|

市场调查报告书

商品编码

1683195

夹层板市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Sandwich Panels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

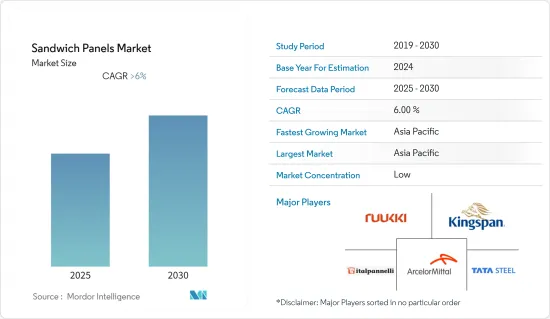

预计预测期内夹层板市场的复合年增长率将超过 6%。

新冠肺炎疫情为市场带来了负面影响。由于疫情影响,全球多个国家已实施封锁。由于供应链中断、资金短缺、劳动力短缺和封锁规定,建筑工作暂时停止。夹层板市场已从疫情中恢復并正在经历强劲成长。

关键亮点

- 短期内,预计冷藏仓储设施对夹层板的需求增加将推动市场发展。此外,预计使用 PVDF 基铝复合板也将有助于推动市场需求。

- 然而,一些夹层板的防火性能较差,预计这将抑制市场。

- 在预测期内,工业和商务用建筑的建设不断增加为夹层板市场带来了巨大的成长机会。

- 由于中国、日本和印度等国家的庞大消费量,预计亚太地区将主导市场。

夹层板市场趋势

工业领域占市场主导地位

- 在现代建筑中,使用高性能材料至关重要。高性能是指材质坚固、轻巧、耐用且用途广泛。由于这种可靠性,夹层板可以成为工业建筑的最佳选择之一。

- 其应用范围从工业建筑施工到隔热屋顶和墙板。夹层板在工业应用领域有着很高的需求,尤其是在冷藏仓储设施和仓库。

- 冷藏仓库的数量正在迅速增长,以延长和保护新鲜农产品、鱼贝类、冷冻食品、胶卷、化学品和药品的保质期。

- 跨国公司食品零售连锁店的扩张导致对冷藏仓库的需求增加。由于这些因素,预计全球对夹层板的需求将会成长。

- 预计2021年全球低温运输物流市场规模将达2,558.2亿美元,未来8年将突破4,100亿美元。

- 2021 年亚太低温运输物流市场规模价值 689.7 亿美元,而 2020 年为 617.5 亿美元。未来六年,预计该市场规模将达到近 1,340 亿美元。

- 2021 年欧洲低温运输物流产业价值超过 850 亿美元,预计到 2025 年将成长到 1,128 亿美元。使用冷藏包装解决方案对供应链中的货物进行温控移动,以保护新鲜农产品、水产品、冷冻食品和药品等产品的品质。这就是所谓的低温运输物流。

- 根据印度製药协会预测,到2021年,药品将占印度低温运输仓库的三分之二以上。低廉的製造成本和政府补贴意味着印度拥有全球第三大製药业务。

- 预计上述因素将推动工业领域的发展并在预测期内增加对夹层板的需求。

亚太地区主导全球市场

- 由于中国、印度和日本等国家的需求旺盛,预计亚太地区将主导全球市场。

- 中国是亚太地区主要建设活动国家之一,工业和建筑业约占其GDP的50%。

- 根据中国建设业协会的数据,2021年中国竣工建筑中住宅占比很大,住宅建筑占竣工占地面积的67%以上。随着国家经济的成长,人们从农村迁移到大城市,增加了这些地区对住宅的需求。此外,用作投资性房地产的公寓也正在刺激需求。

- 印度计划在未来四到五年内投资 2,100 亿印度卢比(25.3 亿美元)建立和升级冷藏设施,以解决生鲜产品储存难题。现有冷藏仓库迫切需要升级机械和技术。

- 在公共和私人基础设施投资、可再生能源和商业计划的推动下,日本建筑业预计将在未来五年内温和扩张。

- 根据国土交通省统计,日本2021财年建筑建设投资超过42.6兆日圆(3,199.3亿美元)。本年度的大部分投资都集中在住宅。 2022财年建设投资将增加至43.4兆日圆(3,259.3亿美元)。

- 因此,所有上述因素都可能在预测期内增加夹层板市场的需求。

夹芯板产业概况

夹层板市场较为分散,众多参与企业争夺市场份额。市场的主要企业包括安赛乐米塔尔、ITALPANNELLI SRL、Rautaruukki Corporation、塔塔钢铁、金斯潘集团等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 扩大结构隔热板在冷藏仓库的应用

