|

市场调查报告书

商品编码

1683827

非洲塑胶包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Africa Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

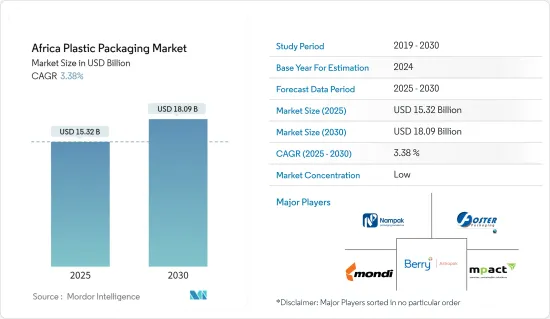

预计 2025 年非洲塑胶包装市场规模为 153.2 亿美元,到 2030 年将达到 180.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.38%。

近年来,非洲人口成长和都市化进程快速推进。随着人口的增长和越来越多的人迁入城市,对包装商品的需求也随之增加,从而产生了对塑胶包装产品的需求。此外,经济成长扩大了该地区各国的中产阶级,增加了各国的可支配收入。随着人们购买力的增强,对包装商品的需求也随之增加,推动了塑胶包装产业的成长。

主要亮点

- 该地区的许多国家都注重工业化和製造业来发展经济,其中包括为食品、食品和饮料、製药和个人保健产品等各个行业设立工厂。塑胶包装是这些行业的多功能且便捷的解决方案,从而导致该地区其需求持续增长。

- 随着人口的成长,非洲国家对食品和饮料的需求不断增加。根据世界银行估计,到 2030 年,非洲食品产业总价值可能成长到 1 兆美元(约 8,415 亿欧元)。

- 由于监管标准的动态变化,市场预计将面临严峻挑战,这主要是由于人们对环境问题的日益关注。该地区各国政府正在回应公众对塑胶包装废弃物的担忧,并实施法规以减少环境废弃物并改善废弃物管理流程。

- 由于产品需求不断增长,国际食品製造公司正在非洲扩大业务。 2022 年 10 月,饼干製造商 Britannia Industries Ltd 签署了在肯亚运营的协议,作为其非洲扩张计画的一部分。

- 预计市场将面临挑战,主要原因是由于环境问题日益严重导致监管标准动态变化。该地区各国政府正在回应公众对塑胶包装废弃物的担忧,并实施法规以减少环境废弃物并改善废弃物管理流程。

非洲塑胶包装市场的趋势

食品业占据硬质和软质塑胶包装市场的大部分份额

- 塑胶食品储存容器透过提供有效的密封,有助于在储存期间保存和保持食物新鲜。这些容器适合在咖啡馆、杂货店或任何食品企业使用。包装是西非的一个重要市场。此次区域工业的发展主要是为了回应农业和食品工业的成长。尼日利亚、南非和肯亚占据该地区塑胶包装市场的很大份额。

- 预计到 2050 年,东部和南部非洲的食品产业将成长 800%,加工食品贸易将成长高达 90%。预计到 2030 年,整个非洲的食品产业规模将达到 1 兆美元,都市区消费将推动更多产品的需求。食品包装是非洲最重要的终端用户塑胶产业之一。硬质塑胶包装在食品业中正日益普及。工业界因为它重量轻、节省成本而被广泛使用。

- 硬质塑胶和一次性容器对于外带、食品连锁店和餐厅来说是必不可少的。但全部区域都存在着环境问题。由于全部区域开设了多家食品连锁店,非洲对塑胶包装的需求激增。 2022 年 5 月,总部位于杜拜的清真速食连锁店 ChicKing 宣布计划未来五年在肯亚开设 30 家门市。

- 典型的柔性食品包装应用包括用于包装起司、肉类、麵包和蔬菜等食品的薄膜和袋子。大多数情况下,软包装被用作初级包装,但在某些情况下也可能被用作二次包装。

- 这些薄膜有贴合加工和无层压型两种,可以耐受冷冻库等恶劣环境。它的抗衝击强度、抗撕裂强度、抗屈挠开裂性能和优异的密封性能使其广泛应用于食品应用。这些因素正在推动非洲软包装市场的发展。

