|

市场调查报告书

商品编码

1683202

屋顶膜:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Roofing Membranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

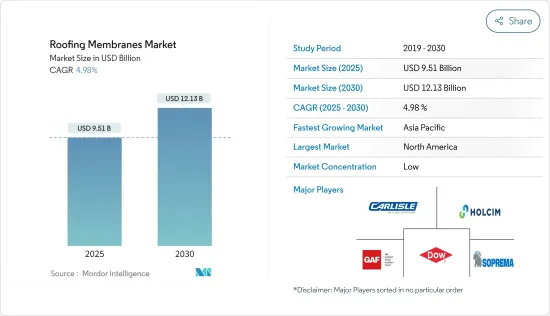

屋顶膜市场规模预计在 2025 年为 95.1 亿美元,预计到 2030 年将达到 121.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.98%。

关键亮点

- 建筑计划中轻量材料的采用越来越多以及建设活动的活性化是推动屋顶膜市场成长的关键因素。

- 然而,原材料价格的波动和严格的法规和标准可能会阻碍市场成长。

- 在预测期内,对节能屋顶膜的需求不断增长和技术进步可能为市场提供有利的成长机会。

- 由于建设活动的活性化,北美占据了屋顶膜市场的主导地位。

屋顶膜市场趋势

商业领域占据市场主导地位

- 屋顶膜广泛应用于业务用途,其需求主要受到全球蓬勃发展的商业建筑业的推动。这些薄膜在商业建筑中充当重要的防水屏障,保护建筑物免受环境因素的影响并保持屋顶系统的完整性。

- 这些薄膜的强度、耐用性和不透水性使其成为商业屋顶应用的首选。

- 这些薄膜用于工厂、火车站、机场、公司总部、购物中心、剧院、学校和医院等商业领域。

- 亚太地区在商业建筑领域占据主导地位。受政府大力发展倡议的推动,尤其是印度和中国政府,该地区近期对办公空间的需求激增。

- 根据国家统计局资料,2022年,中国全年商业营业用地开工面积约8155万平方公尺,较上年的14,105万平方公尺有所下降。此外,2023年终商品房待售占地面积为6.7295亿平方公尺,与前一年同期比较增长19%。

- 在印度,Infosys Pocharam 办公园区的建设预计将于 2023 年第三季开始,并于 2027 年第三季末完工,占地面积的办公园区扩建。

- 在中东,政府为加强商业部门发展而推出的多项倡议,如沙乌地阿拉伯2030愿景和阿布达比2030经济愿景,预计将大幅促进屋顶膜的消费。

- 预计各种饭店建筑计划将进一步推动对屋顶膜的需求。例如,随着旅游业的復苏,万豪国际集团计划在越南顶级旅游目的地(包括河内、胡志明市、岘港和富国岛)开设 20 家豪华酒店和度假村。

- 安纳塔拉酒店、度假村和水疗中心透露了在巴西开设新度假村的计划,该度假村预计将于 2025 年开业。安纳塔拉玛穆卡博度假村拥有 116 间客房、套房和泳池别墅。

- 随着商业建筑建设的增加,预计未来几年对商业屋顶膜的需求将会成长。

北美可望主导市场

- 北美占据全球市场的最大份额。在美国、加拿大和墨西哥等国家,更轻、更快捷的建筑技术的采用正在推动对屋顶膜的需求激增。

- 美国拥有世界上最大的建筑业之一。根据美国人口普查局预测,2023年美国建筑总价值将达到19.78兆美元,较2022年成长7%。截至2024年2月,获准建造的私人住宅数量达到151.8万套,较2023年同期成长2.4%。

- 随着美国多个新的商业建筑计划的建设,对屋顶膜的需求预计将进一步增加。例如,2024 年 1 月,印第安纳州政府与 Meta Platforms Inc. 合作在印第安纳州建造一个价值 8 亿美元的新资料中心园区。该计划预计于 2026 年完工,并将在 River Ridge 商业中心建造一个 70 万平方英尺的设施。