- PVDF 基铝复合板需求不断成长

- 限制因素

- 一些夹层板的防火性能

- 定向刨花板(OSB)的挥发性有机化合物(VOC)排放

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔(以金额为准的市场规模)

- 核心材料

- 聚氨酯(PUR)

- 聚异氰酸酯(PIR)

- 矿棉

- 发泡聚苯乙烯 (EPS)

- 其他核心材料

- 表皮材质

- 常用的纤维增强热塑性塑胶(CFRT)

- 玻璃纤维增强板 (FRP)

- 铝

- 钢

- 其他覆盖材料

- 应用

- 墙板

- 屋顶板

- 保温板

- 其他的

- 最终用途部分

- 住宅

- 商务用

- 工业的

- 设施基础设施

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- ArcelorMittal

- Areco

- Assan Panel AS

- Building Components Solutions LLC

- Cornerstone Building Brands

- DANA Group of Companies

- ITALPANNELLI SRL

- Kingspan Group

- Multicolor Steels (India) Pvt Ltd

- Rautaruukki Corporation

- Safal group

- Sintex

- Tata Steel

第七章 市场机会与未来趋势

- 工业和商业建筑建设增加

- 其他机会

The Sandwich Panels Market is expected to register a CAGR of greater than 6% during the forecast period.

The market was negatively impacted due to the COVID-19 pandemic. Owing to the pandemic scenario, several countries around the world went into lockdown. Construction works were halted temporarily due to supply chain disruptions, lack of funds, labor shortages, and lockdown restrictions. The sandwich panels market recovered from the pandemic and is growing significantly.

Key Highlights

- Over the short term, the rising demand for these panels from cold storage facilities is expected to drive the market. Moreover, the usage of PVDF-based aluminum composite panels is also expected to contribute to the market demand.

- However, the low fire performance of some sandwich panels is expected to restrain the market.

- Nevertheless, increasing the construction of industrial and commercial buildings is a significant growth opportunity for the sandwich panels market over the forecast period.

- Asia-Pacific region is expected to dominate the market with enormous consumption from countries such as China, Japan, and India.

Sandwich Panel Market Trends

Industrial Segment to Dominate the Market

- In modern-day construction, the use of high-performance materials is essential. High performance entails that the material is strong, lightweight, and durable and can be used in various applications. For this reliability, sandwich panels can be one of the best options for industrial buildings.

- The vast spectrum of applications includes everything from industrial building construction to insulated roof and wall panels. Sandwich panels are in high demand in industrial applications, particularly in cold storage facilities and warehouses.

- The number of cold storage operations meant to extend and ensure the shelf life of fresh agricultural produce, seafood, frozen food, photographic film, chemicals, and pharmaceutical drugs is rapidly increasing.

- Multinational companies' expansion of retail food chains led to increased demand for cold storage. These factors, in turn, are expected to augment the demand for sandwich panels across the globe.

- The global cold chain logistics market was worth USD 255.82 billion in 2021 and is expected to exceed USD 410 billion over the next eight years.

- The Asia-Pacific cold chain logistics market was valued at USD 68.97 billion in 2021, compared to USD 61.75 billion in 2020. Over the next six years, this market is expected to reach just under USD 134 billion.

- The European cold chain logistics industry was valued at more than USD 85 billion in 2021 and is predicted to grow to USD 112.8 billion by 2025. The temperature-controlled items movement along a supply chain utilizing chilled packaging solutions to protect the quality of products such as fresh agricultural commodities, seafood, frozen food, or pharmaceutical products. It is known as cold chain logistics.

- According to the Indian Pharmaceutical Association, pharmaceutical items accounted for over two-thirds of India's cold chain storage by 2021. Due to cheap manufacturing costs and government subsidies, India includes the world's third-biggest pharmaceutical business.

- All the above factors are expected to drive the industrial segment, enhancing the demand for sandwich panels during the forecast period.

Asia-Pacific Region to Dominate the Global Market

- Asia-Pacific region is expected to dominate the global market due to the high demand from countries such as China, India, and Japan.

- China is one of the major countries in Asia-Pacific with ample construction activities, with the industrial and construction sectors accounting for approximately 50% of the GDP.

- According to China Construction Industry Association, in 2021, residential buildings accounted for a significant share of finished construction in China. Buildings intended for housing accounted for over 67% of finished floor space. As the country's economy grows, people migrate from rural regions to major cities, increasing demand for residential accommodation in these locations. Furthermore, flats utilized as investment properties also drive up demand.

- In India, in the next 4-5 years, INR 21,000 crore (USD 2.53 billion) is planned to be invested in setting up or upgrading cold storage to address the stockpiling perishable commodities problem. There is an urgent need to upgrade the existing cold storage plant machinery and technology.