- 随着非洲都市化不断加快,越来越多的人居住在城市,获得新鲜农产品的机会也越来越少。此外,消费者越来越关注永续性,导致包装采用更易于回收的再生材料製成,从而支持了对软包装的需求。

南非占据主要市场占有率

- 盒装午餐的日益普及、餐厅和超级市场数量的不断增加以及瓶装水和饮料的消费量的不断增长都是推动该国市场扩张的主要因素。

- 近年来,随着人们越来越追求更健康的生活方式,南非家庭护理产品市场经历了长足的成长。这增加了对饮料瓶、洗漱用品瓶和塑胶袋等产品的需求,从而促进了该地区塑胶包装市场的成长。

- 由于该国的塑胶垃圾数量庞大,政府措施和强大的消费者意识正在帮助推动回收趋势以健康的速度向前发展。此外,南非可口可乐等公司收集和回收的 PET 比当地生产的还要多。

- 在需求方面,随着行动连线的改善,南非消费者正在转向电子商务。由于新冠疫情以及该国对非接触式交易的兴趣日益浓厚,这一趋势进一步加速。这使得一些市场收购得以实现。例如,2021年7月,奥地利塑胶包装公司ALPLA集团收购了南非包装製造商Verigreen Packaging,以扩大在南部非洲的业务。

- 总体来看,儘管受到外部经济变数的影响,但该国饮料消费量仍在快速成长。由于气候条件的影响,该国的软性饮料消费量正在增加,人们饮用碳酸饮料的次数也越来越多。过去两年的严重缺水也导致瓶装水使用量急剧增加。 宝特瓶已成为市场主流, 宝特瓶的需求量也不断增加。因此,这些因素正在推动该国塑胶包装市场的成长。

非洲塑胶包装产业概况

非洲的塑胶包装市场高度分散,由 Mondi、Nampak 和 Very Astrapak 等市场现有企业以及几家区域包装公司组成。随着全球对环境问题的关注度日益提高,各大公司都在加大研发投入,以解决环境问题,让塑胶瓶更加安全。

- 2023 年 1 月,Phatisa 宣布收购 MHL International Holdings 的大量少数股权,该公司透过位于肯亚和奈及利亚的子公司在撒哈拉以南非洲地区开展印刷和包装业务,并且在食品和饮料领域拥有强大的影响力。

- 2022年8月,Alpura扩大了其OTC包装製造技术。 ALPLA 集团旗下的医药包装业务 Alplapharma 已扩展其 OTC 瓶製造能力,包括灵活的挤出吹塑成型(EBM),从而为该领域提供永续的、针对客户的包装解决方案。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 生态系分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 预计宝特瓶需求的增加将推动该地区对硬质包装的需求

- 未来几年饮料包装可望受到青睐

- 市场挑战

- 原物料价格波动

- 新冠疫情与近期地缘政治变化对非洲包装产业成长的影响

- 非洲主要新兴市场分析

- 根据相关 HS 编码分析非洲主要原料进口

- 塑胶包装市场的技术创新

- 包装产业广泛的投资报酬率指标分析

第六章 市场细分

- 硬包装

- 材料

- 聚乙烯 (PE)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 聚苯乙烯 (PS) 和发泡聚苯乙烯 (EPS)

- 聚氯乙烯(PVC)

- 其他材料

- 最终用户

- 食物

- 饮料

- 医疗保健和医药

- 个人护理和化妆品

- 其他最终用户

- 材料

- 软包装

- 材料

- 聚乙烯 (PE)

- 双轴延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 聚氯乙烯(PVC)

- 乙烯 - 乙烯醇(EVOH)

- 其他材料

- 最终用户

- 食物

- 饮料

- 个人护理和化妆品

- 其他最终用户

- 材料

- 国家

- 南非

- 奈及利亚

- 埃及

- 肯亚

- 摩洛哥

- 迦纳

- 衣索比亚

- 坦尚尼亚

- 尚比亚

第七章 竞争格局

- 公司简介

- Berry Astrapak(Berry Global Group Inc.)