- 加拿大统计局的数据显示,建筑业总投资成长了 1.7%,从 2023 年 10 月的 19.446 兆美元增至 2023 年 11 月的 19.767 兆美元。同期住宅建筑投资成长 2.2% 至 137 亿美元,非住宅建筑投资成长 0.6% 至 60 亿美元。

- 2023年,墨西哥国际贸易署报告称,墨西哥建筑业的价值显着增长。整个产业价值将从 2022 年的 1,028.8 亿美元增至 2023 年的 1,205.8 亿美元。特别是基础设施产业,其价值预计将从 2022 年的 388.3 亿美元飙升至 2023 年的 461 亿美元左右。建筑和基础设施领域的这些上升趋势将在未来几年推动墨西哥所研究市场的需求。

- 因此,预计预测期内建筑市场的有利条件和轻量材料的日益采用将增加北美对屋顶膜的需求。

屋顶膜产业概况

屋顶膜市场比较分散。主要参与企业(不分先后顺序)包括 Carlisle SynTec Systems、Sika AG、HOLCIM、GAF Inc. 和 Saint-Gobain。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 计划中越来越多地采用轻量材料

- 建设活动增加

- 其他驱动因素

- 市场限制

- 原物料价格波动

- 严格的法规和标准

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔(以金额为准的市场规模)

- 依产品类型

- 热塑性聚烯(TPO)

- 三元乙丙橡胶(EPDM)

- 聚氯乙烯(PVC)

- 改质沥青(Modbit)

- 其他的

- 按安装类型

- 机械附着力

- 全黏性

- 安定器

- 其他安装类型

- 按应用

- 住宅

- 商业设施

- 设施

- 基础设施

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Carlisle SynTec Systems

- Dow

- GAF Inc.

- Henry Company

- HOLCIM

- IB Roof Systems

- IKO Polymeric

- Johns Manville

- Kingspan Group

- Owens Corning

- Polygomma

- Sika AG

- Siplast Inc.

- SOPREMA

第七章 市场机会与未来趋势

- 节能屋顶膜的需求不断成长

- 技术进步

- 其他机会

简介目录

Product Code: 64123

The Roofing Membranes Market size is estimated at USD 9.51 billion in 2025, and is expected to reach USD 12.13 billion by 2030, at a CAGR of 4.98% during the forecast period (2025-2030).

Key Highlights

- The rising adoption of lightweight materials in construction projects and increasing construction activities are the major factors driving the growth of the roofing membranes market.

- However, fluctuating raw material prices and stringent regulations and standards are likely to hinder the growth of the market.

- Nevertheless, the increasing demand for energy-efficient roofing membranes and advancements in technology are likely to create lucrative growth opportunities for the market during the forecast period.

- North America dominates the roofing membranes market owing to the growing construction activities in the region.

Roofing Membranes Market Trends

Commercial Segment to Dominate the Market

- Roofing membranes are widely utilized in commercial applications, and their demand is largely fueled by a surge in global commercial construction. These membranes serve as a vital waterproof barrier in commercial buildings, shielding them from environmental elements and upholding the roofing system's integrity.

- Due to their strength, durability, and impermeability to water, these membranes have become the preferred choice for commercial roofing applications.

- These membranes are used in commercial areas, such as factories, railway stations, airports, company headquarters, shopping centers, theaters, schools, and hospitals.

- Asia-Pacific is a dominant player in the commercial construction arena. The region recently witnessed a boom in office space demand, particularly in India and China, driven by proactive government development initiatives.

- As per the data from the National Bureau of Statistics of China, in 2022, the annual starting construction of commercial properties in China amounted to around 81.55 million square meters, down from 141.05 million square meters from the previous year. Furthermore, at the end of 2023, the floor space of commercial buildings for sale was 672.95 million square meters, up by 19% over the previous year.

- In India, the construction of Infosys Pocharam Office Campus, which includes the expansion of an office campus with a floor area of 761,804 square meters, was initiated in the third quarter of 2023, and it is likely to be completed by the end of Q3 2027.

- In the Middle East, several government initiatives to bolster the development of the commercial sector, such as Saudi Arabia Vision 2030 and Abu Dhabi Economic Vision 2030, are likely to substantially drive the consumption of roofing membranes.

