|

市场调查报告书

商品编码

1683468

美国汽车防撞系统:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)United States Automotive Collision Avoidance Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

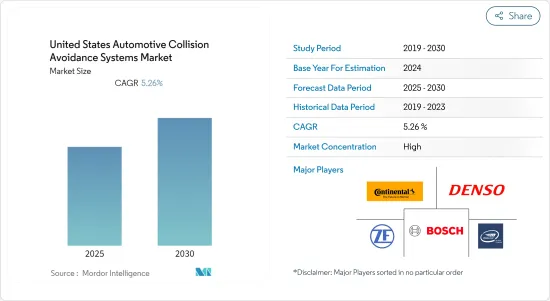

预计预测期内美国汽车防撞系统市场复合年增长率将达到 5.26%。

主要亮点

- 新冠肺炎疫情对市场的影响较小。整个汽车产业都受到了疫情的严重影响。不过,开发防撞系统所涉及的技术并未受到疫情的太大影响,因为它可以远端建置。然而,由于世界各地严格的社交距离规范和封锁规定,硬体的设置和安装受到了阻碍。

- 疫情过后,由于个人出行需求预计将增加,且相较于公共和一般交通方式,个人出行的偏好将有所增加,因此汽车销售量预计将上升。预计这将间接增加对防撞系统的需求并促进产业成长。

- 市场上许多科技公司已经合作解决 ADAS(高阶驾驶辅助系统)开发的复杂性。例如,2020 年 8 月,Veoneer Inc. 和 Qualcomm Technologies Inc. 宣布将合作提供可扩展的高级驾驶辅助系统 (ADAS) 以及协作和自动驾驶 (AD) 解决方案。

- 特斯拉所有车型都已配备自动紧急煞车 (AEB) 标准。包括戴姆勒、宝马和福特在内的其他汽车製造商预计也将在其所有即将推出的车型中配备 AEB。特斯拉汽车配备了实现完全自动驾驶功能所需的所有硬体。

- 2020年10月,总部位于亚利桑那州凤凰城的自动驾驶汽车公司Waymo宣布其自动驾驶汽车可用于计程车服务。由于亚利桑那州的相对容忍度以及汽车对详细3D地图的需求,该服务仅在有限的区域提供。由于新冠疫情,该服务已暂停,但该公司计划在未来几年内将服务范围扩大到更多地区。

美国汽车防撞系统市场趋势

市场领先的警告功能

- 在美国,具有警告功能的防撞系统自2018年以来一直名列最受欢迎的系统之列,预计未来这一趋势仍将持续下去。警告功能类型紧接在自适应功能类型之后。

- 当驾驶者无法看清车辆侧面时,盲点警报系统会侦测并警告驾驶。该系统将因变换车道而导致受伤的事故减少了 23%。

- 具有自动紧急煞车系统 (AEBS) 的先进前方碰撞警报系统可以自动阻止车辆发生正面碰撞,或至少在高速行驶时减少碰撞的力量。带有自动紧急煞车的前方碰撞警报可将造成人员受伤的前后碰撞事故减少 20%。

- 随着高级驾驶辅助系统 (ADAS) 领域的进步和技术进步,主动式车距维持定速系统( ACC) 预计将在未来几年变得更加普及,因为它将成为自动驾驶汽车技术的关键和必要功能。

- ACC 旨在帮助车辆保持安全的跟车距离并保持在速度限制之内。系统会自动调整车辆的速度,无需驾驶进行任何调整。虽然一些高檔汽车OEM将主动式车距维持定速系统控製作为其最新车型的基本和必需功能,但其他OEM则将该功能作为额外选配功能提供,但需支付额外费用。

加州在美国市场各州中排名第一

- 加州作为一个独立的州,在市场占有率上处于领先地位。加州最畅销的汽车是本田思域、本田雅阁、丰田Camry、特斯拉 Model 3 和福特 F 系列。这些模型配备了防撞系统,作为要求或选择。

- 该州也是高檔汽车市场的所在地,预计将增加对汽车防撞系统的需求。 2012 年 9 月,加州成为第三个允许自动驾驶汽车在州高速公路上行驶的州。针对此,许多公司正在投资开发自动驾驶的安全技术。

- 德克萨斯州是全球两大目标商标产品製造商(OEM)——通用汽车和丰田的所在地。德克萨斯州是允许自动驾驶汽车进入的九个州之一。该州也是大陆汽车等防撞系统製造商的所在地,这是预测期内推动市场成长的主要因素。

- 佛罗里达州的豪华车销售量位居美国第二,该州的大部分豪华车都配备了先进的防撞系统,预计将促进市场成长。该州通过了一项法律,允许自动驾驶汽车在州高速公路上行驶,并向自动驾驶汽车製造商开放了市场。

- 2017 年,纽约州将自动驾驶汽车测试合法化,但只有奥迪和凯迪拉克两家公司测试了自动驾驶汽车。奥迪在奥尔巴尼周围行驶了约 170 英里,而凯迪拉克则在从纽约市到新泽西州的路上进行了试驾。它是该州销量第三高的豪华车。梅赛德斯·奔驰 S 级轿车是纽约州最畅销的汽车。该车具有车道偏离警示系统、自动紧急煞车系统、主动式车身控制系统、手动方向盘感知器和夜视功能。