- Nampak Ltd

- Mondi PLC

- Mpact Pty Ltd

- Foster International Packaging

- Constantia Flexibles

- Tetra Pak SA

- Amcor PLC

- LIQUIBOX(Sealed Air Corporation)

- Sonoco Products Company

- Toppan Inc.

- Huhtamaki Oyj

- ALPLA Group

- Plastipak Holdings Inc.

- Polyoak Packaging

第 8 章:非洲主要供应商(按国家/地区)列表

- 南非

- 奈及利亚

- 埃及

- 肯亚

- 摩洛哥

- 迦纳

- 衣索比亚

- 坦尚尼亚

- 尚比亚

第九章:未来市场展望

第十章 投资分析

The Africa Plastic Packaging Market size is estimated at USD 15.32 billion in 2025, and is expected to reach USD 18.09 billion by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

Africa has experienced rapid population growth and urbanization in recent years. As the population increases and more people move to cities, there is a rising demand for packaged goods, creating the need for plastic packaging products. Furthermore, economic growth resulted in an expansion of the middle class and increased disposable income in various countries of the region. As purchasing power of people increases, the demand for packaged goods also rises, driving the growth of the plastic packaging industry.

Key Highlights

- Many countries in the region are focusing on industrialization and manufacturing for their economic development, which includes the establishment of factories for various industries, such as food, beverage, pharmaceuticals, personal care products, and more. As plastic packaging is a convenient solution for these industries in multiple applications, its demand is growing continuously in the region.

- With a growing population, demand for food and beverages is continuously increasing in the countries of Africa. According to World Bank, the total value of the African food industry could rise to USD one trillion (approx. EUR 841.5 billion) by 2030.

- The market is expected to be challenged owing to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments across the region have been responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

- International food manufacturing companies are expanding their operations in Africa due to rising product demand. In October 2022, cookie manufacturer Britannia Industries Ltd finalized a deal for operations in Kenya as part of its plan to expand in Africa.

- The market is expected to be challenged owing to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments across the region have been responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

Africa Plastic Packaging Market Trends

Food Industry to Hold Major Share in Both Rigid and Flexible Plastic Packaging Markets

- Plastic food storage containers help preserve food during storage or keep them fresh by effective sealing. These containers are suitable for use in cafes, grocery shops, or any food business. Packaging is an important market in West Africa. This industry has developed in the sub-region largely in response to farming and the growth of the food industry. Nigeria, South Africa, and Kenya have a substantial share of the plastic packaging market in the region.

- The food sector in Eastern and Southern Africa is expected to grow by 800% by 2050, with trade in processed foods increasing by up to 90%. Africa as a whole is anticipated to be a USD 1 trillion food industry by 2030, with urban consumption driving demand for more products. Food packaging is one of Africa's most significant end-user plastic industries. Rigid plastic packaging is increasing in the food industry. The industry uses it for its properties, such as lightweight and reduced cost.

- Rigid plastic and disposable containers are integral to takeouts, food chains, and restaurants. However, there are environmental concerns across the region. The opening of several food chains across the region has spiked the demand for plastic packaging in Africa. In May 2022, the Dubai-based halal fast-food chain ChicKing announced its intentions to open 30 outlets in Kenya over the next five years.

- Typical flexible food packaging applications include films and pouches to package food products like cheeses, meats, bread, and vegetables, among others. In most cases, flexible packaging is used as the primary packaging, but it can also be used as the secondary packaging in some cases.

- These films can be laminated or nonlaminated and withstand harsh environments like freezers. Their impact strength, tear strength, flex-crack resistance, and excellent sealing properties are extensively used in food applications. Such factors are driving the flexible packaging market in the country.

- Due to increasing urbanization in Africa, more people are living in cities and having less access to fresh produce, which is driving the demand for flexible packaging. Additionally, the growing focus of consumers toward sustainability is leading to packaging made from recycled materials that can be easily recycled, hence supporting the demand for flexible packaging.

South Africa to Hold Significant Market Share

- The rising popularity of packed meals, the expanding number of restaurants and supermarkets, and rising bottled water and beverage consumption are all key drivers of the country's market expansion.

- The South African home care products market has seen considerable growth in recent years owing to a growing trend among individuals to maintain a healthier lifestyle. This has driven demand for products like beverage bottles, toiletry bottles, plastic bags, and others, thereby increasing the growth of the region's plastic packaging market.

- With the country's enormous volume of plastic garbage, the recycling trend is expanding at a healthy rate, owing to government restrictions and strong consumer awareness. Moreover, companies like Coca-Cola in South Africa collected and recycled more PET than was produced within the country.

- On the demand side, customers in South Africa are migrating to e-commerce as mobile connectivity develops. This tendency has accelerated as a result of the COVID-19 pandemic as well as a spike in interest in contactless transactions inside the country. This has permitted several market acquisitions. For instance, in July 2021, Austrian plastic packaging firm ALPLA Group purchased South African packaging producer Verigreen Packaging to extend its footprint in southern Africa.

- Overall, beverage consumption in the country is increasing rapidly, despite the impact of external economic variables. Soft drink consumption is increasing in the country as a result of climatic conditions, with people drinking more carbonated beverages. Due to severe water scarcity in the country over the previous two years, the usage of bottled water has also increased dramatically. With PET bottles becoming the market norm, the demand for plastic bottles has also increased. Therefore, these factors are driving the growth of the plastic packaging market in the country.

Africa Plastic Packaging Industry Overview

The African plastic packaging market is highly fragmented, comprising market incumbents such as Mondi, Nampak, and Berry Astrapak and several regional packaging firms. With environmental concerns rising across countries, major players have boosted their investments in research and development to tackle environmental concerns and make plastic bottles safer.

- In January 2023, Phatisa announced the acquisition of a significant minority stake in MHL International Holdings, a printing and packaging provider operating in Sub-Saharan Africa through subsidiaries in Kenya and Nigeria with strong exposure to the food and beverage sector.

- In August 2022, ALPLA expanded its OTC packaging manufacturing technology. Alplapharma, the pharma packaging business of the ALPLA group, accomplished this by expanding its manufacturing technology for OTC bottles with the inclusion of flexible extrusion blow molding (EBM), which allows for sustainable and customer-specific packaging solutions in this field.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Pet Bottles is Expected to Drive the Need for Rigid Packaging in the Region

- 5.1.2 Beverage Packaging is Expected to Gain Traction over the Coming Years

- 5.2 Market Challenges

- 5.2.1 Fluctuating Raw Material Prices

- 5.3 Impact of COVID -19 and the Recent Geopolitical Changes on the Growth of the African Packaging Industry

- 5.4 Analysis of the Key Emerging Markets in Africa

- 5.5 Analysis of the Key Raw Material Imports into Africa Based on Relevant HS Codes

- 5.6 Technological Innovations in the Plastic Packaging Market

- 5.7 Analysis of the Broader ROI Measures within the Packaging Industry

6 MARKET SEGMENTATION

- 6.1 Rigid Packaging

- 6.1.1 Material

- 6.1.1.1 Polyethylene (PE)

- 6.1.1.2 Polyethylene Terephthalate (PET)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.1.1.5 Polyvinyl Chloride (PVC)

