|

市场调查报告书

商品编码

1683763

西班牙建筑涂料:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Spain Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

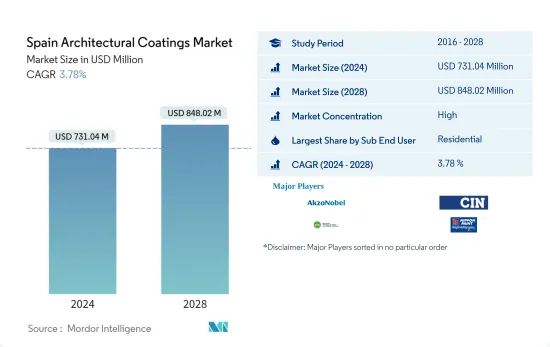

西班牙建筑涂料市场规模预计在 2024 年为 7.3104 亿美元,预计到 2028 年将达到 8.4802 亿美元,预测期内(2024-2028 年)的复合年增长率为 3.78%。

主要亮点

- 按最终用户分類的最大细分市场:住宅:住宅建筑业的稳定成长加上商业产业的成长放缓,推动了住宅产业的消费。

- 按技术分類的最大细分市场:水性涂料:建筑涂料製造商越来越多地采用VOC法规以及生态标籤的销售,正在帮助水性涂料扩大市场占有率。

- 按树脂分類的最大细分市场:丙烯酸:丙烯酸是主要的树脂类型,因为它具有技术优势、建筑领域的低 VOC排放以及偏好用于建筑外墙涂层。

西班牙建筑涂料市场的趋势

按终端用户细分,住宅是最大的细分市场。

- 西班牙建筑涂料消费量在 2017 年达到顶峰,与前一年同期比较增 7.3%,原因是自 2013 年以来经历了长期復苏,且 2017 年修復工程增加。然而,由于 2018 年和 2019 年修復许可证减少,占建筑涂料大部分的修补漆部分出现下滑。

- 2020年,新冠疫情蔓延导致住宅和商业新建建筑数量下降,导致建筑涂料消费量成长乏力。然而,2020 年新建房屋数量的下降被住宅领域 DIY(自己木工)部分的增长所抵消。

- 2021年,随着住宅和商业领域的復苏,油漆消费量也随之復苏。涂料公司对建筑涂料美好前景的信心日益增强,这可能会推动未来几年的需求。

西班牙建筑涂料产业概况。

西班牙建筑涂料市场相当集中,前五名公司占据了73.89%的市场份额。该市场的主要企业是:AkzoNobel NV、CIN、SA、DAW SE、Nippon Paint Holdings 和 PPG Industries, Inc.(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第 2 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第三章 产业主要趋势

- 占地面积趋势

- 法律规范

- 价值链与通路分析

第 4 章 市场细分

- 子终端用户

- 商业的

- 住宅

- 科技

- 溶剂型

- 水性

- 树脂

- 丙烯酸纤维

- 醇酸

- 环氧树脂

- 聚酯纤维

- 聚氨酯

- 其他树脂类型

第五章 竞争格局

- 重大策略倡议

- 市场占有率分析

- 业务状况

- 公司简介

- AkzoNobel NV

- CIN, SA

- DAW SE

- IVM Chemicals srl

- Jotun

- JUNO

- Nippon Paint Holdings Co., Ltd.

- Pinturas Decolor

- PPG Industries, Inc.

- The Barpimo Group

第六章 执行长的关键策略问题

第七章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 93080

The Spain Architectural Coatings Market size is estimated at USD 731.04 million in 2024, and is expected to reach USD 848.02 million by 2028, growing at a CAGR of 3.78% during the forecast period (2024-2028).

Key Highlights

- Largest Segment by End-user - Residential : The steady growth in the residential construction sector, accompanied by lower growth in the commercial sector, fuels the consumption in the residential segment.

- Largest Segment by Technology - Waterborne : The growing adoption of VOC regulations by architectural coating manufacturers and marketing with eco-labels help waterborne coatings gain a significant market share.

- Largest Segment by Resin - Acrylic : Acrylic is a leading type of resin due to its technological advantages, low VOC emissions in the architectural segment, and preference to coat the exterior wall of buildings.

Spain Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

- The architectural coating consumption in Spain peaked in 2017 with an increment of 7.3% Y-o-Y due to the long-time recovery since 2013 and increased rehabilitation work in 2017. However, the repaint segment, which accounts for the major part of architectural coatings, declined due to lower restoration permits in 2018 and 2019.

- The slow growth in the architectural coating consumption was observed in 2020 due to lower new constructions in both residential and commercial sectors due to the spread of COVID-19. However, the decline in new construction was countered by the growth in the do-it-yourself (DIY) segment in the residential sector in 2020.

- The coating consumption recovered in 2021 due to a rebound in both residential and commercial sectors. The growing confidence of coating companies in the positive future of architectural coatings may fuel the demand over the coming years.

Spain Architectural Coatings Industry Overview

The Spain Architectural Coatings Market is fairly consolidated, with the top five companies occupying 73.89%. The major players in this market are AkzoNobel N.V., CIN, S.A., DAW SE, Nippon Paint Holdings Co., Ltd. and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

- 4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

- 4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

- 4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles

- 5.4.1 AkzoNobel N.V.

- 5.4.2 CIN, S.A.

- 5.4.3 DAW SE

- 5.4.4 IVM Chemicals srl

- 5.4.5 Jotun

- 5.4.6 JUNO

- 5.4.7 Nippon Paint Holdings Co., Ltd.

- 5.4.8 Pinturas Decolor

- 5.4.9 PPG Industries, Inc.

- 5.4.10 The Barpimo Group

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

住宅涂料市场按产品类型、应用、最终用户、分销管道、配方和涂料类型划分-2025-2032年全球预测室内建筑涂料市场按产品类型、技术、应用、最终用途和分销管道划分-2025-2032年全球预测建筑材料翻新市场按产品类型、最终用户、应用方法和涂层技术划分-2025-2032年全球预测建筑涂料市场按产品类型、技术、树脂类型、应用方法、最终用途和分销管道划分-2025-2032 年全球预测水性建筑涂料市场按功能、产品类型、应用、分销管道和最终用途划分-2025-2032年全球预测

住宅涂料市场按产品类型、应用、最终用户、分销管道、配方和涂料类型划分-2025-2032年全球预测室内建筑涂料市场按产品类型、技术、应用、最终用途和分销管道划分-2025-2032年全球预测建筑材料翻新市场按产品类型、最终用户、应用方法和涂层技术划分-2025-2032年全球预测建筑涂料市场按产品类型、技术、树脂类型、应用方法、最终用途和分销管道划分-2025-2032 年全球预测水性建筑涂料市场按功能、产品类型、应用、分销管道和最终用途划分-2025-2032年全球预测 2025-2033年室内建筑涂料市场报告(依树脂类型、技术、配销通路、消费者类型、最终用途部门和地区)

2025-2033年室内建筑涂料市场报告(依树脂类型、技术、配销通路、消费者类型、最终用途部门和地区) 2025年全球建筑涂料市场报告

2025年全球建筑涂料市场报告 停车场涂料市场-全球产业规模、份额、趋势、机会和预测(按产品、技术、地区和竞争细分,2020-2030 年)

停车场涂料市场-全球产业规模、份额、趋势、机会和预测(按产品、技术、地区和竞争细分,2020-2030 年) 全球氧化物建筑涂料市场

全球氧化物建筑涂料市场 2024-2031年全球建筑涂料市场

2024-2031年全球建筑涂料市场

▼