|

市场调查报告书

商品编码

1683205

亚太杀线虫剂市场:市场占有率分析、产业趋势与成长预测(2025-2030 年)Asia Pacific Nematicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

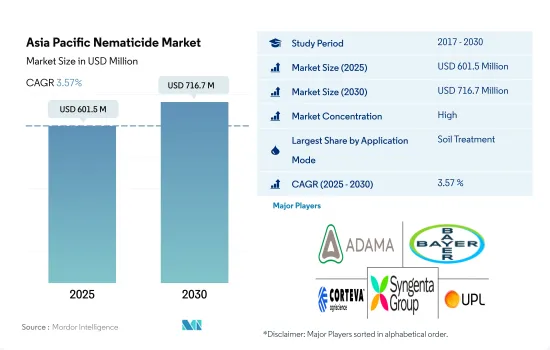

预计 2025 年亚太杀线虫剂市场规模将达到 6.015 亿美元,到 2030 年预计将达到 7.167 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.57%。

土壤施用杀线虫剂因降低接触非目标生物的风险而占据市场主导地位

- 以植物部位为食的线虫称为植物寄生线虫(PPN)。杀线虫剂可透过多种施用方法来控制这些线虫,包括叶面喷布、化学施用和土壤处理。

- 与叶面喷布等其他施用方法相比,土壤施用杀线虫剂通常对非目标生物(包括有益昆虫和传粉昆虫)的暴露风险较小。这是因为杀线虫剂主要留在目标线虫生活的土壤中。因此,到 2022 年,土壤应用将占据市场主导地位,占有 69.3% 的份额。

- 2022 年,叶面喷布占亚太杀线虫剂市场的 12.8% 。叶面喷布的主要目的是控制花序和叶片受到线虫(例如小麦线虫,也称为小麦和其他谷类的病原线虫)的感染。叶面喷布对抗线虫有效,因为它们使用了溴甲烷、草胺酸和巴拉松等活性成分。

- 2022 年,化学灌溉占亚太杀线虫市场的 8.0%。中国在化学灌溉领域占有 36.2% 的市场占有率,2022 年市场规模将达到 1,640 万美元。谷类胞囊线虫 Heterodera avenae 是中国青藏高原和黄河流域的主要线虫害虫之一,据报导可导緻小麦等主要作物10-90% 的产量损失。

- 因线虫侵染造成的农作物损失逐年增加,为农民带来了重大问题。

由于粮食需求的增加,对作物保护的需求推动了市场的成长。

- 在亚太地区,农业蓬勃发展,粮食需求不断增加,使用杀线虫剂保护作物免受线虫侵扰的情况正在增加。到 2022 年,该地区将占全球作物保护市场以金额为准的 19.8%。

- 该地区以农业为主,主要贡献者包括中国、印度、日本和澳洲。为了满足日益增长的需求并确保作物质量,农民正在采取措施保护作物免受线虫侵害,从而推动了市场成长。

- 预计 2023 年至 2029 年间,市场规模将成长 1.389 亿美元。农民越来越意识到线虫对作物产量的有害影响。线虫侵染会导致生产力下降、生长迟缓甚至作物减产。这种意识促使农民投资杀线虫剂来保护作物。

- 商业性农业的扩张推动了对杀线虫剂的需求,尤其是在印尼、泰国、中国和印度等国家。大规模农业作业容易受到线虫侵扰,因为作物集中在有限的区域内。因此,商业农民经常使用杀线虫剂来保护作物并确保更高的产量。

- 由于对农产品的需求不断增加、对线虫造成农作物损失的认识不断提高以及商业性农业的扩张,预计预测期内(2023-2029 年)亚太杀线虫剂市场以金额为准的复合年增长率将达到 3.8%。随着该地区农业的进一步发展以及应对线虫侵染的挑战,这些趋势预计将持续下去。