- 6.1.1.6 Other Materials

- 6.1.2 End User

- 6.1.2.1 Food

- 6.1.2.2 Beverage

- 6.1.2.3 Healthcare and Pharmaceutical

- 6.1.2.4 Personal Care and Cosmetics

- 6.1.2.5 Other End Users

- 6.1.1 Material

- 6.2 Flexible Packaging

- 6.2.1 Material

- 6.2.1.1 Polyethylene (PE)

- 6.2.1.2 Bi-orientated Polypropylene (BOPP)

- 6.2.1.3 Cast Polypropylene (CPP)

- 6.2.1.4 Polyvinyl Chloride (PVC)

- 6.2.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.2.1.6 Other Materials

- 6.2.2 End User

- 6.2.2.1 Food

- 6.2.2.2 Beverage

- 6.2.2.3 Personal Care and Cosmetics

- 6.2.2.4 Other End Users

- 6.2.1 Material

- 6.3 Country

- 6.3.1 South Africa

- 6.3.2 Nigeria

- 6.3.3 Egypt

- 6.3.4 Kenya

- 6.3.5 Morocco

- 6.3.6 Ghana

- 6.3.7 Ethiopia

- 6.3.8 Tanzania

- 6.3.9 Zambia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berry Astrapak (Berry Global Group Inc.)

- 7.1.2 Nampak Ltd

- 7.1.3 Mondi PLC

- 7.1.4 Mpact Pty Ltd

- 7.1.5 Foster International Packaging

- 7.1.6 Constantia Flexibles

- 7.1.7 Tetra Pak SA

- 7.1.8 Amcor PLC

- 7.1.9 LIQUIBOX (Sealed Air Corporation)

- 7.1.10 Sonoco Products Company

- 7.1.11 Toppan Inc.

- 7.1.12 Huhtamaki Oyj

- 7.1.13 ALPLA Group

- 7.1.14 Plastipak Holdings Inc.

- 7.1.15 Polyoak Packaging

8 LIST OF KEY VENDORS IN AFRICA BY COUNTRY

- 8.1 South Africa

- 8.2 Nigeria

- 8.3 Egypt

- 8.4 Kenya

- 8.5 Morocco

- 8.6 Ghana

- 8.7 Ethiopia

- 8.8 Tanzania

- 8.9 Zambia

9 FUTURE OUTLOOK OF THE MARKET

10 INVESTMENT ANALYSIS

塑胶包装市场预测至2032年:按聚合物类型、包装类型、製造流程、销售管道、应用和地区进行的全球分析

塑胶包装市场预测至2032年:按聚合物类型、包装类型、製造流程、销售管道、应用和地区进行的全球分析 全球塑胶包装市场预测(2025-2032 年),按包装类型、包装材料、最终用途产业、製造技术和包装形式划分

全球塑胶包装市场预测(2025-2032 年),按包装类型、包装材料、最终用途产业、製造技术和包装形式划分 2025年PCR塑胶包装全球市场报告2025年全球塑胶瓦楞包装市场报告2025年塑胶替代包装全球市场报告2025年软质塑胶包装全球市场报告PCR塑胶包装市场预测至2032年:按包装类型、材料类型、回收流程、技术、最终用户和地区进行的全球分析全球鬆散填充包装市场:预测至 2032 年—按产品类型、材料类型、分销管道、应用、最终用户和地区进行分析2025年硬质热成型塑胶包装全球市场报告2032 年塑胶防水布市场预测:按产品、材料、厚度、结构、最终用户和地区进行的全球分析

2025年PCR塑胶包装全球市场报告2025年全球塑胶瓦楞包装市场报告2025年塑胶替代包装全球市场报告2025年软质塑胶包装全球市场报告PCR塑胶包装市场预测至2032年:按包装类型、材料类型、回收流程、技术、最终用户和地区进行的全球分析全球鬆散填充包装市场:预测至 2032 年—按产品类型、材料类型、分销管道、应用、最终用户和地区进行分析2025年硬质热成型塑胶包装全球市场报告2032 年塑胶防水布市场预测:按产品、材料、厚度、结构、最终用户和地区进行的全球分析