球市场报告2025年聚对苯二甲酸乙二醇酯(PET)及聚丁烯对苯二甲酸酯(PBT)树脂全球市场报告 再生PET(rPET)市场:全球产业分析、规模、份额、成长、趋势与预测(2025-2032)

再生PET(rPET)市场:全球产业分析、规模、份额、成长、趋势与预测(2025-2032) 聚对苯二甲酸乙二酯市场(2025-2029)

聚对苯二甲酸乙二酯市场(2025-2029) rPET(再生聚对苯二甲酸丙二酯)的全球市场:类别,各应用领域,各地区,机会,预测,2018年~2032年

rPET(再生聚对苯二甲酸丙二酯)的全球市场:类别,各应用领域,各地区,机会,预测,2018年~2032年