|

市场调查报告书

商品编码

1683756

德国建筑涂料:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Germany Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

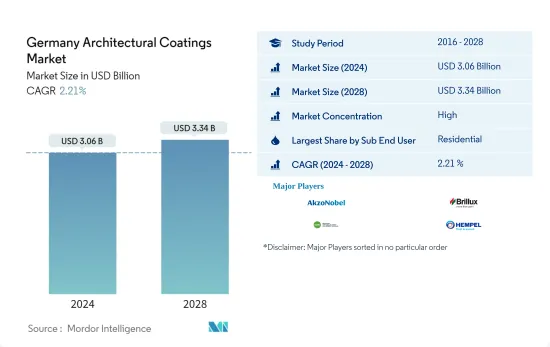

预计 2024 年德国建筑涂料市场规模为 30.6 亿美元,到 2028 年将达到 33.4 亿美元,预测期内(2024-2028 年)的复合年增长率为 2.21%。

主要亮点

- 按最终用户分類的最大细分市场:住宅:研究期间,住宅建设产业非油漆建筑材料的高速成长影响了住宅油漆消费。

- 按技术分類的最大细分市场:水基:绿色和永续材料在国内的日益普及以及政府法规的推出支持了水基技术的发展。

- 按树脂分類的最大细分市场:丙烯酸:在德国,VOC 法规和绿色建筑运动导致水性涂料广泛采用,从而推动了丙烯酸树脂基涂料的成长。

德国建筑涂料市场的趋势

按终端用户细分,住宅是最大的细分市场

- 2016-2019年期间,德国建筑涂料总消费量的复合年增长率为-1.14%。在研究期间,消费量的下降是由于建筑材料(如塑胶片材和预製材料)消费量油漆较少的趋势日益明显。

- 2016年至2019年,德国商用涂料的份额约为26%波动,但由于住宅涂料消费量的异常增长和商用涂料消费量的下降,2020年将下降23%。

- 儘管 2020 年商业建筑和装修涂料消费量有所下降,但整体涂料消费量却出现大幅增长,尤其是在该国住宅领域,因为住宅因 COVID-19 疫情而呆在家里,导致 DIY 涂料消费量大幅增加。

德国建筑涂料产业概况

德国建筑涂料市场适度整合,前五大公司占55.55%的市场。该市场的主要企业是:AkzoNobel NV、Brillux GmbH & Co. KG、DAW SE、Hempel A/S 和 PPG Industries, Inc.(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第 2 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第三章 产业主要趋势

- 占地面积趋势

- 法律规范

- 价值链与通路分析

第 4 章 市场细分

- 次级终端用户

- 商业的

- 住宅

- 科技

- 溶剂型

- 水性

- 树脂

- 丙烯酸纤维

- 醇酸

- 环氧树脂

- 聚酯纤维

- 聚氨酯

- 其他树脂类型

第五章 竞争格局

- 重大策略倡议

- 市场占有率分析

- 业务状况

- 公司简介

- AkzoNobel NV

- Beckers Group

- Brillux GmbH & Co. KG

- DAW SE

- Hempel A/S

- Jotun

- Meffert AG Farbwerke

- MIPA SE

- PPG Industries, Inc.

- Remmers GmbH

第六章 执行长的关键策略问题

第七章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 93072

The Germany Architectural Coatings Market size is estimated at USD 3.06 billion in 2024, and is expected to reach USD 3.34 billion by 2028, growing at a CAGR of 2.21% during the forecast period (2024-2028).

Key Highlights

- Largest Segment by End-user - Residential : The high growth of the non-paintable building materials in the residential construction industry affected the residential paint consumption during the study period.

- Largest Segment by Technology - Waterborne : The increasing popularity of green and sustainable materials in the country is supporting the growth of waterborne technology, along with government regulations.

- Largest Segment by Resin - Acrylic : The high adoption of waterborne coatings in Germany due to VOC regulations and the green building movement is driving the growth of acrylic resin-based coatings.

Germany Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

- Germany's total architectural coatings consumption recorded a CAGR of -1.14% during the 2016-2019 period. During the study period, this contraction in consumption was due to the growing trend of building materials that consume fewer paints, such as plastic sheets and pre-built materials.

- The commercial coatings' share fluctuated by around 26% in Germany during the 2016-2019 period while declining by 23% in 2020 due to abnormal growth in residential paint consumption and declining commercial paint consumption.

- In 2020, even though commercial construction and remodeling paint consumption declined, total paint consumption showed a huge spike due to a large increase in the consumption of the DIY paints, especially in the country's residential sector, as people stayed home due to the COVID-19 pandemic.

Germany Architectural Coatings Industry Overview

The Germany Architectural Coatings Market is moderately consolidated, with the top five companies occupying 55.55%. The major players in this market are AkzoNobel N.V., Brillux GmbH & Co. KG, DAW SE, Hempel A/S and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

- 4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

- 4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

- 4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles

- 5.4.1 AkzoNobel N.V.

- 5.4.2 Beckers Group

- 5.4.3 Brillux GmbH & Co. KG

- 5.4.4 DAW SE

- 5.4.5 Hempel A/S

- 5.4.6 Jotun

- 5.4.7 Meffert AG Farbwerke

- 5.4.8 MIPA SE

- 5.4.9 PPG Industries, Inc.

- 5.4.10 Remmers GmbH

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms