|

市场调查报告书

商品编码

1683813

硬体防火墙:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Hardware Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

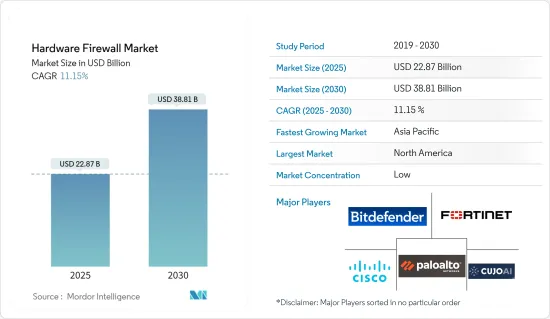

硬体防火墙市场规模预计在 2025 年为 228.7 亿美元,预计到 2030 年将达到 388.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 11.15%。

网路安全威胁增加了网路攻击危害其他组织和个人系统的风险。攻击者的动机是获取资讯以获取经济利益。此类攻击引发了人们对基础设施安全的担忧,并增加了对硬体防火墙的需求。

主要亮点

- 随着企业采用新技术并扩大其数位影响力,硬体防火墙将继续成为网路安全策略的重要组成部分。硬体防火墙市场的未来成长可能受到多种因素的推动,包括日益增加的网路安全威胁、云端基础的服务的成长、物联网的扩展以及对更复杂的安全解决方案的需求。

- 从产业来看,IT及通讯业占比较大。随着人们越来越依赖数通讯和资料传输,采用硬体防火墙的 IT 和通讯业预计未来将迎来技术进步,并更加重视安全性。

- 云端基础的防火墙解决方案的需求正在成长,尤其是在部署云端平台以确保网路安全的大型企业。在金融领域,严重的网路威胁使得网路诈骗预防和安全措施成为必要。此外,效能、威胁识别和缓解能力、云端整合、与其他安全技术的交互作用以及自动化方面的进步预计将推动硬体防火墙市场的发展。

- 云端资料外洩的增加和超越设备的 NGFW(新一代防火墙)的成长正在推动对防火墙即服务解决方案的需求,这成为市场的一个限制因素。此项服务不涉及硬件,且仅需极少的维护。与硬体防火墙不同,防火墙即服务不需要复杂的设定。硬体防火墙比软体防火墙更昂贵,因为初始投资取决于您想要的保护程度。因此,预计该因素将成为防火墙即服务服务业的成长催化剂。

- 自新冠肺炎疫情爆发以来,全球企业面临的网路攻击不断增加,导致全球对网路安全的投资不断增加。加强安全性预计将占网路IT硬体投资的很大一部分。在预测期内,防火墙等网路安全设备可能会占全球企业 IT 支出的很大一部分。

硬体防火墙市场趋势

医疗保健产业有望成为成长最快的终端用户

- 近年来,医疗保健产业已成为网路犯罪分子关注的热门话题。由于医疗保健产生的宝贵资料,医疗保健最近很容易受到网路攻击。根据 HIPAA 杂誌的报导,医疗保健组织将在 2023 年报告 725 起资料外洩事件,超过 1.33 亿笔记录「面临外洩的风险」。报告还发现,从2018年1月到2023年9月30日,医疗保健产业与骇客相关的资料外洩将呈指数级增加239%,而勒索软体攻击将在同一时期增加278%。

- 在 COVID-19 爆发后,骇客大大改进了他们的攻击策略,以利用人们日益升级的恐惧情绪,这促使人们需要采取网路安全实践来应对不断变化的威胁形势,尤其是在医疗保健领域。例如,富士通于 2023 年 3 月宣布推出一个新的云端基础的平台,使用户能够安全地收集资料,从而推动医疗保健领域的数位转型。该公司计划从2023年3月起向日本製药和医疗公司提供其新平台。该平台可自动转换医疗机构记录中的医疗资料,并使用标准框架(HL7 FHIR)对其进行规范,以确保文件安全。

- 公开呼吁世界各国政府与私营部门和学术机构合作,确保医疗机构免受网路威胁,这引发了产业合作的浪潮。例如,2023 年 10 月,网路安全与基础设施安全局 (CISA) 和卫生与公众服务部 (HHS) 宣布召开圆桌会议,讨论美国医疗保健和公共卫生 (HPH) 部门面临的网路安全挑战。他们推出了针对医疗保健和公共卫生部门的网路安全套件和资源。讨论提出了网路安全和隐私风险管理活动的提案。