- 2018 年,俄亥俄州将自动驾驶汽车合法化。为了吸引 AV 研究人员、开发商和製造商,该州成立了 DriveOhio,这是州运输部的一个新部门,允许任何公司进行测试。

- 2020 年 12 月,为回应政府日益增长的关注和支持,Waymo 宣布将在俄亥俄州建立一个测试中心,以测试其下一代自动驾驶汽车和卡车。在政府倡议和企业建立测试设施的推动下,预计该州在预测期内将实现高成长率。

美国汽车防撞系统产业概况

美国汽车防撞系统市场由罗伯特·博世、大陆集团、采埃孚股份公司和Mobileye等大公司主导。这些公司总合占据了该国大部分的市场占有率。

2020 年 8 月,Verizon 宣布与 HERE Technologies 合作,利用高画质地图开发车辆和行人安全技术。透过建构配备高定位精度技术的车对网路 (V2N) 系统,该系统可以准确识别任何障碍物并透过 Verizon 开发的通讯频道传递资料。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 市场领先的警告功能

- 其他的

- 市场限制

- 晶片短缺扰乱供应链

- 其他的

- 波特五力分析

- 新进入者的威胁

- 购买者和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 函数类型

- 自适应

- 自动化

- 监控

- 警告

- 技术类型

- 雷达

- LiDAR

- 相机

- 超音波

- 车辆类型

- 搭乘用车

- 商用车

- 状态

- 加州

- 德克萨斯州

- 佛罗里达

- 纽约

- 俄亥俄州

- 美国其他地区

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- Continental AG

- Delphi Automotive(APTIV PLC)

- Denso Corporation

- Infineon Technologies

- Panasonic Corporation

- Robert Bosch GmbH

- ZF Group

- Autoliv Inc.

- Mobileye

- WABCO Vehicle Control Services

- Magna International

第七章 市场机会与未来趋势

The United States Automotive Collision Avoidance Systems Market is expected to register a CAGR of 5.26% during the forecast period.

Key Highlights

- COVID-19 had a mild impact on the market. The automotive industry as a whole was severely impacted by the pandemic. However, the technology involved in developing the collision avoidance system could be built remotely, so it was not affected by the pandemic as much. The hardware setup and installation that needed to be performed on the cars, however, were hindered due to the stringent social distancing norms and lockdown restrictions all over the world.

- Post-pandemic, with an expected increase in demand and preference for individual mobility over public or common transport, vehicle sales were expected to increase. This was indirectly projected to increase the demand for collision avoidance systems and help in the growth of the industry.

- Many technology companies in the market are teaming up to solve the complexities of developing advanced driver-assistance systems (ADAS). For instance, in August 2020, Veoneer Inc. and Qualcomm Technologies Inc. announced that they were collaborating to deliver scalable advanced driver assistance systems (ADAS) and collaborative and autonomous driving (AD) solutions.

- Tesla is already offering all its cars with automatic emergency breaking (AEB) features as standard. Other automakers like Daimler, BMW, and Ford are expected to provide AEB in all their upcoming models. Tesla cars are equipped with all the necessary hardware to achieve full autonomy.

- In October 2020, the self-driving car company Waymo in Phoenix, Arizona, announced that its autonomous vehicles are available for taxi service. The service is only available in a limited area because of the relatively permissive Arizona and cars' requirement for a detailed three-dimensional map. The service was shut down due to the COVID-19 pandemic, but now the company aims to increase availability in the coming years.

US Automotive Collision Avoidance Systems Market Trends

Warning Function Dominating the Market

- The warning function type system of the collision avoidance system has been consistently on top of usage in the United States since 2018, and it is expected to continue the same trend. The warning function type system is closely followed by the adaptive function type system.

- The blind-spot warning system detects and warns the drivers if they are unable to see alongside their vehicles. It has provided an impressive 23% decrease in lane-change collisions with injuries.

- Advanced forward-collision warning systems with automatic emergency braking systems (AEBS) can automatically stop a vehicle from forward collision or at least reduce collision impact force at high speeds. Forward collision warning with auto-emergency braking has provided a 20% reduction in front-to-rear crashes with injuries.

- With the advancement in technology and technological advancements in the advanced driver-assistance system (ADAS) segment, adaptive cruise control is expected to become more popular, as adaptive cruise control (ACC) will be an important and mandatory feature for autonomous vehicle technology in the future.

- The ACC is designed to help vehicles maintain a safe following distance and stay within the speed limit. This system adjusts a car's speed automatically, so drivers do not have to. Several premium car original equipment manufacturers (OEMs) include adaptive cruise control features in their latest models as a basic and mandatory feature, while other OEMs offer this feature as an optional feature at an additional cost.

California Ranks First Among Other States in the US Market

- California is leading the market share as an individual state. Top-selling vehicles in California are Honda Civic, Honda Accord, Toyota Camry, Tesla Model 3, and Ford F Series. These models are either equipped with mandatory or optional collision avoidance systems.