亚太线虫市场趋势

农民对线虫防治重要性的认识不断提高,导致杀线虫剂的使用增加。

- 日本是每公顷杀线虫剂消费量最高的国家,2022年每公顷农地平均消费量为478.7公克。然而,到2022年,日本的农业用地仅占该地区总农业用地的0.45%,即仅290万公顷。在日本,温室种植和单一栽培等集约化农业方式十分普遍。这些耕作方法虽然具有最大限度提高生产力的优势,但也使作物更容易受到线虫等土壤害虫的侵害,导致日本农民转而使用杀线虫剂来保护作物。

- 澳洲将成为每公顷杀线虫剂消费量第二高的国家,到 2022 年每公顷消耗量将达到 63.6 克。这可能是因为植物寄生线虫为澳洲种植者和草坪管理者带来巨大的隐性成本。在澳大利亚,估计多达 1,900 万公顷的耕地和休閒草坪受到寄生线虫的不利影响,每年造成 3 亿美元的损失。

- 紧随澳洲之后的是菲律宾和越南,2022 年杀线虫剂使用量分别为每公顷 46.3 克和 41.1 克。根结线虫是菲律宾面临的一个主要问题。特别是西红柿等蔬菜作物,已知会造成 20% 至 85% 的损失,具体取决于品种和地区。

- 随着线虫侵染的增加,中国、泰国、缅甸和印度是该地区杀线虫剂的其他主要消费国。然而,随着农民意识的增强和保护作物的需要,杀线虫剂的使用正在增加。

因线虫侵染造成的农作物损失逐年增加,影响了杀线虫剂的价格。

- 植物寄生线虫(PPN)是对粮食安全和植物健康最臭名昭着且最被低估的威胁之一。例如,在印度,主要植物寄生线虫造成的年度作物损失估计为 19.6% 或 2,4,210 亿印度卢比。在蔬菜栽培中,植物寄生线虫被认为是主要害虫之一。磺酸盐、Avermectin和草氨酰是亚太地区常用的杀线虫剂。

- 2022 年磺酸盐的价格为每吨 19,000 美元。磺酸盐用于防治根结线虫 (Meloidogyne spp.)、马铃薯胞囊线虫、针线虫、披针形线虫、刺线虫、矮根线虫 (Trichodorus spp. 和 Paratrichodorus spp.) 和斑点线虫等线虫。

- 已知Avermectin对几种植物寄生线虫 (Rotylenchulus reniformis)、根结线虫 (Meloidogyne incognita) 和囊肿线虫 (Heterodera schachtii)。 2022 年Avermectin的价格为每吨 12,200 美元。

- Oxamyl 是一种氨基甲酸酯杀线虫剂,有液体和颗粒形式。草氨酰是唯一具有向下迁移系统活性的杀线虫剂,因此可用于叶面杀线虫,有助于减少短体线虫。 2022 年,Oxamyl 的价格为每吨 8,700 美元。

- 因线虫侵染造成的农作物损失逐年增加,已成为农民关注的一大问题,迫使他们使用杀线虫剂来保护农作物。预计该因素将影响杀线虫剂的价格。

亚太杀线虫剂产业概览

亚太杀线虫剂市场相当集中,前五大公司占了86.26%的市占率。该市场的主要企业是 ADAMA Agricultural Solutions Ltd、Bayer AG、Corteva Agriscience、Syngenta Group 和 UPL Limited。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 有效成分价格分析

- 法律规范

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 缅甸

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 价值链与通路分析

第五章 市场区隔

- 应用模式

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

- 原产地

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 缅甸

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 其他亚太地区

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- Bayer AG

- Corteva Agriscience

- Syngenta Group

- UPL Limited

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 64382

The Asia Pacific Nematicide Market size is estimated at 601.5 million USD in 2025, and is expected to reach 716.7 million USD by 2030, growing at a CAGR of 3.57% during the forecast period (2025-2030).

Soil application of nematicides dominated the market owing to fewer risks of exposing non-target organisms

- Nematodes that feed on plant parts are called plant parasitic nematodes (PPN). Nematicides are used to control these nematodes through various application methods like foliar application, chemigation, and soil treatment.

- Compared to other application methods, such as foliar application, soil application of nematicides generally poses fewer risks of exposing non-target organisms, including beneficial insects and pollinators. This is because the nematicide remains primarily in the soil, where the target nematodes reside. Owing to this, soil application dominated the market with a share of 69.3% in 2022.