- 美国联邦调查局(FBI)、信号局澳洲网路安全中心(ASD的ACSC)以及网路安全和基础设施安全局(CISA)宣布,将于 2023 年 12 月发布联合网路安全建议(CSA),作为他们持续帮助组织预防网路攻击的努力的一部分。全球登记的事故数量正在增加。例如,澳洲于 2023 年 4 月发现第一起 Play 勒索软体事件,随后在 2023 年 11 月又发现另一起事件。建议建议实施復原计划,在实体上独立的安全位置保存敏感资料的多个副本。我们还建议提供基于时间的敏感资料访问,并维护加密、不可变的离线资料备份。

- 许多组织开始意识到对其网路安全基础设施进行有计划的投资的必要性。例如,HIMSS 医疗网路安全部门进行的一项调查发现,受访者表示其医疗网路安全预算增加(约 55.31%),而其他人则表示其预算保持不变(23.46%)。

预计北美将占据较大的市场占有率

- 北美是技术最发达的地区之一。随着技术的不断应用,该地区预计将在未来几年发生重大变化。有可能改变文明的关键技术进步包括机器人技术、感测器技术、巨量资料和人工智慧,这将导致大量资料的产生,并进一步要求加强资料安全性。

- 近年来,随着组织和个人面临的网路威胁和攻击的总数急剧增加,网路安全已成为美国越来越重要的领域。根据身分盗窃资源中心的数据,2023 年,美国资料外洩事件总数约为 3,205 起。同时,到2023年,将有超过3.53亿个人受到资料外洩的严重影响,包括洩密、资料外洩和暴露。

- 市场正在见证主要企业的合併、收购和投资,这是他们改善业务、接触客户和扩大影响力以满足各种应用需求的策略的一部分。政府已经采取重要倡议保护国家免受网路攻击。

- 例如,2023年3月,白宫发布了《国家网路安全战略》,为更安全的电脑网路空间树立了积极的愿景,为实现我们的共同愿望创造了机会。国家网路安全战略要求实现两个重要的根本性转变:重新调整奖励以支持长期投资,并平衡保卫电脑网路空间的责任。

- 因此,预计在整个预测期内,增加包括网路安全相关的併购、投资和政府倡议在内的市场活动将推动该地区对网路安全解决方案的需求。

硬体防火墙产业概览

硬体防火墙市场较为分散,主要参与者包括 Bitdefender、思科系统公司、Cujo LLC、Fortinet 公司和 Palo Alto Networks 公司。市场上的公司正在采用联盟和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2024年6月,印度IT和顾问公司Tech Mahindra加强了与美国主要通讯设备製造商思科的合作关係。两家公司共同致力于为全球客户提供领先的新一代防火墙 (NGFW) 现代化解决方案。此次合作将透过跨内部和云端环境的统一策略管理等功能增强防火墙的功能。此外,透过整合思科的 Talos 威胁情报,它为网路和端点提供了强大的恶意软体防护。

- 2024 年 4 月:IBM Cloud 和 Fortinet 透过在 IBM Cloud 上推出 Fortinet 虚拟 FortiGate 安全设备 (vFSA) 加强了伙伴关係。 Fortinet 的新解决方案将 FortiGate 硬体防火墙的强大功能与虚拟设备的灵活性相结合。 vFSA 为客户提供 IBM Cloud 基础架构中 FortiGate 新一代防火墙 (NGFW) 的进阶安全功能。此措施旨在保护客户网路并确保持续的高可用性,特别是处理敏感资料的网路。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 防火墙市场主要区域供应商及生产基地覆盖情况

- 涵盖供应侧动态

- 通讯业者案例研究

- 本机防火墙与虚拟防火墙

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- 疫情后防火墙需求覆盖范围

第五章 市场动态

- 市场驱动因素

- 政府监理推动网路安全应用防火墙

- 针对关键基础设施的攻击日益复杂

- 市场限制

- 大量资本投入和防火墙即服务的日益普及

- 硬体防火墙价格趋势分析

- 硬体防火墙 - 技术蓝图

- 防火墙类型分析

- 封包过滤防火墙

- 电路级网关

- 应用层级网关

- UTM 防火墙

第六章 市场细分

- 按组件

- 设备/系统

- 服务(实施服务)

