|

市场调查报告书

商品编码

1683231

电感器磁芯和磁珠市场:市场占有率分析、行业趋势和成长预测(2025-2030 年)Inductors, Cores and Beads - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

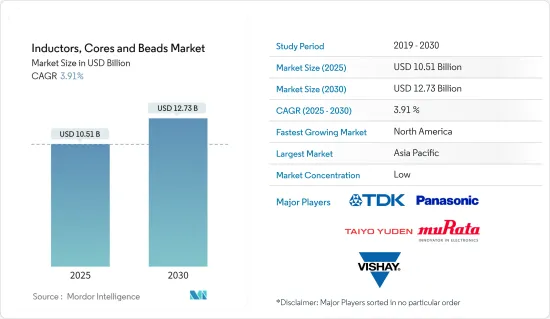

电感磁珠市场规模预计在 2025 年为 105.1 亿美元,预计到 2030 年将达到 127.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.91%。

新型SMD产品开发愈加活跃,重点关注智慧型手机、模组和物联网设备的小型晶片以及汽车应用的高可靠性晶片。

关键亮点

- 提高功率密度和效率对大多数电感器设计人员来说都是一个挑战。人们持续需要紧凑、高效能的电源解决方案来满足日益严苛的应用要求。

- 在全球范围内,智慧型手机、平板电脑、掌上游戏机、笔记型电脑和机上盒等家用电子电器的需求不断增长,是推动各种电感器、磁芯和磁珠需求的主要因素。

- 此外,工业、航太和国防以及医疗领域等对高可靠性要求的应用的需求也不断增加。

电感磁珠市场趋势

家用电子电器占据很大市场占有率

- 约15%的智慧型手机由陶瓷和玻璃製成,其电路基板使用电感器、保险丝和电阻器等被动核心进行温度控管。

- 物联网和5G网路可望提高设备与网路、物联网、自动驾驶、M2M之间资讯通讯的整体速度和效率。

- 大部分消费性电子产品都是高功率设备,功率从几百瓦到几千瓦不等。所使用的磁性元件的数量取决于充电桩的功率。一个充电桩平均需要20个磁性元件,其中电感器占大多数。

- 挑战依然是晶片面积的大小。例如,英特尔表示,其多核心处理器中用于电源管理的 DC-DC 转换器中的晶片电感器占用了可用晶片总面积的约四分之一,因此成本很高。

北美占据主要市场占有率

- 在美国,电感器在汽车电子设备的应用正在扩大,智慧电网技术的采用也正在增加。由于电感器用途广泛,已成为许多电子系统中的关键元件。由于应用范围广泛,电感器在北美多个行业中得到了越来越广泛的应用。

- 2016 年,美国公用事业公司在发电、输电和配电基础设施方面投资约 1,440 亿美元。据国际能源总署称,2018年美国智慧电网基础设施投资达126亿美元。

- 电感磁珠因其低功耗和多功能适应性,在最新的自我调整LED 大灯中得到应用,这些大灯正在取代传统的滷素和 HID 大灯、ADAS、汽车点火系统等。

- 2018年,美国汽车产量为113.1亿辆,加拿大汽车产量为202万辆。

- 美国提高价值2000亿美元的中国产品进口关税,电子元件产业受到进一步影响。

电感磁珠产业概况

电感磁珠市场机会带来了激烈的竞争。有许多製造商在争夺更大的市场占有率。市场正在见证以小型化和改变磁芯形态来实现更高电感的形式出现的技术创新。

- 2019 年 9 月 - TDK 推出专为恶劣汽车环境设计的金属芯功率电感器。

- 2019 年 6 月 - TDK 推出专为行动装置设计而客製化的薄膜功率电感器,与传统产品相比,支援高 4% 的电流和低 12% 的电阻。

- 2019 年 6 月 - Kemet 公司推出了一系列新型 SMD 金属复合功率电感器,适用于笔记型电脑、平板电脑、伺服器和高清电视等各种商业和消费应用中的 DC-DC 转换器中的现代电源应用。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 引入市场驱动因素与限制因素

- 市场驱动因素

- 市场限制

第五章 市场区隔

- 按电感器类型

- 功率电感

- 迭层片式电感

- 射频电感器

- 其他电感类型

- 按核心材料

- 空气芯

- 铁氧体磁芯

- 陶瓷芯

- 其他核心类型

- 透过晶片磁珠

- 多层珠

- 铁氧体磁珠

- EMI 磁珠

- 按最终用户产业

- 车

- 计算

- 通讯设备

- 消费性电子产品

- 其他的

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- TDK Corporation

- Vishay International Inc.

- Panasonic Corporation

- Murata Manufacturing Co. Ltd.

- Taiyo Yuden Co. Ltd.

- Kemet Corporation

- AVX Corporation

- Texas Instruments

- TT Electronics Plc

- Hefei MyCoil Technology Co., Ltd.