- Various hotel construction projects are expected to further propel the demand for roofing membranes. For instance, as the tourism industry rebounds, Marriott International Inc. is set to unveil 20 luxury hotels and resorts across Vietnam's prime tourist spots, including Hanoi, Ho Chi Minh City, Da Nang, and Phu Quoc Island.

- Anantara Hotels, Resorts, and Spas revealed plans for a new resort in Brazil, slated to debut in 2025. Anantara Mamucabo will feature 116 guest rooms, suites, and pool villas.

- Given the growth in commercial construction activities, the demand for roofing membranes in commercial applications is poised for growth in the coming years.

North America Expected to Dominate the Market

- North America holds the largest share of the global market. Countries like the United States, Canada, and Mexico have seen a surge in demand for roofing membranes, driven by the adoption of lightweight and swift construction techniques.

- The United States boasts one of the world's largest construction industries. According to the United States Census Bureau, in 2023, the nation's construction value hit USD 19.78 trillion, marking a robust 7% increase from 2022. By February 2024, the number of privately owned housing units authorized by building permits reached 1,518,000, showing a 2.4% uptick from the same period in 2023.

- Several new commercial construction projects are under construction in the United States, which are likely to increase the demand for roofing membranes further. For instance, in January 2024, the government of Indiana and Meta Platforms Inc. partnered to construct a new USD 800 million data center campus in Hoosier State. The project, which is likely to be completed by the year 2026, is a 700,000-square-foot facility at the River Ridge Commerce Center.

- Statistics Canada reported a 1.7% increase in total investment in building construction, climbing from USD 19,446 billion in October 2023 to USD 19,767 billion in November 2023. In the same period, residential spending saw a 2.2% growth, hitting USD 13.7 billion, while non-residential spending rose by 0.6% to USD 6.0 billion.

- In 2023, Mexico's construction industry, as reported by the International Trade Administration, saw a notable uptick in value. The industry's overall worth climbed to USD 120.58 billion, up from USD 102.88 billion in 2022. Specifically, the infrastructure segment surged to about USD 46.10 billion in 2023, a significant rise from USD 38.83 billion in 2022. These upward trajectories in both the construction and infrastructure sectors are poised to fuel the demand for the market studied in Mexico in the coming years.

- Hence, due to such positive factors in the construction market and the growing adoption of lightweight materials, the demand for roofing membranes is projected to increase in North America during the forecast period.

Roofing Membranes Industry Overview

The roofing membrane market is fragmented in nature. The major players (not in any particular order) include Carlisle SynTec Systems, Sika AG, HOLCIM, GAF Inc., and Saint-Gobain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption of Lightweight Materials in Construction Projects

- 4.1.2 Increasing Construction Activities

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Fluctuating Raw Materials Prices

- 4.2.2 Stringent Regulations and Standards

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 By Product Type

- 5.1.1 Thermoplastic Polyolefin (TPO)

- 5.1.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.1.3 Poly Vinyl Chloride (PVC)

- 5.1.4 Modified Bitumen (Mod-Bit)

- 5.1.5 Other Product Type

- 5.2 By Installation Type

- 5.2.1 Mechanically Attached

- 5.2.2 Fully Adhered

- 5.2.3 Ballasted

- 5.2.4 Other Installation Types

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Institutional

- 5.3.4 Infrastructural

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Carlisle SynTec Systems

- 6.4.2 Dow

- 6.4.3 GAF Inc.

- 6.4.4 Henry Company

- 6.4.5 HOLCIM

- 6.4.6 IB Roof Systems

- 6.4.7 IKO Polymeric

- 6.4.8 Johns Manville

- 6.4.9 Kingspan Group

- 6.4.10 Owens Corning

- 6.4.11 Polygomma

- 6.4.12 Sika AG

- 6.4.13 Siplast Inc.

- 6.4.14 SOPREMA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Energy-efficient Roofing Membranes

- 7.2 Advancements in Technology

- 7.3 Other Opportunities

![TPO屋面膜市场:市场规模、趋势、成长分析 [2024-2030]](/sample/img/cover/42/default_cover_5.png)