- 按组织规模

- 中小型企业

- 大型企业

- 按最终用户产业

- 卫生保健

- 製造业

- 政府

- 资讯科技和电讯

- 教育

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 马来西亚

- 泰国

- 越南

- 新加坡

- 菲律宾

- 印尼

- 中东和非洲

- 拉丁美洲

第七章 竞争格局

- 公司简介

- Bitdefender

- Cisco Systems Inc.

- CUJO LLC

- Fortinet Inc.

- Palo Alto Networks Inc.

- Netgate

- Sonicwall Inc.

- Sophos Ltd

- WatchGuard Technologies Inc.

- Check Point Software Technologies Ltd

8.供应商市场占有率分析

第九章投资分析

The Hardware Firewall Market size is estimated at USD 22.87 billion in 2025, and is expected to reach USD 38.81 billion by 2030, at a CAGR of 11.15% during the forecast period (2025-2030).

Cybersecurity threats increase the risk of cyberattacks, which can breach the systems of another organization or an individual. The attacker's motives are to access information for financial gain. Such attacks raise concerns about infrastructure safety, increasing the demand for hardware firewalls.

Key Highlights

- Hardware firewalls are anticipated to remain an important component of enterprises' and organizations' cybersecurity strategies as they adopt newer technologies and extend their digital presence. The future growth of the hardware firewall market will most likely be driven by various factors, such as increased network security threats, the growth of cloud-based services, the expansion of IoT, and the demand for more sophisticated security solutions.

- The IT and telecom segment held a substantial market share by industry. Due to the increasing reliance on digital communication and data transmission, the future of IT and telecom employing hardware firewalls is expected to witness technological advancements and a greater emphasis on security.

- The demand for cloud-based firewall solutions is rising, especially in large organizations that deploy cloud platforms for network security. The financial sectors experience a need for cyber fraud prevention and security measures due to significant cyber threats. Additionally, advancements in performance, threat identification and mitigation capabilities, cloud integration, interaction with other security technologies, and automation are projected to drive the hardware firewall market.

- Increased cloud data breaches and the growth of NGFW (next-generation firewall) across devices are boosting the demand for firewalls as service solutions, which act as a market constraint. Since there is no hardware involved in this service, maintenance is quick. Unlike a hardware-powered firewall, a firewall as a service does not require complex configuration. A hardware firewall is more expensive than a software firewall since an initial investment depends on the degree of protection. As a result, this factor is expected to act as a growth catalyst for the firewalls-as-a-service industry.

- Post the COVID-19 pandemic, global enterprises have been facing an increasing number of attacks on their networks, leading to an increase in investments in safeguarding networks worldwide. A significant share of the IT hardware investment in the network is expected to be focused on enhancing security. Over the forecast period, network security equipment like firewalls may become a key part of enterprise IT spending worldwide.

Hardware Firewall Market Trends

Healthcare Industry is Expected to be the Fastest-growing End User

- Over the past few years, the healthcare industry has become a target of significant interest among cybercriminals. Due to its generation of valuable data, healthcare has recently become vulnerable to cyber-attacks. As per a HIPAA Journal report, healthcare institutions reported 725 data breaches, of which more than 133 million records were under 'exposed risk' in 2023. The report also stated that the healthcare industry reported a 239% exponential rise in hacking-related data breaches from January 2018 to September 30, 2023, and a 278% rise in ransomware attacks during the same period.

- Post the COVID-19 outbreak, hackers vastly evolved their tactics to exploit the fears escalating among the population, spurring the need to adopt cybersecurity practices to keep pace with changing threats, especially in healthcare. For instance, in March 2023, Fujitsu announced the launch of a new cloud-based platform that allowed users to collect data safely to promote digital transformation in the healthcare domain. The company planned to offer a new platform to pharmaceutical and medical companies in Japan starting in March 2023. The platform ensures the automatic conversion of medical data from the medical records of medical institutions to regulate with the standards framework (HL7 FHIR) and ensure the safety of documents.