第七章 投资机会

第八章 市场机会与未来趋势

The Inductors, Cores and Beads Market size is estimated at USD 10.51 billion in 2025, and is expected to reach USD 12.73 billion by 2030, at a CAGR of 3.91% during the forecast period (2025-2030).

New product development of SMDs are gaining momentum, centering on small chips for smartphones, modules, and IoT terminals, and high-reliability chips for automotive application.

Key Highlights

- The increasing power supply density and efficiency is a challenge for most of the inductor designers. There is a continuous need for reduced size and high-performance power solutions to meet increasingly stringent application requirements.

- Globally, the growing demand for consumer electronics, such as smartphones, tablets, portable gaming consoles, laptops, set-top boxes, among others, is the major factor driving the demand for various inductors, core and beads.

- The market is also witnessing a boost in demand from applications, which require high reliability, in the industrial, aerospace and defense, and medical sectors.

Inductors Cores & Beads Market Trends

Consumer Electronic to Witness a Significant Market Share

- Around 15 percent of a smartphone is made from ceramics and glass that is from electronic applications with circuit boards for thermal management employs cores of passive components like inductors, fuses or resistors.

- The Internet of Things and 5G network is expected to boost the overall speed and efficiency of communicating information between devices and networks, IoT, autonomous driving and M2M performances.

- Most of consumer electronic products are high-power devices, and the power ranges from hundred to several kilowatts.The amount of magnetic components employed depends on the power of the charging pile. On an average, 20 magnetic components are required in a charging pile, of which the inductor is used in a larger amount.

- The challenge remains the large chip area utilisation. For instance, Intel stated that the on-chip inductors used in their DC-DC converters for power management in multi-core processors occupy approximately a quarter of the total available chip area, which made them costly.

North America to Hold a Significant Market Share

- The United States witnesses a growing use of inductors in automotive electronics and increasing adoption of smart grid technologies. Due to their various applications, inductors are one of the primary components of many electronic systems. Because of the extensive usage, more inductors are being applied in several industries across North America.

- U.S. utilities invested approximately USD 144 billion in electricity generation, transmission, and distribution infrastructure in 2016. According to IEA, U.S. investments in smart grids infrastructure stood at USD 12.6 billion in 2018.

- The application of inductors, core and beads find their applications in modern adaptive LED headlights because of their low power consumption and multifunctional adaptability, these are replacing conventional halogen and HID headlights, ADAS, automotive ignition systems, among others.

- The Unites States automotive production in 2018 stands at 11.31 billion cars and commercial vehicles and Canada's automotive production at 2.02 miliion cars and commericial vehicles, as per OICA.

- The region expects a gradual ease in China-US trade spats after May of 2019, when the United States raised import tariffs on USD 200 billion of Chinese goods, which further affected the electronic component industry.

Inductors Cores & Beads Industry Overview

The inductor, cores and beadsmarket's opportunities have resulted in intense competition. There are a significant number of manufacturers vying for the increasing market share. The market witnesses increased innovation in the form of reduced size and varying the form of cores to achieve higher inductance.

- September 2019 - TDK introduced metal-core power inductors tomeet the tough conditions forharsh automotive environments, these conductors have a wide operating temperature range from -55 °C up to +155 °C.

- June 2019 -TDK launched a Thin-Film Power Inductor specifically for Mobile Device Design tohandle 4% higher currents and 12% lower resistance than conventional products.

- June 2019 - Kemet Corporation launched new range of SMD metal composite power inductors to suit modern power applications inDC-DC converters that are utilized in a variety of commercial and consumer applications including notebook computers, tablets, servers and HDTVs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Introduction to Market Drivers and Restraints

- 4.4 Market Drivers

- 4.5 Market Restraints

5 MARKET SEGMENTATION

- 5.1 By Inductor Type

- 5.1.1 Power Inductors

- 5.1.2 MultiLayer Chip Inductors

- 5.1.3 RF Inductors

- 5.1.4 Other Inductor Types

- 5.2 By Core Material

- 5.2.1 Air Core

- 5.2.2 Ferrite Core

- 5.2.3 Ceramic Core

- 5.2.4 Other Core Types

- 5.3 By Chip Beads

- 5.3.1 MultiLayered Beads

- 5.3.2 Ferrite Beads

- 5.3.3 EMI Beads

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Computing

- 5.4.3 Communications

- 5.4.4 Consumer Electronics

- 5.4.5 Other End-User Industries

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 TDK Corporation

- 6.1.2 Vishay International Inc.

- 6.1.3 Panasonic Corporation

- 6.1.4 Murata Manufacturing Co. Ltd.

- 6.1.5 Taiyo Yuden Co. Ltd.

- 6.1.6 Kemet Corporation

- 6.1.7 AVX Corporation

- 6.1.8 Texas Instruments

- 6.1.9 TT Electronics Plc

- 6.1.10 Hefei MyCoil Technology Co., Ltd.