- Foliar applications accounted for 12.8% of the Asia-Pacific nematicide market in 2022. The main purpose of the foliar application is to control the infestation of inflorescence and the infestation of leaves by nematodes such as the Anguina tritici (seed gall nematode), also known as seed gall disease-causing nematodes, which are present in cereals such as wheat. Foliar application is effective against nematodes due to the use of active ingredients like methyl bromide, Oxamyl, and parathion.

- Chemigation accounted for 8.0% of the Asia-Pacific nematicide market in 2022. China dominated the chemigation segment with a market share of 36.2%, valued at USD 16.4 million in 2022. The cereal cyst nematode, Heterodera avenae, is one of the major nematode pests in the Qinghai-Tibetan Plateau and Yellow River regions of China; it is reported to cause 10-90% yield losses in major crops like wheat.

- Crop losses due to nematode infestation are increasing every year and are acting as a major concern for farmers, forcing them to use nematicides in order to protect the crops.

The need to protect the crops due to rising food demand is driving the growth of the market

- Asia-Pacific, with its large agricultural industry and increasing demand for food, has witnessed a rise in the use of nematicides to protect crops from nematode infestations. In 2022, the region accounted for 19.8% of the global crop protection market by value.

- The region has a substantial agricultural industry, with countries like China, India, Japan, and Australia being major contributors. Farmers are adopting measures to protect their crops from nematodes to meet the growing demand and ensure the quality of crops, thus driving the market's growth.

- The market is expected to grow by USD 138.9 million during 2023-2029. Farmers are becoming more aware of the detrimental effects of nematodes on crop yields. Nematode infestations can lead to reduced productivity, stunted growth, and even crop failure. This awareness has prompted farmers to invest in nematicides to protect their crops.

- The expansion of commercial farming, particularly in countries like Indonesia, Thailand, China, and India, has driven the demand for nematicides. Large-scale farming operations are more susceptible to nematode infestations due to the concentration of crops in a confined area. Therefore, commercial farmers often rely on nematicides to protect their crops and ensure higher yields.

- The Asia-Pacific nematicide market is projected to register a CAGR of 3.8% by value during the forecast period (2023-2029) due to the increasing demand for agricultural products, rising awareness about nematode-related crop losses, and expansion of commercial farming. These trends are expected to continue as the region's agricultural industry further develops and addresses the challenges posed by nematode infestations.

Asia Pacific Nematicide Market Trends

Growing awareness among farmers about the importance of nematode control is increasing the application of nematicides

- Japan is the largest consumer of nematicides per hectare, with an average consumption of 478.7 grams per hectare of agricultural land in 2022. However, Japan only accounted for 0.45% of the total agricultural land in the region, with just 2.9 million hectares in 2022. Intensive farming practices, such as greenhouse cultivation and monocropping, are prevalent in Japan. While these practices have their advantages in maximizing productivity, they also increase the vulnerability of crops to soil-borne pests like nematodes, leading the farmers in Japan to rely on nematicides to safeguard their crops.

- Australia is the second-highest consumer of nematicides per hectare, with a consumption of 63.6 grams per hectare in 2022. This could be attributed to the huge hidden cost posed by plant parasitic nematodes to Australian producers and turf managers. It has been estimated that up to 19 million hectares of cultivated land and amenity turf are negatively impacted by parasitic nematodes in Australia, resulting in annual losses of USD 300 million.

- Australia is closely followed by the Philippines and Vietnam, with nematicide consumptions of 46.3 and 41.1 grams per hectare, respectively, in 2022. Root-knot nematode is a major problem in the Philippines. It is known to cause losses between 20% and 85%, especially in vegetable crops like tomatoes, based on the cultivar and region grown.

- China, Thailand, Myanmar, and India are other countries in the region that consume significant amounts of nematicides, owing to the increasing incidences of nematode infestation, which are often neglected by the farmers because of their hidden nature. However, the usage of nematicides is increasing with growing awareness among farmers and the need to protect the crops.