- Various collaborations have been taking place in the industry following a public call asking governments worldwide to join forces with the private sector and academia to ensure that medical facilities are protected from cyber threats. For instance, in October 2023, the Cybersecurity and Infrastructure Security Agency (CISA) and the Department of Health and Human Services (HHS) announced a roundtable regarding the cybersecurity challenges that the US healthcare and public health (HPH) sector experiences. They released a cybersecurity toolkit and customized resources for the healthcare and public health sectors. This discussion provided suggestions around cybersecurity and privacy risk management activities.

- As part of their ongoing efforts to help organizations prevent cyberattacks, the US Federal Bureau of Investigation (FBI), the Signals Directorate's Australian Cyber Security Centre (ASD's ACSC), and the Cybersecurity and Infrastructure Security Agency (CISA) announced a collaboration to release the joint Cybersecurity Advisory (CSA) in December 2023. A growing number of incidents are being registered across the world. For instance, the first Play ransomware incident in Australia was observed in April 2023 and then in November 2023. The advisory recommended executing a recovery plan to maintain the multiple copies of sensitive data in a physical, separate, and secure location. It also suggested having time-based access to highly sensitive data and maintaining offline data backup that is encrypted and immutable.

- Many organizations are becoming more aware of planned investments in cybersecurity infrastructure. For instance, as per a survey conducted by the HIMSS Healthcare Cybersecurity, respondents suggested an increase in healthcare cybersecurity budgets (by around 55.31%), while other respondents suggested their budgets stayed the same (23.46%).

North America is Expected to Hold a Major Market Share

- North America is one of the most technologically developed regions. The growing adoption of technology is expected to result in important changes in the region in the coming years. Some key technological advancements that have the prime potential to alter civilization include robotics, sensor technology, Big Data, and artificial intelligence, resulting in a vast amount of data generation that further needs enhanced data security.

- In recent years, cybersecurity has become an increasingly important area of focus in the United States due to a surge in the total count of cyber threats and attacks faced by organizations and individuals. As per the Identity Theft Resource Center, in 2023, the total number of data compromises in the United States stood at around 3,205 cases. Meanwhile, in 2023, over 353 million individuals were greatly affected by data compromises, including leakage, data breaches, and exposure.

- The market is witnessing mergers, acquisitions, and investments by key players as part of their strategies to improve businesses and their presence to reach customers and meet their requirements for various applications. The government has taken significant initiatives to secure the country against cyberattacks.

- For instance, in March 2023, the White House released its National Cybersecurity Strategy to establish an affirmative vision for a more secure cyberspace that creates opportunities to achieve collective aspirations. The National Cybersecurity Strategy calls for two key fundamental shifts: realigning incentives to favor long-term investments and rebalancing the responsibility to defend cyberspace.

- Thus, a rise in such market activities involving mergers, acquisitions, investments, and government initiatives related to cybersecurity is anticipated to drive the demand for network security solutions within the region throughout the forecast period.

Hardware Firewall Industry Overview

The hardware firewall market is fragmented with the presence of major players like Bitdefender, Cisco Systems Inc., Cujo LLC, Fortinet Inc., and Palo Alto Networks Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- June 2024: Tech Mahindra, an Indian IT and consulting firm, strengthened its partnership with US telecom equipment leader Cisco. Together, they aim to deliver advanced next-generation firewall (NGFW) modernization solutions to their global customer base. This collaboration enhances firewall functionalities with features such as unified policy management across both on-premises and cloud environments. Additionally, it incorporates Cisco's Talos threat intelligence, providing robust malware defense for networks and endpoints.

- April 2024: IBM Cloud and Fortinet strengthened their partnership by launching the Fortinet Virtual FortiGate Security Appliance (vFSA) on IBM Cloud. This new solution from Fortinet combines the powerful features of its FortiGate hardware firewall with the flexibility of virtual appliances. The vFSA provides clients with the advanced security capabilities of FortiGate's next-generation firewall (NGFW) within the IBM Cloud infrastructure. This initiative aims to protect clients' networks, particularly those handling sensitive data, ensuring their continuous high availability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Coverage of the Major Regional Vendors and Production Locations in the Firewall Market