- The state is also home to the luxury car market, which is expected to increase the demand for automotive collision avoidance systems. In September 2012, California became the third state to allow self-driving cars to operate on state roads. This has led to many companies investing in the development of safety technologies for autonomous driving.

- Texas is home to one of the largest original equipment manufacturers (OEMs) in the world, General Motors and Toyota. Texas is one of the nine states to allow autonomous driving. The state is also home to collision avoidance systems manufacturers like Continental AG and others, which is a major factor contributing to the market growth during the forecast period.

- Florida ranks second in the sale of luxury cars across the United States, which is expected to help the market growth as most of the luxury cars come with advanced collision avoidance systems. The state has passed a law that allows autonomous cars to operate on state roads, thus opening the market for autonomous vehicle manufacturers.

- In 2017, New York legalized testing autonomous vehicles, but only two companies, namely Audi and Cadillac, tested their AVs. Audi drove about 170 miles around Albany, while Cadillac tested its cars on a drive from New York City to New Jersey. The state recorded the third-highest sales of luxury cars. Mercedes-Benz S class was the most sold car in the New York state. This car features a lane assist, an automated emergency braking system, an active body control system, a hands-on steering wheel sensor, and night vision.

- In 2018, Ohio legalized autonomous vehicles. To attract AV researchers, developers, and manufacturers, the government created DriveOhio, a new division of the state Department of Transportation, which allows any company to test.

- In December 2020, with the increasing government emphasis and support, Waymo announced that it would be building a testing center in Ohio to test its next-generation autonomous cars and trucks. With government initiatives and companies setting up their testing facilities, the state is expected to witness a high growth rate during the forecasted period.

US Automotive Collision Avoidance Systems Industry Overview

The US automotive collision avoidance systems market is dominated by major players like Robert Bosch, Continental, ZF Friedrichshafen AG, and Mobileye. These companies combined account for the majority of the market share in the country.

In August 2020, Verizon announced its partnership with HERE Technologies to develop technologies for vehicle and pedestrian safety using high-definition mapping. By creating a vehicle-to-network (V2N) equipped with technology for high location accuracy, the system can precisely identify any obstacles and relay the data through the communication channel developed by Verizon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Warning Function Dominating the Market

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Disturbances in Supply Chain due to Chip Shortage

- 4.2.2 Others

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Function Type

- 5.1.1 Adaptive

- 5.1.2 Automated

- 5.1.3 Monitoring

- 5.1.4 Warning

- 5.2 Technology Type

- 5.2.1 Radar

- 5.2.2 LiDAR

- 5.2.3 Camera

- 5.2.4 Ultrasonic

- 5.3 Vehicle type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 State

- 5.4.1 California

- 5.4.2 Texas

- 5.4.3 Florida

- 5.4.4 New York

- 5.4.5 Ohio

- 5.4.6 Rest of the United States

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Continental AG

- 6.2.2 Delphi Automotive (APTIV PLC)

- 6.2.3 Denso Corporation

- 6.2.4 Infineon Technologies

- 6.2.5 Panasonic Corporation

- 6.2.6 Robert Bosch GmbH

- 6.2.7 ZF Group

- 6.2.8 Autoliv Inc.

- 6.2.9 Mobileye

- 6.2.10 WABCO Vehicle Control Services

- 6.2.11 Magna International

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

正面防撞雷达市场:依频率、雷达类型、应用、安装方式、车辆类型划分,全球预测(2026-2032年)交通防撞系统市场:按系统类型、最终用户、平台和安装类型分類的全球预测,2026-2032年交通预警和防碰撞系统市场:按平台、系统类型、安装类型和最终用户划分,全球预测,2026-2032年

正面防撞雷达市场:依频率、雷达类型、应用、安装方式、车辆类型划分,全球预测(2026-2032年)交通防撞系统市场:按系统类型、最终用户、平台和安装类型分類的全球预测,2026-2032年交通预警和防碰撞系统市场:按平台、系统类型、安装类型和最终用户划分,全球预测,2026-2032年 2026年全球防碰撞系统市场报告

2026年全球防碰撞系统市场报告 汽车事故维修估价软体市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车事故维修估价软体市场机会、成长要素、产业趋势分析及2026年至2035年预测 列车防撞系统市场规模、份额和成长分析(按系统类型、技术、推进方式、应用和地区划分)—产业预测(2026-2033 年)汽车防碰撞雷达市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

列车防撞系统市场规模、份额和成长分析(按系统类型、技术、推进方式、应用和地区划分)—产业预测(2026-2033 年)汽车防碰撞雷达市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球列车防撞系统市场全球汽车碰撞评估软体市场

全球列车防撞系统市场全球汽车碰撞评估软体市场 全球列车防撞系统市场:预测至 2032 年 - 按类型、解决方案类型、列车类型、推进类型、组件、应用、最终用户和地区进行分析

全球列车防撞系统市场:预测至 2032 年 - 按类型、解决方案类型、列车类型、推进类型、组件、应用、最终用户和地区进行分析