- Japan's construction sector is expected to expand moderately over the next five years, owing to increasing public and private infrastructure investments, renewable energy, and commercial projects.

- According to The Ministry of Land, Infrastructure, Transport, and Tourism (Japan), building construction investments in Japan were over JPY 42.6 trillion (USD 319.93 billion) in the fiscal year 2021. Most of the investments were made that year to construct residential houses. Building construction investment raised to JPY 43.4 trillion (USD 325.93 billion) in the fiscal year 2022.

- Thus, all the above factors will likely increase demand for the sandwich panels market during the forecast period.

Sandwich Panel Industry Overview

The sandwich panels market is fragmented, with numerous players sharing the market demand. Key players in the market include ArcelorMittal, ITALPANNELLI SRL, Rautaruukki Corporation, Tata Steel, and Kingspan Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Cold Storage Applications of Structural Insulated Panels

- 4.1.2 Increasing Demand for PVDF-based Aluminum Composite Panels

- 4.2 Restraints

- 4.2.1 Fire Performance of Some Sandwich Panels

- 4.2.2 Oriented Stranded Board (OSB) Emissions of Volatile Organic Compounds (VOCs)

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 Core Material

- 5.1.1 Polyurethane (PUR)

- 5.1.2 Polyisocyanurate (PIR)

- 5.1.3 Mineral Wool

- 5.1.4 Expanded Polystyrene (EPS)

- 5.1.5 Other Core Materials

- 5.2 Skin Material

- 5.2.1 Continuous Fiber Reinforced Thermoplastics (CFRT)

- 5.2.2 Fiberglass Reinforced Panel (FRP)

- 5.2.3 Aluminum

- 5.2.4 Steel

- 5.2.5 Other Skin Materials

- 5.3 Application

- 5.3.1 Wall Panels

- 5.3.2 Roof Panels

- 5.3.3 Insulated Panels

- 5.3.4 Other Applications

- 5.4 End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Institutional and Infrastructure

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 Areco

- 6.4.3 Assan Panel A.S.

- 6.4.4 Building Components Solutions LLC

- 6.4.5 Cornerstone Building Brands

- 6.4.6 DANA Group of Companies

- 6.4.7 ITALPANNELLI SRL

- 6.4.8 Kingspan Group

- 6.4.9 Multicolor Steels (India) Pvt Ltd

- 6.4.10 Rautaruukki Corporation

- 6.4.11 Safal group

- 6.4.12 Sintex

- 6.4.13 Tata Steel

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Construction of Industrial and Commercial Buildings

- 7.2 Other Opportunities

夹芯板市场:以芯材、应用、面板材料、最终用途、厚度和防火等级划分-2025-2032年全球预测

夹芯板市场:以芯材、应用、面板材料、最终用途、厚度和防火等级划分-2025-2032年全球预测 2025年全球聚异氰酸酯(PIR)隔热夹芯板市场报告2025年全球夹芯板市场报告

2025年全球聚异氰酸酯(PIR)隔热夹芯板市场报告2025年全球夹芯板市场报告 全球夹层板市场

全球夹层板市场 夹层板市场规模、份额和成长分析(按产品、应用、表皮材料、最终用途和地区)- 2025-2032 年产业预测

夹层板市场规模、份额和成长分析(按产品、应用、表皮材料、最终用途和地区)- 2025-2032 年产业预测 钢製夹层板市场规模、份额和成长分析(按产品类型、应用、最终用途和地区)- 产业预测 2025-2032

钢製夹层板市场规模、份额和成长分析(按产品类型、应用、最终用途和地区)- 产业预测 2025-2032 夹芯板的印度市场评估:各芯材类型,厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测(2018年度~2032年度)日本的夹芯板市场评估:核心木材类型·厚度·用途·建筑类型·终端用户产业·各地区的机会及预测 (2018-2032年)

夹芯板的印度市场评估:各芯材类型,厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测(2018年度~2032年度)日本的夹芯板市场评估:核心木材类型·厚度·用途·建筑类型·终端用户产业·各地区的机会及预测 (2018-2032年) 夹芯板市场 - 全球行业规模、份额、趋势、机会和预测,细分、按类型、按应用、按表皮材料、按地区和竞争,2019-2029F夹芯板市场:各核心材料类型,各厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测,2017年~2031年

夹芯板市场 - 全球行业规模、份额、趋势、机会和预测,细分、按类型、按应用、按表皮材料、按地区和竞争,2019-2029F夹芯板市场:各核心材料类型,各厚度,各用途,各建设类型,各最终用途产业,各地区,机会,预测,2017年~2031年