- 4.3 Coverage of Supply-side Dynamics

- 4.4 Case Studies of Telcos

- 4.5 Coverage of Native vs Virtual Firewalls

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value Chain Analysis

- 4.8 Coverage of Firewall Demand in the Post-Pandemic Scenario

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Administrative Regulations Encouraging Network Security Application Firewall

- 5.1.2 Rising Sophistication of Attacks on Critical Infrastructure

- 5.2 Market Restraints

- 5.2.1 Heavy Capital Expenditure and Rising Adoption of Firewall-as-a-Service

- 5.3 Hardware Firewall Price Trend Analysis

- 5.4 Hardware Firewall - Technology Roadmap

- 5.5 Analysis of Types of Firewalls

- 5.5.1 Packet Filtering Firewalls

- 5.5.2 Circuit-level Gateways

- 5.5.3 Application-level Gateways

- 5.5.4 UTM Firewalls

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Device/System

- 6.1.2 Services (Installation Services)

- 6.2 By Organization Size

- 6.2.1 SMEs

- 6.2.2 Large Enterprises

- 6.3 By End-user Industry

- 6.3.1 Healthcare

- 6.3.2 Manufacturing

- 6.3.3 Government

- 6.3.4 IT and Telecom

- 6.3.5 Education

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Malaysia

- 6.4.3.5 Thailand

- 6.4.3.6 Vietnam

- 6.4.3.7 Singapore

- 6.4.3.8 Philippines

- 6.4.3.9 Indonesia

- 6.4.4 Middle East and Africa

- 6.4.5 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bitdefender

- 7.1.2 Cisco Systems Inc.

- 7.1.3 CUJO LLC

- 7.1.4 Fortinet Inc.

- 7.1.5 Palo Alto Networks Inc.

- 7.1.6 Netgate

- 7.1.7 Sonicwall Inc.

- 7.1.8 Sophos Ltd

- 7.1.9 WatchGuard Technologies Inc.

- 7.1.10 Check Point Software Technologies Ltd

8 VENDOR MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

企业防火墙硬体市场 - 全球产业规模、份额、趋势、机会和预测(按部署类型、组织、最终用户、地区和竞争格局划分,2020-2030 年预测)企业防火墙软体市场 - 全球产业规模、份额、趋势、机会和预测(按部署类型、组织、最终用户、地区和竞争对手划分,2020-2030 年预测)智慧防火墙市场 - 全球产业规模、份额、趋势、机会和预测,按组件、业务功能、应用、组织规模、地区和竞争格局划分,2020-2030 年预测

企业防火墙硬体市场 - 全球产业规模、份额、趋势、机会和预测(按部署类型、组织、最终用户、地区和竞争格局划分,2020-2030 年预测)企业防火墙软体市场 - 全球产业规模、份额、趋势、机会和预测(按部署类型、组织、最终用户、地区和竞争对手划分,2020-2030 年预测)智慧防火墙市场 - 全球产业规模、份额、趋势、机会和预测,按组件、业务功能、应用、组织规模、地区和竞争格局划分,2020-2030 年预测 企业防火墙市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、部署、最终用户、功能及解决方案

企业防火墙市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、部署、最终用户、功能及解决方案 SMS 防火墙市场(按组件、部署类型、组织规模和最终用户)- 全球预测,2025 年至 2032 年企业网路防火墙市场(按组件、部署类型、公司规模和垂直行业)—2025-2032 年全球预测

SMS 防火墙市场(按组件、部署类型、组织规模和最终用户)- 全球预测,2025 年至 2032 年企业网路防火墙市场(按组件、部署类型、公司规模和垂直行业)—2025-2032 年全球预测 2025年全球企业防火墙市场报告2025年新一代防火墙全球市场报告工业防火墙市场:依防火墙类型、层级保护、部署、应用、垂直领域和组织规模划分 - 2025-2030 年全球预测新一代防火墙市场:按组件、部署类型、功能、组织规模、垂直行业和销售管道- 全球预测 2025-2030

2025年全球企业防火墙市场报告2025年新一代防火墙全球市场报告工业防火墙市场:依防火墙类型、层级保护、部署、应用、垂直领域和组织规模划分 - 2025-2030 年全球预测新一代防火墙市场:按组件、部署类型、功能、组织规模、垂直行业和销售管道- 全球预测 2025-2030