Crop losses due to nematode infestation are increasing every year, influencing the prices of nematicides

- Plant parasitic nematodes (PPNs) are among the most notorious and underrated threats to food security and plant health. For instance, in India, the annual crop losses due to major plant parasitic nematodes are estimated to be 19.6%, valued at INR 242.1 billion. In vegetable cultivation, plant parasitic nematodes are considered among the major pests. Fluensulfone, Abamectin, and Oxamyl are commonly used nematicides in Asia-Pacific.

- Fluensulfone was valued at USD 19.0 thousand per metric ton in 2022. It can be used to suppress nematodes, including root-knot nematodes (Meloidogyne spp.), potato cyst nematodes, needle nematodes, lance nematodes, sting nematodes, stubby root nematodes (Trichodorus and Paratrichodorus spp.), and lesion nematodes.

- Abamectin is known to have nematicidal activity against some plant parasitic nematodes, including the root lesion nematode (Pratylenchus penetrans), the reniform nematode (Rotylenchulus reniformis), the root-knot nematode (Meloidogyne incognita), and the cyst nematode (Heterodera schachtii). Abamectin was valued at USD 12.2 thousand per metric ton in 2022.

- Oxamyl is a carbamate nematicide that is manufactured in liquid and granular forms. Oxamyl is the only nematicide with downward-moving systemic activity; thus, it has foliar nematicidal applications that help to reduce Pratylenchus nematodes. Oxamyl was valued at USD 8.7 thousand per metric ton in 2022.

- Crop losses due to nematode infestation are increasing every year and are acting as a major concern for farmers, forcing them to use nematicides in order to protect the crops. This factor is expected to influence the prices of nematicides.

Asia Pacific Nematicide Industry Overview

The Asia Pacific Nematicide Market is fairly consolidated, with the top five companies occupying 86.26%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Syngenta Group

- 6.4.6 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

杀虫剂市场:按类型、剂型、作物和应用划分-2026-2032年全球市场预测

杀虫剂市场:按类型、剂型、作物和应用划分-2026-2032年全球市场预测 全球马钱苷市场规模、份额、趋势和成长分析报告(2026-2034年)

全球马钱苷市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球杀线虫剂市场报告

2026年全球杀线虫剂市场报告 杀线虫剂市场规模、份额和成长分析(按类型、作物、配方、线虫类型、应用方法和地区划分)—产业预测(2026-2033 年)

杀线虫剂市场规模、份额和成长分析(按类型、作物、配方、线虫类型、应用方法和地区划分)—产业预测(2026-2033 年) 杀线虫剂市场-全球产业规模、份额、趋势、机会和预测,依产品类型、剂型、应用方式、作物类型、地区和竞争格局划分,2020-2030年预测

杀线虫剂市场-全球产业规模、份额、趋势、机会和预测,依产品类型、剂型、应用方式、作物类型、地区和竞争格局划分,2020-2030年预测 2021-2031年全球及区域份额、趋势及成长机会分析杀线虫剂市场规模及预测报告涵盖范围:依线虫类型、杀线虫剂类型、应用方式、耕作类型及作物类型划分

2021-2031年全球及区域份额、趋势及成长机会分析杀线虫剂市场规模及预测报告涵盖范围:依线虫类型、杀线虫剂类型、应用方式、耕作类型及作物类型划分 全球杀线虫剂市场(按类型、线虫种类、施用方法、剂型、作物类型和地区划分)- 预测至2030年

全球杀线虫剂市场(按类型、线虫种类、施用方法、剂型、作物类型和地区划分)- 预测至2030年 杀线虫剂市场报告(按化学类型、线虫类型、剂型、应用和地区)2025-2033

杀线虫剂市场报告(按化学类型、线虫类型、剂型、应用和地区)2025-2033 北美杀线虫剂市场:市场占有率分析、产业趋势与成长预测(2025-2030 年)杀线虫剂:市场占有率分析、产业趋势与成长预测(2025-2030)

北美杀线虫剂市场:市场占有率分析、产业趋势与成长预测(2025-2030 年)杀线虫剂:市场占有率分析、产业趋势与成长预测(2025-2030)

▼